Online Medical Education Market Size 2024-2028

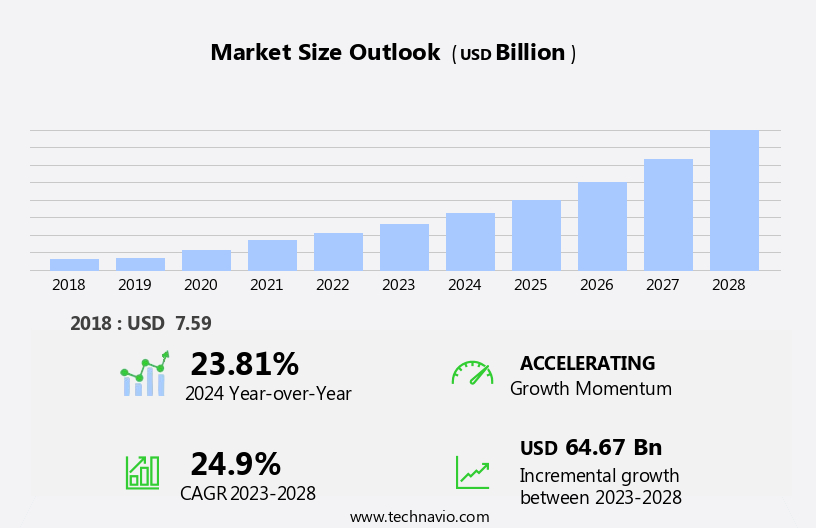

The online medical education market size is forecast to increase by USD 64.67 billion at a CAGR of 24.9% between 2023 and 2028.

- The online medical education market is experiencing substantial growth, largely driven by the increasing adoption of online education globally. As more students and professionals seek flexible and accessible learning opportunities, online platforms are becoming a vital resource for medical education. The growth is further supported by the increasing adoption of e-learning platforms globally.

- Within this market, the institutional segment is expected to see significant growth during the forecast period. Educational institutions are increasingly integrating online medical courses to enhance their curriculum, making advanced medical training more accessible to a broader audience. This trend is expected to continue, as institutions recognize the potential of online education in improving learning outcomes and expanding access to quality medical education worldwide.

- Another key factor fueling market growth is the integration of advanced simulation technologies in online medical courses, providing students with realistic and immersive learning experiences through virtual reality.

What will be the Size of the Online Medical Education Market During the Forecast Period?

- The market encompasses various forms of online education, including correspondence courses, open online courses, synchronous distance education, and tele-learning. These platforms offer students interactive learning experiences through virtual patient rooms, message boards, chats, and transactional e-mail. Medical schools increasingly employ tele-learning platforms to deliver e-learning materials, enabling continuous education (CE) for students and professionals.

How is this Online Medical Education Industry segmented and which is the largest segment?

The online medical education industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Institutional

- Individual

- Type

- Graduation courses

- Post graduate courses

- Certifications and trainings

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

By End-user Insights

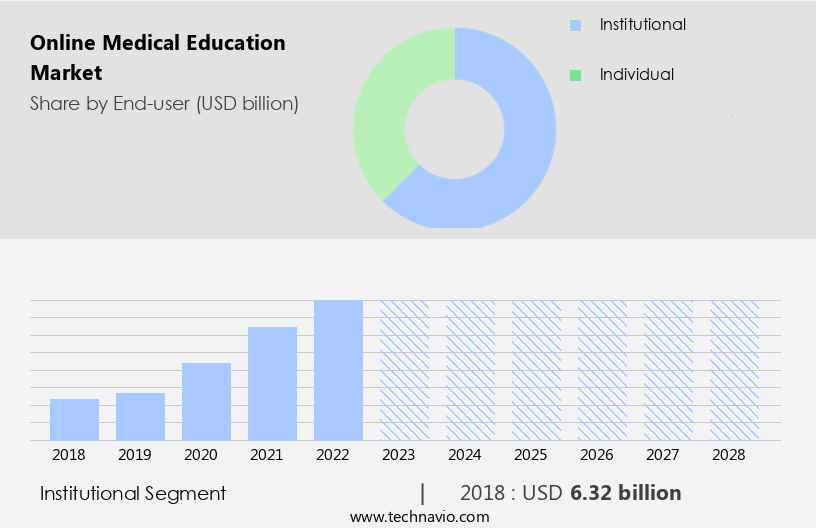

- The institutional segment is estimated to witness significant growth during the forecast period.

Online medical education offers convenient access to comprehensive resources for individuals seeking medical knowledge, enabling them to engage in medical training courses from anywhere, at any time. This includes access to course content, lectures, online tutoring, and study materials through advanced training facilities and e-learning platforms. Medical students and working professionals, regardless of their geographical location, can enroll in medical education without the need for relocation or attendance at traditional institutions. Online medical education is cost-effective, eliminating expenses related to commuting, accommodation, and campus fees. Many online courses and resources are affordably priced, making medical education accessible to individuals with limited financial resources.

Accreditation systems ensure the quality and validity of online medical education, while education apps allow for learning on-the-go. Continuous education (CE) opportunities enable medical professionals to maintain their certifications and stay updated with the latest medical advancements. Online medical education provides a flexible, cost-effective, and accessible alternative to traditional medical education.

Get a glance at the Online Medical Education Industry report of share of various segments Request Free Sample

The Institutional segment was valued at USD 6.32 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

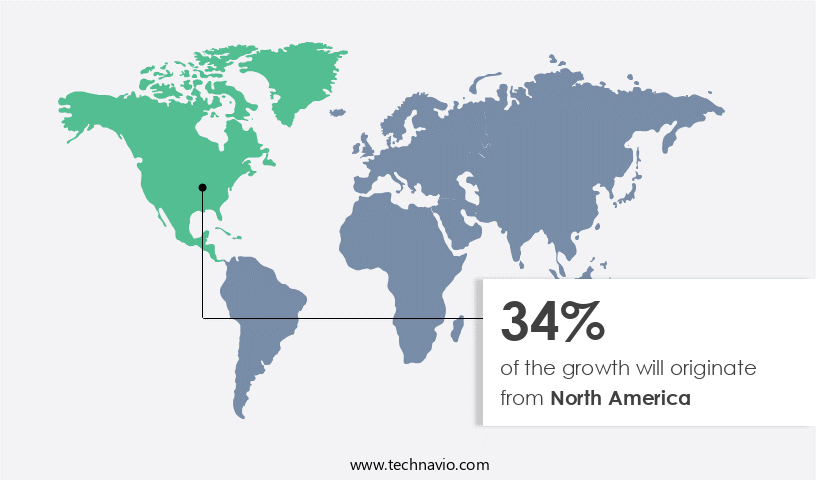

- North America is estimated to contribute 34% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America, specifically in the US and Canada, is experiencing significant growth due to the advantages it offers over traditional offline education. These advantages include ease of accessibility, flexibility in terms of time and location, and affordability. Online medical courses are often less expensive than traditional degrees, eliminating the need for additional expenses such as on-campus housing and meals. Online medical education encompasses various formats, including correspondence courses, open online courses, tele-learning, virtual patient rooms, and e-learning. Synchronous distance education, message boards, chats, e-mail, and teleconferencing facilitate interactive learning experiences. Online medical education provides a cost-effective solution for students seeking quality education in the medical field.

Market Dynamics

Virtual patient simulation and live events provide immersive educational experiences, while textual content, audio, and video on mobile platforms expand accessibility. Electronic media facilitates flexible, self-paced learning, making online medical education an essential component of modern healthcare education. Teachers leverage these tools to deliver engaging, high-quality instruction, ensuring students receive a comprehensive medical education.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Online Medical Education Industry?

Increase in adoption of online education globally is the key driver of the market.

- Online medical education has witnessed significant growth due to the convenience and flexibility it offers to students, particularly for medical professionals with demanding schedules. With the advent of technology, online learning platforms provide access to courses and lectures anytime, anywhere, enabling students to balance their professional commitments and academic pursuits. Interactive learning experiences, such as virtual simulations, artificial intelligence, and virtual reality (VR) technology, have revolutionized online medical education. These tools offer students hands-on experience in a secure and controlled environment, enhancing their knowledge and skills. Moreover, online medical education offers a wealth of academic resources, including e-books, journals, and multimedia content, accessible at any time with smart education mode.

- Accreditation systems ensure the quality and credibility of online medical education, offering courses that provide Continuing Education (CE) points, Medical Education (CME) credits, and even medical licenses for some programs. Online medical education caters to various medical disciplines, including biomedical sciences, diagnostics, disease management, and senior medical professionals, offering well-resourced classrooms, virtual patient rooms, and advanced training facilities. E-learning materials, such as adaptive tutorials, audio-visual clips, and virtual models, facilitate self-paced learning, while synchronous distance education, message boards, chats, e-mail, teleconferencing, and web-based systems enable real-time interaction with teachers and peers. Online medical education is transforming healthcare education, providing accessible, flexible, and interactive learning experiences for students.

What are the market trends shaping the Online Medical Education Industry?

Rising adoption of advanced simulation technologies in online medical courses is the upcoming market trend.

- The market is experiencing significant growth due to the integration of advanced e-technologies into medical training. Traditional methods of medical education are being supplemented with correspondence courses, open online courses, tele-learning, and e-learning. Virtual patient rooms, adaptive tutorials, audio-visual clips, and virtual models are becoming essential components of online medical education. These technologies enable students to access academic resources, interact with teachers and peers through message boards, chats, and e-mail, and participate in teleconferencing sessions. Online medical education offers students the opportunity to learn at their own pace and schedule, making it an attractive alternative to traditional clinical education.

- Virtual universities, undergraduate programs, and web-based systems provide students with well-equipped classrooms and training rooms, enabling them to acquire skills and knowledge in biomedical sciences, diagnostics, disease management, and senior medical professionals. E-learning platforms offer students access to a vast array of course content, medical education curriculum, and CME points. Medical students, physicians, nurses, and other healthcare professionals can earn medical licenses and continuing education (CE) points through online programs. Virtual patient simulation, interactive learning experiences, and advanced training facilities are essential features of online medical education. Accreditation systems ensure the quality and credibility of online medical education programs.

- Mobile platform education and live events provide students with additional learning opportunities. Textual content, audio, video, and electronic media are used to deliver comprehensive and engaging educational content. Overall, online medical education offers students a flexible, cost-effective, and well-resourced learning experience that aligns with the demands of modern healthcare.

What challenges does the Online Medical Education Industry face during its growth?

Restricted scope for assessing and evaluating students is a key challenge affecting the industry growth.

- Online medical education has emerged as a viable alternative to traditional clinical education, offering flexibility and convenience to students. However, replicating the intricacies of real-world patient interactions in a virtual setting poses challenges in the market. While virtual patient simulations and e-learning materials offer practical exposure, they may not fully capture the complexities of clinical competencies and decision-making abilities. Moreover, evaluating soft skills such as communication, empathy, and professionalism in an online environment can be challenging. The use of teleconferencing, message boards, chats, and e-mail for interaction between students and teachers or medical mentors can help mitigate some of these challenges.

- Well-equipped virtual classrooms, training rooms, and academic resources offer students access to biomedical sciences, diagnostics, disease management, and senior medical professionals. E-learning platforms and web-based systems provide students with course content, interactive learning experiences, and CME points. Accreditation systems ensure the quality and credibility of online medical education programs. Online medical education offers advanced training facilities and educational institutes the opportunity to reach a larger student base through mobile platform education, continuous education, and live events. The use of audio-visual clips, virtual models, and virtual patient simulation provides students with a rich learning experience. Online medical education caters to undergraduate, graduate, and continuing education for physicians, nurses, and medical students, offering them the flexibility to learn at their own pace and convenience.

Exclusive Customer Landscape

The online medical education market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the online medical education market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, online medical education market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amboss GmbH - The company provides specialized online medical education offerings, including NEJM Knowledge Plus Internal Medicine Board Review and NEJM Knowledge Plus Pediatrics Board Review.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amboss GmbH

- Apollo Hospitals Enterprise Ltd.

- CardioVillage

- DigiNerve

- edX LLC

- GIBLIB

- Harvard Medical School

- Haymarket Media Group

- IKONA Health

- Lecturio GmbH

- Manipal Global Education Services

- Medtronic

- Olympus Corp.

- Osso VR Inc.

- RELX Plc

- Stanford University

- The Cleveland Clinic Foundation

- The University of Melbourne

- Vumedi

- Wolters Kluwer NV

- Mayo Foundation for Medical Education and Research

- Medigrad Pte Ltd

- Relias LLC

- University of Liverpool

- WebMD LLC

- AffinityCE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Online medical education has emerged as a dynamic and innovative sector, offering flexible and accessible learning opportunities for students and professionals in the healthcare industry. This form of education encompasses various modalities, including correspondence courses, open online courses, tele-learning, and e-learning. Tele-learning platforms enable students to engage in real-time interactive sessions with their instructors and peers, utilizing tools such as message boards, chats, and e-mail. Synchronous distance education provides an immersive experience, allowing students to participate in virtual patient rooms, adaptive tutorials, and audio-visual clips. Virtual models and simulations offer students the opportunity to explore complex medical concepts and procedures in a risk-free environment.

Online assessments provide instant feedback, enabling students to track their progress and identify areas for improvement. Well-equipped classrooms and training rooms, whether physical or virtual, offer students access to a wealth of academic resources. Biomedical sciences, diagnostics, disease management, and senior medical professionals are just a few of the many subjects covered in online medical education. Traditional clinical education continues to play a crucial role in medical training, but online education offers several advantages. Simulation training, virtual anatomy, brain dissections, and virtual universities provide students with a more comprehensive and flexible learning experience. Undergraduate and postgraduate students, as well as medical schools and educational institutes, are increasingly turning to web-based systems for their medical education needs.

Continuous education (CE) programs, mobile platform education, live events, textual content, and online programs cater to the diverse learning styles and schedules of students. E-learning materials, such as audio, video, and electronic media, offer students the flexibility to learn at their own pace and in their preferred format. Medical education curriculum covers a wide range of topics, from basic sciences to advanced training facilities. Accreditation systems ensure the quality and validity of online medical education programs, providing students with the confidence that their education meets the highest standards. Online medical education offers a wealth of opportunities for students and professionals to acquire the knowledge, skills, and behavior necessary to excel in the healthcare industry.

Medical students and educators benefit from the interactive learning experiences offered by online courses. Tele-learning platforms and e-learning materials provide students with access to a wealth of resources, enabling them to learn from anywhere at any time. Online medical education offers several advantages over traditional classroom-based education. It is more flexible, allowing students to learn at their own pace and schedule. It is also more cost-effective, as students can save on travel and accommodation expenses. In conclusion, online medical education is a dynamic and innovative sector that offers flexible and accessible learning opportunities for students and professionals in the healthcare industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24.9% |

|

Market growth 2024-2028 |

USD 64.67 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

23.81 |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Online Medical Education Market Research and Growth Report?

- CAGR of the Online Medical Education industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the online medical education market growth of industry companies

We can help! Our analysts can customize this online medical education market research report to meet your requirements.

RIA -

RIA -