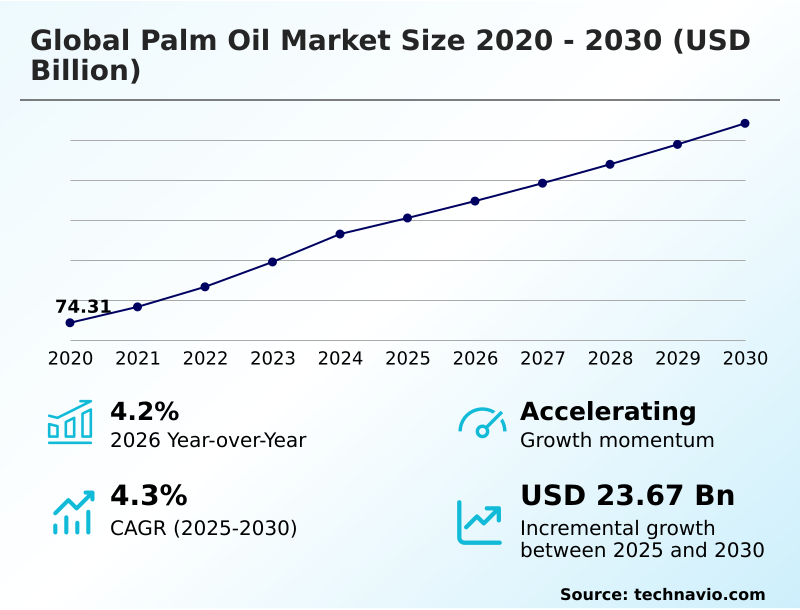

Palm Oil Market Size 2026-2030

The palm oil market size is valued to increase by USD 23.67 billion, at a CAGR of 4.3% from 2025 to 2030. Versatility and cost-effectiveness driving food and beverage sector demand will drive the palm oil market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 75.9% growth during the forecast period.

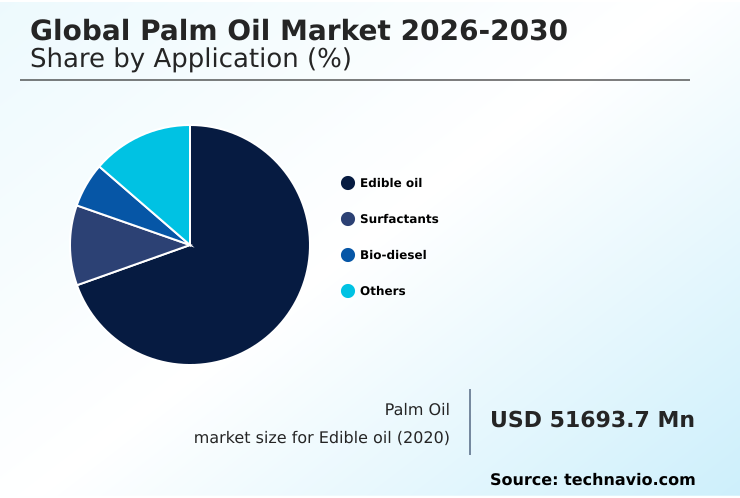

- By Application - Edible oil segment was valued at USD 67.37 billion in 2024

- By Type - Conventional segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 49.87 billion

- Market Future Opportunities: USD 23.67 billion

- CAGR from 2025 to 2030 : 4.3%

Market Summary

- The palm oil market is shaped by the convergence of robust demand and significant sustainability pressures. Its utility as a cost-effective, versatile ingredient ensures its central role in the food, oleochemical, and biofuel sectors. Demand is driven by population growth and increased consumption of processed foods in developing nations.

- However, the industry grapples with challenges tied to deforestation and social issues, spurring a market-wide shift towards traceability and certification. For instance, a food manufacturer aiming to comply with new import regulations must now invest in a transparent supply chain.

- This involves integrating technologies to verify the origin of its raw materials, ensuring they are sourced from plantations that adhere to strict no-deforestation policies and fair labor standards. This pivot from a commodity-based approach to a quality-and-compliance model is redefining operational strategies and competitive positioning for all stakeholders involved.

What will be the Size of the Palm Oil Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Palm Oil Market Segmented?

The palm oil industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

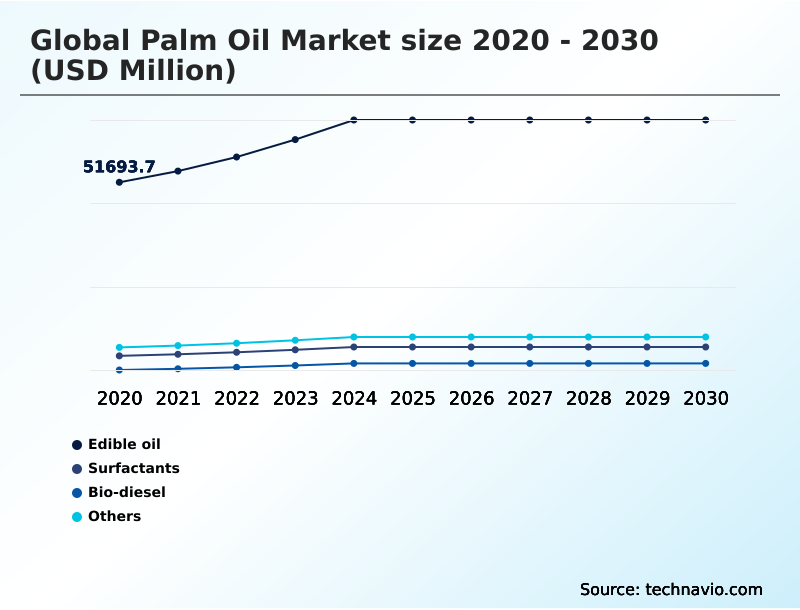

- Application

- Edible oil

- Surfactants

- Bio-diesel

- Others

- Type

- Conventional

- Organic

- Product type

- Crude palm oil

- Fractionated palm oil

- Palm kernel oil

- Geography

- APAC

- Indonesia

- India

- China

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Europe

- Germany

- The Netherlands

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Application Insights

The edible oil segment is estimated to witness significant growth during the forecast period.

The edible oil segment is foundational, driven by palm oil’s functional versatility and economic efficiency in food manufacturing ingredient applications.

The process of fractionation separates crude palm oil into liquid olein and solid stearin, creating tailored specialty fats and non-hydrogenated fats for diverse edible oil applications.

Its high oxidative stability and semi-solid fat texture make it ideal for bakery shortenings and confectionery fats, providing structure without hydrogenation. For frying oil stability, its resistance to thermal degradation extends shelf life.

The refining, bleaching, and deodorizing (RBD) process ensures a neutral profile essential for bio-based ingredients.

This functional adaptability, combined with its high-yield production that delivers a more than five-fold output advantage over other oilseed crops, secures its role in the food supply chain.

The Edible oil segment was valued at USD 67.37 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 75.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Palm Oil Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which functions as both the primary production hub and a major consumption zone, accounting for over 75% of the market's incremental growth.

Countries in this region are central to the global supply of palm kernel oil, a key source of lauric acid and glycerin for surfactant production and personal care formulations.

In contrast, Europe and North America act as regulatory epicenters, driving the adoption of advanced supply chain traceability technologies like blockchain traceability and geospatial mapping.

This pressure compels producers to focus on sustainable intensification and improve the oil extraction rate (OER).

The industry is also seeing greater smallholder farmer integration into certified supply chains, a crucial step for achieving sector-wide compliance with international standards for fractionated palm oil.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the global palm oil market 2026-2030 requires a nuanced view of its entire value chain. The debate over sustainable palm oil production methods is central, with a clear distinction between conventional vs organic palm oil processing. The role of technology in palm oil is critical, especially for improving palm oil crop yield sustainably.

- After harvesting, the crude palm oil refining process and the subsequent palm oil fractionation process explained through technical documentation, are key to creating products for various sectors. For instance, using palm oil in biodiesel production is a major economic driver for the palm oil market, though it fuels the biofuel mandates effect on palm oil.

- The palm oil vs soybean oil comparison is constantly evaluated by industrial buyers. In other sectors, palm kernel oil in cosmetics formulation relies on palm kernel oil lauric acid extraction. The future of palm oil oleochemicals looks robust, driven by the palm oil market in emerging economies.

- However, operators face the impact of esg on palm oil and must contend with managing palm oil supply chain volatility.

- Meeting the challenges in palm oil traceability and achieving deforestation-free palm oil sourcing are now essential for market access, with producers that have rspo certified palm oil benefits seeing a competitive advantage that can be as significant as a 15% price premium in certain European markets.

What are the key market drivers leading to the rise in the adoption of Palm Oil Industry?

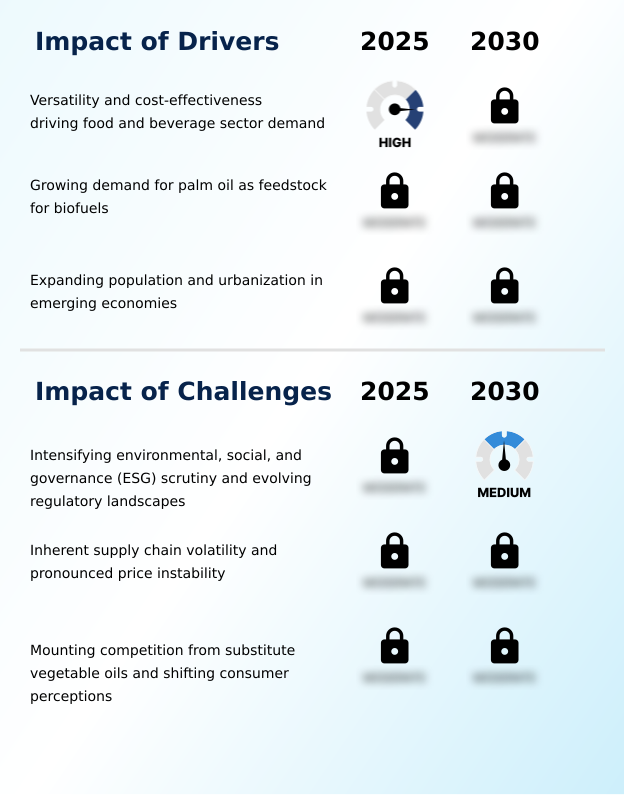

- The key market driver is sustained demand from the food and beverage sector, fueled by the versatility and cost-effectiveness of palm oil as a primary food ingredient.

- Robust demand from emerging economy demand, driven by rapid urban consumption patterns, underpins market expansion. The food vs.

- fuel debate intensifies as biodiesel becomes a primary demand driver, with government energy security policy and biofuel feedstock mandates absorbing a significant portion of supply. For example, Indonesia’s B35 mandate diverts over 30% of its domestic production to transesterification processes.

- Concurrently, agricultural advancements focusing on high-yielding seed varieties are boosting the output of fresh fruit bunches (FFB) per hectare, which enhances supply chain risk management against commodity price volatility.

- This focus on yield improvement as a renewable feedstock source helps stabilize the supply of essential fatty acids for both food and industrial applications without requiring further land expansion.

What are the market trends shaping the Palm Oil Industry?

- The ascendancy of sustainability mandates and the increasing demand for certified palm oil are prominent market trends. These factors are compelling producers and end-users to overhaul supply chains to meet stringent ESG criteria.

- A significant trend is the strategic diversification into downstream processing to create value-added derivatives. This pivot towards the oleochemical industry growth is fueled by demand for sustainable ingredients in consumer goods. The circular economy model is being actively implemented through waste-to-value conversion, where palm oil mill effluent (POME) is used for biogas generation and solid waste is turned into bio-fertilizers.

- Adherence to sustainability certification, including RSPO certification and MSPO certification, is no longer optional. Leading vertically integrated companies have achieved over 98% traceability in their sustainable sourcing efforts. This focus on creating a transparent oleochemicals supply chain is enabling companies to meet stringent regulatory demands while capturing higher margins, with some specialized derivatives commanding a 20% premium over crude oil.

What challenges does the Palm Oil Industry face during its growth?

- A key challenge affecting industry growth is intensifying environmental, social, and governance (ESG) scrutiny, which is compounded by an evolving and complex regulatory landscape.

- The market faces intense challenges from environmental, social, and governance (ESG) scrutiny and complex regulatory compliance, which now dictate market access. The pressure of consumer perception management has spurred a product reformulation trend, leading to increased competition from vegetable oil substitutes. For example, the 'palm-free' movement has contributed to a 5% market share decline in certain European consumer goods categories.

- Producers must now prove their deforestation-free supply chain credentials by documenting that plantations are not on high-carbon-stock or high-conservation-value lands and by upholding strict labor practice standards and land tenure rights. The operational cost to meet these NDPE commitments and obtain ISPO certification can increase production expenses by up to 10% for some operators, squeezing margins amidst price pressures.

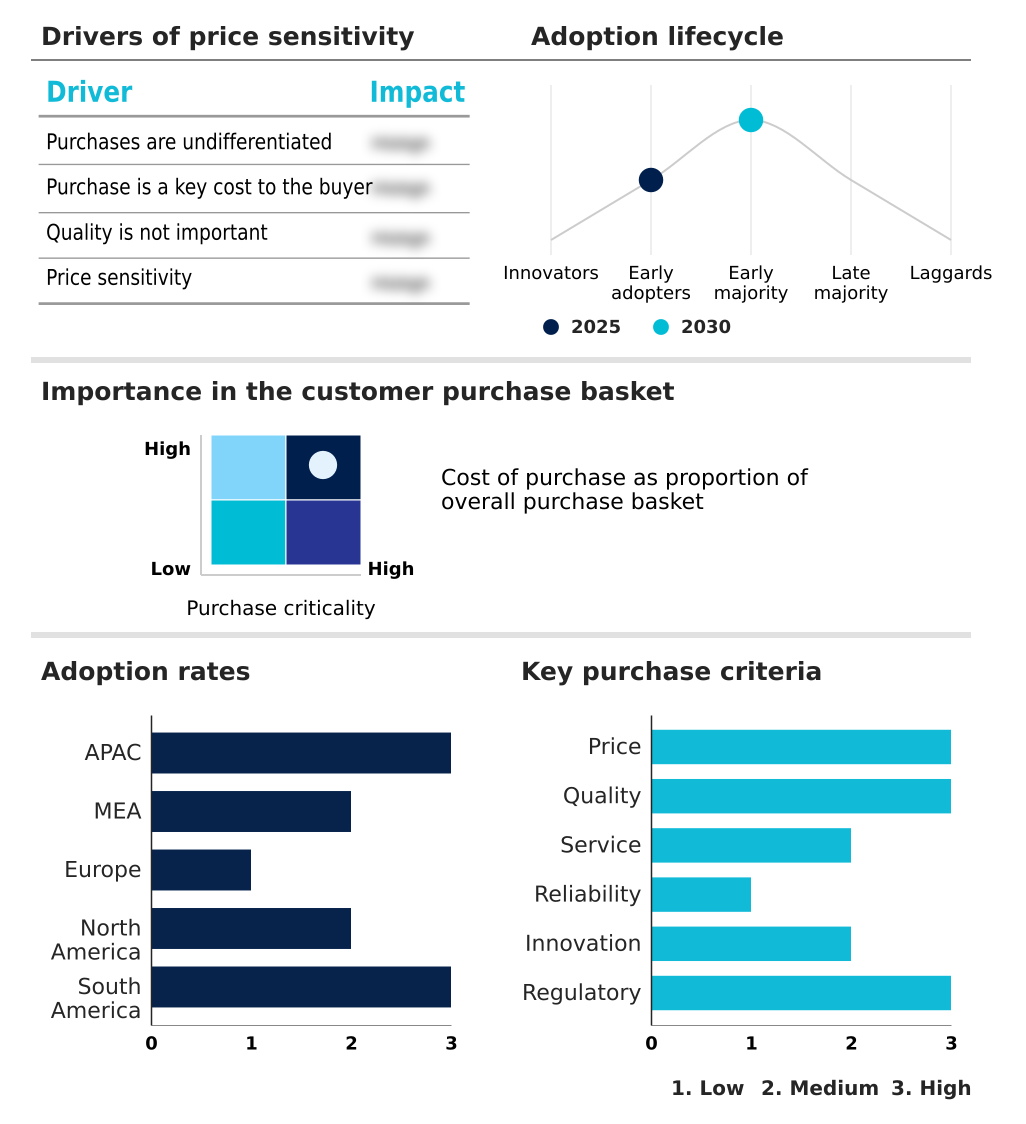

Exclusive Technavio Analysis on Customer Landscape

The palm oil market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the palm oil market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Palm Oil Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, palm oil market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alami Commodities Sdn Bhd - Offerings span from crude and fractionated oils for food applications to specialized oleochemicals and biodiesel, addressing diverse industrial needs with versatile feedstocks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alami Commodities Sdn Bhd

- Archer Daniels Midland Co.

- Asian Agri

- Best Industry Group

- Bunge Global SA

- Cargill Inc.

- Charleston Holdings Pte Ltd.

- FGV Holdings Berhad

- Gujarat Ambuja Exports Ltd.

- IOI Corp. Berhad

- Kuala Lumpur Kepong Berhad

- Musim Mas Group

- Nisshin Oillio Group Ltd.

- Oil Palm India Ltd.

- Olam Group Ltd.

- Patanjali Ayurved Ltd.

- Sinar Mas Group

- Univanich Palm Oil PCL

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Palm oil market

- In November 2024, Cargill Inc. announced the expansion of its smallholder partnership program to over 26,400 participants as part of its strategy to build a deforestation-free supply chain.

- In February 2025, palm oil producer associations from Colombia, Ecuador, and Brazil signed the Latin American Charter for Sustainable Palm Oil, committing to 100% deforestation-free production across the region.

- In March 2025, a consortium of major North American food manufacturers and retailers launched the North American Responsible Palm Oil Sourcing Charter, creating unified requirements for supply chain traceability and labor rights.

- In May 2025, Malaysia announced a strategic relocation of its regional palm oil council office to Kenya, aiming to establish the country as a central processing and distribution hub for East Africa.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Palm Oil Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2026-2030 | USD 23672.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.2% |

| Key countries | Indonesia, Malaysia, India, China, Thailand, Japan, Nigeria, Egypt, Saudi Arabia, South Africa, UAE, Germany, The Netherlands, France, UK, Spain, Italy, US, Canada, Mexico, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The palm oil market is undergoing a fundamental transformation where environmental, social, and governance compliance is now a primary determinant of corporate strategy. Boardroom decisions are increasingly focused on capital expenditures for sustainable intensification and advanced supply chain traceability to mitigate risks and secure market access.

- This involves deploying technologies like blockchain traceability and geospatial mapping to verify NDPE commitments and ensure no sourcing from high-carbon-stock or high-conservation-value areas. Operationally, this shift promotes a circular economy, with investments in biogas generation from palm oil mill effluent (POME) and the creation of bio-fertilizers.

- The entire production chain, from managing fresh fruit bunches (FFB) to optimizing the oil extraction rate (OER) and monitoring free fatty acid (FFA) content, is being re-engineered. The adoption of high-yielding seed varieties and precision agriculture is becoming standard.

- Downstream, the value chain extends from crude palm oil through the refining, bleaching, and deodorizing (RBD) process to create fractionated palm oil, semi-solid fat, and specialty fats.

- These bio-based ingredients, known for oxidative stability, are a renewable feedstock for biodiesel through transesterification, and for oleochemicals like fatty acids, lauric acid, and glycerin, all underpinned by robust RSPO, ISPO, and MSPO sustainability certification frameworks. For instance, leading producers now demonstrate over 98% traceability to the mill, a critical benchmark for stakeholders.

What are the Key Data Covered in this Palm Oil Market Research and Growth Report?

-

What is the expected growth of the Palm Oil Market between 2026 and 2030?

-

USD 23.67 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Edible oil, Surfactants, Bio-diesel, and Others), Type (Conventional, and Organic), Product Type (Crude palm oil, Fractionated palm oil, and Palm kernel oil) and Geography (APAC, Middle East and Africa, Europe, North America, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Middle East and Africa, Europe, North America and South America

-

-

What are the key growth drivers and market challenges?

-

Versatility and cost-effectiveness driving food and beverage sector demand, Intensifying environmental, social, and governance (ESG) scrutiny and evolving regulatory landscapes

-

-

Who are the major players in the Palm Oil Market?

-

Alami Commodities Sdn Bhd, Archer Daniels Midland Co., Asian Agri, Best Industry Group, Bunge Global SA, Cargill Inc., Charleston Holdings Pte Ltd., FGV Holdings Berhad, Gujarat Ambuja Exports Ltd., IOI Corp. Berhad, Kuala Lumpur Kepong Berhad, Musim Mas Group, Nisshin Oillio Group Ltd., Oil Palm India Ltd., Olam Group Ltd., Patanjali Ayurved Ltd., Sinar Mas Group, Univanich Palm Oil PCL and Wilmar International Ltd.

-

Market Research Insights

- The market is shaped by a dynamic interplay between cost efficiency and stringent sustainability requirements. While its functional properties drive demand in food and industrial applications, regulatory compliance and consumer perception management are increasingly influential. A clear bifurcation is evident, with sustainably sourced palm oil commanding a market advantage.

- For instance, major producers have achieved over 98% traceability to the mill, a critical metric for retaining access to regulated markets. Concurrently, partnership programs have successfully integrated more than 26,000 smallholders into deforestation-free supply chains, showcasing a commitment to social responsibility. This focus on verifiable sustainability is reshaping supply chain risk management and sourcing strategies globally.

We can help! Our analysts can customize this palm oil market research report to meet your requirements.

RIA -

RIA -