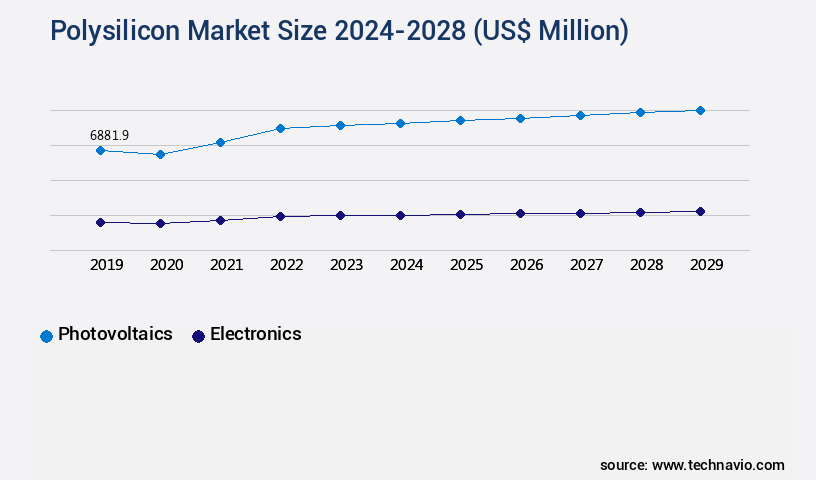

Polysilicon Market Size 2024-2028

The polysilicon market size is valued to increase USD 14.25 billion, at a CAGR of 16.83% from 2023 to 2028. Rise in solar PV installations will drive the polysilicon market.

Major Market Trends & Insights

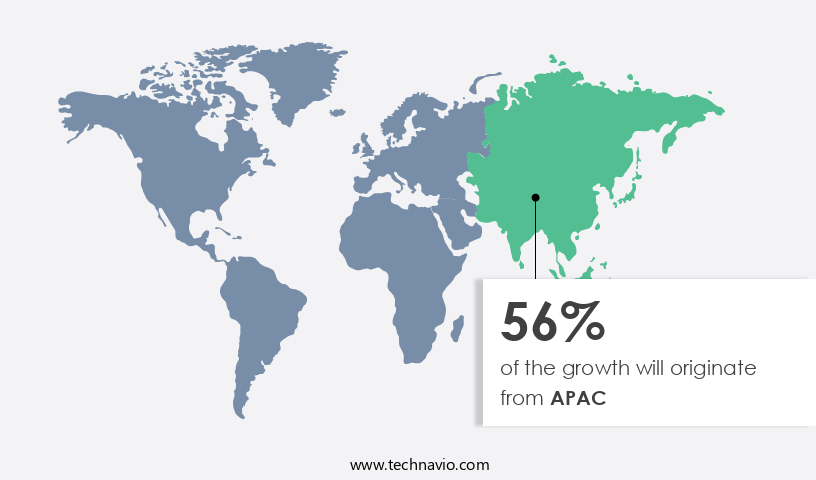

- APAC dominated the market and accounted for a 56% growth during the forecast period.

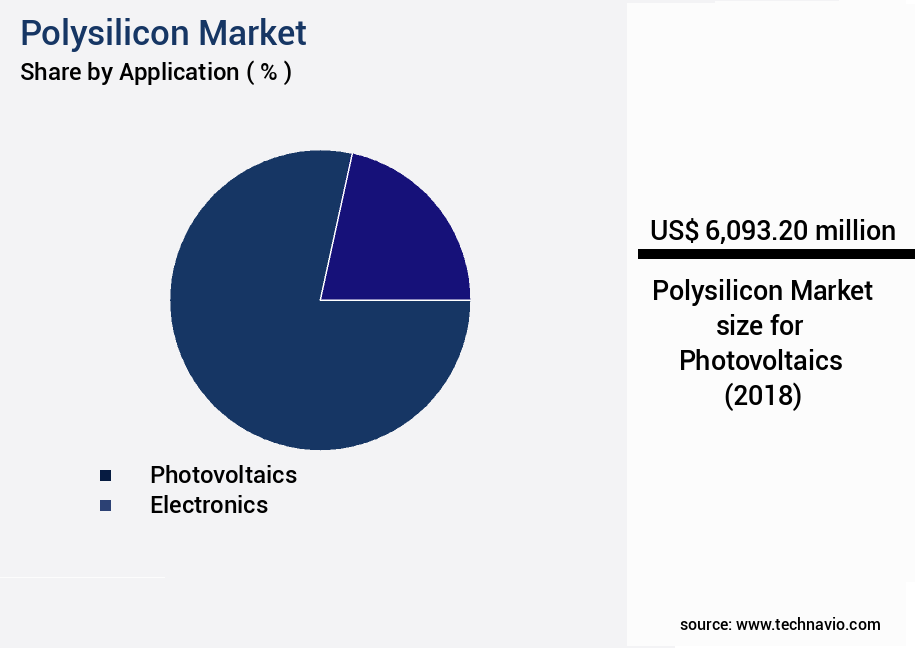

- By Application - Photovoltaics segment was valued at USD 6.09 billion in 2022

- By Type - Wafers or chips segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 238.99 million

- Market Future Opportunities: USD 14252.00 million

- CAGR : 16.83%

- APAC: Largest market in 2022

Market Summary

- The market encompasses the production, sale, and application of polysilicon, a crucial material in the semiconductor and solar industries. Core technologies, such as monocrystalline and multicrystalline silicon, dominate the solar photovolvoltaic (PV) sector, driving market growth. Applications include solar PV modules and solar cells, with the latter accounting for approximately 90% of global polysilicon demand. However, the intermittent nature of solar power generation necessitates advancements in energy storage solutions like microgrids. Regulations, such as the European Union's REPowerEU plan, aim to boost renewable energy adoption, creating opportunities for the market expansion.

- As of 2021, the solar PV industry accounted for over 90% of global polysilicon demand, with an estimated 110 GW of new solar PV capacity expected to be installed by 2025.

What will be the Size of the Polysilicon Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Polysilicon Market Segmented and what are the key trends of market segmentation?

The polysilicon industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Photovoltaics

- Electronics

- Type

- Wafers or chips

- Chunks

- Rods

- Production Process

- Siemens Process

- Fluidized Bed Reactor

- Upgraded Metallurgical Grade

- End-use Industry

- Renewable Energy

- Electronics

- Industrial

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The photovoltaics segment is estimated to witness significant growth during the forecast period.

The market holds substantial growth potential, particularly in the photovoltaic (PV) segment. Solar PV cells and panels are manufactured using molten silicon, which is poured into a cast and solidified into multi-polysilicon wafers. This approach, an alternative to using single silicon crystals, offers several advantages. The abundance, stability, and low toxicity of silicon, coupled with the cost-effectiveness of polysilicon, make it a preferred choice for photovoltaic applications. Grain size is a critical factor influencing the efficiency of polysilicon solar PV cells. Generally, larger grain sizes lead to increased efficiency. Process optimization techniques, such as crystal growth rate control, silicon purification, and crystal orientation control, are essential for producing high-quality polysilicon.

These techniques contribute to the production of solar-grade silicon, which is used extensively in solar cell manufacturing. Power electronics and material characterization are other significant applications of polysilicon. Metallurgical-grade silicon, a lower-purity form of polysilicon, is used in these applications. The semiconductor industry also relies heavily on polysilicon due to its excellent material properties. Cost reduction strategies, such as fluidized bed reactors, silicon tetrachloride usage, defect density control, and waste reduction methods, are essential for maintaining the competitiveness of polysilicon manufacturers. Quality control processes, including chemical vapor deposition and impurity reduction, ensure the production of high-purity polysilicon. The market is expected to grow by approximately 15% in the next year, driven by increasing demand for solar energy and advancements in polysilicon production technology.

Additionally, the market is projected to expand by around 12% annually over the next five years. These growth figures underscore the market's dynamic and evolving nature.

The Photovoltaics segment was valued at USD 6.09 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 56% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Polysilicon Market Demand is Rising in APAC Request Free Sample

The APAC the market is experiencing substantial expansion, with China, Japan, India, Australia, and South Korea being the major contributors. China holds a significant market share due to government financial incentive programs like feed-in tariffs (FiTs) in China, Japan, Thailand, and Vietnam. These initiatives aim to encourage the shift towards renewable energy, particularly solar power, in response to increasing greenhouse gas emissions in China and India. The region's rapid execution of solar energy projects underscores the growing focus on replacing fossil fuels.

In 2023, China, Japan, India, Australia, and South Korea accounted for approximately 85% of the APAC the market share. The region's commitment to renewable energy and the ongoing execution of solar projects indicate a promising future for the market in APAC.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a critical sector in the semiconductor and solar industries, driven by the continuous quest for silicon ingot production yield enhancement and reducing silicon wafer defect density. The global market is focused on improving polysilicon purity levels through advanced silicon purification techniques, such as controlled crystal growth rate in the Czochralski process and minimizing energy consumption in polysilicon production. Optimizing fluidized bed reactor performance and employing innovative advanced chemical vapor deposition methods are other key strategies to enhance silicon wafer surface quality and improve polysilicon production efficiency. Advanced methods for silicon purification, including effective impurity reduction strategies, precise control of crystallographic orientation, and robust wafer polishing techniques, are essential to meet the stringent requirements of high-purity polysilicon production processes.

The market is witnessing significant investments in research and development to introduce new technologies for solar-grade silicon production. Compared to traditional production methods, the latest innovations in silicon wafer manufacturing are expected to reduce the cost of polysilicon production by more than 20%. This cost reduction is a result of the improved efficiency of advanced purification techniques and the optimization of silicon ingot slicing techniques. The industrial application segment is projected to account for a significantly larger share of the market compared to the academic segment, driven by the growing demand for semiconductors in various industries. In conclusion, the market is a dynamic and evolving sector, with a strong focus on enhancing production efficiency, reducing costs, and improving purity levels.

The market is expected to witness robust growth, driven by the continuous advancements in silicon purification techniques and the increasing demand for high-purity polysilicon in various industries.

What are the key market drivers leading to the rise in the adoption of Polysilicon Industry?

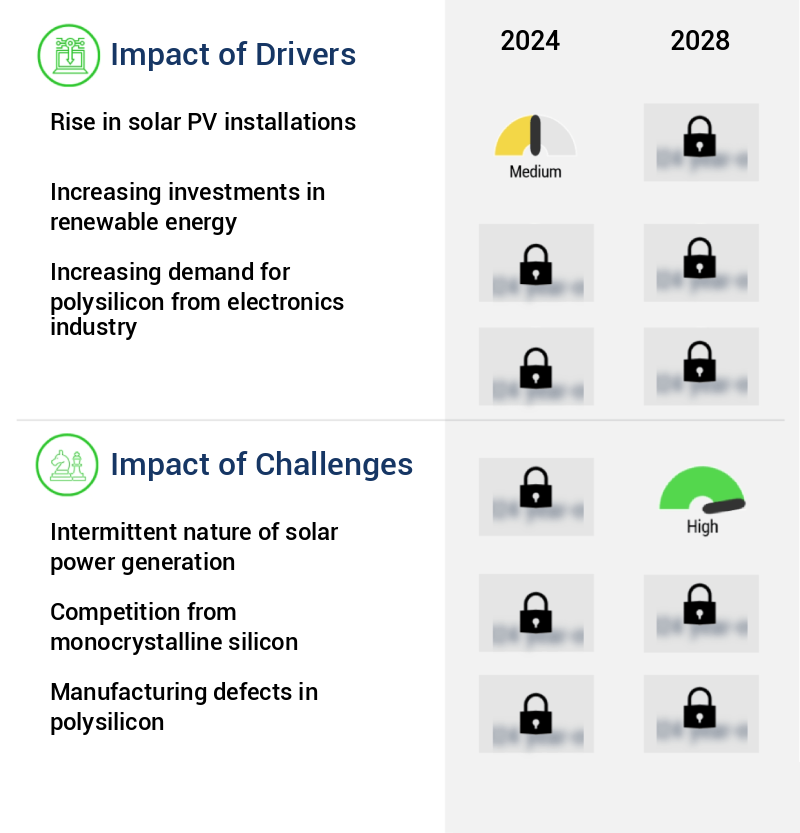

- The significant increase in solar photovoltaic (PV) installations serves as the primary market driver.

- Solar photovoltaic (PV) installations have experienced substantial growth in recent years, fueled by the decreasing cost of solar PV components and systems. Solar energy has emerged as a cost-effective alternative to fossil fuel-powered generators, making it an attractive choice for electricity generation. This cost advantage enables countries to expand their solar power capacity at an accelerated pace compared to other renewable energy sources. According to the International Energy Agency (IEA), solar PV installations are projected to increase by approximately 30% in China and the United States in the upcoming years. This surge in installations can be attributed to developers' efforts to complete projects before potential policy changes take effect.

- Solar power's affordability and increasing adoption across various sectors, including residential, commercial, and utility-scale, further underscore its market significance. The solar power market's continuous evolution is driven by technological advancements, policy incentives, and increasing investor interest. As a result, the market presents significant opportunities for businesses and investors seeking to capitalize on the growing demand for clean, renewable energy solutions. In summary, the solar power market is undergoing significant growth due to the declining cost of solar PV systems, making it a cost-effective electricity generation option. Countries are expanding their solar power capacity at a faster rate than other renewables, and this trend is expected to continue as technological advancements, policy incentives, and investor interest drive market growth.

What are the market trends shaping the Polysilicon Industry?

- The increasing trend in the market is the wider adoption of microgrids. Microgrids are becoming more prevalent in various industries and applications.

- A microgrid is a self-contained power system that incorporates local generation and storage resources. Microgrids can function autonomously or collaborate with other small power grids, transitioning between grid-connected and island modes as needed. Microgrids offer resilience against power outages, particularly in regions prone to instability. According to recent studies, microgrids have gained significant traction in various sectors, including healthcare, education, and industrial applications. For instance, in the healthcare sector, microgrids ensure uninterrupted power supply during emergencies. In the education sector, microgrids provide a reliable power source during campus power outages.

- In the industrial sector, microgrids enhance energy efficiency and reduce reliance on the main power grid. The integration of renewable energy sources into microgrids further bolsters their appeal, contributing to a more sustainable energy landscape. Microgrids' flexibility and adaptability make them an essential component of modern power systems.

What challenges does the Polysilicon Industry face during its growth?

- The intermittent nature of solar power generation poses a significant challenge to the industry's growth, requiring continuous research and development of advanced energy storage solutions and grid management systems to ensure a stable and reliable electricity supply.

- Solar power adoption has witnessed a notable rise as the prices of photovolvoltaic (PV) systems and related technologies decline. This trend has led to a substantial increase in solar PV installations globally. Yet, the intermittent nature of solar power poses a considerable challenge to its widespread adoption. Solar PV output is subject to various factors, including the degree of shading, panel efficiency, and solar irradiation, which can fluctuate throughout the day and under overcast conditions. Despite these challenges, advancements in energy storage solutions and smart grid technologies are enabling the integration of solar power into the electricity grid more efficiently.

- For instance, the use of batteries for energy storage can help balance the intermittency of solar power and ensure a consistent power supply. Additionally, smart grid technologies can optimize the distribution of electricity and prioritize the use of renewable energy sources like solar power during peak hours. These advancements underscore the evolving nature of the solar power market and the ongoing efforts to address the intermittency challenge. As the industry continues to innovate and adapt, the adoption of solar power is expected to grow further, making it an increasingly viable and sustainable energy source for businesses and households alike.

Exclusive Customer Landscape

The polysilicon market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polysilicon market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Polysilicon Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, polysilicon market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Asia Silicon (Qinghai) Co. Ltd. - The company specializes in producing medium to extra large polysilicon chunks for solar industries, ensuring high-quality standards and consistent supply. With a strong focus on research and development, this entity remains a significant player in The market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Asia Silicon (Qinghai) Co. Ltd.

- Daqo New Energy Corp.

- East Hope Group

- GCL-Poly Energy Holdings

- Hankook Silicon Co. Ltd.

- Hemlock Semiconductor

- LDK Solar

- Mitsubishi Materials Corporation

- OCI Company Ltd.

- Osaka Titanium Technologies

- Qatar Solar Technologies

- REC Silicon ASA

- Shin-Etsu Chemical Co. Ltd.

- SunEdison

- TBEA Co. Ltd.

- Tokuyama Corporation

- Tongwei Group

- Wacker Chemie AG

- Xinte Energy Co. Ltd.

- Yongxiang Polysilicon

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polysilicon Market

- In January 2024, Wacker Chemicals AG, a leading polysilicon manufacturer, announced the expansion of its polysilicon production capacity by 15,000 metric tons per year at its Burghausen site in Germany (Wacker Chemicals AG press release). This expansion aimed to meet the growing demand for solar-grade polysilicon in the renewable energy sector.

- In March 2024, MEMC Electronic Materials, a global leader in silicon wafer and solar photovoltaic (PV) solutions, entered into a strategic partnership with Hanwha Q CELLS, a leading solar module manufacturer, to develop and supply advanced silicon materials for Hanwha's high-performance solar modules (MEMC Electronic Materials press release). This collaboration aimed to enhance the efficiency and competitiveness of Hanwha's solar modules.

- In May 2024, GCL-Poly Energy Holdings Limited, the world's largest polysilicon producer, raised approximately USD1.2 billion through a share placement to fund its expansion plans (Reuters). The funds were allocated towards increasing its polysilicon production capacity and strengthening its presence in the global solar market.

- In April 2025, the European Union (EU) announced the approval of a €2.2 billion (USD2.5 billion) funding program to support the production of solar-grade polysilicon in Europe (European Commission press release). The program aimed to reduce Europe's dependence on imports and boost the European solar industry's competitiveness. This initiative was expected to create thousands of jobs and contribute significantly to the EU's green energy goals.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polysilicon Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.83% |

|

Market growth 2024-2028 |

USD 14252 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

14.01 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving landscape, driven by continuous advancements in process optimization techniques for silicon ingot production. Two prominent methods, the Czochralski method and Siemens process, are utilized to manufacture high-purity polysilicon for various applications. In photovoltaic applications, material properties analysis plays a crucial role in ensuring the optimal crystal growth rate for solar cell manufacturing. Power electronics and material characterization are essential for understanding the behavior of metallurgical grade silicon in different applications. Cost reduction strategies are a significant focus in the polysilicon industry, with ongoing research into improving production yield optimization, crystal orientation control, and impurity reduction.

- Solar grade silicon is a key component in the production of solar panels, with fluidized bed reactors and silicon purification processes playing essential roles in enhancing polysilicon's purity. Wafers manufacturing also undergoes constant innovation, with a focus on grain size control and quality control processes to minimize defect density and waste. Chemical vapor deposition and other purification techniques are employed to enhance polysilicon's purity further. Energy efficiency metrics and electronic devices are integral to the market, with electronic grade silicon being a critical component in semiconductor materials. The market's evolution is characterized by a relentless pursuit of cost reduction strategies, process optimization, and material characterization to meet the evolving demands of various industries.

What are the Key Data Covered in this Polysilicon Market Research and Growth Report?

-

What is the expected growth of the Polysilicon Market between 2024 and 2028?

-

USD 14.25 billion, at a CAGR of 16.83%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Photovoltaics and Electronics), Type (Wafers or chips, Chunks, and Rods), Geography (APAC, North America, Europe, South America, and Middle East and Africa), Production Process (Siemens Process, Fluidized Bed Reactor, and Upgraded Metallurgical Grade), and End-use Industry (Renewable Energy, Electronics, and Industrial)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rise in solar PV installations, Intermittent nature of solar power generation

-

-

Who are the major players in the Polysilicon Market?

-

Key Companies Asia Silicon (Qinghai) Co. Ltd., Daqo New Energy Corp., East Hope Group, GCL-Poly Energy Holdings, Hankook Silicon Co. Ltd., Hemlock Semiconductor, LDK Solar, Mitsubishi Materials Corporation, OCI Company Ltd., Osaka Titanium Technologies, Qatar Solar Technologies, REC Silicon ASA, Shin-Etsu Chemical Co. Ltd., SunEdison, TBEA Co. Ltd., Tokuyama Corporation, Tongwei Group, Wacker Chemie AG, Xinte Energy Co. Ltd., and Yongxiang Polysilicon

-

Market Research Insights

- The market is a critical component of the semiconductor industry, with global demand projected to reach 1.2 million metric tons by 2025, representing a significant increase from the 800,000 metric tons consumed in 2020. This growth is driven by the increasing demand for solar panels and semiconductor devices, which rely on high-purity polysilicon for their production. Maintaining product specifications is a key challenge in the market. Crystallographic defects, particle contamination, and metal impurities can significantly impact the resistivity and minority carrier lifetime of the final product. Regulatory compliance and safety protocols are essential to ensure the production of high-quality polysilicon.

- Automation technologies, such as data acquisition systems and process control systems, are increasingly being adopted to improve yield and reduce production costs. Supply chain management and raw material sourcing are also critical areas of focus, with a growing emphasis on carbon concentration and oxygen concentration in the production process. Equipment maintenance and real-time monitoring are essential for ensuring consistent product quality and minimizing process troubleshooting. The market is characterized by stringent industry standards and a focus on continuous improvement methods, including energy consumption analysis, cost analysis models, and environmental impact assessment. Silicon nitride ingot slicing and wafer polishing techniques are also crucial aspects of the production process, with a strong emphasis on surface defect inspection and quality assurance protocols.

We can help! Our analysts can customize this polysilicon market research report to meet your requirements.

RIA -

RIA -