Primary Immunodeficiency Therapeutics Market Size 2024-2028

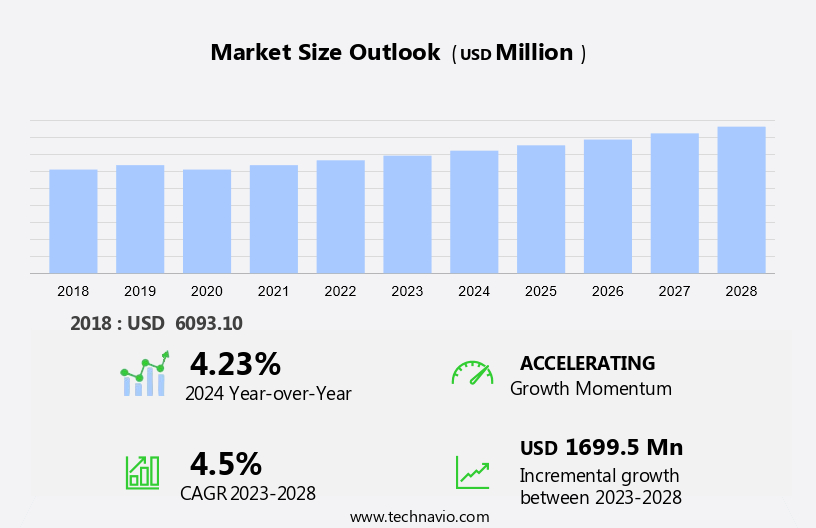

The primary immunodeficiency therapeutics market size is forecast to increase by USD 1.7 billion at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing prevalence of immunodeficiency diseases and the subsequent demand for innovative treatments. Medical technologies, including genetic testing and medical diagnostics, are playing a crucial role in the identification and diagnosis of these conditions. Immunotherapy, a key area of focus in the market, is witnessing increased R&D activities to address the side effects associated with current treatments.

- Furthermore, the emergence of gene therapies offers promising solutions for conditions such as hypothyroidism and other genetic disorders. Antibiotics, while effective for treating infections, are not a long-term solution for individuals with primary immunodeficiencies. The market analysis report provides a comprehensive overview of these trends and challenges, offering insights into the future growth prospects of the market.

What will be the Size of the Primary Immunodeficiency Therapeutics Market During the Forecast Period?

- The market encompasses a range of treatments for various immune deficiencies, including antibody deficiencies and cellular immunodeficiencies, such as innate immune disorders. Key therapeutic approaches include immunoglobulin replacement therapy, stem cell and bone marrow transplantation, antibiotic therapy, gene therapy, and immunomodulatory agents. Indications covered within this market include, but are not limited to, immunodeficiency diseases, rheumatoid disease, deficiency anemia, hypothyroidism, and tumors caused by genetic abnormalities. Therapies aim to address recurring infections, immune cell dysfunction, and protein deficiencies.

- Diagnostic tests and genetic testing play a crucial role in identifying these conditions, enabling timely intervention with appropriate supportive care and therapeutic interventions.The market is driven by the increasing prevalence of immune deficiencies, advancements in diagnostic technologies, and the development of novel therapies, such as immunomodulatory agents and gene therapy.

How is this Primary Immunodeficiency Therapeutics Industry segmented and which is the largest segment?

The primary immunodeficiency therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Disease Type

- Antibody deficiency

- Cellular immunodeficiency

- Innate immune disorders

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

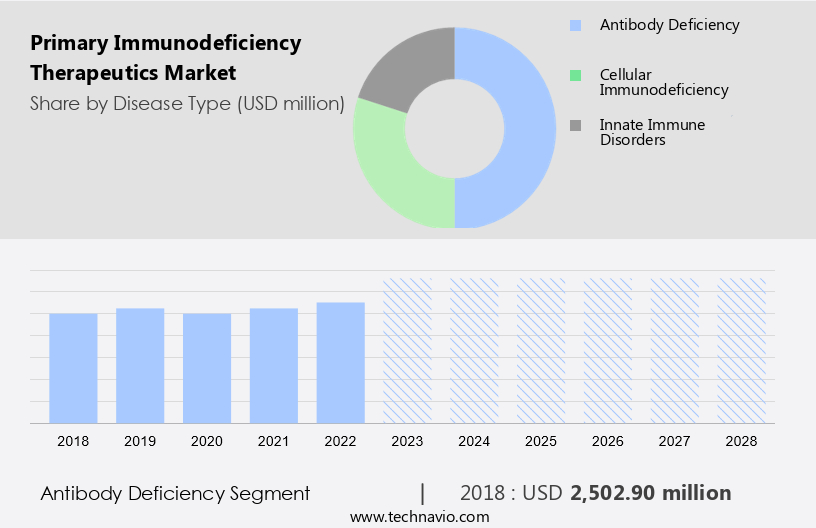

By Disease Type Insights

The antibody deficiency segment is estimated to witness significant growth during the forecast period. The market encompasses various treatments for a range of immune disorders. Antibody deficiency, a significant segment, affects approximately half of diagnosed primary immunodeficiency patients. This category includes humoral immunodeficiency diseases, primarily impacting B cells. Cellular immunodeficiencies, innate immune disorders, and coagulopathies are other notable segments. Therapeutic interventions include Immunoglobulin replacement therapy, stem cell and bone marrow transplantation, antibiotic therapy, gene therapy, and immunomodulatory drugs. Conditions treated include immunodeficiency diseases, recurring infections, tumors, genetic abnormalities, rheumatoid disease, deficiency anemia, hypothyroidism, lymphoma, neurologic disorders, arrhythmias, electrolyte disorders, coagulopathies, weight loss, rhinitis, atopic dermatitis, X-linked SCID, Wiskott Aldrich Syndrome, non-Hodgkin's lymphoma, rheumatoid arthritis, and more.

Healthcare professionals utilize diagnostic technologies such as flow cytometry and next-generation sequencing to diagnose these disorders. Healthcare expenditure on primary immunodeficiency therapeutics continues to grow, driven by increasing awareness, advancements in diagnostic technologies, and the development of targeted therapies and gene therapies.

Get a glance at the market report of various segments Request Free Sample

The Antibody deficiency segment was valued at USD 2.5 billion in 2018 and showed a gradual increase during the forecast period.

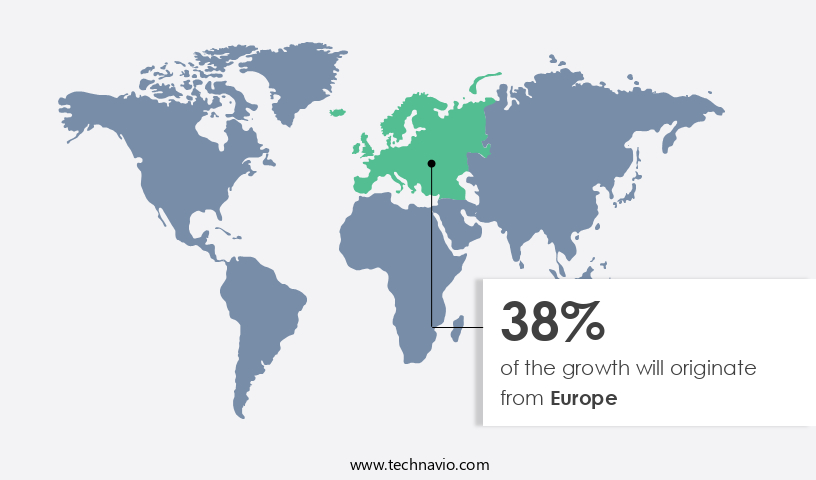

Regional Analysis

Europe is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in North America is anticipated to dominate due to the rising prevalence of immunodeficiency diseases and technological advancements in genetic and stem cell therapies. Immunodeficiency diseases, including Antibody Deficiency, Cellular Immunodeficiency, Innate Immune Disorders, and Genetic abnormalities, affect individuals of all ages and can lead to recurring infections, tumors, and genetic abnormalities. For instance, severe combined immunodeficiency (SCID), affecting infants, can be fatal without medical diagnostics intervention. The region's large patient population, changing lifestyles, and increasing healthcare expenditures contribute to the market's growth. Advanced diagnostic technologies, such as flow cytometry and next-generation sequencing, enable early diagnosis and effective treatment.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Primary Immunodeficiency Therapeutics Industry?

- Increasing prevalence of immunodeficiency diseases is the key driver of the market.The market is driven by the rising prevalence of various immunodeficiency diseases. Adenosine deaminase deficiency, a rare form of severe combined immunodeficiency syndrome (SCID), affects approximately 1 in 200,000 to 1,000,000 newborns worldwide and contributes to around 15% of SCID cases. Additionally, the World Health Organization (WHO) reported 1.5 million new HIV infections and 37.6 million people living with HIV globally in 2020. HIV causes acquired immunodeficiency disorder syndrome (AIDS), which is another significant immunodeficiency disease. In the US, the prevalence of primary immunodeficiency diseases (PIDDs) is estimated at 1 in 2000 individuals. These diseases result in recurring infections, tumors, and genetic abnormalities, leading to a need for various therapeutic interventions.

- Immunoglobulin replacement therapy, stem cell transplantation, antibiotic therapy, gene therapy, and immunomodulatory drugs are some of the common therapeutic approaches used to manage immunodeficiencies. Immunodeficiency diseases encompass a range of disorders, including antibody deficiency, cellular immunodeficiency, and innate immune disorders. They can manifest as deficiency anemia, hypothyroidism, lymphoma, neurologic disorders, arrhythmias, electrolyte disorders, coagulopathies, weight loss, rhinitis, atopic dermatitis, X-linked SCID, Wiskott Aldrich Syndrome, non-Hodgkin's lymphoma, rheumatoid arthritis, and various other conditions. Diagnostic tests, such as flow cytometry and next-generation sequencing, play a crucial role in identifying these disorders. Healthcare professionals rely on diagnostic technologies and supportive care to manage these complex conditions, leading to increased healthcare expenditure. Healthcare regulatory scenarios continue to evolve, with an emphasis on personalized medicine and targeted therapies, including biologics and gene therapies.

What are the market trends shaping the Primary Immunodeficiency Therapeutics market?

- Increasing R and D activities is the upcoming market trend.The market is experiencing growth due to the rising number of research and development (R&D) initiatives by companies. According to a recent study supported by the National Institutes of Health (NIH) in the US and the UK, 96% of children receiving new experimental lentiviral gene therapy for immunodeficiency diseases reported restored immune function. This underscores the importance of R&D in advancing primary immunodeficiency treatments and therapies. To gain a competitive edge, companies should focus on developing custom-made medicines for these conditions. Immunodeficiency diseases encompass various conditions, including antibody deficiency, cellular immunodeficiency, and innate immune disorders. These conditions can lead to recurring infections, tumors, genetic abnormalities, and immune dysfunction.

- Therapies for these diseases include immunoglobulin replacement therapy, stem cell and bone marrow transplantation, antibiotic therapy, gene therapy, and immunomodulatory drugs. Diagnostic tests, such as flow cytometry and next-generation sequencing, play a crucial role in identifying these conditions. Key diseases include X-linked SCID, Wiskott Aldrich Syndrome, non-Hodgkin's lymphoma, rheumatoid arthritis, deficiency anemia, hypothyroidism, lymphoma, neurologic disorders, arrhythmias, electrolyte disorders, coagulopathies, weight loss, rhinitis, and atopic dermatitis. Healthcare expenditure on these conditions is significant, and healthcare regulatory scenarios continue to evolve. Life line curves and diagnostic technologies are essential tools for understanding disease progression and treatment efficacy. Biologics and targeted therapies are increasingly being used to treat primary immunodeficiencies. Healthcare professionals play a vital role in diagnosing and managing these conditions.

What challenges does the Primary Immunodeficiency Therapeutics Industry face during its growth?

- Side effects of immunotherapy is a key challenge affecting the industry growth. Immunodeficiency diseases encompass a range of genetic abnormalities that impair the immune system's ability to fight infections effectively. These conditions include Antibody Deficiency, Cellular Immunodeficiency, and Innate Immune Disorders. Treatment options vary and may include Immunoglobulin Replacement Therapy, Stem Cell Transplantation, Antibiotic Therapy, Gene Therapy, and Immunomodulatory Drugs. Immunoglobulin Therapy involves administering antibodies to patients to boost their immune response. Antibiotics are used to treat infections caused by bacteria. Stem Cell Transplantation and Bone Marrow Transplantation are used to replace damaged or non-functional immune cells. Gene Therapy and Genetic Therapy offer potential cures for certain genetic disorders, such as X-linked SCID, Wiskott Aldrich Syndrome, and Non-Hodgkin's Lymphoma.

- Side effects from these therapies can vary and may include Rhinitis, Atopic Dermatitis, Arrhythmias, Electrolyte Disorders, Coagulopathies, Weight Loss, and Hypothyroidism. Neurologic disorders and Lymphoma are potential complications from Stem Cell Transplantation. Rheumatoid Arthritis and other autoimmune diseases may be exacerbated by Immunomodulatory Drugs. Healthcare professionals must closely monitor patients for these side effects and provide supportive care as needed. Diagnostic tests, such as Flow Cytometry and Next-Generation Sequencing, are essential for diagnosing these conditions and monitoring treatment progress. Targeted Therapies and Biologics offer more precise treatments for specific conditions. Healthcare expenditure on Immunodeficiency diseases continues to rise due to the increasing prevalence of these conditions and the high cost of treatments. Healthcare regulatory scenarios are evolving to address these challenges and ensure patient safety and access to effective treatments. Life line curves demonstrate the importance of early diagnosis and timely intervention in managing these conditions.

Exclusive Customer Landscape

The primary immunodeficiency therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the primary immunodeficiency therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, primary immunodeficiency therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADMA Biologics Inc. - Primary immunodeficiency therapies facilitate endogenous protein production within the body to address deficiencies. These treatments cater to various immunodeficiency conditions, enabling improved immune function and overall health.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADMA Biologics Inc.

- Astellas Pharma Inc.

- Baxter International Inc.

- Bayer AG

- Bio Products Laboratory Ltd.

- Biocon Ltd.

- Biotest AG

- CSL Ltd.

- Grifols SA

- Kedrion Spa

- LFB SA

- Lupin Ltd.

- Octapharma AG

- Pfizer Inc.

- Sanquin

- Takeda Pharmaceutical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Primary immunodeficiencies refer to a group of disorders characterized by the impairment of the immune system's ability to fight infections effectively. These disorders can be categorized into antibody deficiencies and cellular immunodeficiencies, which affect the production and function of antibodies and immune cells, respectively. Antibody deficiencies result from the insufficient production of immunoglobulins, proteins that play a crucial role in neutralizing pathogens. Immunoglobulin replacement therapy is the primary therapeutic approach for these conditions, which involves administering exogenous immunoglobulins to compensate for the deficiency. Cellular immunodeficiencies, on the other hand, result from the impairment of immune cells' function. Stem cell and bone marrow transplantation are the most common therapeutic options for these disorders, as they aim to restore the production of functional immune cells.

Innate immune disorders, which affect the body's first line of defense against infections, can also lead to primary immunodeficiencies. Antibiotic therapy is often used to manage infections in these cases, but there is a growing interest in alternative therapeutic approaches, such as gene therapy and immunomodulatory drugs. Immunodeficiency diseases can manifest in various forms, including rheumatoid disease, deficiency anemia, hypothyroidism, lymphoma, neurologic disorders, arrhythmias, electrolyte disorders, coagulopathies, weight loss, rhinitis, atopic dermatitis, X-linked SCID, Wiskott Aldrich Syndrome, non-Hodgkin's lymphoma, and rheumatoid arthritis, among others. The market is driven by the increasing prevalence of these disorders, the growing awareness of their impact on patients' quality of life, and the development of innovative therapeutic approaches.

Immunoglobulin therapy, antibiotics, and supportive care are the current mainstays of treatment, but gene therapy, genetic testing, and diagnostic technologies, such as flow cytometry and next-generation sequencing, are gaining popularity due to their potential to offer more targeted and effective treatments. Healthcare professionals play a critical role in the diagnosis and management of primary immunodeficiencies. The healthcare expenditure on these disorders is significant, with hospitals and clinics being the primary settings for their diagnosis and treatment. Healthcare regulatory scenarios also influence the market dynamics, with regulatory approvals and reimbursement policies impacting the availability and affordability of therapeutic options. In conclusion, the market is a dynamic and evolving landscape, driven by the growing prevalence of these disorders and the development of innovative therapeutic approaches.

The market is characterized by the use of various therapeutic modalities, including immunoglobulin therapy, antibiotics, gene therapy, and immunomodulatory drugs, among others. The role of healthcare professionals and regulatory scenarios in shaping the market dynamics cannot be overstated.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

136 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 1699.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Germany, China, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Primary Immunodeficiency Therapeutics Market Research and Growth Report?

- CAGR of the Primary Immunodeficiency Therapeutics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the primary immunodeficiency therapeutics market growth of industry companies

We can help! Our analysts can customize this primary immunodeficiency therapeutics market research report to meet your requirements.

RIA -

RIA -