Printing And Writing Paper Market Size 2025-2029

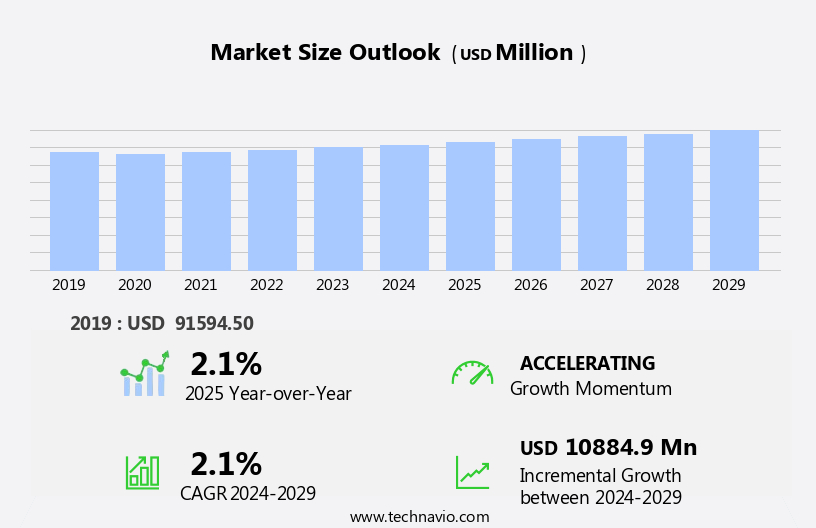

The printing and writing paper market size is forecast to increase by USD 10.88 billion at a CAGR of 2.1% between 2024 and 2029.

- The market is witnessing significant growth due to the emergence of various types of paper, catering to diverse applications. One notable trend is the increasing demand for handmade paper, which offers unique textures and aesthetics, particularly in high-end stationery and artisanal product segments. However, the market faces challenges from the increasing number of digital platforms that offer alternative solutions for communication and document management. This shift towards digital media may impact the traditional printing and writing paper industry, necessitating companies to explore new opportunities and adapt to evolving consumer preferences. The market is witnessing significant growth due to the emergence of various types of paper, including cotton-based and LED-compatible paper, catering to the needs of commercial printing, e-learning, and publishing industries. The increasing demand for data security and privacy is driving the usage of thermal paper for secure transactions in real estate, logistics, and e-commerce sectors.

- To capitalize on the market's dynamics, businesses must focus on innovation, product differentiation, and strategic partnerships, ensuring they cater to both traditional and emerging market segments. By staying attuned to consumer trends and addressing the challenges posed by digital media, companies can effectively navigate the market landscape and maintain a competitive edge.

What will be the Size of the Printing And Writing Paper Market during the forecast period?

- The market continues to evolve, driven by shifting consumer preferences, regulatory requirements, and technological advancements. Writing paper remains a staple in the industry, with a growing emphasis on sustainability and renewable resources. Paper regulations impact paper mills and wholesalers, shaping industrial goods production and distribution. Sustainable forestry and paperboard packaging are key trends, with paper bags and napkins gaining popularity in the consumer goods sector. Paper distribution channels expand, incorporating screen printing, specialty paper, and flexographic printing. Wood pulp and paper innovation fuel the development of bio-based materials and digital media. Circular economy principles influence paper recycling and the use of recycled fiber in various applications. Moreover, the market is witnessing a focus on information management, data security, and content marketing, leading to the adoption of advanced document management systems and certifications.

- Paper pricing and technology shape demand for offset paper, copy paper, and paper alternatives. The paper industry's continuous evolution encompasses paper finishing, text paper, printing paper, and various paper types, including bond paper, paper plates, and packaging paper, catering to diverse sectors like food and beverage and office supplies.

How is this Printing And Writing Paper Industry segmented?

The printing and writing paper industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

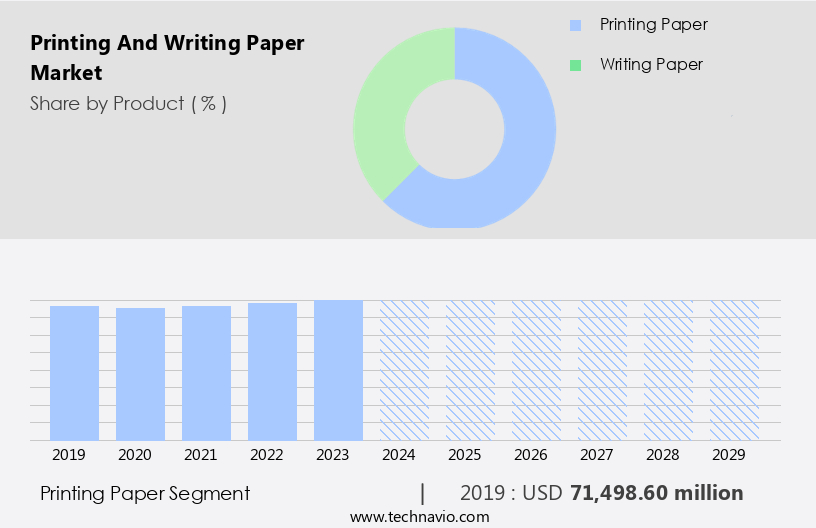

- Printing paper

- Writing paper

- Distribution Channel

- Offline

- Online

- Type

- Uncoated wood-free

- Coated wood-free

- Coated mechanical

- Uncoated mechanical

- Specialty papers

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The printing paper segment is estimated to witness significant growth during the forecast period. The market encompasses various types of paper used for diverse applications, including inkjet printer paper, laser print paper, and matte paper. These papers are essential for producing office stationery such as letterheads, documents, business cards, postcards, and invitation cards, as well as A4 size paper sheets. The global demand for printing papers is driven by the increasing need for printed book covers, magazines, and catalogs. The growing popularity of personal catalogs is a significant factor fueling this demand. Retailers are embracing multichannel marketing strategies to engage customers and boost sales, necessitating the mailing of printed catalogs. The emergence of multichannel shopping as a retail marketing trend further bolsters the demand for printing papers. Other trends include the use of chelating agents and bleach in decorative paper and the adoption of biocides to enhance the durability and resistance of labels and displays.

Sustainability is a critical consideration in the paper industry. Renewable resources, such as sustainable forestry and bio-based materials, are increasingly being used to manufacture paper. Paper mills and wholesalers are implementing paper technology to improve production efficiency and reduce their carbon footprint. Paper recycling plays a vital role in the circular economy, with recycled fiber being used to produce new paper products. Regulations governing paper production and distribution are becoming more stringent, with a focus on reducing waste and promoting sustainable practices. Industrial goods, such as corrugated cardboard, paperboard packaging, paper bags, and paper cups, are essential components of various industries, including consumer goods, food and beverage, and packaging. The market encompasses a diverse range of chemicals utilized in various applications within the pulp and paper industry. These applications include packaging, printing, labeling, and industrial supply chains. Commodity chemicals, such as caustic soda and chlorine, form the foundation of the industry.

The Printing paper segment was valued at USD 71.5 billion in 2019 and showed a gradual increase during the forecast period. Paper retailers and converters are using advanced paper finishing techniques, such as paper coating and paper plate making, to enhance the quality and appearance of their products. Writing paper, including bond paper and text paper, remains a significant segment of the market. Digital media, including digital paper and paperless office alternatives, are gaining traction but have not yet surpassed the demand for traditional paper products. Printing techniques, such as gravure printing, screen printing, and offset printing, continue to evolve, with innovations in paper machines and digital printing leading to improved product quality and efficiency. In summary, the market is a dynamic and evolving industry, with various players contributing to its growth and development. From paper mills and wholesalers to retailers and consumers, all stakeholders are adapting to changing market trends and prioritizing sustainability and efficiency.

Regional Analysis

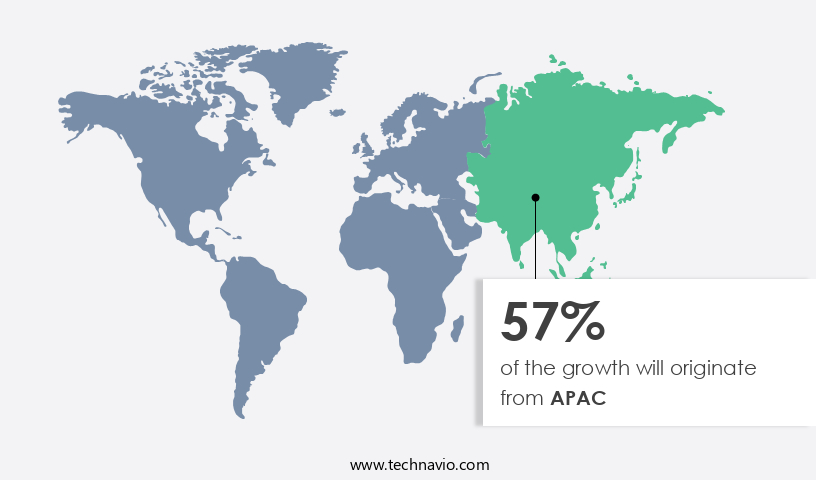

APAC is estimated to contribute 57% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market witnesses significant growth, particularly in the Asia Pacific (APAC) region. This region is the largest consumer of printing and writing paper due to increasing demand from schools, offices, governments, and businesses. Key countries driving the market in APAC include China, India, Japan, and South Korea. China is the leading market for printing and writing paper products, with a substantial demand generated from offices and schools. The shift towards using recycled paper is fueling the growth of the regional market. Paper mills and wholesalers supply various paper products, such as uncoated paper, coated paper, bond paper, text paper, and specialty paper, to meet the increasing demand. Product innovation and sustainability are key differentiators, as companies invest in developing eco-friendly chemicals and technologies for corrugated boxes, wrapping paper, cartons, display packaging, cups and trays, inserts and dividers, and tapes and labels.

Industrial goods, including paper technology, paper coating, gravure printing, screen printing, flexographic printing, and offset printing, contribute to the production of these paper products. Sustainability is a crucial factor in the printing and writing paper industry, with a focus on renewable resources, sustainable forestry, and circular economy. Paper recycling, fiber recovery, and the use of bio-based materials are essential practices in reducing the carbon footprint and promoting sustainability. Paper pricing, paper machines, and paper supply also play significant roles in the market dynamics. The demand for paper cups, paper plates, paper towels, office supplies, and packaging paper continues to rise in various industries, including food and beverage, consumer goods, and graphic arts.

Paper retailers distribute these products to various sectors, ensuring a steady supply and meeting the evolving demands of consumers and businesses.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Printing And Writing Paper Industry?

- The emergence and development of diverse types of printing and writing papers have been the primary catalysts driving the growth of the market. The global printing and writing paper industry experiences growth due to the diverse range of paper offerings. This variety expands the market's application scope, propelling its expansion during the forecast period.

- Paper made from freshly cut trees is used for high-quality, long-lasting paper products. The printing and writing paper industry's growth is fueled by the availability of various paper types and their diverse applications. From uncoated freesheet paper to paperboard packaging and specialty paper, each type plays a crucial role in driving market expansion. Sustainable forestry practices, efficient distribution networks, and ongoing paper innovation further support the industry's growth.

What are the market trends shaping the Printing And Writing Paper Industry?

- Handmade paper is gaining increasing popularity in the market, making it a noteworthy trend. The demand for this authentic and eco-friendly alternative to mass-produced paper continues to rise among consumers and businesses alike. The market is witnessing a shift towards eco-friendly alternatives, with handmade paper emerging as a significant trend. This type of paper is manufactured using 100% recycled materials, making it an environmentally sustainable choice. The production process of handmade paper consumes fewer resources, including energy, water, and chemicals, compared to traditional paper manufacturing. The increasing awareness of environmental concerns and the need to reduce carbon footprint are fueling the demand for handmade paper. Additionally, the use of waste products, such as cotton rags, for making writing and printing paper presents lucrative business opportunities. The recycled fibers used in handmade paper production require up to 40%-50% less energy and up to 70%-75% less water compared to conventional paper manufacturing.

- Office supplies, digital paper, paper cups, paper towels, and other paper products can all be made from recycled fibers. Fiber recovery and paper recycling are essential aspects of the paper industry, contributing to the sustainability of the market. The trend towards digital documents and paperless offices is also impacting the market, but the demand for paper products remains strong. Overall, the adoption of handmade paper is a step towards reducing the environmental impact of the printing and writing paper industry.

What challenges does the Printing And Writing Paper Industry face during its growth?

- The proliferation of digital platforms poses a significant challenge to industry growth, requiring businesses to adapt and innovate in order to remain competitive. The market faces significant challenges due to the increasing digitization trend. With the widespread use of digital devices such as computers, laptops, smartphones, and tablets, the demand for traditional paper products, including printing and writing paper, has decreased. The adoption of cloud services and virtual document storage solutions has further reduced the need for printing and writing paper. However, there are still various applications where paper remains essential. Paper alternatives, such as paper plates in the food and beverage industry, packaging paper, tissue paper, and paper pulp, continue to hold a strong position in the market.

- Paper finishing, paper converting, coated paper, and offset printing are also key areas of growth. Online printing services have gained popularity due to their convenience and cost-effectiveness, providing an opportunity for market expansion. Paper retailers and manufacturers must adapt to the changing market dynamics by focusing on innovation, quality, and sustainability. Meeting paper standards and offering eco-friendly options can help attract customers and maintain competitiveness. While the digital revolution has undeniably impacted the market, there are still numerous opportunities for growth in various applications and sectors.

Exclusive Customer Landscape

The printing and writing paper market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the printing and writing paper market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, printing and writing paper market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - The company specializes in supplying a diverse range of printing and writing papers to both large-scale and artisanal paper mills and retail shops.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Asia Pulp and Paper APP Sinar Mas

- Asia Symbol Shandong Pulp and Paper Co. Ltd.

- Domtar Corp.

- InterlogChile

- International Paper Co.

- ITC Ltd.

- Legion Paper

- Marusumi Paper Co. Ltd.

- Monadnock Paper Mills Inc.

- Mondi Plc

- Nippon Paper Industries Co. Ltd.

- PG Paper Co. Ltd.

- Sappi Ltd.

- Shulman Paper Co. Inc.

- Stora Enso Oyj

- Suzano SA

- UPM Kymmene Corp.

- West Coast Paper Mills Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Printing And Writing Paper Market

- In February 2024, international paper manufacturing company Smurfit Kappa announced the launch of its new range of recycled printing and writing paper, Greenpak, in response to increasing consumer demand for eco-friendly alternatives (Smurfit Kappa Press Release, 2024). This development marks a significant shift towards sustainable production methods in the market.

- In May 2025, paper and packaging giant, Mondi Group, entered into a strategic partnership with tech giant Microsoft to develop digital solutions for the paper industry. This collaboration aims to enhance the customer experience by integrating digital technologies into paper products, positioning Mondi as a leader in the digital transformation of the market (Mondi Group Press Release, 2025).

- In August 2024, Japanese paper manufacturer Oji Holdings Corporation completed the acquisition of Finnish paper company UPM's European paper business for USD 3.7 billion. This merger strengthened Oji's position as a global leader in the market, expanding its production capacity and market share (Reuters, 2024).

Research Analyst Overview

The market analysis reveals a dynamic industry with various trends shaping its growth. Paper caliper and tensile strength are crucial factors in determining product quality and suitability for specific applications. Paper transportation and warehousing play a significant role in ensuring efficient inventory management and timely delivery. The paper sector continues to evolve, with paper recovery rates and waste reduction initiatives driving sustainability. Paper efficiency is a key focus, with additives, coatings, and surface treatments enhancing product performance. Paper industry outlook is positive, with logistics and supply chain optimization essential for cost optimization. Paper testing, including burst strength, folding endurance, and opacity, ensures compliance with standards such as SFI, FSC, and PEFC certifications. These chemicals, which include cellulosic specialties, chelates, ethylene amines, metal alkyls, micronutrients, organic peroxides, polysulfides, re-dispersible powder polymers, salt specialties, sulfur products, dyes, pigments, and coating chemicals, are essential for manufacturing high-quality paper used in commercial printing, labels, retail labels, newsprint, industrial papers, and more

Paper perforation, die-cutting, embossing, and converting processes add value to the final product. Paper sizing, brightness, and pigments contribute to product aesthetics, while fillers and resins improve paper properties. Recycling programs and traceability are critical for sustainability and customer trust. Paper smoothness and paper grammage are essential considerations for various applications. Overall, the market is a complex ecosystem, requiring a comprehensive understanding of these factors to stay competitive.

The Printing and Writing Paper Market is evolving with innovations in paper brightness, paper opacity, and paper whiteness, ensuring superior print quality. Strength properties like paper tensile strength, paper tear strength, paper burst strength, and paper folding endurance enhance durability. Advanced paper coatings, paper additives, paper pigments, paper fillers, and paper resins improve texture and ink absorption. Key treatments include paper sizing agents, paper surface treatment, paper calendering, paper embossing, paper diecutting, paper laminating, and paper converting processes for diverse applications. Strict paper quality control, paper standards compliance, and paper certification, such as FSC certification, SFI certification, and PEFC certification ensure sustainability. Efficient paper logistics, paper warehousing, paper inventory management, paper supply chain, and paper traceability optimize distribution.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Printing And Writing Paper Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

222 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.1% |

|

Market growth 2025-2029 |

USD 10.88 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.1 |

|

Key countries |

China, US, India, Germany, Japan, UK, South Korea, Brazil, Australia, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Printing And Writing Paper Market Research and Growth Report?

- CAGR of the Printing And Writing Paper industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the printing and writing paper market growth of industry companies

We can help! Our analysts can customize this printing and writing paper market research report to meet your requirements.

RIA -

RIA -