Process Instrumentation Market Size 2024-2028

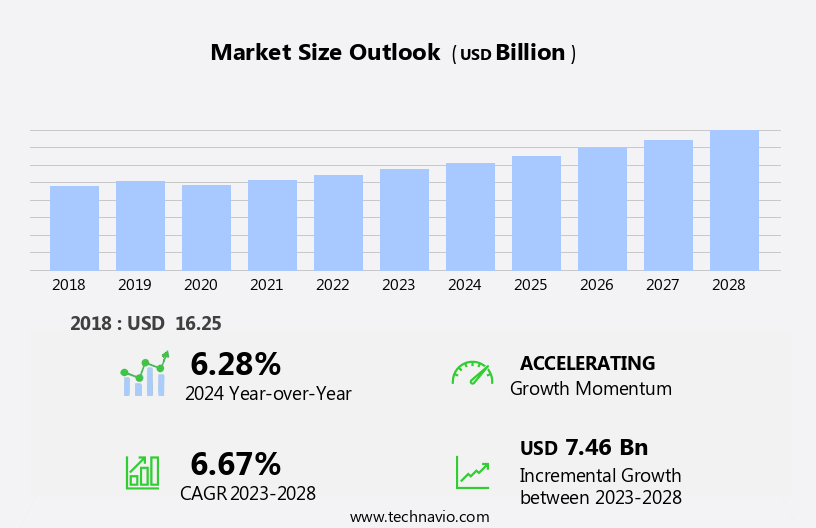

The process instrumentation market size is forecast to increase by USD 7.46 billion at a CAGR of 6.67% between 2023 and 2028.

- The rising demand for automation in manufacturing processes is a key driver of the process instrumentation market. In line with this, the rising demand for wireless field instruments is emerging as a key trend. These instruments offer increased flexibility, ease of installation, and reduced maintenance costs, making them an attractive choice for industries seeking to optimize production efficiency. Wireless solutions also enable real-time data monitoring and analysis, enhancing operational decision-making and driving innovation in process automation.

- The adoption of advanced technologies, such as wireless communication and the Internet of Things (IoT), is driving the market's growth. These technologies enable data analytics, leading to improved operational efficiency and productivity. However, safety concerns due to faulty instruments pose a significant challenge to market growth.

What will be the Size of the Process Instrumentation Market During the Forecast Period?

- The market encompasses the supply of equipment and systems used for recording, positioning, and controlling various process parameters such as flow, pressure, level, temperature, humidity, and others in industrial applications. This market is driven by the rising trend of industrial automation, which aims to enhance asset utilization, improve product quality, ensure safety, and reduce energy consumption and emission.

- The increasing focus on energy efficiency and environmental impact has further fueled the demand for advanced process instrumentation solutions. However, the high initial investments and cybersecurity risks associated with these systems pose challenges for market growth. Communication protocols like Profibus PA facilitate the integration of process instrumentation equipment into industrial automation systems.

- Ex-proof and intrinsically safe devices cater to industries with hazardous environments. Economic factors and industry-specific applications also influence the market dynamics. Competitor analysis is crucial to understanding the competitive landscape and staying abreast of the latest trends and innovations.

How is this Process Instrumentation Industry segmented and which is the largest segment?

The process instrumentation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

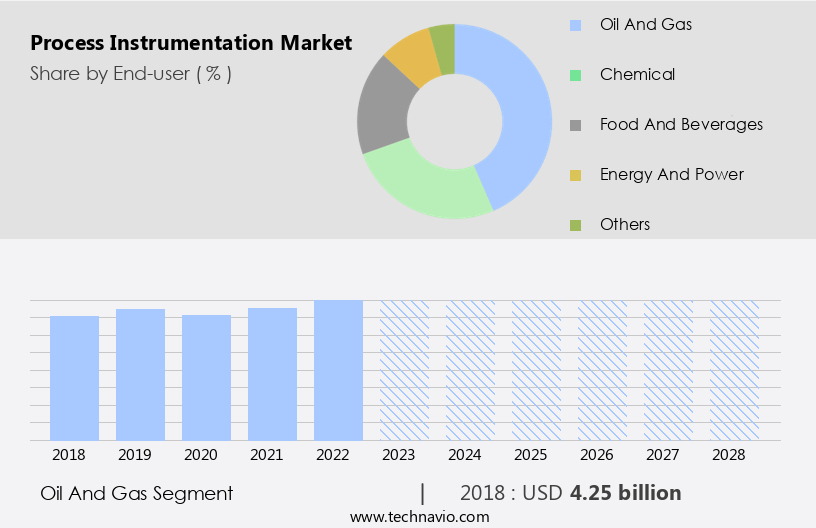

- End-user

- Oil and gas

- Chemical

- Food and beverages

- Energy and power

- Others

- Type

- Field instrument

- Control valve

- Analyzer

- Instrument

- Transmitter

- Control Valve

- Technology

- Programmable Logic Controller (PLC)

- Distributed Control System (DCS)

- Supervisory Control and Data Acquisition (SCADA)

- Manufacturing Execution System (MES)

- Geography

- APAC

- China

- India

- North America

- Canada

- US

- Europe

- UK

- South America

- Middle East and Africa

- APAC

By End-user Insights

The oil and gas segment is estimated to witness significant growth during the forecast period. The market plays a pivotal role in various industries, including manufacturing, energy, and utilities, by enhancing process control systems through the use of sensors, transmitters, switches, and gauges. These instruments enable asset utilization, energy efficiency, emission reduction, and recording of data points from connected equipment. The increasing adoption of automation, labor shortages, and intelligent robotics in production processes necessitates the deployment of precise and accurate process instrumentation equipment. The importance of absolute reliability, long-term contracts, and safety in business operations drives the demand for process instrumentation solutions. Key applications include flow control valves, pressure, level, temperature, humidity, and communication protocols such as Profibus PA, Foundation Fieldbus, and HART.

The market is influenced by economic factors, digital transformation, and the Internet of Things (IoT), leading to the integration of real-time monitoring and M2M communication. Industries like power generation, mining and metals, pharmaceuticals, and agriculture and livestock benefit from process instrumentation, with significant growth expected In the chemical, food and beverages, and water availability sectors. The Energy Information Administration (IEA) and Industrial Bank of China (IBEF) report that the market is expected to grow due to increasing demand for product quality, safety, and environmental impact considerations. Competitor analysis reveals that companies offering process instrumentation solutions include Equilibar, SDO valves, OleumTech, Rising Industrial Automation, and others.

The market faces challenges such as high initial investments, cybersecurity risks, and economic factors. Despite these challenges, the market is expected to continue growing due to the increasing need for process optimization and sustainability.

Get a glance at the share of various segments. Request Free Sample

The Oil and gas segment was valued at USD 4.25 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

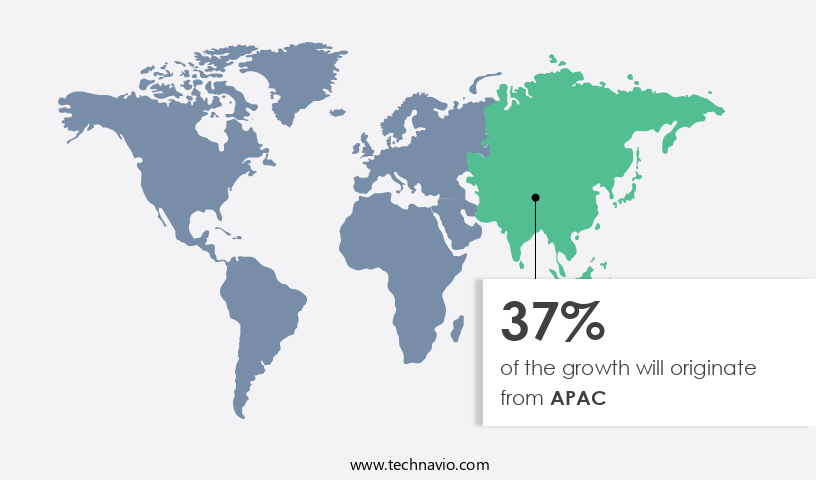

APAC is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in APAC is projected to experience significant growth, with China, South Korea, Japan, India, Thailand, Malaysia, and Australia being key contributors. The increasing manufacturing sector expansion In the region, driven by population growth and rising per capita income, is a major factor fueling market growth. In China, a priority is placed on improving water quality and infrastructure, with substantial investments in advanced water technologies, such as wastewater treatment, recycling, and membrane technologies. The Chinese government allocated over USD104 billion towards water infrastructure development in 2019. Process control systems, including Asset utilization, Energy efficiency, and Emission reduction, are integral to manufacturing businesses.

Process instrumentation equipment, such as sensors, transmitters, switches, and gauges, enable real-time monitoring, automation, and M2M communication. Key sectors rely on process instrumentation for product quality, safety, and environmental iImpact. Companies offer a range of solutions to meet the diverse needs of various industries. The market's high initial investments necessitate careful consideration of Industry applications, competitor analysis, and communication protocols.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Process Instrumentation Industry?

Rising demand for automation in manufacturing processes is the key driver of the market.

- Process instrumentation plays a crucial role in optimizing manufacturing processes by providing real-time data on various parameters such as flow, pressure, level, temperature, and humidity. Process control systems rely on this data for asset utilization, energy efficiency, emission reduction, and maintaining product quality and safety. The market for process instrumentation equipment is driven by economic factors, including the need for absolute reliability, accuracy, and precision in various industry applications. Automation, digital transformation, and the Internet of Things (IoT) are transforming manufacturing businesses by enabling M2M communication between connected equipment and intelligent robotics. This enables labor-intensive production processes to become more efficient and sustainable, addressing labor shortages and environmental impact.

- The serviceable addressable market for process instrumentation is vast, with significant opportunities in sectors such as energy and utilities, metals and mining, chemical, food and beverages, and pharmaceuticals. Key players In the market include Equilibar, SDO valves, OleumTech, and others. Process instrumentation is essential for industries such as power generation and transportation, where high initial investments and cybersecurity risks require absolute reliability and accuracy. Communication protocols like Profibus PA, Foundation Fieldbus, and HART enable seamless integration of field instruments into control systems. Ex-Proof/Intrinsically safe sensors and transmitters are critical for industries with hazardous environments, such as agriculture and livestock, mining and metals, and oil and gas.

- Competitor analysis, industry trends, and economic factors are essential considerations for businesses looking to invest in process instrumentation.

What are the market trends shaping the Process Instrumentation Industry?

Rising demand for wireless field instruments is the upcoming market trend.

- Process instrumentation plays a crucial role in optimizing process control systems in various industries, including manufacturing businesses. The integration of advanced technologies such as M2M communication, automation, and intelligent robotics has led to improved asset utilization, energy efficiency, and emission reduction. Process instrumentation equipment, including sensors, transmitters, switches, and gauges, record and measure critical data points in real-time, enabling precise controlling and monitoring of production processes. Absolute reliability and accuracy are essential for maintaining product quality, safety, and environmental impact. The serviceable addressable market for process instrumentation is significant, with applications in sectors such as energy and utilities, metals and mining, chemical, food and beverages, and pharmaceutical industries.

- Key technologies include flow control valves, pressure, level, temperature, and humidity sensors, and communication protocols such as Profibus PA, Foundation Fieldbus, and HART. Despite the benefits, high initial investments and cybersecurity risks are challenges for businesses considering process instrumentation upgrades. Economic factors, digital transformation, and the increasing importance of sustainability also influence business investment decisions. The Internet of Things (IoT) and smart sensors enable real-time monitoring and data analysis, while transportation and power plants require specialized field instruments. Competitor analysis and industry applications continue to drive innovation in process instrumentation, with companies such as Equilibar, SDO valves, and OleumTech offering solutions for various industries.

What challenges does the Process Instrumentation Industry face during its growth?

Safety issues due to faulty instruments is a key challenge affecting the industry growth.

- Process instrumentation plays a pivotal role in ensuring safety and efficiency in various industries by providing precise measurements for process control systems. These measurements are essential for optimizing asset utilization, enhancing energy efficiency, and reducing emissions. Process instrumentation equipment, including sensors, transmitters, switches, and gauges, enable real-time monitoring and automation of manufacturing processes. The importance of absolute reliability and accuracy in process measurements is evident in industries such as energy and utilities, chemicals, food and beverages, and metals and mining. For instance, a faulty measurement instrument in a power plant could lead to inefficient energy consumption or even safety hazards.

- In the food and beverage industry, inaccurate temperature readings could affect product quality, while incorrect pressure measurements In the mining sector could impact equipment performance and worker safety. Moreover, the integration of M2M communication and the Internet of Things (IoT) in process instrumentation has led to intelligent automation and remote monitoring capabilities, addressing labor shortages and enabling businesses to make data-driven decisions. However, high initial investments and cybersecurity risks are some economic factors that may hinder market growth. Key industry applications of process instrumentation include flow control valves, pressure, level, temperature, humidity, and communication protocols such as Profibus PA, Foundation Fieldbus, and HART.

- Additionally, the market encompasses various sectors, including agriculture and livestock, mining and metals, power generation, pharmaceuticals, and water availability, among others. Competitor analysis and understanding industry trends are crucial for businesses looking to invest in process instrumentation.

Exclusive Customer Landscape

The process instrumentation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the process instrumentation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, process instrumentation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

ABB Ltd. - The market encompasses temperature transmitters and sensors, as well as pressure transmitters and remote seals, catering to the life sciences sector. These instruments facilitate process monitoring and control, ensuring optimal performance and compliance with industry regulations. Temperature transmitters and sensors measure and transmit temperature data, enabling real-time process monitoring and temperature maintenance. Pressure transmitters and remote seals, on the other hand, measure and transmit pressure data, ensuring process safety and efficiency. By implementing these advanced process instrumentation solutions, organizations In the life sciences industry can enhance their operational efficiency, product quality, and regulatory compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Delta Electronics Inc.

- Emerson Electric Co.

- Endress Hauser Group Services AG

- Fuji Electric Co. Ltd.

- General Electric Co.

- Hitachi Ltd.

- Honeywell International Inc.

- KROHNE Messtechnik GmbH

- Metso Outotec Corp.

- Mitsubishi Electric Corp.

- OMRON Corp.

- Pepperl and Fuchs SE

- Rockwell Automation Inc.

- Schlumberger Ltd.

- Schneider Electric SE

- Siemens AG

- Teledyne Technologies Inc.

- Titan Co. Ltd.

- Yokogawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Process instrumentation plays a crucial role in optimizing production processes and enhancing asset utilization in various manufacturing businesses. By providing real-time data on critical process parameters such as flow, pressure, level, temperature, and humidity, process instrumentation equipment enables manufacturers to improve energy efficiency, reduce emissions, and ensure product quality and safety. The adoption of process instrumentation is driven by several market dynamics. The increasing focus on sustainability and environmental impact reduction has led manufacturers to prioritize energy efficiency and water availability In their operations. Moreover, the rise of industrial automation and digital transformation has resulted In the integration of process instrumentation with connected equipment and M2M communication, enabling intelligent robotics and automation systems to make data-driven decisions in real-time.

Manufacturing businesses across industries, including chemical, food and beverages, metals and mining, pharmaceuticals, energy and utilities, and power generation, are investing in process instrumentation to enhance their production processes. The serviceable addressable market for process instrumentation is expected to grow significantly due to these factors. However, the high initial investments required for process instrumentation and cybersecurity risks associated with connected equipment are some of the challenges hindering the growth of the market. Moreover, economic factors such as labor shortages and business investment trends also influence the adoption of process instrumentation. The market is witnessing significant innovation, with companies developing new technologies and communication protocols such as Profibus PA, Foundation Fieldbus, and HART to improve accuracy, precision, and absolute reliability.

Transmitters, switches, gauges, and flow control valves are some of the key types of process instrumentation equipment in demand. The market for process instrumentation is diverse, with applications ranging from agriculture and livestock to mining and metals, power generation, and transportation. The market is competitive, with several players offering a range of products and services to cater to the varying needs of different industries. Competitor analysis is essential to understand market trends and positioning In the market. In conclusion, process instrumentation plays a vital role in optimizing production processes and enhancing asset utilization in manufacturing businesses. The market is driven by several factors, including sustainability, digital transformation, and industrial automation.

However, challenges such as high initial investments and cybersecurity risks need to be addressed to fully realize the potential of process instrumentation.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

191 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.67% |

|

Market growth 2024-2028 |

USD 7.46 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.28 |

|

Key countries |

US, Canada, China, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Process Instrumentation Market Research and Growth Report?

- CAGR of the Process Instrumentation industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the process instrumentation market growth of industry companies

We can help! Our analysts can customize this process instrumentation market research report to meet your requirements.

RIA -

RIA -