Saudi Arabia Telecom Market Size and Growth Forecast 2026-2030

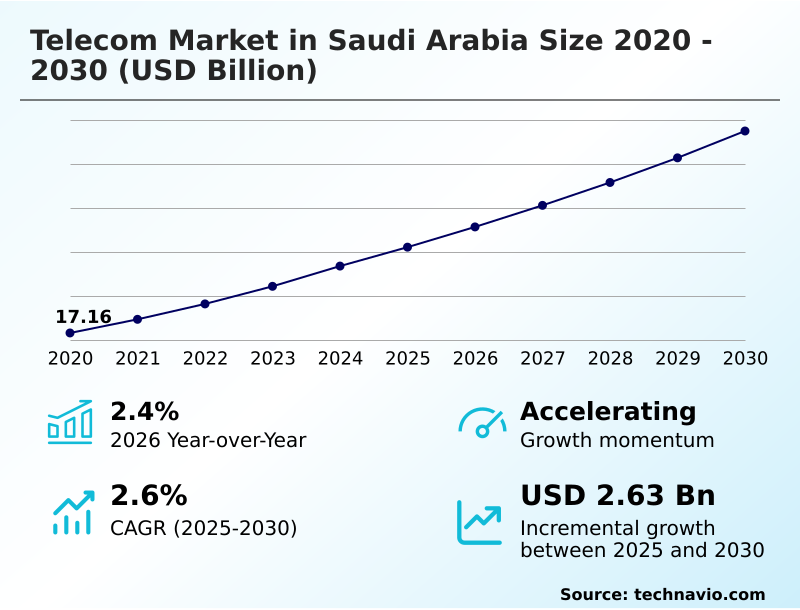

The Saudi Arabia Telecom Market size was valued at USD 19.11 billion in 2025 growing at a CAGR of 2.6% during the forecast period 2026-2030.

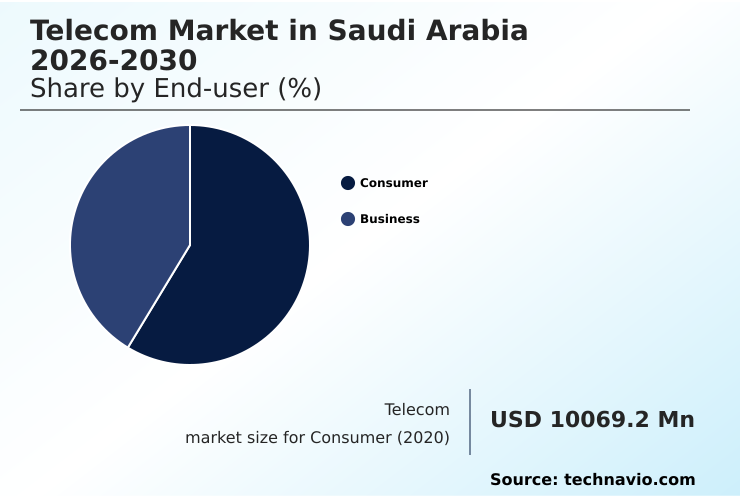

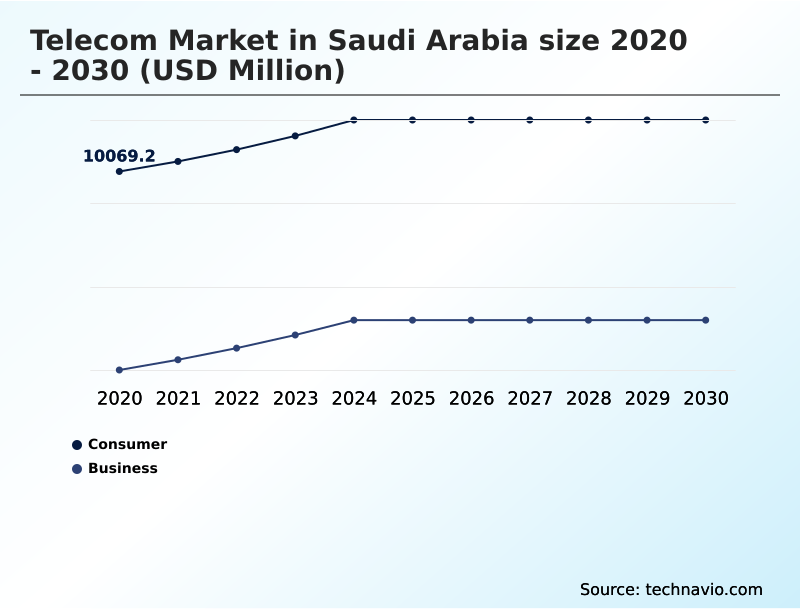

The Consumer segment by End-user was valued at USD 10.84 billion in 2024, while the Wireless segment holds the largest revenue share by Type.

The market is projected to grow by USD 4.58 billion from 2020 to 2030, with USD 2.63 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Saudi Arabia Telecom Market Overview

The telecom market in Saudi Arabia is undergoing a significant transformation, propelled by national digitalization goals. With a year-over-year growth of 2.4%, the sector's expansion is underpinned by a surge in data consumption and enterprise adoption of advanced connectivity. A key operational reality is the deployment of private 5G networks in industrial zones; for instance, a large-scale logistics hub implementing such a network to manage automated guided vehicles and real-time inventory tracking can achieve a significant reduction in operational errors and improve throughput. This shift necessitates robust carrier aggregation technology and predictive network analytics to maintain quality of service. However, the market also contends with the complexities of network slicing for 5G to serve diverse enterprise needs. Investment in fiber to the home (FTTH) infrastructure continues, but the high cost of extending networks to remote areas remains a persistent issue, prompting exploration into non-terrestrial networks (NTN). The market is defined by a push towards smart city connectivity solutions and the integration of managed IT services.

Drivers, Trends, and Challenges in the Saudi Arabia Telecom Market

Strategic decision-making in the telecom market in Saudi Arabia is increasingly complex, balancing technological advancement with operational realities. The impact of 5G on industrial automation is a primary consideration, with procurement teams evaluating how deploying private 5G for smart cities can improve public services. However, this is constrained by the challenges of fiber optic network expansion into remote territories.

This has heightened interest in the investment trends in non-terrestrial networks for remote coverage, although their cost-benefit profile is still under scrutiny. Simultaneously, the role of AI in telecom network optimization is central to managing network performance and security. Cybersecurity threats in IoT telecom networks require a robust defense strategy, forcing operators to look beyond traditional security perimeters.

Compliance with the Communications, Space and Technology Commission's (CSTC) regulations for data residency in telecom is non-negotiable. An industrial facility in a remote economic zone, for instance, must ensure its IoT sensor data, transmitted over a satellite backhaul, is processed and stored in compliance with these rules, impacting architectural decisions.

Operators also focus on strategies for reducing customer churn with predictive analytics, with some achieving churn reduction rates more than double those of competitors who rely on reactive measures. This confluence of technological opportunity and regulatory rigor defines the market's trajectory.

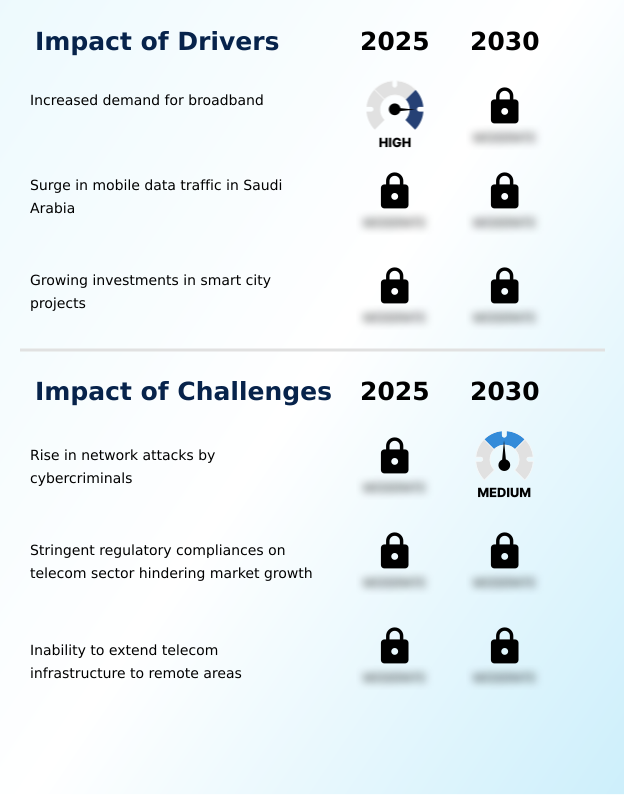

Primary Growth Driver: The increased demand for high-speed broadband, driven by digital lifestyle adoption and business transitions to cloud operations, is a key driver for the market.

Demand for high-capacity connectivity is a primary market driver, fueled by both consumer and enterprise needs.

The aggressive rollout of fiber to the home (FTTH) and the deployment of fixed wireless access (FWA) are direct responses to the demand for high-speed internet for remote working enablement and e-government service delivery.

In parallel, investments in smart city connectivity solutions are creating new ecosystems of connected devices, from smart energy grid communication to real-time data monitoring for public services.

These initiatives rely heavily on robust Internet of Things (IoT) connectivity and advanced mobile networks that utilize carrier aggregation technology.

To manage the resulting explosion in data, operators are increasingly employing big data analytics for networks to optimize performance and plan capacity upgrades, underpinning the nation's broader digital transformation initiatives.

Emerging Market Trend: Significant investment in the development and commercialization of 5G networks stands as an influential market trend. This is driving a shift toward high-performance networks that support industrial and digital economy use cases.

Key trends are reshaping service delivery and operational efficiency. The maturation of 5G standalone architecture is enabling advanced applications through network slicing for 5G, allowing operators to offer customized service levels for enterprise clients. This is complemented by the integration of predictive network analytics and cloud computing integration, which facilitate proactive network management and resource optimization.

On the customer-facing side, unified communications platforms are evolving into comprehensive collaboration suites, driven by the demand for hybrid work models. For instance, a multinational enterprise using a unified communications as a service (UCaaS) solution can ensure consistent connectivity for its workforce, governed by a single service level agreement.

This shift is supported by ongoing 5G advanced research and proactive customer management strategies, including the use of sentiment analysis in customer service to improve satisfaction.

Key Industry Challenge: The rise in sophisticated network attacks by cybercriminals presents a key challenge to the market, threatening the integrity of critical digital infrastructure.

The market faces significant challenges related to security, regulation, and infrastructure reach. The escalating threat of sophisticated cyberattacks requires a shift toward a zero trust architecture adoption and the implementation of advanced network encryption to secure sensitive data.

Navigating regulatory compliance for data residency in telecom, as mandated by the Communications, Space and Technology Commission (CSTC), adds complexity, particularly for operators leveraging sovereign cloud solutions and managing cross-border terrestrial links. Furthermore, extending connectivity to remote areas remains a logistical and financial hurdle, prompting investment in alternative technologies like non-terrestrial networks (NTN) and high-altitude platform stations (HAPS).

The adoption of software-defined networking (SDN) offers greater network agility but also introduces new security management considerations that must be addressed to ensure network integrity.

Explore Full Market Dynamics Analysis Request Free Sample

Saudi Arabia Telecom Market Segmentation

The saudi arabia telecom industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

End-user Segment Analysis

The consumer segment is estimated to witness significant growth during the forecast period.

The consumer segment represents a highly dynamic landscape, accounting for approximately 58% of the market. This segment is characterized by a digitally native population with high per-capita data consumption rates, driven by demand for video streaming and mobile gaming.

The adoption of the eSIM activation process is simplifying user onboarding, while AI-assisted customer service and intelligent chatbot deployment are becoming standard for enhancing user experience.

Operators are leveraging mobile data traffic management to handle network loads, especially with the rise of augmented reality shopping and immersive virtual reality tourism applications.

The focus remains on delivering high-speed, low-latency connectivity for digital content delivery to meet the expectations of a tech-savvy user base, guided by the service standards set by the Communications, Space and Technology Commission.

The Consumer segment was valued at USD 10.84 billion in 2024 and showed a gradual increase during the forecast period.

Customer Landscape Analysis for the Saudi Arabia Telecom Market

The saudi arabia telecom market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the saudi arabia telecom market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Saudi Arabia Telecom Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the saudi arabia telecom market industry.

Etihad Etisalat Co. - Core offerings include 5G RAN infrastructure, managed services, and comprehensive network modernization support for major telecommunications operators.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Etihad Etisalat Co.

- Huawei Technologies Co. Ltd.

- Nokia Corp.

- Orange SA

- Proximus Group

- Saudi Telecom Co.

- Telefonaktiebolaget Ericsson

- Teleperformance SE

- Virgin Mobile KSA

- Vodafone Group Plc

- Zain KSA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Saudi Arabia Telecom Market

- In April 2025, Salam completed a major fiber expansion project across several residential districts in Jeddah, delivering high-speed wireline connectivity to thousands of new households.

- In March 2025, the Communications Space and Technology Commission published a network performance report confirming Saudi Arabia's leadership position in mobile download speeds and 5G network availability.

- In February 2025, stc group announced a significant investment to enhance digital consumer experiences through AI-driven personalized services and expanded 5G Advanced coverage.

- In January 2025, stc Bank received final regulatory approval to operate as a full digital bank, marking a key convergence of telecommunications and financial services in the kingdom.

Research Analyst Overview: Saudi Arabia Telecom Market

The telecom market in Saudi Arabia is characterized by a rapid evolution in service delivery and infrastructure, with a notable year-over-year growth of 2.4%. The push for digital transformation is compelling operators to move beyond basic connectivity and invest heavily in technologies like 5G standalone architecture and predictive network analytics.

Boardroom decisions are now intrinsically linked to technology roadmaps; for instance, the capital allocation for private 5G networks is weighed against the potential for new revenue streams from enterprise clients in logistics and manufacturing. The integration of unified communications platforms and managed IT services into core offerings is becoming a key differentiator.

Compliance with the Communications, Space and Technology Commission (CSTC) framework for cybersecurity in telecom networks dictates investment priorities in security infrastructure. As such, the deployment of network slicing for 5G is not merely a technical upgrade but a strategic imperative to offer customized, secure services to various enterprise verticals, directly impacting profitability and market positioning.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Saudi Arabia Telecom Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 167 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.6% |

| Market growth 2026-2030 | USD 2633.9 million |

| Market structure | Concentrated |

| YoY growth 2025-2026(%) | 2.4% |

| Key countries | Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Saudi Arabia Telecom Market: Key Questions Answered in This Report

-

What is the expected growth of the Saudi Arabia Telecom Market between 2026 and 2030?

-

The Saudi Arabia Telecom Market is expected to grow by USD 2.63 billion during 2026-2030, registering a CAGR of 2.6%. Year-over-year growth in 2026 is estimated at 2.4%%. This acceleration is shaped by increased demand for broadband, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Consumer, and Business), Type (Wireless, and Wireline), Application (Residential, and Commercial) and Geography (Middle East and Africa). Among these, the Consumer segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Middle East and Africa. Country-level analysis includes Saudi Arabia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increased demand for broadband, which is accelerating investment and industry demand. The main challenge is rise in network attacks by cybercriminals, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Saudi Arabia Telecom Market?

-

Key vendors include Etihad Etisalat Co., Huawei Technologies Co. Ltd., Nokia Corp., Orange SA, Proximus Group, Saudi Telecom Co., Telefonaktiebolaget Ericsson, Teleperformance SE, Virgin Mobile KSA, Vodafone Group Plc and Zain KSA. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Saudi Arabia Telecom Market Research Insights

Market dynamics are shaped by enterprise and consumer demands, with the consumer segment constituting roughly 58% of the market. Digital transformation initiatives are compelling businesses to adopt advanced enterprise connectivity solutions, while proactive customer management through AI enhances retention. Operators are pursuing streaming platform partnerships and digital banking integration to diversify revenue streams.

The framework established by the Communications, Space and Technology Commission (CSTC) governs service quality and competition. For example, a large enterprise might leverage a unified communications as a service (UCaaS) platform for global collaboration, relying on the provider's adherence to data residency rules. This competitive environment encourages innovations in digital self-onboarding and proactive network maintenance to meet evolving customer expectations.

We can help! Our analysts can customize this saudi arabia telecom market research report to meet your requirements.

RIA -

RIA -