Screenless Display Market Size 2024-2028

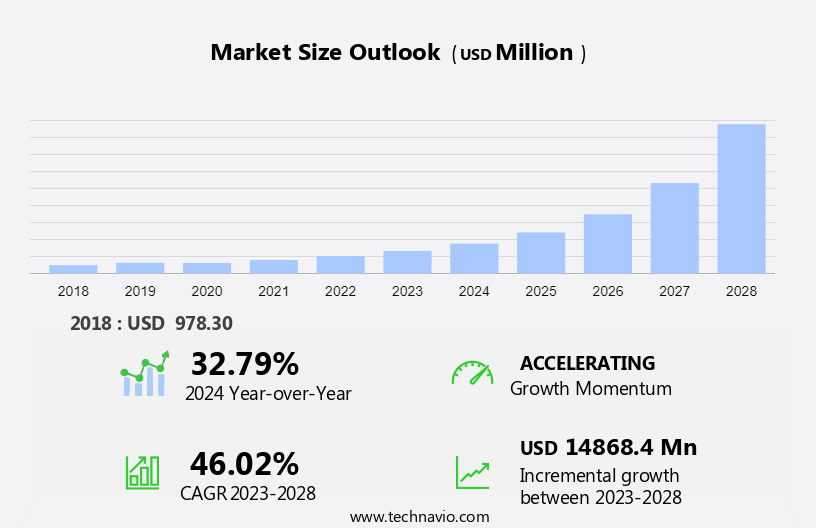

The screenless display market size is forecast to increase by USD 14.87 billion at a CAGR of 46.02% between 2023 and 2028. The market is experiencing significant advancements in visual display technology, with a focus on next-generation holographic solutions and 3D projection. The increasing demand for more convenient and portable display options, as well as growing interest in holographic displays, are driving market growth. However, the high cost of screenless display devices remains a challenge. Privacy and security concerns are also emerging as important factors, as these technologies may raise questions regarding data protection and potential misuse. To stay competitive, market participants must continue investing in research and development to address these challenges and offer innovative, cost-effective solutions.

The screenless display market is poised for significant growth, driven by innovations in visual image screen less display systems. These advanced solutions, including Laser Valve Video Projectors and Internet Glasses, offer experiences without the limitations of traditional screens. With low power and space requirements, they are ideal for diverse applications in the manufacturing field and transportation system. Multi touch capabilities enhance user interaction, while tools like CUBIT and micro vision are revolutionizing how we visualize data. The emergence of 3D scope animations and the EYE file format further enrich the user experience. Additionally, the aerospace & defense sectors are exploring hologram projection for enhanced operational efficiency, solidifying the importance of screen less TV technology in various industries. The development of screen less displays, such as laser valve video projector and multi-touch interfaces, is transforming machines in various sectors, including transportation and aerospace, by offering low power & space requirements while enhancing operational efficiency.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

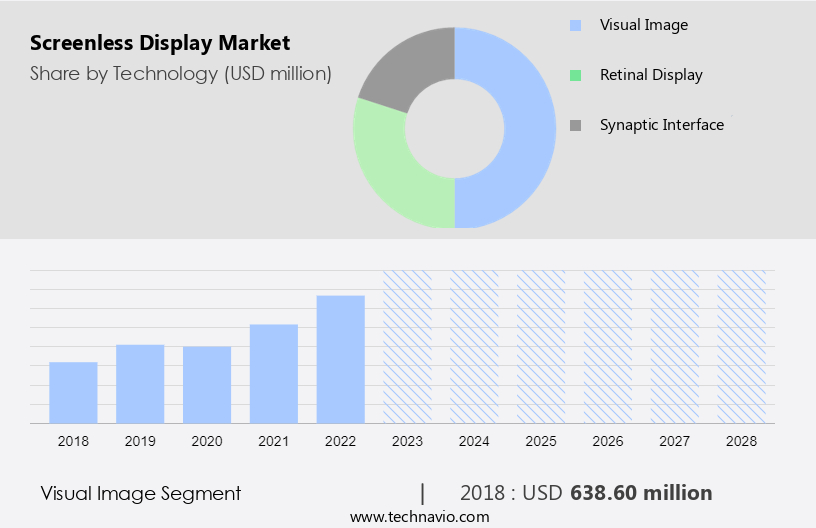

- Visual image

- Retinal display

- Synaptic interface

- Application

- Automotive

- Consumer electronics

- Aerospace and defense

- Healthcare

- Commercial

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- Middle East and Africa

- South America

- North America

By Technology Insights

The visual image segment is estimated to witness significant growth during the forecast period. Visual image technology, which includes patents on holograms, retinal displays, and synaptic interfaces, is transforming the way businesses connect with their audiences. This technology projects high-definition images directly onto surfaces, eliminating the need for traditional LCD panels. The engaging experience offered by visual image technology is particularly appealing in advertising and marketing, where companies seek innovative methods to captivate consumers. From projecting images on buildings and vehicles to implementing retinal displays and holograms, this technology provides a unique and attention-grabbing platform for communicating messages and promoting products or services.

Get a glance at the market share of various segments Request Free Sample

The visual image segment accounted for USD 638.60 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

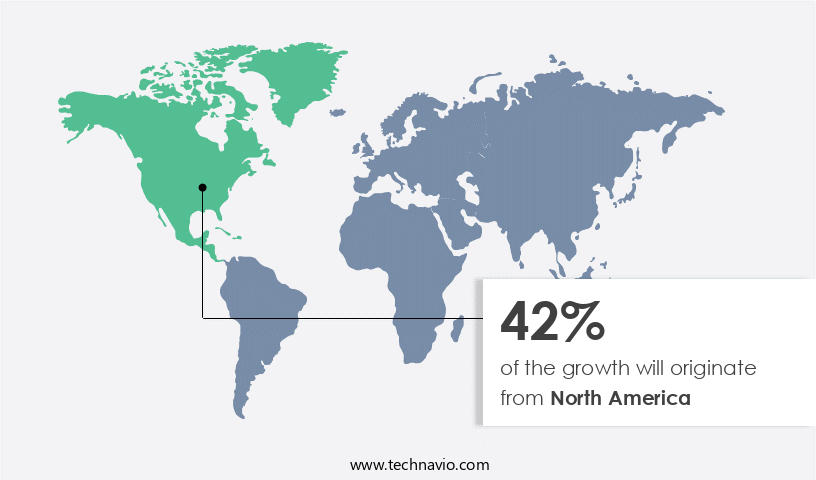

North America is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the market is experiencing significant growth due to several key factors. The region's expanding population and rising living standards have led to an increasing demand for advanced and innovative visual image display technologies. One of the primary drivers of this market's growth in North America is the presence of technologically advanced hubs, such as Silicon Valley in California. This region is renowned for its thriving tech industry, attracting major players in the field of display technologies.

For instance, Magic Leap, an American company based in Florida, has pioneered an augmented reality display called Magic Leap One, which utilizes Retinal Direct display technology. Further, pico projectors and Virtual Retinal Display are other screenless display technologies gaining popularity in the region. The market is further bolstered by the medical field's adoption of these technologies for various applications.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Rising demand for more convenient and portable display solutions is the key driver of the market. The market in the United States is experiencing notable growth due to the escalating requirement for more portable and convenient display solutions. This trend is fueled by several factors, including the escalating popularity of wearable technology, the increasing preference for entertainment experiences, and the necessity of sophisticated visualization solutions in sectors such as healthcare and transportation. One of the primary drivers is the burgeoning demand for wearable technology. With the emergence of smartwatches, fitness trackers, and augmented reality glasses, consumers are increasingly relying on screenless displays to access information and engage with devices in a hassle-free manner. For example, smartwatches enable users to view notifications, make calls, and monitor their fitness metrics without the need for a conventional screen.

Furthermore, advancements in mobile technology and laptops have led to the development of screenless displays for hands-free use, enhancing productivity and convenience. In industries such as healthcare and transportation, screenless displays offer significant advantages, such as real-time data visualization and improved safety.

Market Trends

Growing interest in holographic displays is the upcoming trend in the market. Holographic displays represent an intriguing development in the market, offering the ability to generate three-dimensional visual images without conventional screens. This technology holds significant potential for delivering a more captivating experience for consumers. One notable application of holographic displays is in retail, where businesses can replace traditional product displays with holographic projections.

For example, a fashion retailer might project holographic models showcasing their latest designs, enabling customers to view clothing from various angles without even trying them on. However, the high cost and limited availability of these technologies, coupled with a lack of widespread awareness, hinder their broader adoption. Smart infrastructure solutions may eventually address these challenges, making holographic displays a more accessible and viable option for businesses.

Market Challenge

The high cost of screenless display devices is a key challenge affecting the market growth. Screenless display technology, such as 3D projection and next-generation holographic solutions, have garnered significant interest in various industries due to their ability to present visual information without the need for traditional displays. These advancements in visual display technology hold potential applications in sectors like automotive, aerospace, gaming, healthcare, and entertainment. However, the high cost of screenless display devices remains a significant barrier to their widespread adoption. For instance, the automotive industry has been investigating the implementation of augmented reality (AR) head-up displays (HUDs) to improve the driving experience. These AR HUDs project essential data, such as speed, navigation, and traffic alerts, directly onto the windshield, enabling drivers to maintain focus on the road.

Despite their advantages, the substantial investment required for these devices has restricted their usage. Privacy and security concerns associated with screenless display technology are also under scrutiny and require further research and development to ensure their implementation in a secure and confidential manner.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- Sony Group Corp.: The company offers a cylindrical transparent screen display, namely Holographic optical element screen.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Avegant Corp.

- BAE Systems Plc

- Eon Reality Inc.

- Holoxica Ltd.

- Leia Display System

- Magic Leap Inc.

- Microsoft Corp.

- RealView Imaging Ltd.

- Robert Bosch GmbH

- SeeReal Technologies SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Screenless display technology is revolutionizing the way we consume visual content, offering experiences without the need for traditional LCD panels or CRT monitors. This innovation encompasses various technologies such as holograms, retinal displays, synaptic interfaces, and visual image displays. Holograms, utilizing laser technology and electron beam lithography, create 3D projections in mid-air, providing a captivating viewing experience. Retinal displays, on the other hand, project visual images directly onto the retina, offering a more personalized experience. Advancements in technologies like synaptic interfaces, intelligent glasses, and voice recognition enable more interactive and intuitive user experiences. Holographic projections in the medical field offer enhanced visualization for surgeries and training, while in manufacturing, they facilitate better product design and quality control.

Further, in transportation systems, screenless displays can provide real-time information and enhance safety. However, high costs and limited availability hinder the widespread adoption of screenless display technology. Privacy and security concerns also arise due to the potential for intrusive holographic projections. The lack of awareness and understanding about this technology further hinders its growth. Despite these challenges, next-generation holographic solutions continue to advance, offering exciting possibilities in mobile technology, laptops, and even aerospace and defense applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 46.02% |

|

Market Growth 2024-2028 |

USD 14.87 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

32.79 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 42% |

|

Key countries |

US, Germany, Canada, China, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Avegant Corp., BAE Systems Plc, Eon Reality Inc., Holoxica Ltd., Leia Display System, Magic Leap Inc., Microsoft Corp., RealView Imaging Ltd., Robert Bosch GmbH, SeeReal Technologies SA, and Sony Group Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -