Small Satellite Market Size 2026-2030

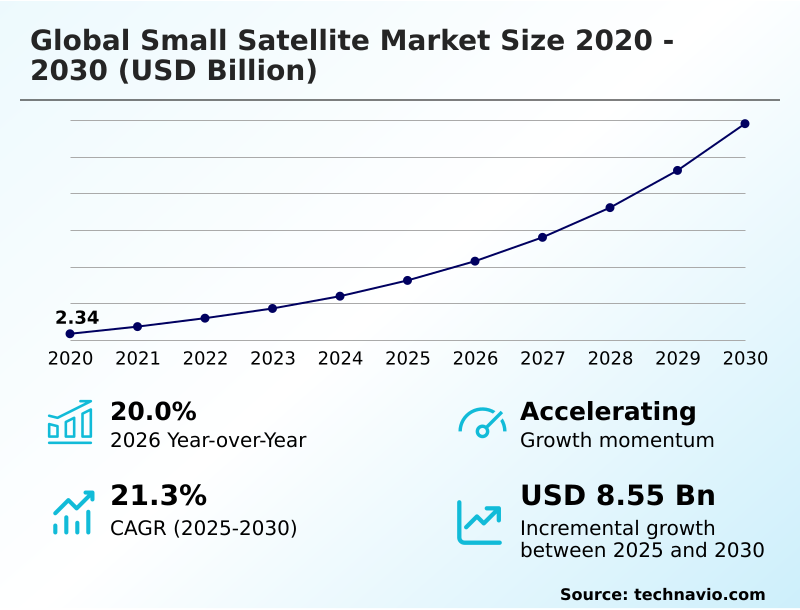

The small satellite market size is valued to increase by USD 8.55 billion, at a CAGR of 21.3% from 2025 to 2030. Democratizing space access with rideshare launches will drive the small satellite market.

Major Market Trends & Insights

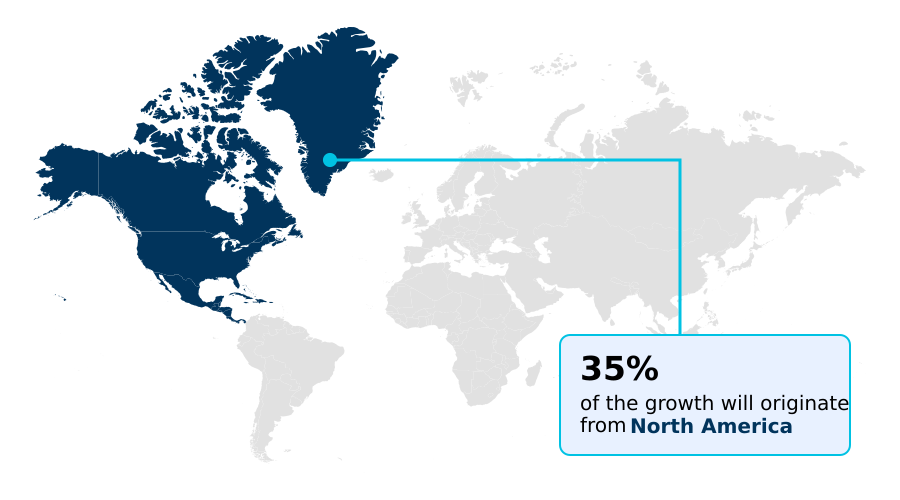

- North America dominated the market and accounted for a 34.7% growth during the forecast period.

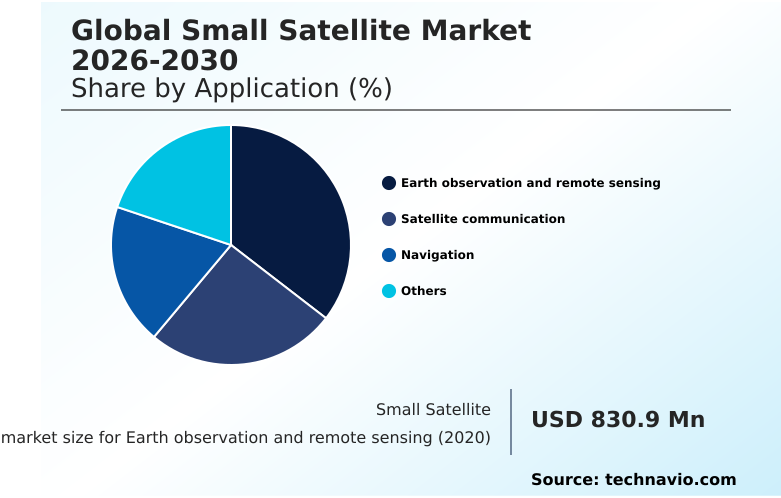

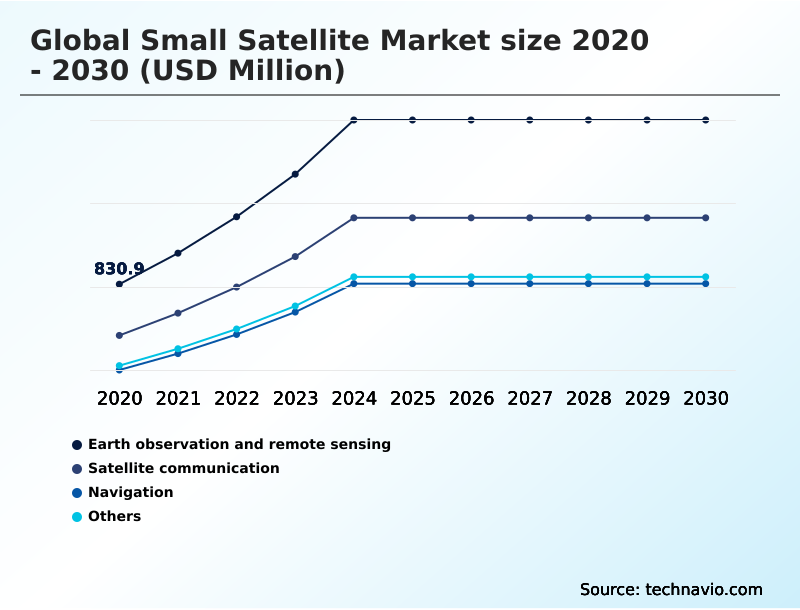

- By Application - Earth observation and remote sensing segment was valued at USD 1.57 billion in 2024

- By Type - Minisatellite segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.45 billion

- Market Future Opportunities: USD 8.55 billion

- CAGR from 2025 to 2030 : 21.3%

Market Summary

- The small satellite market is undergoing a period of significant growth, fueled by technological advancements and expanding commercial demand. This dynamic market is characterized by rapid innovation, with new applications emerging at an unprecedented rate.

- The proliferation of low earth orbit (LEO) constellations is a key factor, enabling a new era of global connectivity and data services through advanced satellite communication. This environment fosters intense competition, leading to the development of more sophisticated and cost-effective small satellite platforms, including the popular cubesat standard.

- The market's growth is not just quantitative; it represents a qualitative shift in how space is utilized, with small satellites becoming integral to critical infrastructure worldwide. For instance, a logistics company can now leverage a nanosatellite network for real-time, global asset tracking, a service previously unfeasible due to cost.

- This capability, alongside developments in earth observation, is reshaping industries by providing timely, actionable data. However, this rapid expansion also brings challenges, such as the need for robust space situational awareness (SSA) to manage orbital congestion and mitigate collision risks. The industry's trajectory points toward increased autonomy, with onboard ai processing becoming standard for data handling and operational efficiency.

What will be the Size of the Small Satellite Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Small Satellite Market Segmented?

The small satellite industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Earth observation and remote sensing

- Satellite communication

- Navigation

- Others

- Type

- Minisatellite

- Nanosatellite

- Microsatellite

- Product type

- LEO

- MEO

- GEO

- End-user

- Government and military

- Commercial

- Academic

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- UK

- Germany

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Application Insights

The earth observation and remote sensing segment is estimated to witness significant growth during the forecast period.

The earth observation and remote sensing segment is a primary driver within the market, where demand for high-frequency geospatial data is escalating.

This area has been transformed by the use of satellite constellation deployment, enabling daily or even hourly monitoring of changes on the Earth's surface, a feat not possible with older, monolithic satellites.

The market uses a mix of minisatellite, microsatellite, and nanosatellite platforms, each integrated with advanced remote sensing technology. These systems support industries from agriculture to finance by providing actionable intelligence.

Through sophisticated satellite data fusion and analysis, data processing for cloud detection can be optimized by over 40%, allowing for more efficient delivery of valuable information from high-throughput satellite (HTS) networks and those with hyperspectral imaging sensor capabilities.

The Earth observation and remote sensing segment was valued at USD 1.57 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Small Satellite Market Demand is Rising in North America Get Free Sample

The geographic landscape of the small satellite market is led by North America, which accounts for over 34% of the market's incremental growth, driven by extensive private and government investment in the US.

The APAC region is the fastest-growing, with a projected growth rate of 23.5%, as countries like China, India, and Japan expand their sovereign space capabilities. Europe maintains a strong position through collaborative programs and specialized industrial expertise.

Activity is even expanding into geostationary earth orbit (GEO) for specialized missions. A key application driving global adoption is satellite communication, which bridges the digital divide in underserved regions of South America and Africa.

Furthermore, the deployment of synthetic aperture radar (SAR) satellites for all-weather imaging and cubesat platforms for scientific research highlights the technological diversification across all regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic considerations within the global small satellite market 2026-2030 are increasingly nuanced, focusing on specific trade-offs and applications. A key debate involves minisatellite vs microsatellite capabilities, where operators weigh higher payload capacity against deployment costs. The rapid expansion of the nanosatellite constellation for IoT is a testament to the value of scaled, low-cost platforms for global connectivity.

- The LEO satellite latency advantage remains a critical differentiator for broadband services, enabling real-time applications that are impossible from higher orbits. For persistent monitoring, the SAR satellite for all-weather imaging provides invaluable data regardless of cloud cover or time of day.

- Economically, the cost-benefit of COTS components in space has been a primary enabler, though this is balanced by the need for radiation hardening of electronic components in harsher orbits. Operationally, the challenges of space debris mitigation are forcing innovation in end-of-life planning. The use of a software-defined radio for mission flexibility allows operators to adapt to changing market demands post-launch.

- This adaptability is enhanced by AI for onboard satellite data processing, which can reduce data downlink volumes by over 50%, directly lowering ground segment costs for constellations. Inter-satellite links for mesh networks are creating a resilient, space-based internet backbone. However, regulatory hurdles for spectrum licensing remain a significant barrier.

- Innovations like electric propulsion for small satellites are extending mission lifecycles, enabling new use cases like the GEO small satellite inspection use case and PNT augmentation with LEO satellites.

- The complexity of the rideshare mission payload integration process is being streamlined, while advances in phased array antenna for satellite broadband are boosting connectivity speeds, all contributing to the growth in high-revisit rate earth observation services.

What are the key market drivers leading to the rise in the adoption of Small Satellite Industry?

- The democratization of space access, driven by lower-cost rideshare launches and reusable rocket technology, is a primary factor accelerating market expansion.

- The market's rapid expansion is fueled by the convergence of several key drivers. The proliferation of rideshare launch mission opportunities and the development of responsive launch capability have democratized space access.

- Simultaneously, satellite payload miniaturization, underpinned by the availability of high-performance commercial-off-the-shelf (COTS) parts, allows for more capable systems within smaller, lighter satellite bus platform designs.

- Modern onboard computers, for instance, can now fit within a 10cm x 10cm x 5cm volume while delivering gigaflop-level processing power. This has spurred the growth of sophisticated geospatial data analytics services.

- Furthermore, nations are increasingly focused on establishing sovereign satellite capability, driving domestic investment in the entire value chain, from manufacturing to on-orbit servicing and manufacturing (OSAM). Advances in phased array antenna technology are also pivotal for enabling high-throughput communication services.

What are the market trends shaping the Small Satellite Industry?

- The integration of onboard artificial intelligence is enabling a shift toward autonomous satellite operations and real-time, in-orbit data analysis.

- Key trends are reshaping the global small satellite market 2026-2030, driven by the integration of onboard AI processing and autonomous satellite operations. This allows for edge computing in space, where satellites can analyze data in orbit, with algorithms capable of filtering out unusable imagery, thereby optimizing downlink bandwidth by over 40%.

- The widespread adoption of optical inter-satellite links (OISL), a form of inter-satellite laser communication, is creating high-speed mesh networks capable of gigabit-per-second data rates. This architecture significantly reduces latency for real-time services. Another transformative trend is in-orbit reconfigurability, enabled by the software-defined radio (SDR) and software-defined satellite payload, allowing operators to repurpose assets after launch.

- This flexibility is complemented by the increasing use of advanced electric propulsion system technology, extending mission lifetimes and enabling more complex orbital maneuvers.

What challenges does the Small Satellite Industry face during its growth?

- Navigating the growing threat of orbital debris and space congestion presents a significant challenge to the sustainability and safety of small satellite operations.

- The market faces significant operational and regulatory challenges. The proliferation of satellites in low earth orbit (LEO) has intensified the problem of orbital debris, with over 36,500 tracked objects larger than 10cm posing a catastrophic risk. This necessitates advanced space situational awareness (SSA) and robust space traffic management (STM) protocols, including adherence to end-of-life deorbiting guidelines.

- Another major constraint is radio frequency spectrum allocation, a complex and costly process that can significantly delay service deployment. Furthermore, while launch costs have decreased, the high expense of establishing a global ground station network or paying for ground station as a service (GSaaS) remains a substantial financial barrier.

- Operating in higher orbits like medium earth orbit (MEO) also requires costly radiation-hardened components to withstand the harsh environment, impacting the business case for certain missions.

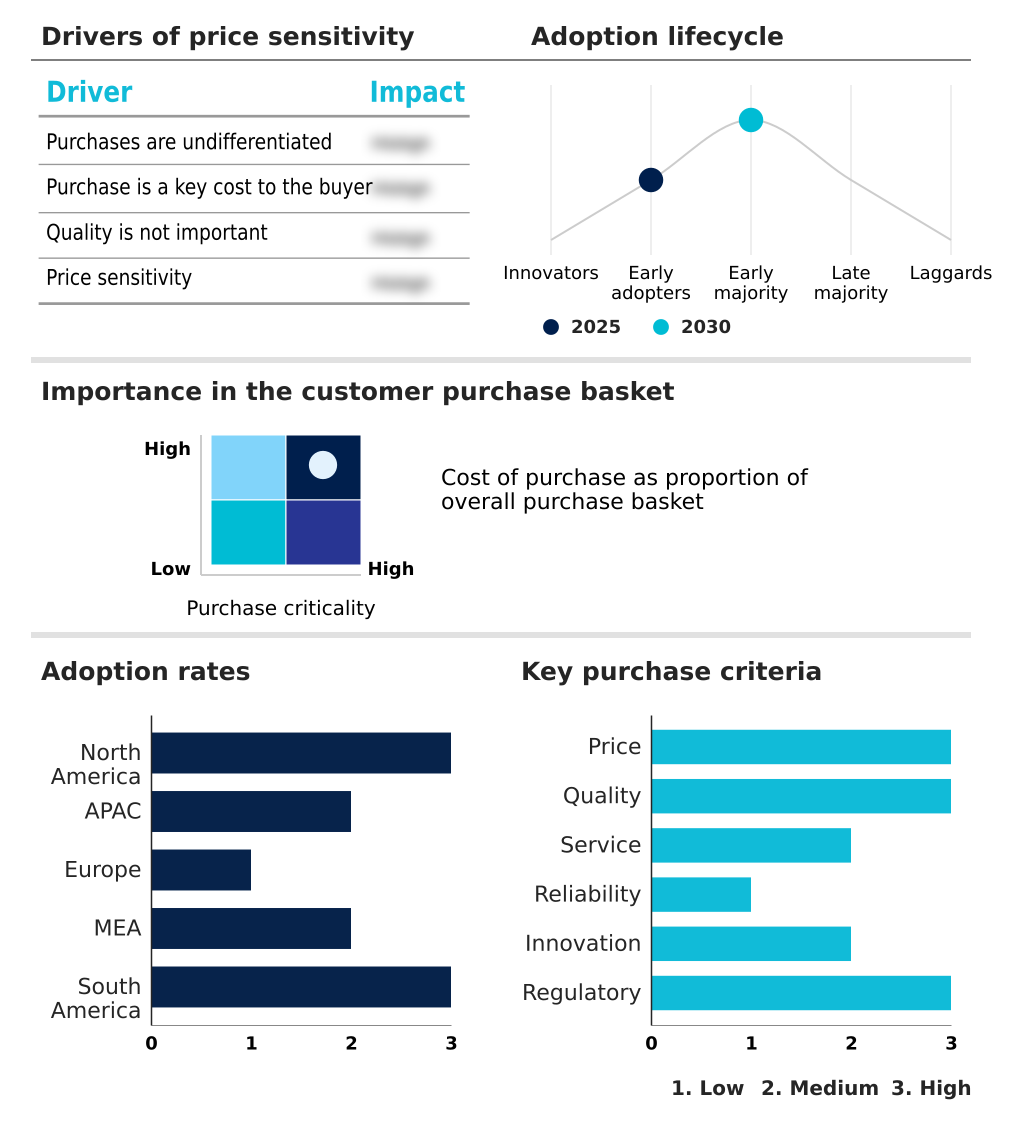

Exclusive Technavio Analysis on Customer Landscape

The small satellite market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the small satellite market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Small Satellite Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, small satellite market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAC Clyde Space AB - Offerings encompass integrated small satellite solutions, from mission design and turnkey systems to specialized components and subscription-based data services for diverse applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AAC Clyde Space AB

- Airbus SE

- Capella Space Corp.

- China Aerospace S and T Corp.

- GomSpace Group AB

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- Maxar Technologies Inc.

- MDA Corp.

- Mitsubishi Electric Corp.

- Northrop Grumman Corp.

- OHB SE

- Planet Labs PBC

- Rocket Lab USA Inc.

- Sierra Nevada Corp.

- Space Exploration Tech. Corp.

- Spire Global Inc.

- ST Engineering Ltd.

- Thales Alenia Space

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Small satellite market

- In December, 2024, Airbus Defence and Space received a contract from Eutelsat Communications to build the next-generation OneWeb Low Earth Orbit constellation, ensuring continuity for the satellite broadband network.

- In January, 2025, The United States National Aeronautics and Space Administration launched the Technology Education Satellite 22 (TES-22) CubeSat to advance educational and technological development objectives.

- In March, 2025, The Saudi Space Agency announced the launch of two small satellites designed and built by university students as a strategic initiative to cultivate a skilled national workforce for its future space industry.

- In April, 2025, OHB SE secured a contract to deliver six electric propulsion systems for SWISSto12's small geostationary satellite platform, highlighting the trend toward more efficient and longer-duration missions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Small Satellite Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 334 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.3% |

| Market growth 2026-2030 | USD 8549.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.0% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Russia, Spain, UAE, Saudi Arabia, South Africa, Egypt, Nigeria, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The small satellite market is defined by a strategic shift from monolithic spacecraft to distributed constellations, primarily in low earth orbit (LEO), which leverage platforms like the minisatellite, microsatellite, and the standardized cubesat. This transition is enabled by the accessibility of commercial-off-the-shelf (COTS) parts and the availability of frequent rideshare launch mission opportunities.

- Key applications driving this architecture are earth observation and global satellite communication, with remote sensing technology providing unprecedented geospatial data analytics. For boardroom decisions, the trend of in-orbit reconfigurability, made possible by software-defined radio (SDR) and electric propulsion system technology, is critical for maximizing long-term asset value and adapting to new market opportunities.

- The adoption of COTS components has been shown to shorten satellite development timelines by up to 60%, a crucial metric for maintaining competitive agility. Payloads like synthetic aperture radar (SAR) and advanced phased array antenna systems are becoming more common on smaller satellite bus platform designs. However, operating in MEO and GEO presents challenges related to radiation-hardened components.

- The entire ecosystem relies on a robust ground station network and effective space situational awareness (SSA) for management, with onboard AI processing emerging as a key differentiator.

What are the Key Data Covered in this Small Satellite Market Research and Growth Report?

-

What is the expected growth of the Small Satellite Market between 2026 and 2030?

-

USD 8.55 billion, at a CAGR of 21.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Earth observation and remote sensing, Satellite communication, Navigation, and Others), Type (Minisatellite, Nanosatellite, and Microsatellite), Product Type (LEO, MEO, and GEO), End-user (Government and military, Commercial, Academic, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Democratizing space access with rideshare launches, Navigating growing threat of space debris

-

-

Who are the major players in the Small Satellite Market?

-

AAC Clyde Space AB, Airbus SE, Capella Space Corp., China Aerospace S and T Corp., GomSpace Group AB, L3Harris Technologies Inc., Lockheed Martin Corp., Maxar Technologies Inc., MDA Corp., Mitsubishi Electric Corp., Northrop Grumman Corp., OHB SE, Planet Labs PBC, Rocket Lab USA Inc., Sierra Nevada Corp., Space Exploration Tech. Corp., Spire Global Inc., ST Engineering Ltd., Thales Alenia Space and The Boeing Co.

-

Market Research Insights

- Market dynamics are shaped by the strategic shift toward proliferated LEO architecture, which enhances service resilience and coverage. This trend is supported by an expanding ecosystem of ground station as a service (GSaaS) providers, which reduces upfront capital expenditure for operators, with antenna time priced between $3 and $10 per minute.

- The development of a responsive launch capability further accelerates constellation deployment. The adoption of dual-use satellite technology meets both commercial and government needs, while resilient PNT services are being developed to augment existing navigation systems.

- Utilizing satellite data for insurance purposes can reduce claim assessment costs by 30% to 40%, demonstrating a clear return on investment and driving further adoption of space-based data solutions.

We can help! Our analysts can customize this small satellite market research report to meet your requirements.

RIA -

RIA -