Software-defined Data Center (SDDC) Market Size 2026-2030

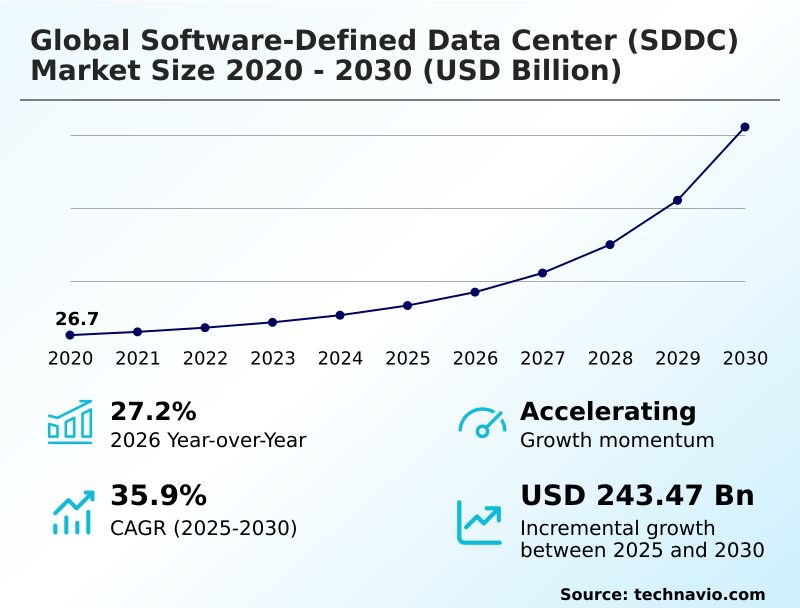

The software-defined data center (sddc) market size is valued to increase by USD 243.47 billion, at a CAGR of 35.9% from 2025 to 2030. Rising demand for agile IT infrastructure solutions will drive the software-defined data center (sddc) market.

Major Market Trends & Insights

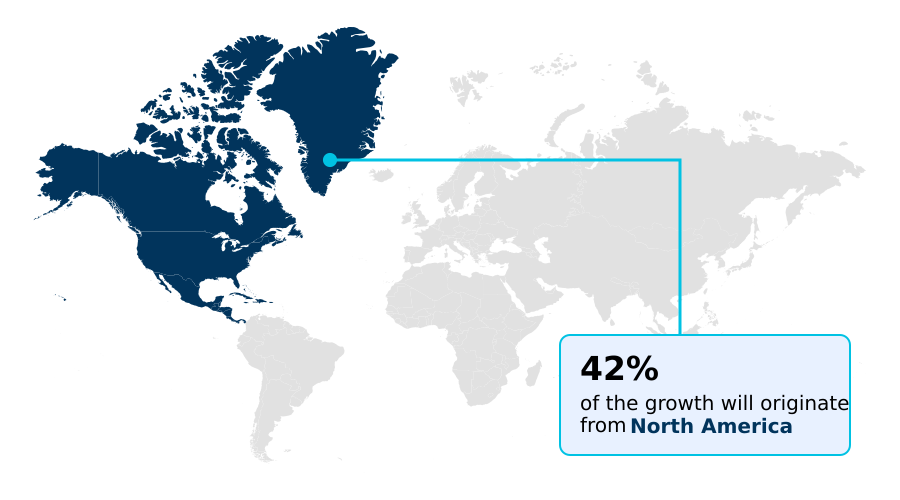

- North America dominated the market and accounted for a 41.8% growth during the forecast period.

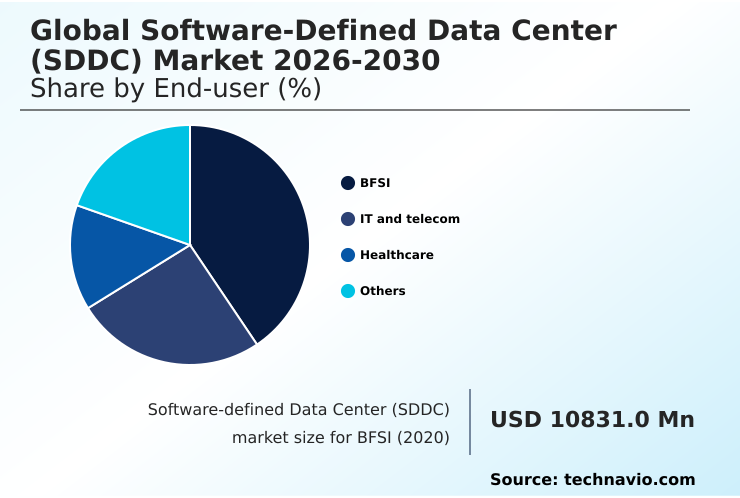

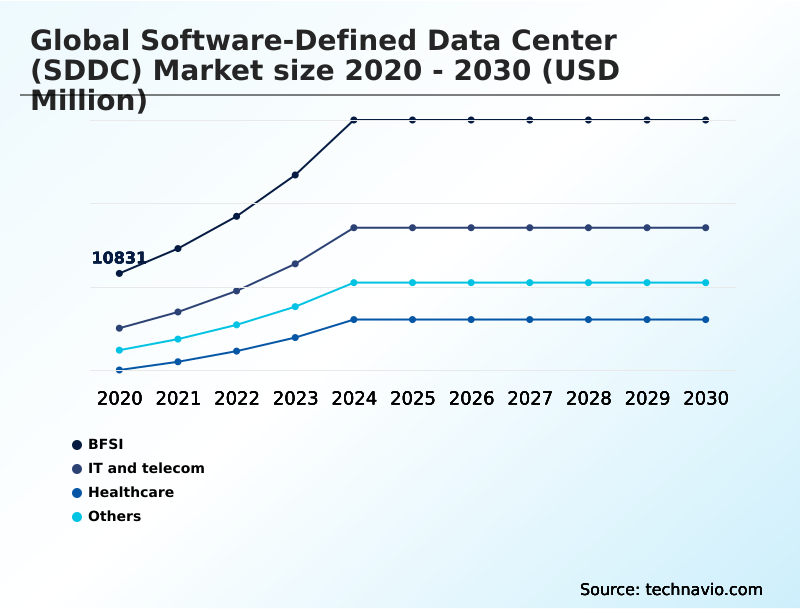

- By End-user - BFSI segment was valued at USD 22.01 billion in 2024

- By Type - SDS segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 283.77 billion

- Market Future Opportunities: USD 243.47 billion

- CAGR from 2025 to 2030 : 35.9%

Market Summary

- The Software-defined Data Center (SDDC) market represents a fundamental paradigm shift where compute, storage, and networking infrastructure are virtualized and delivered as a service. This architectural evolution is driven by the enterprise-wide need for greater agility, operational efficiency, and cost control in managing complex IT environments.

- By abstracting control planes from physical hardware, server virtualization and software-defined networking enable policy-driven automation, significantly reducing manual intervention and accelerating service delivery. A key trend is the integration of AI for automated resource management, allowing for predictive analytics that optimize workload placement and energy consumption.

- For example, a global logistics firm can leverage an SDDC to dynamically scale its supply chain management applications during peak seasons, ensuring consistent performance without overprovisioning resources. However, challenges such as virtualized infrastructure security and the complexities of legacy system migration require careful strategic planning.

- The adoption of hyper-converged infrastructure and container orchestration is further simplifying deployment, making SDDC a cornerstone of modern hybrid cloud strategy and digital transformation.

What will be the Size of the Software-defined Data Center (SDDC) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Software-defined Data Center (SDDC) Market Segmented?

The software-defined data center (sddc) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- BFSI

- IT and telecom

- Healthcare

- Others

- Type

- SDS

- SDN

- SDC

- Component

- Solution

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

The BFSI sector's adoption of software-defined data center technologies is driven by the need for robust data center security and compliance with evolving regulations. Financial institutions are pursuing infrastructure modernization to enhance IT agility improvement and support digital-first services.

This shift involves leveraging a unified control plane and resource abstraction to manage complex, distributed systems.

By implementing micro-segmentation and a zero-trust architecture, firms can better protect sensitive data against cyber threats, with some achieving a 40% reduction in breach detection times.

The transition to a hybrid cloud strategy is also critical, allowing for a balance between on-premise control and public cloud scalability, facilitated by advanced orchestration tools and policy-driven automation.

This approach supports business continuity planning and ensures high availability for critical financial services.

The BFSI segment was valued at USD 22.01 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Software-defined Data Center (SDDC) Market Demand is Rising in North America Get Free Sample

The geographic landscape is shaped by regional priorities, with North America leading in adoption due to a high concentration of hyperscale providers and a focus on application performance monitoring. This region accounts for over 41% of the incremental growth.

In Europe, data sovereignty compliance and sustainability are paramount, driving demand for localized solutions and private cloud deployment.

The APAC region is the fastest-growing market, with countries like China and India leapfrogging legacy systems to adopt modern server virtualization and network functions virtualization to support their digital economies.

Across all regions, the expansion of edge computing infrastructure is a common theme, requiring remote data center management capabilities. The need for infrastructure scalability and disaster recovery automation to ensure service continuity is a universal driver influencing investment decisions globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly evaluating the cost benefits of server virtualization and comparing hyper-converged vs traditional infrastructure to improve data center operations. A primary focus is on improving data center agility with sddc, which allows for dynamic resource allocation and rapid deployment.

- The adoption of software-defined storage for unstructured data and network automation with software-defined networking are key components of this transformation. For managing modern workloads, understanding kubernetes orchestration in sddc platforms and the role of software-defined compute for ai workloads is crucial. A significant challenge remains in securing multi-tenant sddc environments, prompting the adoption of a zero-trust security model in sddc.

- Effective sddc for hybrid cloud workload management relies on robust policy-based management in sddc. The benefits of infrastructure-as-code deployment include consistency and speed, yet organizations must also consider the impact of sddc on it operational costs. Successful implementation requires strong sddc performance monitoring best practices and clear disaster recovery strategies in sddc.

- As the role of sddc in edge computing grows, ai-driven data center resource optimization becomes even more critical. Navigating challenges in sddc migration projects and managing sddc in a multi-vendor ecosystem are essential for achieving long-term success and ensuring data sovereignty with sddc.

- Organizations that successfully migrate report a 2x improvement in infrastructure provisioning times compared to those that remain on legacy systems.

What are the key market drivers leading to the rise in the adoption of Software-defined Data Center (SDDC) Industry?

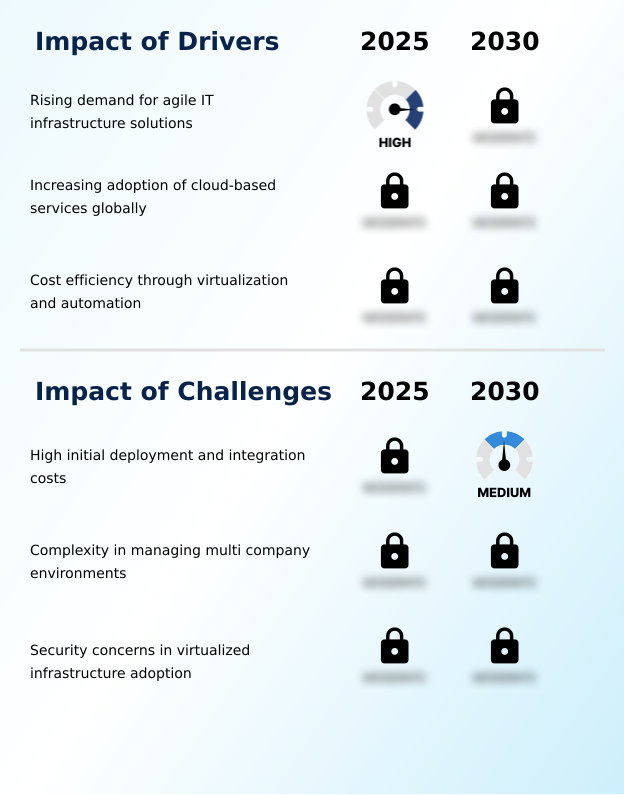

- The rising demand for agile IT infrastructure solutions is a key driver, as organizations seek greater flexibility, scalability, and efficiency.

- The demand for agile IT infrastructure is a primary driver, as businesses seek flexibility to support cloud-native applications and accelerate digital transformation. The increasing cloud-based services adoption globally necessitates architectures that enable seamless hybrid cloud integration and centralized management.

- Cost optimization is another significant factor, with virtualization technologies and automation leading to notable operational cost reduction.

- By abstracting resources from physical hardware using a hardware abstraction layer, organizations achieve better utilization and minimize capital expenditure, with some reporting a 25% lower data center TCO reduction.

- This shift facilitates hardware dependency reduction and enables a more scalable IT model. The focus on efficiency makes these software-defined approaches a cornerstone for modern enterprises aiming for competitive advantage.

What are the market trends shaping the Software-defined Data Center (SDDC) Industry?

- The integration of AI for automated resource management is an emerging trend, enabling predictive analytics and intelligent orchestration to optimize data center operations.

- A key trend transforming the market is the integration of AI for automated resource management, creating autonomous infrastructure that can anticipate workload demands. This approach uses predictive analytics and intelligent orchestration for dynamic resource allocation, improving IT operational efficiency by up to 30%.

- The growing adoption of container orchestration platforms like Kubernetes is also pivotal, enabling rapid application delivery speed and workload portability in multi-cloud environment setups. Organizations are leveraging these trends for enhanced DevOps integration, leading to faster innovation cycles.

- The rise of hyper-converged infrastructure simplifies management by combining compute, storage, and networking, reducing hardware footprint and supporting initiatives for more energy-efficient data centers. This convergence streamlines IT infrastructure automation for greater business agility.

What challenges does the Software-defined Data Center (SDDC) Industry face during its growth?

- High initial deployment and integration costs represent a key challenge, acting as a barrier to adoption despite long-term benefits.

- Despite the benefits, significant challenges persist, particularly the complexity of multi-vendor environment management. Integrating disparate systems for software-defined compute, storage, and networking often requires extensive customization, impacting IT budget optimization. Security concerns in virtualized infrastructure security also restrain adoption, as the abstraction of control planes introduces new potential vulnerabilities.

- Organizations must invest in advanced solutions to ensure effective data protection policies and network visibility across dynamic environments. High initial deployment costs associated with legacy system migration and the need for specialized skills for automated IT operations can be prohibitive.

- Addressing these issues through careful planning and phased implementation is crucial for justifying the investment, as missteps can lead to fragmented systems and diminish the promised returns on agility and efficiency.

Exclusive Technavio Analysis on Customer Landscape

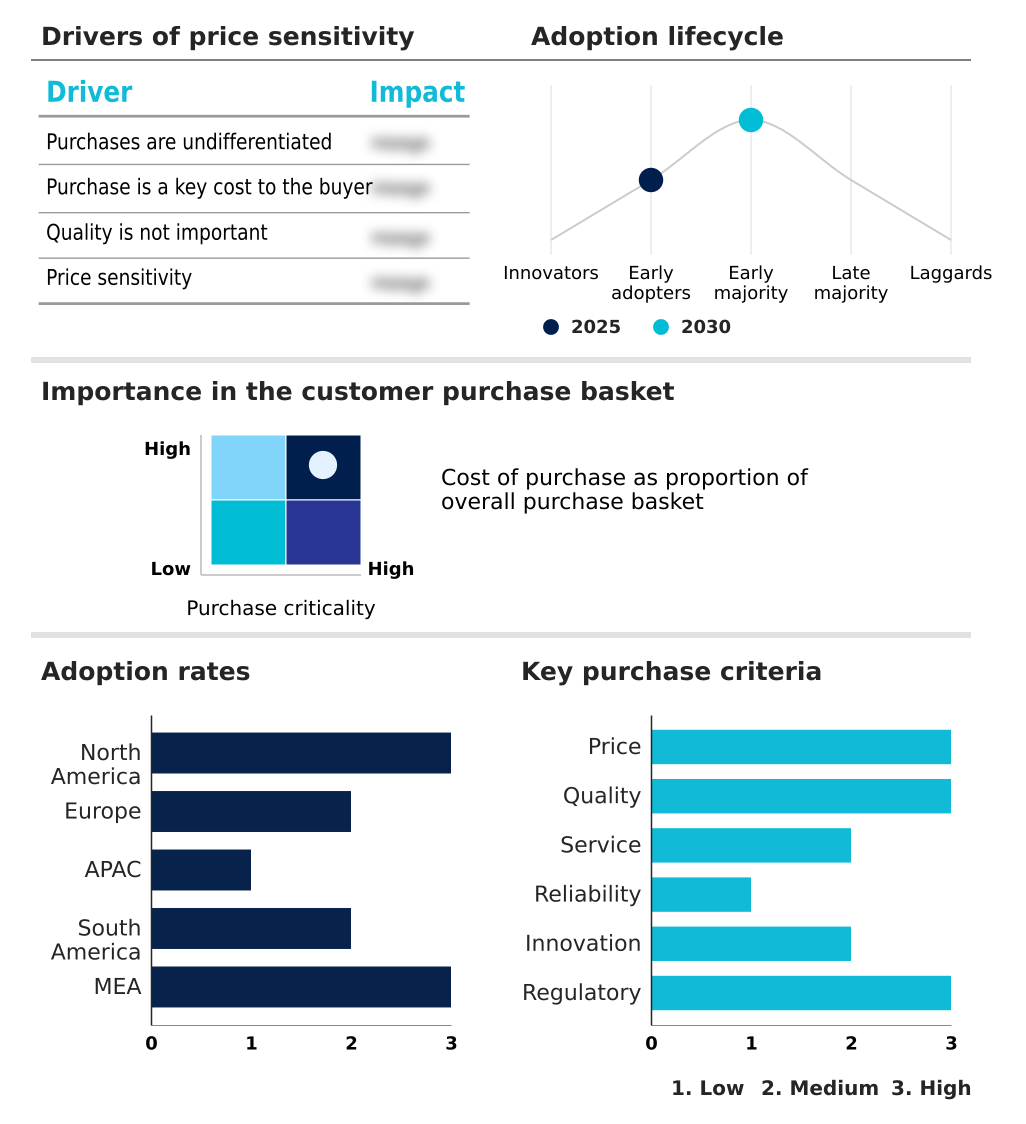

The software-defined data center (sddc) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software-defined data center (sddc) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Software-defined Data Center (SDDC) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, software-defined data center (sddc) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arista Networks Inc. - Key offerings include integrated platforms that virtualize compute, storage, and networking, delivering infrastructure-as-a-service with policy-driven automation and centralized management for enhanced operational agility.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arista Networks Inc.

- Cisco Systems Inc.

- Citrix Systems Inc.

- DataCore Software Corp.

- Dell Technologies Inc.

- EdgeConneX Inc.

- F5 Inc.

- Fujitsu Ltd.

- Hewlett Packard

- Hitachi Vantara LLC

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Juniper Networks Inc.

- Lenovo Group Ltd.

- Microsoft Corp.

- NetApp Inc.

- Nutanix Inc.

- Oracle Corp.

- VMware Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Software-defined data center (sddc) market

- In August 2024, Khazna Data Centers inaugurated a massive facility in the United Arab Emirates that employs a comprehensive software-defined management system to oversee everything from cooling to compute allocation.

- In November 2024, Kyndryl Holdings Incorporated expanded its strategic collaboration with Microsoft Corp. to launch a specialized service dedicated to migrating legacy data centers to software-defined environments hosted on the Azure platform.

- In February 2025, Accenture collaborated with Google Cloud to accelerate sovereign cloud and generative AI adoption in Saudi Arabia, utilizing software-defined data center principles to ensure data residency and compliance with regional regulations.

- In April 2025, Microsoft and G42 announced a joint initiative to deploy a sovereign cloud solution in Abu Dhabi that utilizes a software-defined data center stack to ensure sensitive government data remains within national borders.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software-defined Data Center (SDDC) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 35.9% |

| Market growth 2026-2030 | USD 243474.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 27.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The software-defined data center market is characterized by a continuous evolution toward fully autonomous operations. The core components—software-defined networking, software-defined storage, and software-defined compute—are converging into unified platforms, often through hyper-converged infrastructure. This shift is driven by the need for policy-driven automation and centralized management to handle the complexity of modern IT.

- Virtualization technologies and resource abstraction, supported by a robust hardware abstraction layer, enable workload portability across any multi-cloud environment. For boardroom decisions, the adoption of a zero-trust architecture and micro-segmentation for data center security is now a critical compliance discussion, with some firms achieving a 50% improvement in security policy enforcement.

- Technologies like network functions virtualization and data processing units are enabling intelligent orchestration and predictive analytics for automated resource management. This move toward an autonomous infrastructure, managed via infrastructure-as-code and a unified control plane, supports container orchestration, cloud-native applications, dynamic resource allocation, disaster recovery automation, and self-healing capabilities, enabling data center virtualization for both core and edge computing infrastructure.

- The goal is network traffic automation and efficient automated provisioning.

What are the Key Data Covered in this Software-defined Data Center (SDDC) Market Research and Growth Report?

-

What is the expected growth of the Software-defined Data Center (SDDC) Market between 2026 and 2030?

-

USD 243.47 billion, at a CAGR of 35.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, IT and telecom, Healthcare, and Others), Type (SDS, SDN, and SDC), Component (Solution, and Services) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for agile IT infrastructure solutions, High initial deployment and integration costs

-

-

Who are the major players in the Software-defined Data Center (SDDC) Market?

-

Arista Networks Inc., Cisco Systems Inc., Citrix Systems Inc., DataCore Software Corp., Dell Technologies Inc., EdgeConneX Inc., F5 Inc., Fujitsu Ltd., Hewlett Packard, Hitachi Vantara LLC, Huawei Technologies Co. Ltd., IBM Corp., Juniper Networks Inc., Lenovo Group Ltd., Microsoft Corp., NetApp Inc., Nutanix Inc., Oracle Corp. and VMware Inc.

-

Market Research Insights

- The software-defined data center market is driven by the pursuit of enhanced IT operational efficiency and infrastructure scalability. Organizations adopting an agile IT infrastructure have reported up to a 40% faster application deployment time compared to traditional models.

- A core component of this shift is the implementation of a comprehensive hybrid cloud strategy, which allows businesses to balance security and scalability. The focus on operational cost reduction is significant, with automated provisioning and resource pooling leading to an average 15% decrease in IT spending.

- Furthermore, as enterprises undergo infrastructure modernization, the emphasis on data sovereignty compliance has become a critical decision factor, influencing private and hybrid cloud architecture choices. This dynamic environment reflects a strategic move toward flexible, software-driven operations.

We can help! Our analysts can customize this software-defined data center (sddc) market research report to meet your requirements.

RIA -

RIA -