Data Center IT Infrastructure Market Size 2026-2030

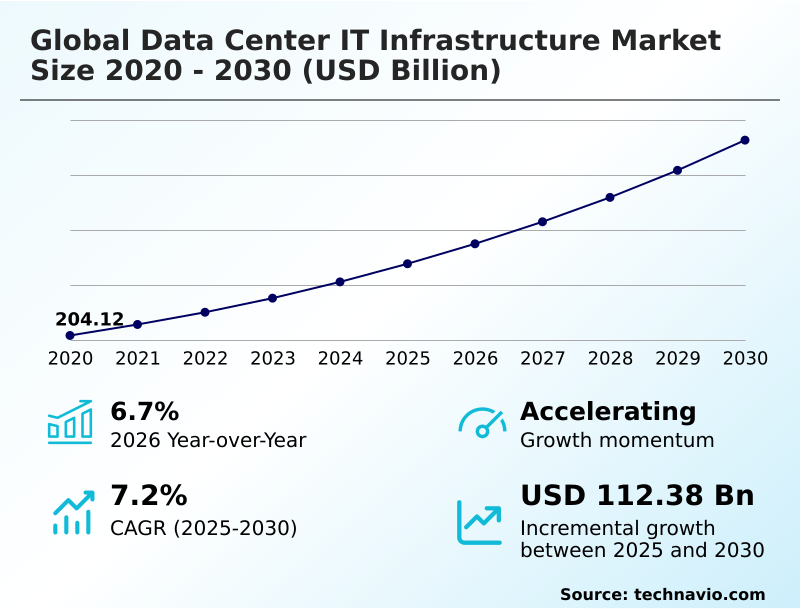

The data center it infrastructure market size is valued to increase by USD 112.38 billion, at a CAGR of 7.2% from 2025 to 2030. Exponential growth of hyperscale cloud services and digital transformation initiatives will drive the data center it infrastructure market.

Major Market Trends & Insights

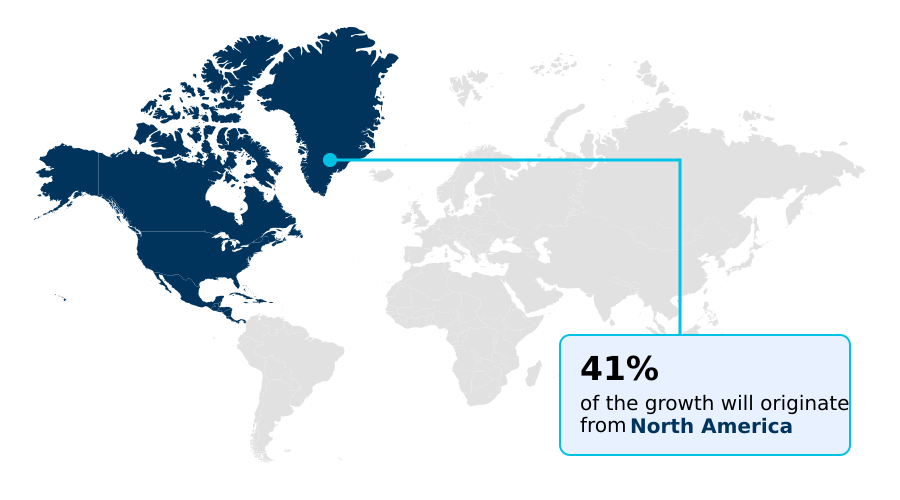

- North America dominated the market and accounted for a 40.6% growth during the forecast period.

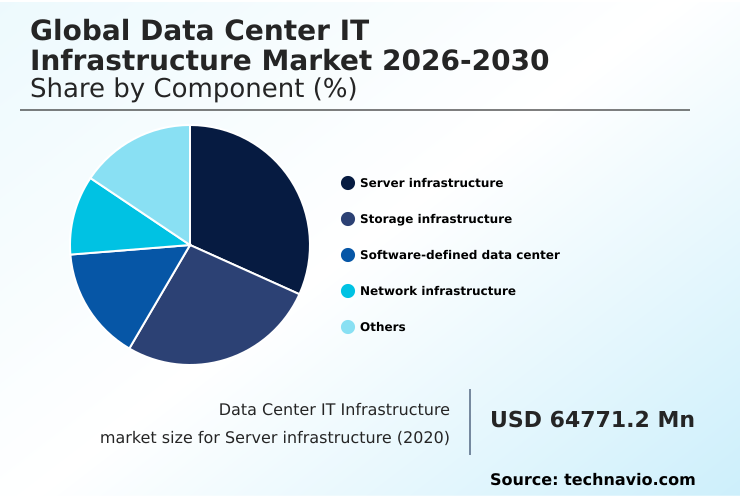

- By Component - Server infrastructure segment was valued at USD 81.22 billion in 2024

- By End-user - BFSI segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 177.57 billion

- Market Future Opportunities: USD 112.38 billion

- CAGR from 2025 to 2030 : 7.2%

Market Summary

- The data center IT infrastructure market is undergoing a significant architectural evolution, driven by the dual pressures of digital service delivery and operational efficiency. The backbone of the digital economy, this market includes the essential server infrastructure, storage infrastructure, and low-latency networking equipment required to process and manage escalating data volumes.

- A key trend is the move toward workload optimization, where specialized hardware like graphics processing units is deployed to handle AI and other data-intensive workloads more effectively. For instance, a financial services firm might deploy an all-flash storage array to reduce trade analysis times, thereby gaining a competitive edge.

- This is balanced by challenges such as geopolitical trade restrictions, which can disrupt supply chains for critical components. Simultaneously, the push for sustainable data center operations influences procurement strategies, favoring energy-efficient hardware. The interplay between performance demands, cybersecurity risks, and regulatory compliance, particularly around data sovereignty, defines the strategic landscape for enterprises navigating their IT modernization journey.

What will be the Size of the Data Center IT Infrastructure Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Data Center IT Infrastructure Market Segmented?

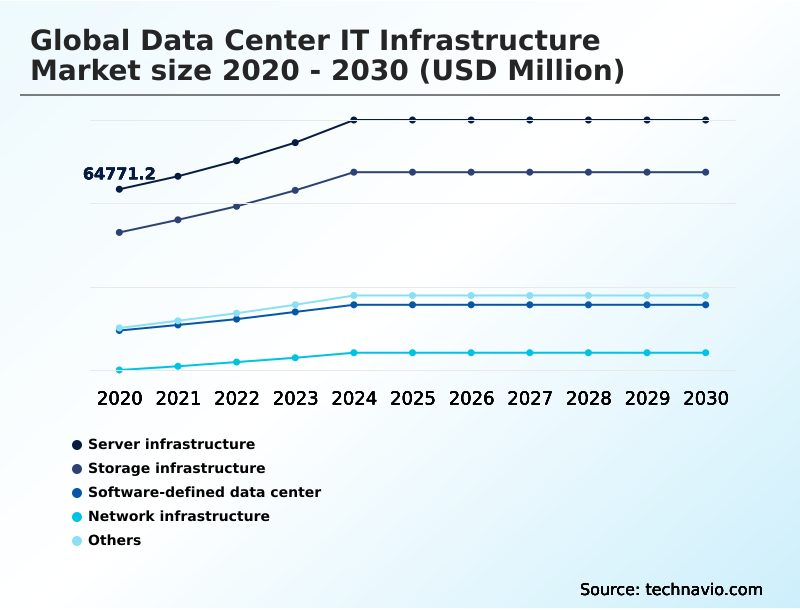

The data center it infrastructure industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Server infrastructure

- Storage infrastructure

- Software-defined data center

- Network infrastructure

- Others

- End-user

- BFSI

- Energy

- Information system

- Others

- Type

- Hyperscale data center

- Colocation data center

- Enterprise data center

- Edge data center

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The server infrastructure segment is estimated to witness significant growth during the forecast period.

The server infrastructure segment forms the computational backbone of the data center IT infrastructure market, encompassing everything from traditional rack servers to high-density blade systems and specialized multi-node servers.

This area is driven by a constant demand for increased processing power to handle data-intensive workloads and enterprise IT modernization. A key market dynamic is the architectural shift toward distributed, scale-out systems that enhance operational resilience and offer linear scalability.

This evolution fuels innovation in server design, focusing on modularity and optimized performance-per-watt, with some advanced configurations improving workload allocation efficiency by up to 15%.

This segment, crucial for both enterprise data center and hyperscale data center environments, sees continuous refresh cycles as organizations adopt high-performance servers and scalable storage systems to power every digital initiative.

The Server infrastructure segment was valued at USD 81.22 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Data Center IT Infrastructure Market Demand is Rising in North America Get Free Sample

The geographic landscape of the data center IT infrastructure market is defined by regional concentrations of investment and specific regulatory pressures.

North America, contributing over 40% of the market's incremental growth, remains dominant due to its dense concentration of hyperscale data center operators and aggressive enterprise IT modernization programs.

This region sees high demand for high-performance servers to support advanced AI workloads. In Europe, the market is heavily influenced by stringent data sovereignty compliance rules, driving demand for localized infrastructure and boosting the colocation data center segment.

This focus on regulatory compliance can lead to a 15% increase in infrastructure costs but is essential for operating within the region.

APAC is the fastest-growing region, fueled by rapid digitalization and government-led initiatives that spur investment in both enterprise data center and network infrastructure, creating diverse opportunities for vendors specializing in scalable solutions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the global data center IT infrastructure market is increasingly shaped by complex, intersecting challenges and opportunities. Navigating the impact of data localization regulations has become a primary boardroom concern, forcing a re-evaluation of global data strategies and sometimes leading to a 15% increase in compliance-related capital expenditure for data center buildouts.

- Simultaneously, the industry is grappling with how to best implement sustainable and green data center design, with a focus on optimizing power usage effectiveness (PUE). This includes exploring innovations like direct-to-chip liquid cooling solutions, which are critical for managing the heat from high-density server racks.

- Organizations are actively developing AI-optimized server procurement strategies to support next-generation applications while also working to mitigate data center power constraints. Addressing the specialized talent gap in IT remains a persistent challenge, impacting the ability to effectively manage hybrid and multi-cloud environments.

- Furthermore, data center supply chain volatility, exacerbated by geopolitical factors, complicates the procurement of everything from standard components to advanced systems for high-performance computing, such as those based on non-x86 server architecture for AI.

- Effectively deploying infrastructure for edge computing adds another layer of complexity, demanding a holistic approach that balances performance, cost, and security while securing infrastructure from cyber threats.

What are the key market drivers leading to the rise in the adoption of Data Center IT Infrastructure Industry?

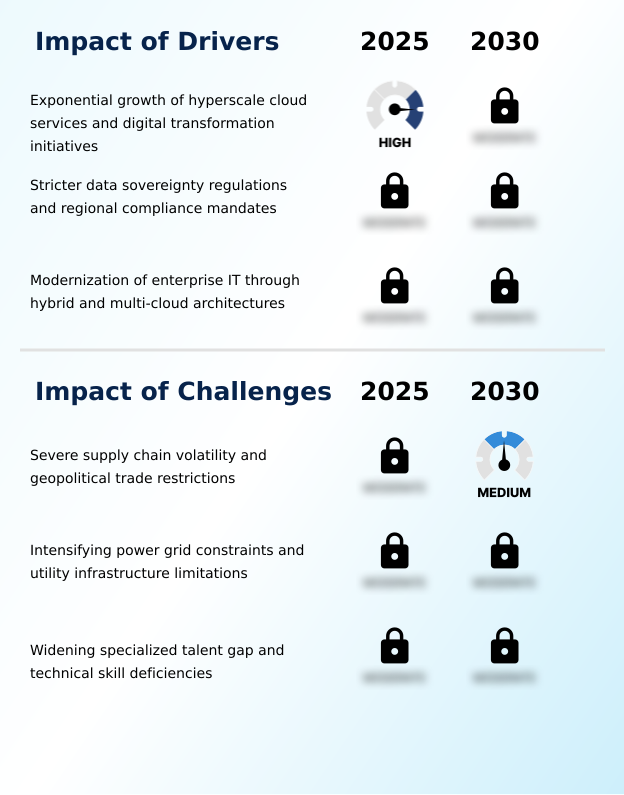

- The exponential growth of hyperscale cloud services, coupled with widespread digital transformation initiatives, serves as a key driver for market expansion.

- The market's expansion is propelled by several key drivers, foremost among them being the widespread adoption of hybrid cloud architecture.

- Enterprises are modernizing their on-premises infrastructure to seamlessly integrate with public clouds, improving operational resilience and enabling a more agile multi-cloud strategy. This modernization, often involving hyper-converged infrastructure, can automate up to 80% of routine provisioning tasks.

- A second major driver is the enforcement of strict data sovereignty and data localization regulations. These rules mandate in-country data storage, compelling organizations to invest in regional colocation or private enterprise data center facilities to ensure regulatory compliance.

- Finally, the relentless pace of digital transformation initiatives across industries continues to fuel demand for scalable storage systems and high-performance computing capabilities to support ever-growing data-intensive workloads.

What are the market trends shaping the Data Center IT Infrastructure Industry?

- The proliferation of artificial intelligence is driving a fundamental shift toward accelerated computing infrastructure. This transition has become a primary catalyst for investment and architectural change in the market.

- Key trends are reshaping the data center IT infrastructure market, led by the integration of artificial intelligence, which necessitates a move to accelerated computing infrastructure. This requires specialized hardware like graphics processing units and advanced thermal solutions such as liquid-to-chip cooling, with some facilities seeing rack power densities increase tenfold.

- Another critical trend is the expansion of edge computing infrastructure, which moves processing closer to data sources to support mission-critical applications. This shift can reduce latency by over 50% for real-time data processing. Finally, the drive for sustainability is mandating the adoption of green data center technologies and circular economy principles.

- This focus on operational efficiency is pushing operators to improve power usage effectiveness, with advanced energy management systems delivering efficiency gains of up to 15%.

What challenges does the Data Center IT Infrastructure Industry face during its growth?

- Severe supply chain volatility and geopolitical trade restrictions present a key challenge affecting the industry's growth trajectory.

- The data center IT infrastructure market faces significant headwinds, primarily from severe supply chain volatility and geopolitical trade restrictions. These issues create unpredictability in the procurement strategy for critical hardware, with lead times for specialized high-performance servers and networking components extending beyond 12 months in some cases.

- Another pressing issue is intensifying energy grid constraints, which can increase the total cost of ownership by over 25% in power-constrained regions and halt new hyperscale data center projects. Finally, a widening gap in technical skill deficiencies poses a direct threat to operational stability.

- The lack of experts in areas like advanced cooling and cybersecurity risks can slow deployment and increase operational risk, undermining an organization's digital transformation initiatives and overall operational efficiency.

Exclusive Technavio Analysis on Customer Landscape

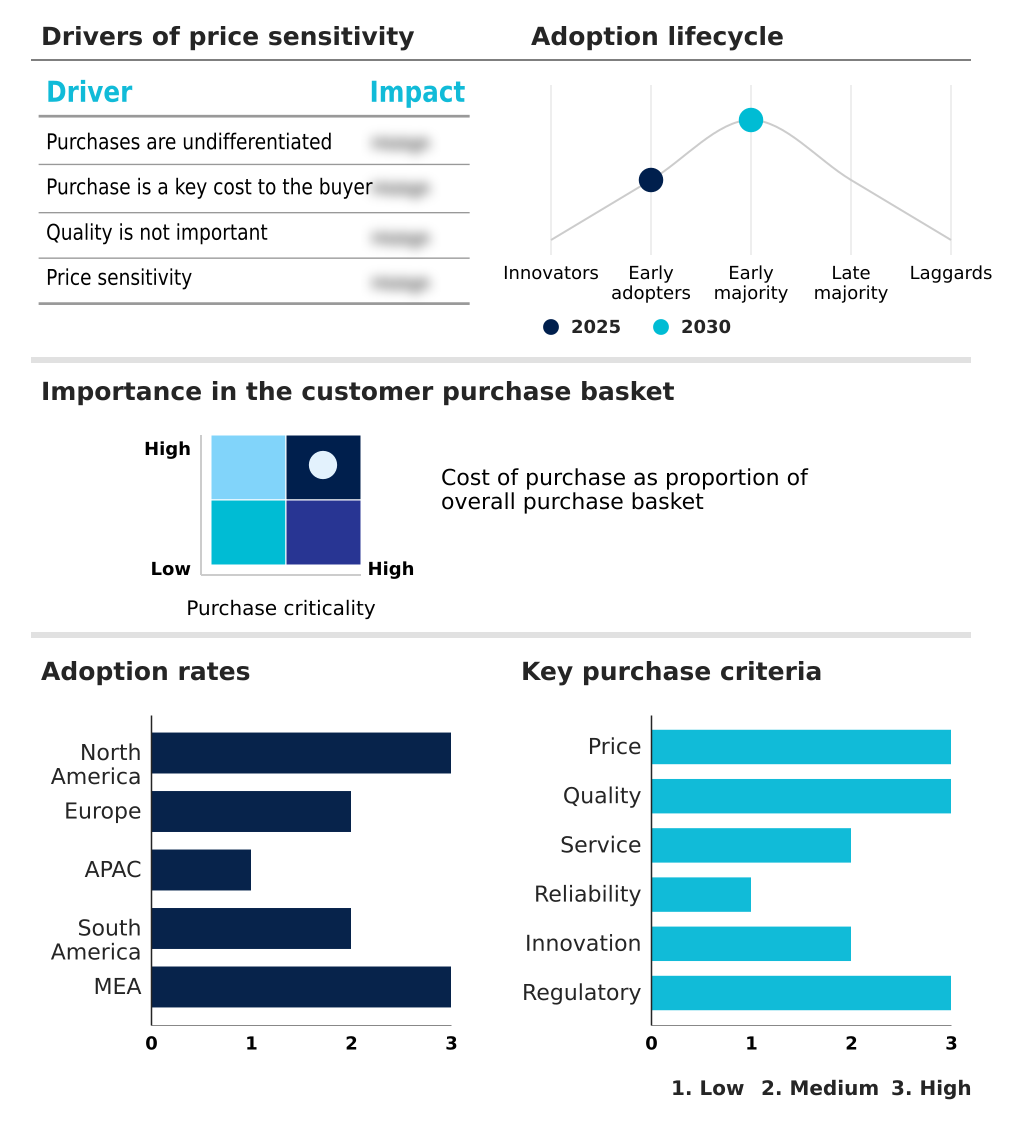

The data center it infrastructure market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center it infrastructure market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Data Center IT Infrastructure Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, data center it infrastructure market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arista Networks Inc. - Analyzes cloud networking solutions and ethernet switch innovations designed for high-performance data center and hyperscale computing environments, emphasizing scalable and efficient data transit.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arista Networks Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Extreme Networks Inc.

- Fujitsu Ltd.

- Gigabyte Technology Co. Ltd.

- Hewlett Packard Enterprise Co.

- Hitachi Vantara LLC

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Lenovo Group Ltd.

- NetApp Inc.

- New H3C Technologies

- NVIDIA Corp.

- Oracle Corp.

- Pure Storage Inc.

- Seagate Technology LLC

- Super Micro Computer Inc.

- Western Digital Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data center it infrastructure market

- In August 2024, a consortium including BMW Group and Mercedes-Benz Group established the Automotive Data Trust Initiative, a project to create a sovereign data-sharing platform for autonomous driving development, mandating that all underlying IT infrastructure be housed within EU borders.

- In February 2025, the sovereign wealth fund of Saudi Arabia and Google Cloud announced Project SAHARA, a joint venture to construct three AI-optimized hyperscale data center regions in the Kingdom, focusing on developing sovereign large language models.

- In March 2025, the Indian Ministry of Electronics and Information Technology launched a Production Linked Incentive scheme for data center IT infrastructure, partnering with Reliance Industries to build a domestic server manufacturing facility to boost self-reliance.

- In April 2025, Microsoft unveiled its Project Isotope initiative, a multi-year plan to re-architect its global Azure data center fleet for generative AI, involving a strategic procurement of next-generation, liquid-cooled servers from partners including Super Micro Computer and NVIDIA.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Center IT Infrastructure Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 324 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2026-2030 | USD 112380.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, Australia, South Korea, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center IT infrastructure market is in a state of architectural transformation, driven primarily by the demands of artificial intelligence and the consequent shift to accelerated computing infrastructure. This evolution necessitates a strategic overhaul of capital expenditure priorities at the boardroom level, moving beyond traditional refresh cycles.

- The focus is now on workload-optimized systems, including high-performance servers equipped with graphics processing units and tensor processing units. This shift is critical for enterprises aiming to leverage AI for a competitive advantage.

- The adoption of technologies like direct liquid cooling and liquid-to-chip cooling is becoming mainstream to manage the thermal output of high-density server racks, with some operators reporting a 40% improvement in cooling efficiency. This transition impacts the entire ecosystem, from server infrastructure and storage infrastructure to the underlying network infrastructure.

- Decisions are no longer just about capacity but about specialized performance, driving investment in hyper-converged infrastructure, all-flash storage arrays, and advanced, low-latency networking to build resilient and scalable platforms for the future.

What are the Key Data Covered in this Data Center IT Infrastructure Market Research and Growth Report?

-

What is the expected growth of the Data Center IT Infrastructure Market between 2026 and 2030?

-

USD 112.38 billion, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Server infrastructure, Storage infrastructure, Software-defined data center, Network infrastructure, and Others), End-user (BFSI, Energy, Information system, and Others), Type (Hyperscale data center, Colocation data center, Enterprise data center, and Edge data center) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential growth of hyperscale cloud services and digital transformation initiatives, Severe supply chain volatility and geopolitical trade restrictions

-

-

Who are the major players in the Data Center IT Infrastructure Market?

-

Arista Networks Inc., Broadcom Inc., Cisco Systems Inc., Dell Technologies Inc., Extreme Networks Inc., Fujitsu Ltd., Gigabyte Technology Co. Ltd., Hewlett Packard Enterprise Co., Hitachi Vantara LLC, Huawei Technologies Co. Ltd., IBM Corp., Lenovo Group Ltd., NetApp Inc., New H3C Technologies, NVIDIA Corp., Oracle Corp., Pure Storage Inc., Seagate Technology LLC, Super Micro Computer Inc. and Western Digital Corp.

-

Market Research Insights

- The data center IT infrastructure market is shaped by a push for greater agility and efficiency. Hybrid cloud management is a core strategy, with enterprises reporting a 35% improvement in deployment flexibility by blending on-premises and cloud resources. This approach facilitates better workload optimization and supports digital transformation initiatives.

- Concurrently, data sovereignty compliance is a non-negotiable driver, compelling organizations to adopt solutions that guarantee data residency. Automated provisioning tools are critical, enabling IT teams to reduce manual configuration errors by up to 60%. These dynamics pressure businesses to refine their procurement strategy, balancing capital expenditure against the long-term benefits of operational resilience and scalable performance for mission-critical applications.

We can help! Our analysts can customize this data center it infrastructure market research report to meet your requirements.

RIA -

RIA -