Spatial Computing Market Size 2024-2028

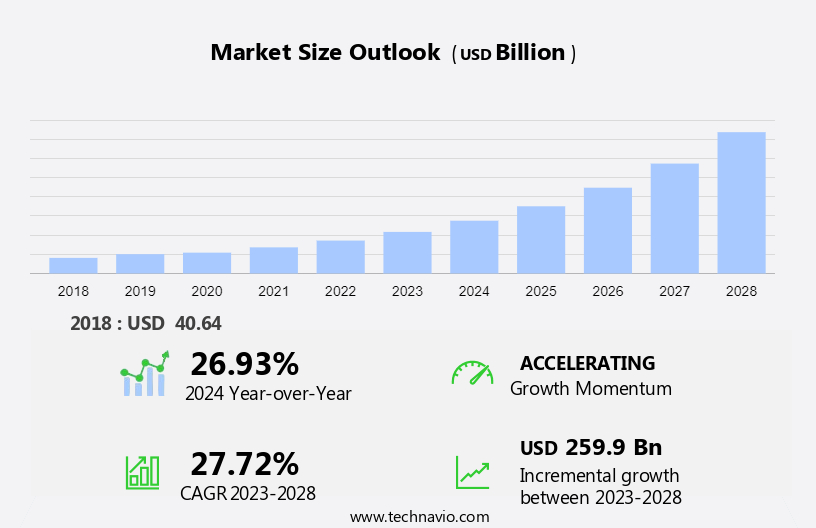

The spatial computing market size is forecast to increase by USD 259.9 billion at a CAGR of 27.72% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for augmented reality (AR) and virtual reality (VR) technology. This trend is driven by advancements in spatial computing technology, which enables the creation of great experiences in various industries such as gaming, education, healthcare, and manufacturing. However, the market faces challenges related to privacy concerns over the use of spatial computing technology. As users become more conscious of their digital footprint, companies must address these concerns by implementing strong security measures and transparent data handling practices. In addition, continued advancements in technology are expected to drive innovation and expand the applications of spatial computing, making it an exciting area to watch In the coming years.

What will be the Size of the Spatial Computing Market During the Forecast Period?

- In the contemporary landscape of healthcare, technological advancements have revolutionized the way medical practitioners engage with patients. Modern healthcare organizations are increasingly adopting spatial computing technologies, such as augmented reality (AR), virtual reality (VR), and mixed reality (MR), to enhance doctor-patient interaction and improve overall healthcare experiences. Doctors and medical practitioners are leveraging these technologies to provide virtual wellness services, offering fitness and mental health assessments and treatments in a more accessible manner. Patients, in turn, benefit from the convenience and personalized care these solutions provide. HMDs (Head-Mounted Displays), VR devices, mobile phones, tablets, and computers are some of the devices driving this market's growth.

- Legacy hardware is being replaced with these advanced technologies, enabling more efficient and effective doctor-patient communication and consultation. The driving forces behind this trend include the investment and funding in technological advancements, the retail sector's integration of spatial computing for customer experiences, and the training and simulation opportunities these technologies offer. In the realm of healthcare, spatial computing is transforming the way we approach wellness, providing new business opportunities and enhancing the patient experience. Spatial computing technologies, including AR, VR, and MR, are revolutionizing the way medical practitioners engage with patients. From virtual wellness services to doctor-patient consultations, these technologies are transforming the healthcare landscape.

How is this Spatial Computing Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Augmented reality

- Virtual reality

- Internet of Things

- Artificial intelligence

- Mixed reality

- Solution

- Hardware

- Software

- Services

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- UK

- Middle East and Africa

- South America

- North America

By Type Insights

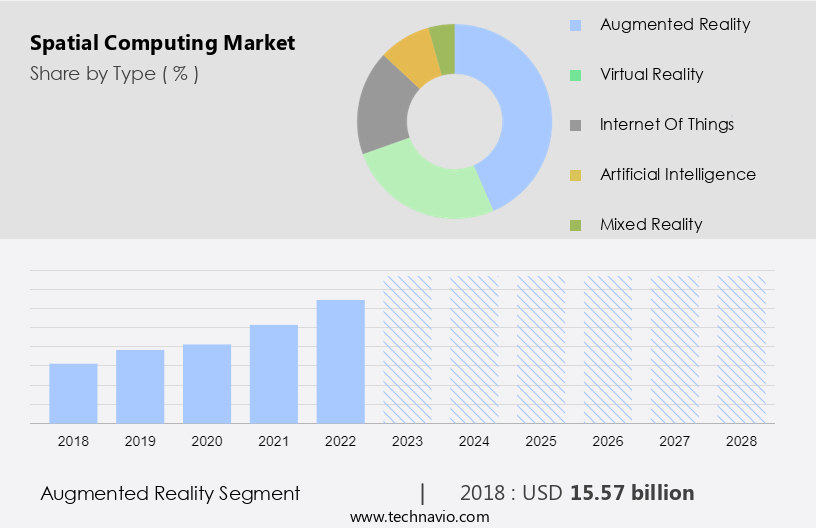

- The augmented reality segment is estimated to witness significant growth during the forecast period.

The market, specifically the Augmented Reality (AR) segment, is experiencing significant growth due to increasing adoption in various industries. AR technology enhances the real world by digitally overlaying information, enabling more efficient and interactive enterprise operations. Factors contributing to this growth include new product launches, expanding applications in healthcare, design and engineering, remote collaboration, training, and education, and increasing investment and funding in AR technology.

AR can be delivered through apps or web-based platforms and is increasingly integrated into industries such as healthcare for medical visualization, design and engineering for prototyping, and car technology for head-up Displays. Technological advancements in AR hardware and software, as well as the integration of AR with platforms like Unity for ads, mediation, and in-app bidding, further fuel market growth. The market is expected to continue expanding during the forecast period, offering opportunities for developers and businesses alike.

Get a glance at the Industry report of share of various segments Request Free Sample

The augmented reality segment was valued at USD 15.57 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

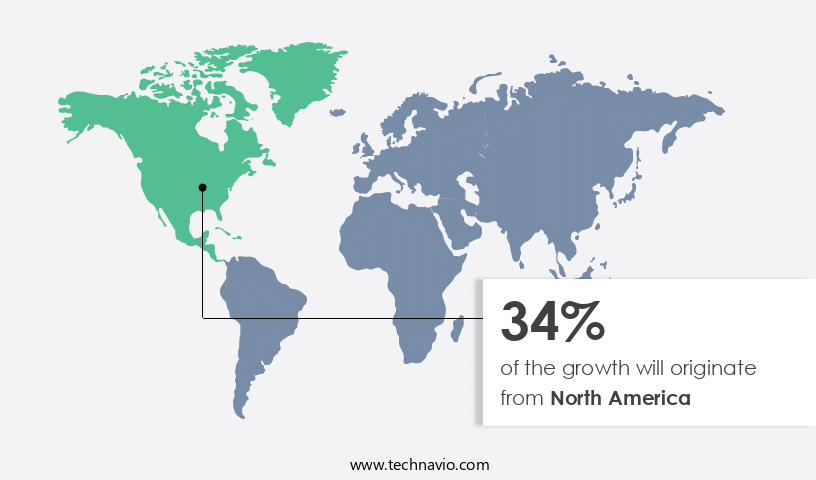

- North America is estimated to contribute 34% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American region dominates The market, accounting for the largest share in 2023. Key factors driving this growth include the presence of major companies, increasing investments in spatial technology, and the rising adoption of advanced applications by consumers. Notable contributors to the market in this region are the US and Canada. The presence of prominent companies is expected to further propel market expansion. The application of spatial technology in modern healthcare organizations, including virtual wellness, fitness, mental health, and doctor-patient interaction, is a significant growth area. Spatial computing is revolutionizing industries by integrating HMDs, legacy hardware, mobile phones, tablets, computers, VR devices, and AR/VR/MR technologies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Spatial Computing Industry?

Growing demand for AR and VR technology is the key driver of the market.

- The market, encompassing augmented reality (AR) and virtual reality (VR) technologies, is experiencing significant growth due to increasing consumer adoption. Modern healthcare organizations and medical practitioners are integrating these technologies for virtual wellness, mental health, doctor-patient interaction, and training. Doctors use VR devices, such as HMDs, to simulate complex medical procedures, while AR glasses offer real-time patient data during surgeries. Economic downturns and consumers' discretionary spending have not hindered the market's growth, as investments in startups and funding for technological development continue. AR and VR applications, including remote work, education, and entertainment, are driving user immersion and presence. The convergence of AR, VR, and MR technologies, along with hardware capabilities, operating systems, and the development landscape, is optimized for consistent, high-quality experiences.

- The aerospace & defense sector, automotive industry, and consumer privacy concerns are among the market's driving forces. Technological advancements in real-time rendering technology, AI/ML solutions deployment, and software handling will further fuel the market's growth during the forecast period. The healthcare end-use segment, including medical visualization, design and engineering, and remote collaboration, is expected to dominate the market.

What are the market trends shaping the Spatial Computing Industry?

Rising technological advancements in spatial computing is the upcoming market trend.

- Spatial computing technology, which includes virtual reality (VR), augmented reality (AR), and mixed reality (MR) devices, is experiencing significant growth due to the integration of egocentric sensing and spatial computation. This technology is revolutionizing various industries, including healthcare, automotive, and aerospace, by providing great experiences and enhancing human-robot collaboration. In modern healthcare organizations, spatial computing is being used for medical visualization, surgical training, patient examination, and medical interventions. Doctors and medical practitioners are utilizing VR headsets, AR glasses, and other spatial computing devices to provide virtual wellness services, improve doctor-patient interaction, and offer remote consultation. The economic downturns caused by the pandemic have led to increased discretionary spending on consumer technologies, driving investments in spatial computing startups and funding for technological development.

- The convergence of AR, VR, and MR technologies with real-time rendering technology, AI/ML solutions, and cloud computing is creating new opportunities for software handling, onboarding, and training. The automotive industry is using spatial computing for car technology market applications, such as Head-up Displays, and In the aerospace sector for simulating applications, and virtual representation of aircraft, satellite, and semiconductor subsystems. The development landscape for spatial computing is optimizing hardware capabilities, operating systems, and user interfaces for consistent, high-quality experiences. The technological advancements in spatial computing are also impacting retail, education, and remote work, with the use of motion controllers, wearable devices, and smartwatches for biometric data tracking and fitness training.

What challenges does the Spatial Computing Industry face during its growth?

Privacy concerns over spatial computing technology is a key challenge affecting the industry growth.

- The market, driven by technologies such as augmented reality (AR), virtual reality (VR), and mixed reality (MR), is transforming various industries, including healthcare. Modern healthcare organizations and medical practitioners are increasingly adopting spatial computing to enhance doctor-patient interaction, virtual wellness, fitness, and mental health applications. HMDs, such as AR glasses and VR headsets, along with legacy hardware like mobile phones, tablets, computers, and VR devices, are key hardware components in this market. AR and VR applications offer user immersion, presence, and real-time rendering technology, driving innovation in medical visualization, design and engineering, prototypes, remote collaboration, training, and education. Spatial computing is also making strides In the aerospace & defense sector for simulating applications, and virtual representation of aircraft, satellites, and other larger systems for prototyping, inspection, malfunctions, safety, and weapon training.

- However, privacy concerns arise due to the vast amounts of sensitive user data collected by AR devices, including biometric data and social networking account information. Consumer privacy, cloud computing, blockchain, and AI/ML solutions are essential to mitigate these concerns. Economic downturns, discretionary spending, and technological advancements influence investments in startups and funding in this market. The development landscape includes hardware capabilities, operating systems, optimization, compatibility testing, customization, and technical intricacies. User interfaces and interaction methods must deliver consistent, high-quality experiences. AR/VR applications use 3D objects, images, video, and textual data, requiring content creation tools, game engines, and authoring platforms.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apple Inc.

- Augtual Reality Pvt Ltd.

- Blippar Ltd.

- HTC Corp.

- Lenovo Group Ltd.

- Magic Leap Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NexTech AR Solutions Corp.

- Nimo Planet Inc.

- NVIDIA Corp.

- PlugXR Reality Pvt. Ltd.

- PTC Inc.

- Rokid.

- Samsung Electronics Co. Ltd.

- Seiko Epson Corp.

- Unity Software Inc.

- Weald Creative Ltd

- Qualcomm Inc.

- Sony Group Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Spatial computing, a revolutionary technology encompassing Augmented Reality (AR), Virtual Reality (VR), and Mixed Reality (MR), is transforming various industries by delivering great experiences and enhancing user interaction. This technology is poised to redefine the way we perceive and engage with digital content, from healthcare to education, entertainment, and beyond. In modern healthcare organizations, spatial computing is revolutionizing doctor-patient interaction. Medical practitioners are utilizing AR and VR to provide virtual wellness services, enabling patients to access fitness programs, mental health resources, and consultations from the comfort of their homes.

Moreover, these technologies offer an unparalleled level of user immersion, allowing for more effective and engaging healthcare experiences. The driving forces behind the market are numerous. Economic downturns have led consumers to focus on discretionary spending, making cost-effective and accessible technologies like AR and VR increasingly popular. Investments in startups and funding for technology development have also been on the rise, fueling innovation and growth In the sector. The gaming and entertainment industries have been early adopters of spatial computing, with VR headsets and AR glasses offering great experiences for consumers. However, the technology's potential extends far beyond entertainment.

Furthermore, in remote work environments, spatial computing enables real-time collaboration and training, allowing teams to work together seamlessly from anywhere In the world. Government stimulus packages and technological advancements have further accelerated the adoption of spatial computing. Real-time rendering technology and AR/VR applications have found applications in various sectors, including aerospace & defense, where they are used for simulating applications, virtual representation, and training. The development landscape for spatial computing is diverse and complex. Optimization, compatibility testing, and customization are essential considerations for hardware capabilities, operating systems, and user interfaces. Interaction methods and user experiences must be consistent and high-quality to ensure a seamless and engaging experience for users.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 27.72% |

|

Market Growth 2024-2028 |

USD 259.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

26.93 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -