Spherical Alumina Filler Market Size 2024-2028

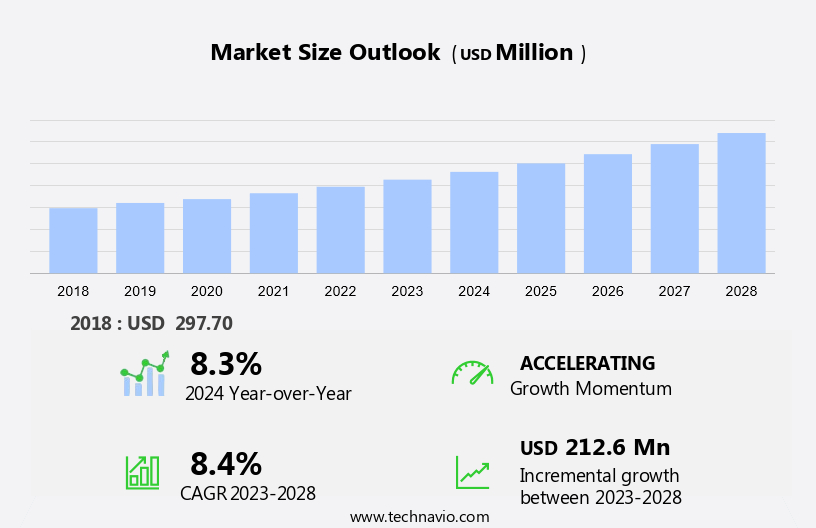

The spherical alumina filler market size is forecast to increase by USD 212.6 million at a CAGR of 8.4% between 2023 and 2028.

- The market is experiencing significant growth due to the expanding electronic industry, which is driving the demand for lightweight and high-performance components. companies in this market are focusing on inorganic growth strategies, such as mergers and acquisitions, to expand their product portfolios and strengthen their market positions. In the ceramics and abrasives sectors, it is used for its excellent grinding and polishing capabilities. However, fluctuations in raw material prices pose a challenge to market growth. Producers must closely monitor these price trends and implement cost management strategies to mitigate their impact on profitability. Additionally, increasing competition and the need for product differentiation are key trends shaping the market. Companies that can offer innovative solutions and competitive pricing will be well-positioned to succeed in this dynamic market.

What will be the Size of the Market During the Forecast Period?

- The market encompasses the production and supply of spherical alumina, a thermally conductive material, used primarily in thermal interface materials and advanced ceramics. This market is driven by the increasing demand for effective thermal management solutions in various industries, including new energy vehicles, 5G technology, and high-performance composite materials. The morphology of spherical alumina, characterized by its spherical structure and uniform particle size measured in microns, offers enhanced thermal conductivity and improved thermal interface properties. Manufacturing processes, such as liquid phase precipitation and high-temperature plasma, are used to produce spherical alumina with high sphericity, surface energy, and surface fluidity, ensuring optimal integration into polymer matrices and other materials.

- In addition, the physical and chemical properties of spherical alumina, including its high thermal conductivity, crystalline forms, and resistance to grinding and polishing, make it a sought-after star material in numerous applications. The market is expected to grow significantly due to the increasing demand for energy-efficient thermal management solutions and the expanding use of advanced ceramics in catalysis and other industries.

How is this Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

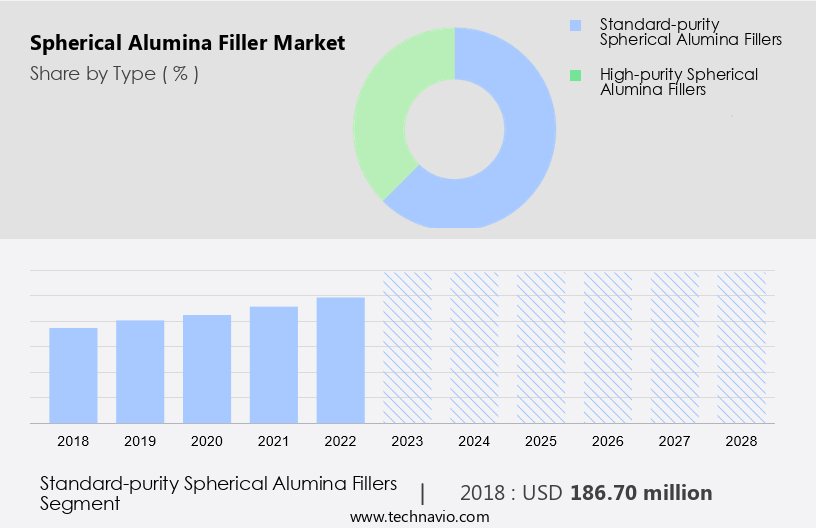

- Standard-purity spherical alumina fillers

- High-purity spherical alumina fillers

- End-user

- Electronics

- Automotive

- Aerospace and defence

- Others

- Geography

- APAC

- China

- India

- Japan

- South Korea

- North America

- Canada

- US

- Europe

- Germany

- UK

- South America

- Brazil

- Middle East and Africa

- APAC

By Type Insights

- The standard-purity spherical alumina fillers segment is estimated to witness significant growth during the forecast period.

The market encompasses standard-purity alumina fillers, which are integral to various industries due to their cost-effective thermal management properties. These fillers, boasting purity levels between 99.0% and 99.8%, are crucial in sectors such as automotive, electronics, and industrial manufacturing. In the automotive industry, standard-purity spherical alumina fillers are employed in resins and rubbers to enhance the thermal conductivity of components like electronic control units, battery packs, and LED lighting systems. The morphology of these fillers, characterized by their spherical structure and controlled particle size in microns, enables improved thermal interface materials. Manufacturing processes like liquid phase precipitation, high-temperature plasma, and spray pyrolysis are utilized to achieve the desired sphericity, surface energy, and surface fluidity for optimal integration into polymer matrices.

Get a glance at the Spherical Alumina Filler Industry report of share of various segments Request Free Sample

The standard-purity spherical alumina fillers segment was valued at USD 186.70 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

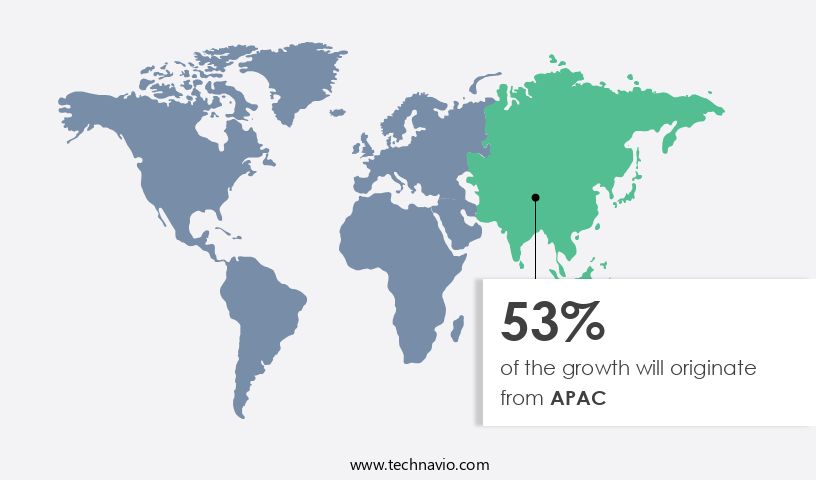

- APAC is estimated to contribute 53% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The APAC region is a major contributor to the market due to rapid industrialization, technological advancements, and substantial investments in sectors such as electronics, automotive, and defense. The Indian electronic manufacturing sector, in particular, is experiencing significant growth, projected to reach approximately USD250 billion by 2029. This expansion is driven by increasing domestic production and the Indian government's efforts to establish the country as a global manufacturing hub. Spherical alumina fillers play a crucial role In thermal management for electronic devices, making them an essential component in this growing industry. With a spherical structure and morphology, spherical alumina fillers offer improved thermal conductivity, making them effective thermally conductive fillers for thermal interface materials.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Spherical Alumina Filler Industry?

Growing electronic industry is the key driver of the market.

- The market is experiencing significant growth due to the increasing demand for thermally conductive materials in various industries. Spherical alumina, as a thermal interface material, offers superior thermal conductivity and morphology, which makes it an ideal choice for applications requiring efficient thermal management. The spherical structure and small particle size, typically measured in microns, contribute to the material's high packing density, fluidity, and application performance. Manufacturing processes like liquid phase precipitation, high-temperature plasma, and spray pyrolysis are used to produce spherical alumina with high sphericity, surface energy, and surface fluidity. These properties make it an excellent additive for composite materials, including advanced ceramics, catalysts, and polymer matrices.

- In addition, the global electronic industry's expansion, driven by the development of new energy vehicles, 5G technology, and advanced ceramics, is a significant market driver for spherical alumina fillers. The material's unique thermal insulator properties, thermal stability, thermal expansion coefficient, and mechanical properties make it an essential component in electronic packaging, integrated circuits (ICs), and thermal insulator applications. In the petrochemical industry, spherical alumina is used as a refractory material due to its high thermal conductivity and resistance to high temperatures. In the papermaking industry, it is used as a filler to improve paper strength and thermal insulation.

What are the market trends shaping the Spherical Alumina Filler Industry?

Inorganic growth by companies is the upcoming market trend.

- The market is witnessing notable growth, driven by the increasing demand for advanced thermal management solutions in various industries. Spherical alumina, a type of thermally conductive material, is a key component In thermal interface materials (TIMs), which facilitate efficient heat dissipation and maintain high performance in applications such as electronics, new energy vehicles, and 5G infrastructure. The morphology of spherical alumina, characterized by its spherical structure and narrow particle size distribution in microns, enhances its properties, including thermal conductivity, surface energy, and surface fluidity. Manufacturing techniques such as liquid phase precipitation, high-temperature plasma, and spray pyrolysis are used to produce spherical alumina with high sphericity and improved physical and chemical properties.

- Moreover, composite materials made with spherical alumina fillers exhibit superior application performance, including composites for thermal insulation, electrical insulation, and mechanical properties. In the polymer matrix, spherical alumina enhances the packing density, fluidity, and viscosity of the composite material, leading to improved thermal stability, thermal expansion coefficient, and thermal cycling performance. The market for spherical alumina fillers is diverse, with applications in various industries such as electronics, petrochemicals, refractories, ceramics, abrasives, papermaking, aerospace, and packaging. Other thermally conductive materials, including aluminum nitride (AlN), silica (SiO2), silicon carbide (SiC), carbon nanotubes (CNTs), graphene, and nano-sheets, are also used in similar applications, but spherical alumina's unique properties make it a star material for thermal management solutions.

What challenges does the Spherical Alumina Filler Industry face during its growth?

Fluctuations in raw material prices is a key challenge affecting the industry growth.

- The market is currently experiencing volatility due to price fluctuations in raw materials. Since early 2024, the alumina industry has faced persistent supply disruptions, causing a continuous rise in prices. For instance, on October 14, 2024, the Shanghai Futures Exchange (SHFE) recorded an all-time high for its main alumina contract, with prices reaching USD677.30 per ton and closing at USD676.88 per ton. This instability in raw material pricing poses challenges for industries reliant on spherical alumina fillers, such as automotive, aerospace, and electronics. Manufacturers In these sectors face increased costs, potentially leading to production delays and higher end-product prices.

- Furthermore, morphology and particle size are crucial factors In the production of spherical alumina fillers, which are essential In thermal interface materials, thermal management systems, and composite materials. Techniques like liquid phase precipitation, high-temperature plasma, and spray pyrolysis are used to produce spherical alumina with high sphericity, surface energy, surface fluidity, and packing density. These physical and chemical properties make spherical alumina a valuable additive in various applications, including thermal insulation, electrical insulation, and catalysis. In the electronics industry, spherical alumina is used in electronic packaging, integrated circuits (ICs), and thermal insulator properties. In the petrochemical industry, refractories, ceramics, abrasives, and papermaking benefit from the use of spherical alumina fillers.

Exclusive Customer Landscape

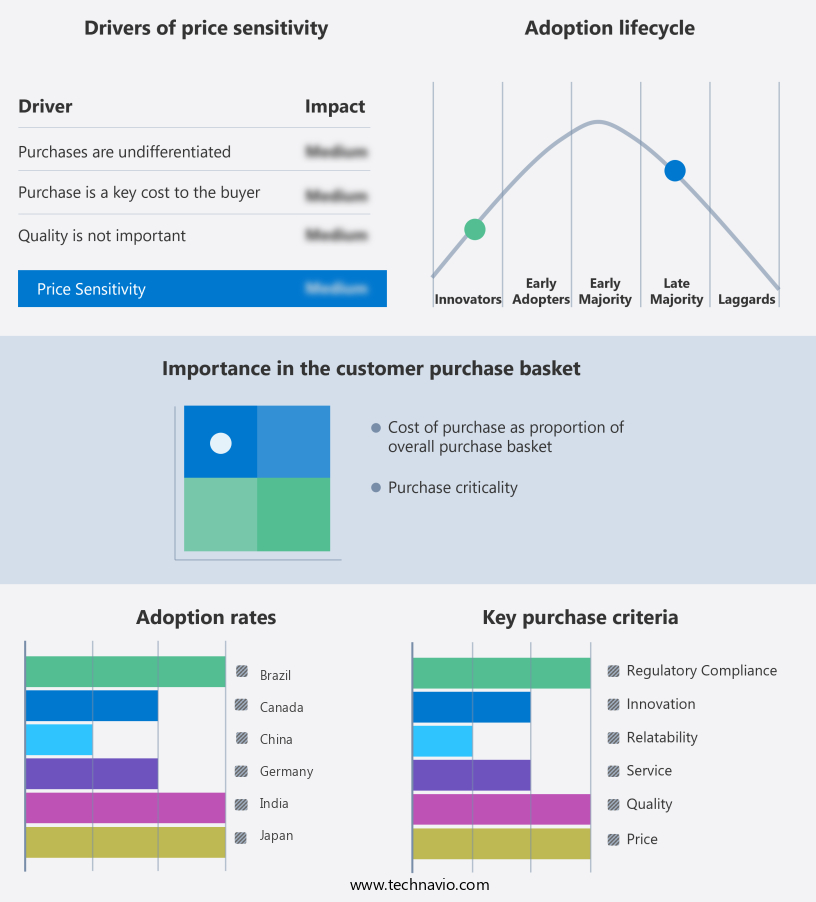

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Admatechs Corp Ltd.

- Advanced Ceramic Materials

- Almatis BV

- Bestry

- Chengdu Huarui Industrial Co. Ltd.

- Compagnie de Saint-Gobain SA

- DAEHAN CERAMICS Co Ltd.

- Denka Co. Ltd.

- GNPGraystar

- Momentive Technologies Inc.

- Nippon Steel Corp.

- Resonac Holdings Corp.

- SAT nano Technology Material Co. Ltd.

- SCR Sibelco NV

- Stanford Advanced Materials

- Sumitomo Chemical Co. Ltd.

- TOPCO TECHNOLOGIES CORP.

- Zibo Aotai New Material Technology Co. Ltd.

- ZIBO LITUO COMPOSITE Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Spherical alumina fillers have gained significant attention in various industries due to their unique thermal conductivity properties. These fillers, also known as thermally conductive fillers, play a crucial role In thermal interface materials (TIM), which are essential components in managing the thermal performance of electronic devices and new energy vehicles. The morphology of spherical alumina fillers, characterized by their spherical structure and consistent particle size, contributes to their superior thermal conductivity. The particle size, typically measured in microns, influences the filler's ability to transfer heat efficiently within the polymer matrix of composite materials. The production methods for spherical alumina fillers include liquid phase precipitation and high-temperature plasma.

In addition, the former method involves the precipitation of alumina particles from a liquid solution, while the latter method uses plasma to generate spherical alumina particles. Both methods aim to produce spherical particles with high sphericity, ensuring optimal thermal conductivity and improved application performance. Surface energy and surface fluidity are essential factors In the production and application of spherical alumina fillers. A high surface energy and fluidity facilitate the wetting and dispersion of the filler In the polymer matrix, enhancing the composite material's overall thermal management capabilities. Thermal management is a critical application area for spherical alumina fillers, with significant demand coming from the electronics industry.

Furthermore, the high thermal conductivity of these fillers enables efficient heat dissipation in electronic packaging, integrated circuits (ICS), and thermal insulator properties. In new energy vehicles, spherical alumina fillers contribute to improved thermal stability and thermal expansion coefficient, essential for battery cooling and overall vehicle performance. Advanced ceramics, refractories, ceramics, abrasives, papermaking, aerospace, and the petrochemical industry are other sectors that utilize spherical alumina fillers. In these industries, spherical alumina is employed as a high-performance composite material due to its excellent mechanical properties, including packing density, fluidity, and viscosity. The physical and chemical properties of spherical alumina fillers, such as crystal forms, thermal stability, and electrical insulation, make them suitable for various applications.

In addition, the thermal cycling and thermal percolation threshold properties of these fillers are essential for their application In thermal interface materials and composite materials. Ceramic fillers, including aluminum nitride (AlN), silica (SiO2), silicon carbide (SiC), carbon nanotubes (CNTs), graphene, nano-sheets, and other materials, are often compared to spherical alumina fillers in terms of their thermal conductivity and application performance. However, the unique morphology and production methods of spherical alumina fillers set them apart, making them a preferred choice for specific applications. Their unique morphology, production methods, and physical and chemical properties make them an essential component in various industries, including electronics, new energy vehicles, and advanced ceramics. The ongoing research and development In the field of spherical alumina fillers are expected to further expand their applications and improve their performance in various industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

207 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.4% |

|

Market growth 2024-2028 |

USD 212.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.3 |

|

Key countries |

US, China, Japan, South Korea, Germany, Canada, Brazil, UK, Taiwan, and India |

|

Competitive landscape |

Leading Companies, market growth and forecasting, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -