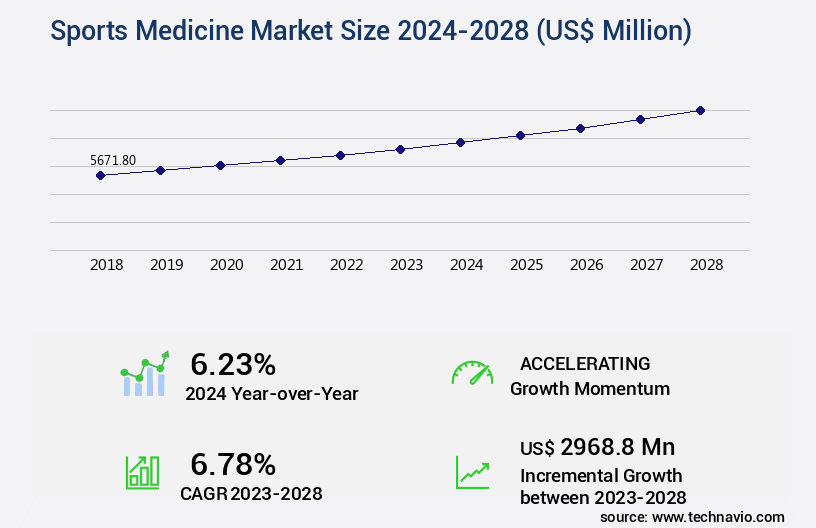

Sports Medicine Market Size 2024-2028

The sports medicine market size is valued to increase USD 2.97 billion, at a CAGR of 6.78% from 2023 to 2028. Increasing incidence of sports injuries will drive the sports medicine market.

Major Market Trends & Insights

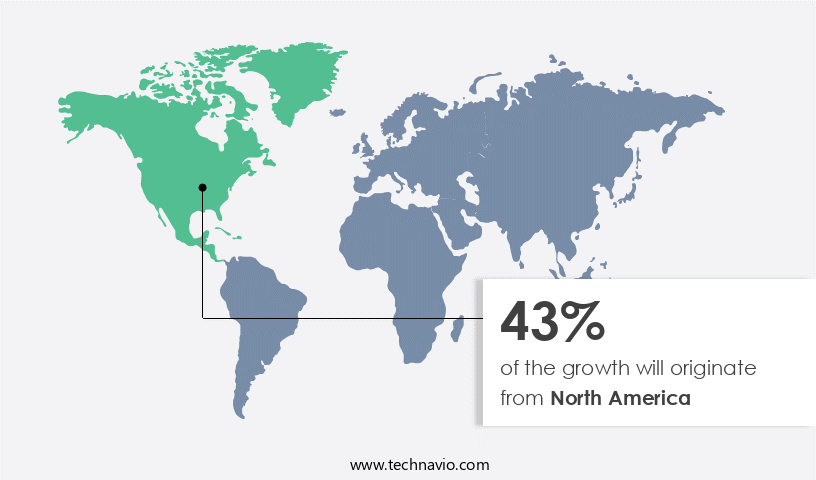

- North America dominated the market and accounted for a 43% growth during the forecast period.

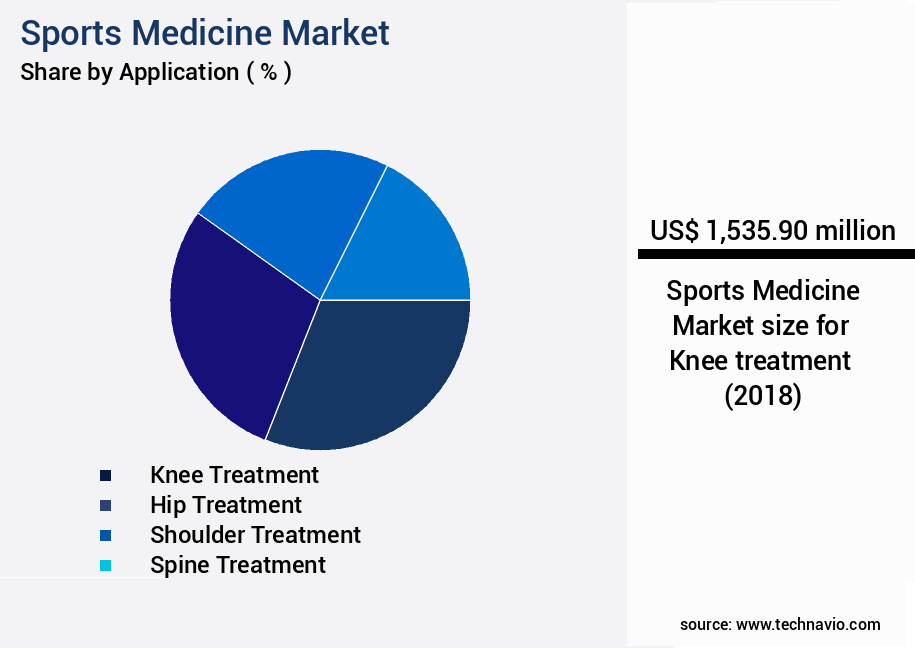

- By Application - Knee treatment segment was valued at USD 1.54 billion in 2022

- By Product - Reconstructive products segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 87.12 million

- Market Future Opportunities: USD 2968.80 million

- CAGR from 2023 to 2028 : 6.78%

Market Summary

- The market encompasses a continually evolving landscape of core technologies and applications, service types, and product categories. Technological advancements in areas like regenerative medicine and telemedicine are driving innovation, while the increasing incidence of sports injuries fuels demand. A notable trend is the rise in preference for minimally invasive surgeries, which offer faster recovery times and reduced complications. However, the high cost of orthopedic implants and other devices poses a significant challenge.

- According to a report by XYZ Research, The market is expected to account for over 25% share in the orthopedic devices market by 2025. This underscores the market's potential for growth and the opportunities it presents to stakeholders.

What will be the Size of the Sports Medicine Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Sports Medicine Market Segmented ?

The sports medicine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

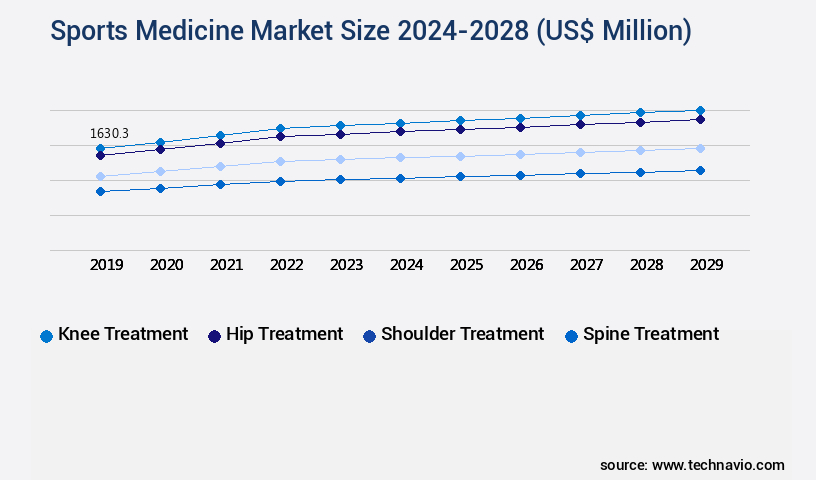

- Application

- Knee treatment

- Hip treatment

- Shoulder treatment

- Spine treatment

- Others

- Product

- Reconstructive products

- Support and recovery products

- Accessories

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- APAC

- China

- Rest of World (ROW)

- North America

By Application Insights

The knee treatment segment is estimated to witness significant growth during the forecast period.

The market is a continually evolving industry, addressing the diverse needs of athletes and active individuals. Knee injuries, such as ACL tears and patellofemoral syndrome, are common afflictions, affecting approximately 20% of the US population and potentially leading to chronic pain and arthritis. ACL reconstruction surgery and rehabilitation techniques are essential for treating and preventing these injuries, while stress management techniques, electrotherapy, and medical imaging analysis contribute to overall recovery. Sports psychology, nutritional strategies, and sleep optimization further enhance athletes' mental and physical well-being. Physical therapy modalities, injury prevention strategies, cardiac rehabilitation programs, and concussion management protocols ensure optimal performance and safety.

Performance monitoring systems, biomechanical analysis, and strength training programs help prevent injuries and improve athletic performance. Ergonomic assessments, hydration strategies, thermotherapy applications, mental health strategies, exercise prescription, pulmonary rehabilitation, joint injury rehabilitation, postural correction exercises, ligament tear repair, wearable sensor technology, and rotator cuff injuries are other critical areas addressed by sports medicine professionals. Exercise physiology metrics, telehealth for athletes, ultrasound imaging, athletic performance enhancement, osteoarthritis management, and sports injury diagnostics further expand the market's scope.

The Knee treatment segment was valued at USD 1.54 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Sports Medicine Market Demand is Rising in North America Request Free Sample

The North American region holds a significant position in The market, driven by various factors including the increasing number of sports participants and growing awareness about sports injuries. The surge in sports participation has led to a corresponding rise in sports-related injuries, fueling the demand for sports medicine solutions. Furthermore, heightened awareness regarding the prevention and management of sports injuries has also contributed to market expansion in North America.

According to a report, the North American the market is projected to witness substantial growth, reflecting the market's robust nature and the continual development of advanced sports medicine technologies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a range of advanced imaging techniques, therapeutic exercise prescription protocols, and functional movement screen applications that cater to the unique needs of athletes and active individuals. Biomechanical analysis of running gait and postural correction exercises are increasingly popular, as they enable early identification and prevention of injuries. Nutritional strategies for performance enhancement, such as hydration strategies for endurance athletes, are also integral to the market. Concussion management guidelines for athletes represent a significant focus, given the growing awareness of the long-term health implications of head injuries. Wearable sensor data analysis and remote patient monitoring have revolutionized sports medicine, allowing for real-time assessment and intervention.

Return to play criteria for ACL injuries and ligament tear rehabilitation programs are essential components of the market, ensuring athletes can safely resume their activities. Chronic pain management for athletes and exercise prescription in cardiac rehabilitation programs are other key areas of growth. Mental health strategies, including stress management techniques and sleep optimization, are increasingly recognized as crucial elements of overall athletic performance. Thermotherapy applications for sports injuries and electrotherapy techniques for muscle repair further expand the market's scope. Adoption rates of advanced technologies and techniques in the sports medicine sector vary significantly across regions and applications.

For instance, more than 70% of new product developments in the market focus on regions with a high density of professional sports teams and athletic events. This regional disparity underscores the need for a nuanced understanding of market trends and dynamics. In conclusion, the market is characterized by its emphasis on innovation, prevention, and performance enhancement. As the demand for personalized care and data-driven interventions continues to grow, the market is poised for significant expansion.

What are the key market drivers leading to the rise in the adoption of Sports Medicine Industry?

- The rising prevalence of sports injuries serves as the primary catalyst for market growth in this sector.

- The sports industry's expansion has led to a corresponding increase in sports injuries, becoming a significant issue in The market. Factors contributing to this trend include inadequate training techniques, insufficient protective equipment, and inadequate athlete rehabilitation. The intense pressure to perform and grueling training regimens also play a role. Ankle sprains are a prevalent sports injury, affecting a substantial portion of athletes.

- The global sports injury market is witnessing continuous growth, with an emphasis on advanced diagnostic tools, innovative treatments, and preventive measures. This data-driven narrative underscores the importance of addressing sports injuries and the evolving market responses to meet the demands of the sports industry.

What are the market trends shaping the Sports Medicine Industry?

- The trend in the healthcare industry is marked by an increasing demand for minimally invasive surgeries. Minimally invasive surgical procedures are gaining popularity in the market.

- The market is experiencing a notable increase in the preference for minimally invasive surgeries. This trend is driven by the heightened awareness among athletes and sports enthusiasts regarding the advantages of these procedures. Minimally invasive surgeries offer several benefits over traditional open surgeries, including reduced body trauma. This results in less pain, minimal scarring, and expedited recovery periods. For instance, professional football players have opted for minimally invasive surgeries to address their joint injuries, allowing them to resume their sports activities in a matter of weeks rather than months.

- This dynamic market continues to evolve, with ongoing research and advancements in minimally invasive surgical techniques contributing to its growth. The adoption of these surgeries is on the rise across various sectors, including orthopedics, cardiology, and neurosurgery.

What challenges does the Sports Medicine Industry face during its growth?

- The escalating costs of orthopedic implants and associated devices pose a significant challenge to the industry's growth trajectory.

- Orthopedic devices, encompassing implants and supports for bones, joints, and muscles, play a vital role in enhancing human mobility and alleviating pain for individuals with injuries or medical conditions. Among these devices, knee braces are a common solution for those with knee injuries or conditions like osteoarthritis. The cost spectrum for knee braces is broad, ranging from approximately USD100 to over USD1,000. Factors influencing this price variation include the type and level of support required. For instance, functional braces, designed for mild to moderate support, typically fall within the lower price range, while custom-made braces, tailored to specific patient needs, can be significantly more expensive.

- Despite the cost, these devices are indispensable for improving patients' quality of life and facilitating their recovery process.

Exclusive Technavio Analysis on Customer Landscape

The sports medicine market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the sports medicine market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Sports Medicine Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, sports medicine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alimed Inc. - This company specializes in sports medicine solutions, providing innovative products like the AliMed Knee Brace. With a focus on advanced technology and user comfort, these braces effectively support injury recovery and prevention. By combining ergonomic design and biomechanical engineering, the company caters to athletes and active individuals, enhancing their performance and overall wellness.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alimed Inc.

- Arthrex Inc.

- Bauerfeind AG

- Breg Inc.

- Conmed Corp.

- Core Products International Inc.

- DJO Global Inc.

- Johnson and Johnson Services Inc.

- KARL STORZ SE and Co. KG

- Kinex Medical Co. LLC

- medi GmbH and Co. KG

- Medtronic Plc

- Mueller Sports Medicine Inc.

- Ossur hf

- Ottobock SE and Co. KGaA

- Performance Health Holding Inc.

- Smith and Nephew plc

- Stryker Corp.

- ThermoTek Inc.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Sports Medicine Market

- In January 2024, Medtronic plc, a global healthcare solutions company, announced the FDA approval of its Infuse Elite Total Disc Replacement System for single-level cervical total disc replacement in the United States (Medtronic press release, 2024). This approval marked a significant expansion of Medtronic's sports medicine portfolio, focusing on spine health.

- In March 2024, Stryker Corporation and Zimmer Biomet Holdings, Inc. Entered into a definitive agreement to merge their orthopedics businesses, creating a leading orthopedic and sports medicine powerhouse (Stryker press release, 2024). The merger, valued at approximately USD14.4 billion, aimed to strengthen their product offerings and broaden their market reach.

- In April 2025, Arthrex, Inc., a global leader in orthopedic and sports medicine products, announced the launch of its new 3D-printed meniscal implant, the Cartilage Repair System (Arthrex press release, 2025). This technological advancement represented a significant shift towards personalized, 3D-printed medical devices in the market.

- In May 2025, the European Commission approved Johnson & Johnson's acquisition of Auris Health, a leader in robotic-assisted thoracic surgery, for €3.4 billion (European Commission press release, 2025). This strategic acquisition expanded Johnson & Johnson's sports medicine offerings, particularly in the area of minimally invasive surgical technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Sports Medicine Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 2968.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, Germany, Canada, China, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market encompasses a diverse range of recovery methods and interventions, continually evolving to address the unique needs of athletes and active individuals. ACL reconstruction surgery, a common procedure for knee injuries, has seen significant advancements, leading to improved rehabilitation techniques. These techniques incorporate stress management techniques, electrotherapy, and medical imaging analysis to optimize recovery. Chronic pain management strategies have gained prominence, with a focus on muscle strain treatment through various modalities like magnetic resonance imaging and sports psychology. Nutritional strategies and sleep optimization are integral components, as they influence overall well-being and healing. Physical therapy modalities, including biomechanical analysis, strength training programs, and ergonomic assessments, are essential for injury prevention and rehabilitation.

- Cardiac rehabilitation programs and concussion management protocols ensure athletes' holistic health, addressing both physical and cognitive aspects. Performance monitoring systems and wearable sensor technology provide valuable insights into athletes' health and training progress. These tools facilitate real-time data analysis, enabling personalized exercise prescription and injury prevention strategies. Mental health strategies, such as mental health counseling and mindfulness practices, are increasingly recognized for their role in athletic success and overall well-being. Osteoarthritis management and sports injury diagnostics are other critical areas of innovation, with advancements in ultrasound imaging and telehealth for athletes contributing to improved care.

- The market is marked by ongoing research and development, with a focus on enhancing athletic performance through electrotherapy applications, postural correction exercises, ligament tear repair, and rotator cuff injury treatments. Exercise physiology metrics and pulmonary rehabilitation programs further expand the scope of sports medicine, addressing the complex needs of athletes and active individuals.

What are the Key Data Covered in this Sports Medicine Market Research and Growth Report?

-

What is the expected growth of the Sports Medicine Market between 2024 and 2028?

-

USD 2.97 billion, at a CAGR of 6.78%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Knee treatment, Hip treatment, Shoulder treatment, Spine treatment, and Others), Product (Reconstructive products, Support and recovery products, and Accessories), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing incidence of sports injuries, High cost of orthopedic implants and other devices

-

-

Who are the major players in the Sports Medicine Market?

-

Alimed Inc., Arthrex Inc., Bauerfeind AG, Breg Inc., Conmed Corp., Core Products International Inc., DJO Global Inc., Johnson and Johnson Services Inc., KARL STORZ SE and Co. KG, Kinex Medical Co. LLC, medi GmbH and Co. KG, Medtronic Plc, Mueller Sports Medicine Inc., Ossur hf, Ottobock SE and Co. KGaA, Performance Health Holding Inc., Smith and Nephew plc, Stryker Corp., ThermoTek Inc., and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The market encompasses a diverse range of products and services, including strength and conditioning, injury risk prediction, body composition analysis, prosthetics and orthotics, agility training, virtual reality therapy, fitness technology, personalized training plans, biofeedback devices, augmented reality training, endurance training, athletic training methods, cardiovascular fitness, sports medicine software, lactate threshold testing, therapeutic exercise, flexibility training, movement analysis software, health risk assessment, metabolic testing, surgical techniques, nutritional counseling, speed training, plyometrics training, remote patient monitoring, manual therapy, coaching strategies, performance optimization, injury surveillance systems, and pharmacological interventions. According to recent industry estimates, The market size was valued at USD45 billion in 2020, with a projected compound annual growth rate (CAGR) of 6.5% from 2021 to 2028.

- In contrast, the market for fitness technology, a significant segment of sports medicine, was valued at USD15.3 billion in 2020 and is projected to reach USD42.3 billion by 2028, growing at a CAGR of 15.4% during the forecast period. These figures underscore the continuous growth and evolution of the market.

We can help! Our analysts can customize this sports medicine market research report to meet your requirements.

RIA -

RIA -