Stevedoring and Marine Cargo Handling Market Size 2024-2028

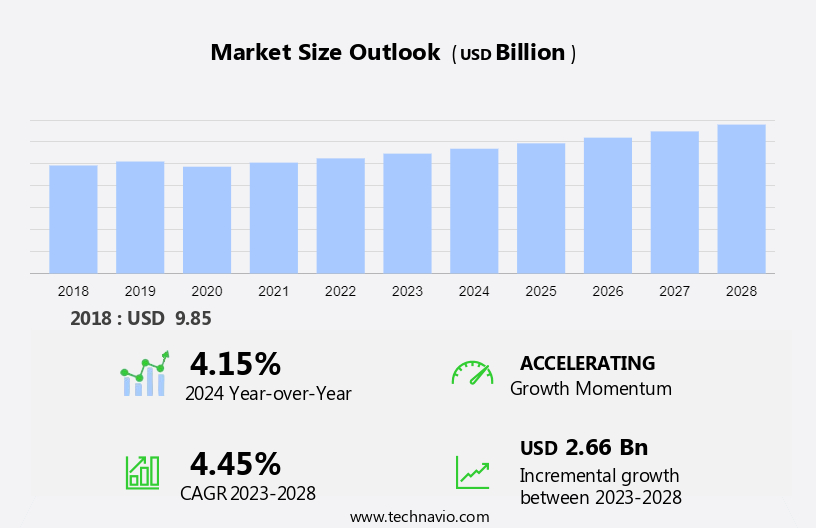

The stevedoring and marine cargo handling market size is forecast to increase by USD 2.66 billion at a CAGR of 4.45% between 2023 and 2028. The market is witnessing significant growth due to the increasing adoption of containerization as a more efficient and cost-effective method for transporting goods. This trend is particularly evident in international trade, where container ships dominate the seaborne trade landscape. Another key trend is the emergence of smart ports and IoT integration in stevedoring and marine cargo handling, which enhances operational efficiency and reduces errors.

Furthermore, congestion issues in ports and terminals continue to pose a challenge, necessitating the adoption of advanced technologies and strategies to streamline operations and improve turnaround times. Overall, the market is expected to experience strong growth in the coming years, driven by these and other factors.

The market is experiencing significant growth due to the privatization of ports and the increasing volume of seaborne trade. The market is driven by the rise in waterborne transportation of containerized cargo shipping, gas shipping, and dry bulk shipping. Automated technology, online commerce, and the digital transformation of maritime logistics are also key factors fueling market growth. Cargo handling equipment, such as forklift trucks and cranes, play a crucial role in the efficient handling of marine cargo. The market is also influenced by inflation, which affects the cost of fuel and cargo handling services. Fuel efficiency and emission norms are becoming increasingly important in the shipping industry, leading to the adoption of market and novel technologies.

Furthermore, the market for cargo handling in the maritime industry caters to various sectors, including crude oil shipments, gas shipping, and dry bulk shipping. The market is further segmented into containerized cargo and non-containerized cargo. Air cargo movement is another important aspect of the market, which is influenced by factors such as fuel efficiency, propulsion type, and secure transportation. The market is expected to grow at a steady pace due to the increasing demand for low-cost transportation and the secure transportation of goods. The integration of automation and e-commerce is also expected to drive market growth. Despite these opportunities, the market faces challenges such as inflation, emission norms, and the need for advanced cargo-handling equipment.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Type

- Bulk Cargo

- Containerized cargo

- Others

- Service

- Stevedoring

- Cargo handling and transportation

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- France

- North America

- US

- Middle East and Africa

- South America

- APAC

By Type Insights

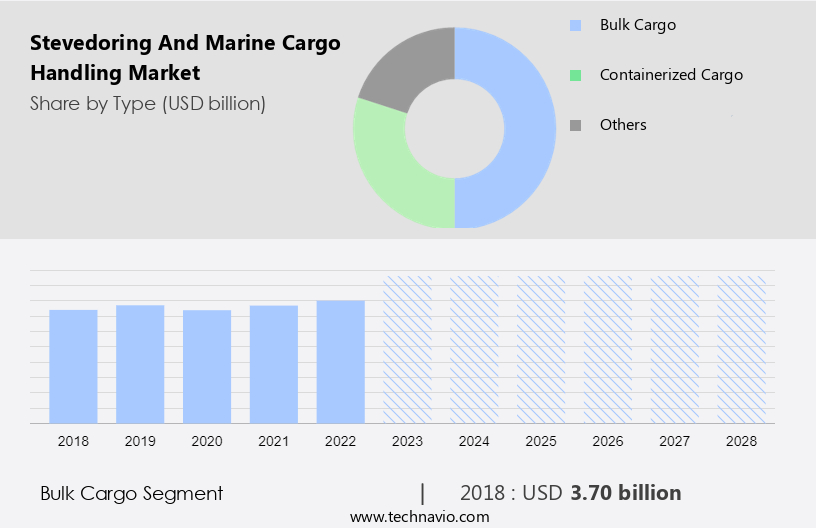

The bulk cargo segment is estimated to witness significant growth during the forecast period. The maritime industry encompasses various sectors, including marine cargo handling, which is undergoing significant transformation due to privatization, automation, and inflation. Marine cargo handling involves the efficient movement and stacking of diverse cargoes, such as containerized goods, dry bulk shipping, gas shipping, and crude oil shipments, at marine ports. Stevedoring companies specialize in this process, utilizing specialized cargo handling equipment, including cranes, forklift trucks, and conveyor systems. Waterborne transportation plays a crucial role in global trade, with seaborne trade volume accounting for a substantial proportion of international commerce. Macroeconomic headwinds, such as retail sales, industrial production, and e-commerce growth, impact the demand for cargo handling services.

Furthermore, automated technology, including online commerce, has transformed the logistics landscape, necessitating the need for low-cost, secure, and fuel-efficient transportation solutions. Fuel efficiency and emission norms are critical considerations for cargo transportation, with market and propulsion type gaining prominence. Air cargo movement complements seaborne trade, but its growth is influenced by factors such as fuel costs and competition from e-commerce. Stevedoring companies adapt to these trends by investing in novel technologies and optimizing their operations to cater to the unique requirements of various cargo types.

Get a glance at the market share of various segments Request Free Sample

The bulk cargo segment was valued at USD 3.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

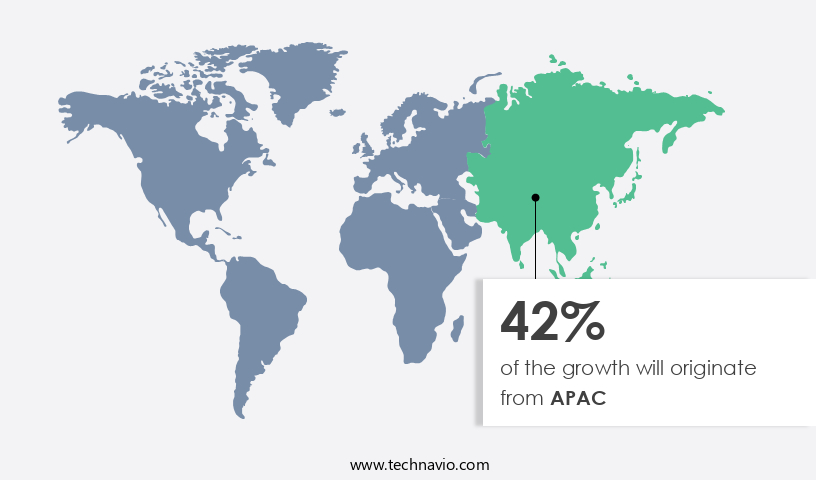

APAC is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the APAC region, the shipping industry experiences continuous growth due to increasing international trade activities driven by economic development, industrialization, and globalization. This wave in trade volumes, consisting of various cargo types such as manufactured goods, raw materials, energy products, and agricultural commodities, necessitates efficient cargo handling and port services. The transformation of maritime logistics through containerization has become the preferred mode of cargo transportation in the APAC region, accounting for a significant portion of maritime trade. Container handling services, container terminals, and specialized equipment for handling containerized cargo are in high demand. Stevedoring companies are essential players in this sector, supporting efficient container movement and transshipment activities.

Moreover, the adoption of Digital transformation in the maritime industry, including IoT, AI, and Blockchain, is revolutionizing cargo handling operations. Real-time cargo positioning data, vessel deployment, and port call optimization facilitate more effective and sustainable shipping operations. Empty back-haul trips are minimized through efficient trade agreements and multimodal transportation. Sustainable energy sources are being integrated into shipping operations to reduce carbon emissions and promote eco-friendly maritime transport. The stevedoring market caters to various cargo types, including general cargo, bulk cargo (dry and liquid), neo-bulk, and specialized cargo, necessitating versatile handling capabilities. Vessel chartering, crew management, and infrastructure investment are other key areas where stevedoring companies contribute to the overall efficiency of the maritime supply chain.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Stevedoring and Marine Cargo Handling Market Driver

Growing adoption of containerization is the key driver of the market. The privatization of marine cargo handling has significantly transformed the maritime trade landscape, particularly in the handling of containerized cargo. Containerization has become a dominant mode of waterborne transportation due to its efficiency in packing and transporting a diverse range of goods, from manufactured products and raw materials to consumer goods. This trend has driven the demand for stevedoring services, which optimize cargo handling operations at marine ports. Container handling equipment, such as container cranes, reach stackers, and straddle carriers, have automated and streamlined the process, reducing the need for manual labor and enhancing space utilization. The growth of online commerce and e-retail has further fueled the demand for efficient and secure cargo handling, as retail sales shift towards digital platforms.

Moreover, the adoption of automation and advanced technologies, including electric forklift trucks and automated guided vehicles, has improved fuel efficiency and reduced emissions, aligning with emission norms and the electric market's growing importance. The maritime logistics industry is also adapting to macroeconomic headwinds, such as inflation and retail market trends, by focusing on low-cost transportation and secure transportation solutions. In addition to containerized cargo, the stevedoring and cargo handling market caters to various other cargo types, including gas shipping, dry bulk shipping, and crude oil shipments. Air cargo movement is another critical component of the logistics industry, and the adoption of automation and advanced technologies is transforming this sector as well.

Stevedoring and Marine Cargo Handling Market Trends

The emergence of smart ports and IoT integration in stevedoring and marine cargo handling is the upcoming trend in the market. The maritime industry, specifically marine cargo handling, has undergone significant transformations with the advent of privatization and automation. The global market for marine cargo handling is driven by various factors, including the growth in waterborne transportation, inflated retail sales due to online commerce, and macroeconomic headwinds such as industrial production and retail market trends. Seaborne trade volume has witnessed a wave in containerized cargo, gas shipping, and crude oil shipments. Automated technology, such as IoT devices and sensors, plays a crucial role in enhancing the efficiency of cargo handling operations. Smart ports integrate IoT technology into cargo handling equipment, terminals, and infrastructure to collect real-time data on container movements, equipment status, weather conditions, and environmental parameters. This data enables seamless connectivity and data exchange between different systems and stakeholders, leading to optimized resource allocation and improved operational efficiency.

Moreover, the increasing popularity of e-commerce and the need for low-cost and secure transportation have led to the adoption of electric and automated cargo handling equipment, such as forklift trucks. Fuel efficiency and emission norms are also major considerations in the marine cargo handling market. The electric market is expected to grow significantly due to the shift towards cleaner propulsion types. Air cargo movement also plays a vital role in the logistics industry, and the integration of IoT technology in air cargo handling has led to improved efficiency and productivity. The future of marine and land cargo handling lies in the adoption of novel technologies, such as automation, data analytics, and predictive modeling, to optimize resource allocation and enhance productivity.

Stevedoring and Marine Cargo Handling Market Challenge

Congestion issues in ports and terminals is a key challenge affecting the market growth. The privatization of marine cargo handling has significantly transformed the maritime industry, particularly in the realm of waterborne transportation. With the tide in maritime trade, driven by factors such as inflation, retail sales, e-commerce, and industrial production, the volume of containerized cargo, gas shipping, dry bulk shipping, and crude oil shipments has escalated. This growth has led to an increased demand for efficient cargo handling, including cargo stacking and automation. Automated technology, such as online commerce and automated cargo handling equipment, has become essential in addressing the challenges posed by the influx of cargo. Forklift trucks, powered by diesel and electric, play a crucial role in the handling process.

However, the increasing focus on fuel efficiency and emission norms has led to the adoption of electric and alternative propulsion types. Moreover, the integration of novel technologies, like automation and e-commerce, has revolutionized the logistics landscape. Seaborne trade volume continues to grow, and air cargo movement remains a critical component of the global supply chain. Despite these advancements, macroeconomic headwinds, such as inflation and retail market trends, pose challenges to the industry. The need for secure transportation, low-cost solutions, and adherence to emission norms remains a priority for stakeholders.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- APS Stevedoring LLC - The company provides specialized stevedoring and marine cargo handling services for various types of cargoes, including automobiles, general merchandise, and breakbulk goods.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- APS Stevedoring LLC

- Blue Water Shipping AS

- Bothra Group

- Carver Companies.

- CHARLESTON STEVEDORING COMPANY LLC

- CJ Logistics Corp.

- CMA CGM SA Group

- Crowley Maritime Corp.

- Deutsche Post AG

- Enstructure

- Hapag Lloyd AG

- Japan Transcity Corp.

- Jones Stevedoring

- King Ocean Services Ltd.

- Newcastle Stevedores

- Orissa Stevedores Ltd.

- Richardson Companies

- Shannon Foynes Port

- Texas Stevedoring Services LLC

- The Cooper Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the privatization of marine ports and the increasing volume of containerized cargo in waterborne transportation. The automation of cargo handling processes, including cargo stacking and the use of automated technology, is also driving market growth. Online commerce and retail sales are major contributors to the maritime trade of containerized cargo, particularly in e-commerce. Macroeconomic headwinds such as inflation and retail market trends are influencing the demand for low-cost transportation and secure transportation of various commodities, including dry bulk shipping, gas shipping, and crude oil shipments.

Further, cargo handling equipment, such as forklift trucks, is becoming increasingly important in the efficient handling of cargo, with a shift towards fuel efficiency and emission norms. The electric market is gaining traction in the propulsion type of marine cargo, land cargo, and air cargo. Novel technologies, including automation and electrification, are expected to revolutionize the cargo handling industry in the coming years.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.45% |

|

Market Growth 2024-2028 |

USD 2.66 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.15 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 42% |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

APS Stevedoring LLC, Blue Water Shipping AS, Bothra Group, Carver Companies., CHARLESTON STEVEDORING COMPANY LLC, CJ Logistics Corp., CMA CGM SA Group, Crowley Maritime Corp., Deutsche Post AG, Enstructure, Hapag Lloyd AG, Japan Transcity Corp., Jones Stevedoring, King Ocean Services Ltd., Newcastle Stevedores, Orissa Stevedores Ltd., Richardson Companies, Shannon Foynes Port, Texas Stevedoring Services LLC, and The Cooper Group |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -