Subscriber Data Management Market Size 2024-2028

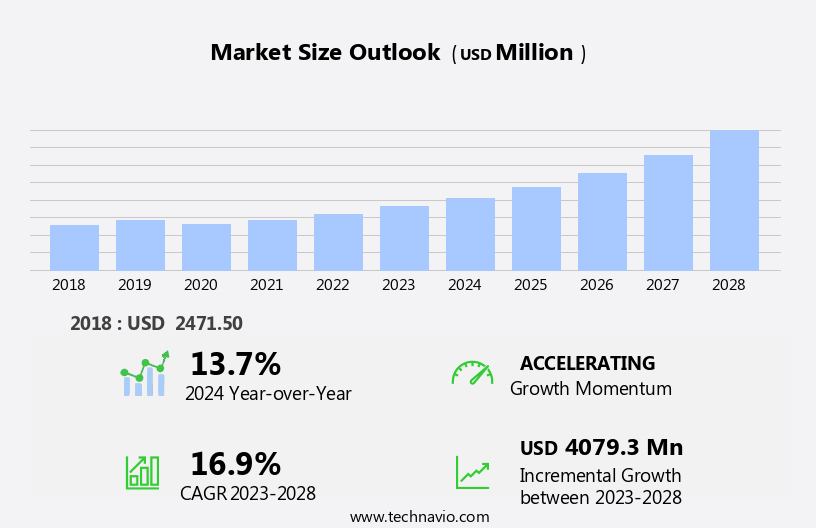

The subscriber data management market size is forecast to increase by USD 4.08 billion at a CAGR of 16.9% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing adoption of target advertisement-based streaming apps. This trend is driven by the rising demand for personalized content and services, which necessitates effective management of subscriber data. Furthermore, the proliferation of 5G technology is fueling the need for faster and more secure data processing and transmission. However, this market is not without challenges. Data privacy and security risks continue to pose a significant threat, with subscriber data being a valuable asset for cybercriminals. Companies must invest in security measures to protect sensitive information and maintain customer trust. Additionally, regulatory compliance and data interoperability across multiple platforms are other challenges that market participants must navigate to capitalize on the opportunities presented by this dynamic market.

- Overall, the market offers significant potential for growth, particularly for those players who can effectively address the evolving needs of subscribers and mitigate the risks associated with managing large volumes of sensitive data.

What will be the Size of the Subscriber Data Management Market during the forecast period?

- The market in the US is experiencing significant growth due to the increasing number of mobile subscriptions and the shift towards cloud-based solutions. Telecom operators are prioritizing network functions virtualization (NFV) and long-term evolution (LTE) technologies to enhance their mobile networks, leading to an escalating demand for user data repositories and policy management systems. Telecommunication network providers are also focusing on data security to mitigate cyberattacks and ensure data privacy policies are adhered to. Moreover, the proliferation of Voice over LTE (VoLTE) and Volte services, as well as the integration of subscriber data management systems in telecom service providers' customer relationship management (CRM) and identity management solutions, is driving market expansion.

- The market is expected to continue growing as 5G subscriptions increase, with hybrid solutions gaining popularity among network carriers to optimize their on-premise and cloud-based offerings. The market's size and direction reflect the industry's commitment to delivering secure, efficient, and innovative subscriber data management solutions to meet the evolving needs of mobile subscribers.

How is this Subscriber Data Management Industry segmented?

The subscriber data management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Mobile networks

- Fixed networks

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Middle East and Africa

- South America

- North America

By Type Insights

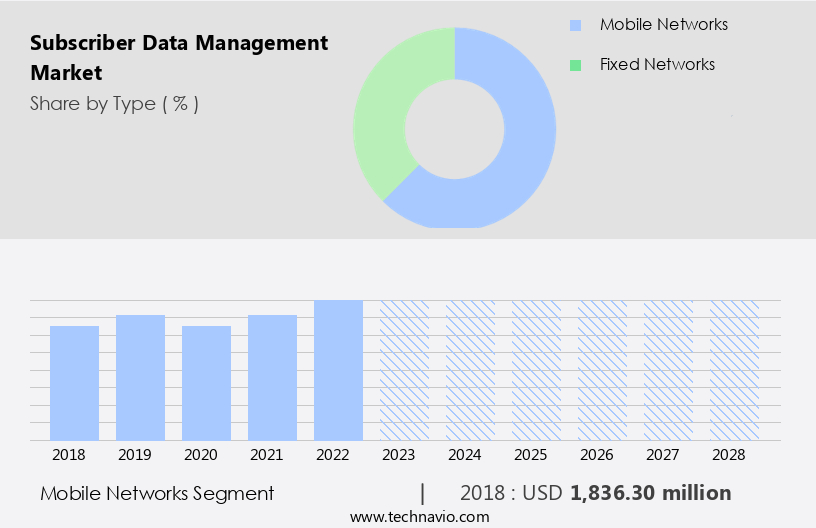

The mobile networks segment is estimated to witness significant growth during the forecast period.

The Subscriber Data Management (SDM) market is driven by the mobile networks segment, which accounts for a substantial revenue share. This growth is attributed to the widespread use of mobile devices and the escalating demand for high-speed data services, particularly with the emergence of 5G technology. Mobile networks necessitate advanced SDM solutions to manage the voluminous subscriber data, ensuring uninterrupted service delivery and superior user experiences. The integration of 5G has intensified the need for sophisticated SDM systems due to the complexities introduced in data management, including real-time processing, authentication, and security. Cloud-based SDM solutions with cloud-native design are increasingly popular due to their flexibility, scalability, and ability to handle large volumes of data.

Identity management, data integration, and policy management are crucial components of these solutions. The Internet of Things (IoT) and Voice Over IP (VoIP) are additional areas driving the market, as they generate substantial subscriber data that needs to be managed effectively. Data security and privacy are paramount concerns, necessitating the adoption of advanced security solutions and adherence to stringent data privacy policies. Network Carriers, Telecom Operators, and Communication Service Providers (CSPs) are key players in the market, leveraging SDM systems to manage their subscriber data and enhance network performance. Network Functions Virtualization (NFV) and Long-Term Evolution (LTE) are key technologies enabling the deployment of SDM solutions in a hybrid environment, ensuring seamless integration with fixed networks and mobile networks.

The market is further fueled by the increasing penetration of smartphones and smart TVs, urban telephone subscriptions, and the growing number of mobile users. Network congestion analysis and cyberattacks are challenges that the market must address to ensure optimal network performance and data security.

Get a glance at the market report of share of various segments Request Free Sample

The Mobile networks segment was valued at USD 1.84 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

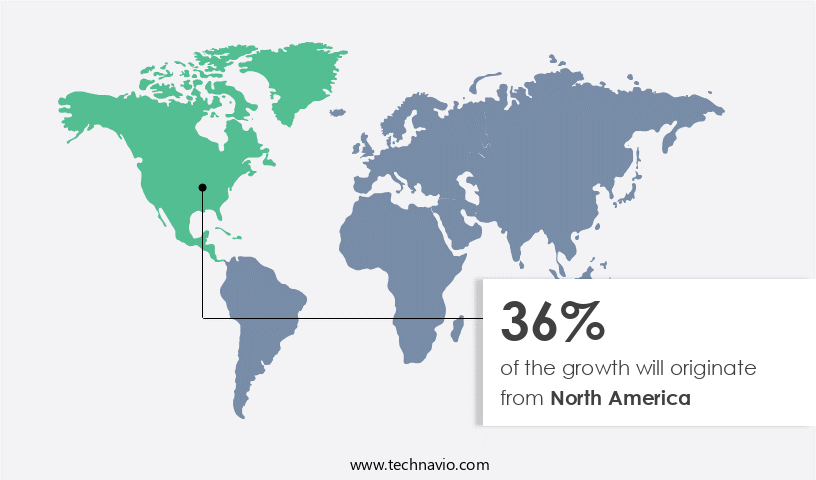

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The Subscriber Data Management (SDM) market in North America is experiencing significant growth due to the increasing digital transformation across various industries, including retail, BFSI, healthcare, and public sector. This digital shift is leading to an exponential increase in data generation, necessitating advanced data management solutions. Cloud-based SDM solutions with cloud-native design are gaining popularity among large enterprises and telecom operators for their scalability, flexibility, and cost-effectiveness. The Internet of Things (IoT) and Voice Over IP (VoIP) are also driving the demand for SDM systems, as mobile subscriptions and smartphone penetration continue to rise. Telecommunications providers and network carriers are investing in Policy Management, Network Functions Virtualization (NFV), and Long-Term Evolution (LTE) to manage the increasing network congestion and cyberattacks.

Small-medium enterprises (SMEs) are also adopting SDM systems to manage their customer information more effectively. The adoption of 5G Technology and the integration of data from various sources, including Smart TVs and home subscriber servers, require data architecture and security solutions for data privacy and security. The market is further by the deployment of SDM systems in the cloud for real-time access, data backup, and integration with other systems. Data storage and management systems are essential for telecom service providers to manage their vast amounts of data generated from fixed networks and mobile networks.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Subscriber Data Management Industry?

- Growing adoption of target advertisement-based streaming apps is the key driver of the market.

- Subscriber data management is a crucial aspect for companies in the media and entertainment industry, particularly those relying on advertisement-based revenue models or streaming applications. The importance of managing subscriber data effectively lies in the potential for increased subscriber numbers, which in turn leads to higher revenue. Innovative offers, such as attractive discounts for new subscribers and bundling services across various platforms, have proven effective in attracting and retaining customers. In late 2022, notable players in the market, like Netflix and Disney+, introduced ad-supported tiers, leading to a significant in subscribers. By the first quarter of 2023, the number of ad-supported subscriptions grew by 24.6% year-over-year, reaching 55.2 million.

- These trends are anticipated to fuel the demand for subscriber data management solutions during the forecast period. companies must leverage advanced data analytics tools and techniques to gain valuable insights from subscriber data, enabling them to tailor their offerings and improve customer engagement.

What are the market trends shaping the Subscriber Data Management Industry?

- Increasing subscriber demand for 5G is the upcoming market trend.

- The market is poised for significant growth due to the increasing adoption of advanced mobile technologies, such as 5G. With the widespread availability of 5G devices from various companies and their increasingly affordable prices, the number of 5G subscriptions is projected to increase at a rapid pace. By the end of 2027, it is estimated that over 4.4 billion people worldwide will have 5G subscriptions, accounting for nearly half of all mobile subscriptions. As 5G becomes the dominant mobile access technology, it will drive the growth of the market.

- This trend is attributed to the need for efficient management of the vast amounts of data generated by 5G networks and subscribers. The increasing demand for seamless and personalized digital experiences, coupled with the importance of data security and privacy, further boosts the market's growth prospects.

What challenges does the Subscriber Data Management Industry face during its growth?

- Data privacy and security risk is a key challenge affecting the industry growth.

- The market faces a significant challenge with data privacy concerns in conversational AI, particularly chatbots and value-added services (VAS). Enterprises worldwide are adopting these technologies to streamline business processes, but the increasing incidence of cybercrimes raises security issues. Despite these concerns, customers prioritize convenience and cost-benefit analysis over other aspects. During interactions with chatbots or VAS, customers share various types of information.

- Ensuring data privacy and security in these interactions is crucial for maintaining customer trust and adhering to regulatory requirements. The global market for subscriber data management is expected to grow as enterprises continue to adopt conversational AI technologies, but addressing data privacy concerns will be essential for market expansion.

Exclusive Customer Landscape

The subscriber data management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the subscriber data management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, subscriber data management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALE International - The company provides a unified subscriber data management solution, accommodating 4G and 5G subscriptions, streamlining network upgrades. This platform facilitates collaboration with third-party service providers and introduces advanced services, including 5G slicing and enterprise IoT.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALE International

- Alepo

- Cisco Systems Inc.

- Enea AB

- Enea Openwave

- Extreme Networks Inc.

- Hewlett Packard Enterprise Co.

- HMD Global Oy

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- MSI Data LLC

- NetNumber Inc.

- Optiva Inc.

- Oracle Corp.

- R Systems Inc.

- Sandvine Corp.

- Sonic Foundry Inc.

- Telefonaktiebolaget LM Ericsson

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of solutions designed to help telecommunications providers effectively manage and secure the vast amounts of data generated by their mobile and fixed network subscribers. With the proliferation of cloud-based technologies and the increasing adoption of cloud-native designs, these solutions are increasingly being deployed in the cloud to enable real-time access, data integration, and backup. Identity management is a critical component of subscriber data management, as it involves the secure storage and management of user data, including authentication and access control. This is particularly important in the era of the Internet of Things (IoT), where an ever-growing number of connected devices require secure management.

Data security is another key concern in the market. With the increasing threat of cyberattacks, telecom operators must implement security solutions to protect their networks and subscribers' data. This includes implementing data privacy policies and ensuring compliance with various regulations. Policy management is also an essential aspect of subscriber data management. Telecommunications providers must be able to manage and enforce policies related to network congestion analysis, data usage, and other factors to ensure a positive user experience and optimize network performance. The adoption of cloud deployment models, such as Network Functions Virtualization (NFV) and Software-Defined Networking (SDN), is driving innovation in the market.

These technologies enable telecom operators to more effectively manage their networks and subscribers, while also reducing costs and improving agility. The market for subscriber data management solutions is diverse, with offerings catering to both large enterprises and Small-Medium Enterprises (SMEs). Telecommunications providers must be able to offer flexible, scalable solutions that can meet the unique needs of different customer segments. The penetration of smartphones and other mobile devices continues to drive growth in the market. Mobile subscribers require solutions that can manage their data across multiple devices and networks, including Voice over IP (VoIP) and Long-Term Evolution (LTE) networks.

The adoption of 5G technology is also set to have a significant impact on the market. With its increased speeds and low latency, 5G will enable new use cases and applications that will require advanced data management capabilities. In , the market is a dynamic and evolving landscape, driven by the increasing adoption of cloud technologies, the growing number of connected devices, and the need for security and policy management solutions. Telecommunications providers must be able to offer flexible, scalable, and secure solutions to meet the unique needs of their subscribers and stay competitive in an increasingly crowded market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.9% |

|

Market growth 2024-2028 |

USD 4079.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.7 |

|

Key countries |

US, Germany, China, UK, Japan, France, India, Canada, Mexico, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Subscriber Data Management Market Research and Growth Report?

- CAGR of the Subscriber Data Management industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the subscriber data management market growth of industry companies

We can help! Our analysts can customize this subscriber data management market research report to meet your requirements.

RIA -

RIA -