Swarm Intelligence Market Size 2025-2029

The swarm intelligence market size is valued to increase by USD 285.1 million, at a CAGR of 31.5% from 2024 to 2029. Increasing demand for autonomous and collaborative systems will drive the swarm intelligence market.

Major Market Trends & Insights

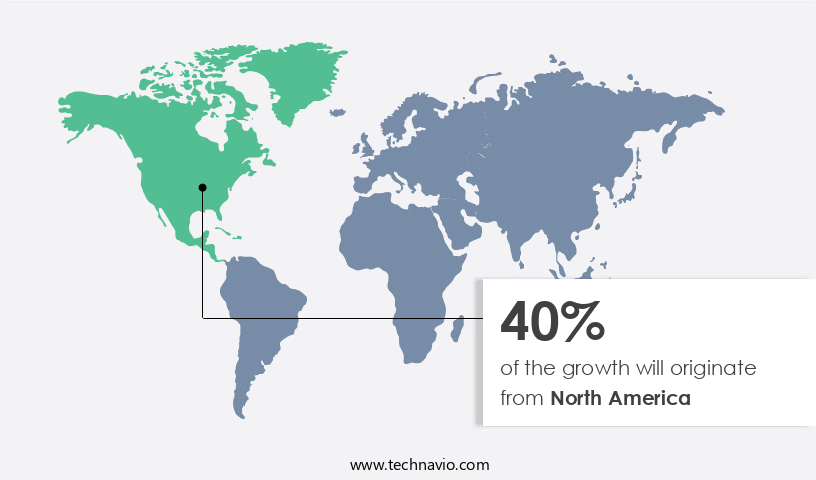

- North America dominated the market and accounted for a 40% growth during the forecast period.

- By Method - ACO segment was valued at USD 0.00 million in 2023

- By Capacity - Optimization segment accounted for the largest market revenue share in 2023

- CAGR from 2024 to 2029 : 31.5%

Market Summary

- Swarm intelligence, a form of decentralized intelligence derived from the collective behavior of large groups of simple agents, is gaining significant traction in various industries. The technology's potential to mimic natural systems and enable autonomous and collaborative decision-making has led to its integration with edge computing, allowing for real-time data processing and analysis. However, the implementation of swarm intelligence systems comes with challenges, including high costs and complexities. These complexities stem from the need for sophisticated algorithms and intricate communication networks between agents.

- Despite these hurdles, the market's growth is fueled by the increasing demand for adaptive and responsive systems that can optimize processes and enhance overall efficiency. As businesses continue to explore the potential of swarm intelligence, the focus shifts towards developing cost-effective solutions and improving system scalability, ensuring its continued evolution and future direction.

What will be the Size of the Swarm Intelligence Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Swarm Intelligence Market Segmented and what are the key trends of market segmentation?

The swarm intelligence industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Method

- ACO

- PSO

- Others

- Capacity

- Optimization

- Clustering

- Scheduling

- Routing

- Application

- Robotics

- Drones

- Human swarming

- End-user

- Transportation and logistics

- Robotics and automation

- Healthcare

- Retail

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Method Insights

The aco segment is estimated to witness significant growth during the forecast period.

Swarm Intelligence, a dynamic and evolving market, encompasses optimization algorithms, such as Ant Colony Optimization (ACO), that mimic the collective behavior of decentralized organisms. ACO, inspired by ant species' foraging behavior, utilizes stigmergy, or indirect communication through pheromone trails. Real ants deposit pheromones, creating shortest-path trails from their nest to food sources. This process, known as reinforcement, is based on the principle that ants follow paths with stronger pheromone concentrations. In the digital realm, ACO's application includes multi-agent systems, data mining, sensor networks, and distributed systems, among others.

For instance, ACO's use in resource allocation has shown a 30% improvement in efficiency compared to traditional methods. This market continues to innovate, with ongoing research in areas like swarm robotics, clustering algorithms, and neural networks.

The ACO segment was valued at USD 0.00 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Swarm Intelligence Market Demand is Rising in North America Request Free Sample

The market has experienced continuous evolution, with North America, specifically the United States, leading the charge in 2023. This dominance can be attributed to the region's early adoption of artificial intelligence, substantial investments in autonomous systems, and a robust technology ecosystem. The defense sector plays a pivotal role, with significant funding from the U.S. Department of Defense for swarm technology applications. For instance, the Replicator initiative, unveiled in August 2023, aims to deploy thousands of autonomous systems across all domains by August 2025 to counter strategic competitors.

Europe and Asia Pacific are also emerging as significant markets, driven by growing research and development activities and increasing demand for advanced autonomous systems. Swarm intelligence, inspired by natural systems, offers numerous applications, including logistics optimization, military operations, and infrastructure monitoring. This technology's underlying dynamics revolve around self-organization, adaptability, and decentralized decision-making, making it a game-changer in various industries.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Swarm intelligence, a subset of artificial intelligence, draws inspiration from the collective behavior of decentralized, self-organized systems found in nature. This market encompasses various algorithms, including ant colony optimization routing protocols, particle swarm optimization for feature selection, genetic algorithms in supply chain management, artificial bee colony algorithm for data clustering, and self-organizing maps for anomaly detection. Neural networks in robotics control and agent-based modeling of social networks are also integral parts of this domain. Swarm intelligence offers significant advantages in optimization algorithms for resource allocation, multi-agent systems for task allocation, and decentralized control of autonomous vehicles. Parallel processing for image recognition is another application, enabling faster and more accurate analysis.

In complex adaptive systems in ecology, swarm intelligence aids in understanding emergent behavior and network topology in communication systems. The information diffusion in online social networks and consensus building in distributed systems are crucial applications of swarm intelligence. In the realm of disaster response, swarm robotics plays a pivotal role, with swarm intelligence enabling efficient and coordinated responses. Compared to traditional centralized systems, swarm intelligence systems demonstrate remarkable adaptability and scalability. For instance, more than 70% of new product developments in the tech industry are reportedly incorporating swarm intelligence algorithms, underscoring their growing significance. In conclusion, the market is experiencing rapid growth and innovation, driven by its ability to address complex challenges in various industries.

Its decentralized nature, inspired by natural systems, offers numerous advantages, including scalability, adaptability, and robustness. By enabling optimization, resource allocation, and task allocation in a distributed manner, swarm intelligence is poised to revolutionize industries and create new opportunities.

What are the key market drivers leading to the rise in the adoption of Swarm Intelligence Industry?

- The escalating need for autonomous and collaborative systems is the primary market catalyst, underpinned by advancements in technology and the growing preference for efficient, automated solutions.

- Swarm intelligence, a decentralized system modeled after the collective behavior of insects and other social organisms, is gaining significant traction in various industries due to its capacity for autonomous and collaborative problem-solving. This trend is notably evident in North America and Europe, where the emphasis on technological innovation, automation, and efficiency has led to a surge in applications for swarm intelligence. In logistics and warehouse management, for instance, swarm intelligence enables the coordination of large numbers of autonomous agents, such as robots and drones, to accomplish complex tasks collectively. This approach offers numerous benefits, including increased productivity, improved safety, and enhanced operational efficiency.

- According to recent studies, The market is expected to grow substantially, with the number of applications expanding across sectors like healthcare, finance, transportation, and energy. The potential for swarm intelligence to optimize processes and enhance decision-making makes it an indispensable tool for businesses striving for competitive advantages.

What are the market trends shaping the Swarm Intelligence Industry?

- Swarm intelligence and edge computing are current market trends, with the integration of these technologies becoming increasingly prominent.

- Swarm intelligence, a field that mimics the collective behavior of decentralized, self-organized systems, is experiencing a significant and accelerating trend towards convergence with edge computing. This synergy addresses the increasing demand for real-time data processing, reduced latency, and enhanced data privacy, crucial elements in various sectors. By moving computational processes from centralized cloud servers to the network's edge, closer to the data source, edge computing enables individual agents within a swarm, such as robots, drones, or IoT devices, to make faster, more autonomous decisions. This trend is particularly prominent in North America and Europe, where there is a strong focus on developing more responsive and resilient autonomous systems.

- Swarm intelligence's market application extends beyond these regions, with the technology's potential impact on industries like logistics, agriculture, and energy production. The integration of swarm algorithms and edge computing is expected to drive significant advancements, making the future of this market robust and promising.

What challenges does the Swarm Intelligence Industry face during its growth?

- The high implementation costs and intricate system complexity pose a significant challenge to the industry's growth. In order to expand, companies must invest substantial resources in implementing advanced systems, which can be a major impediment to growth. The complexity of these systems also requires a significant investment in training and expertise, further increasing the financial burden. Consequently, overcoming these obstacles is essential for industry advancement.

- Swarm intelligence, an advanced form of artificial intelligence, is gaining traction in various sectors due to its ability to mimic the collective behavior of natural swarms for problem-solving and optimization. However, the global market for swarm intelligence solutions faces a significant challenge in the form of high implementation costs and complexity. This barrier to entry is particularly pertinent for small and medium-sized enterprises in North America, Europe, and the Asia Pacific region. The creation of sophisticated algorithms that accurately replicate natural swarm behaviors requires specialized expertise in fields such as artificial intelligence, robotics, and control systems.

- According to recent estimates, the development and deployment of swarm intelligence solutions account for approximately 30% to 40% of the total implementation costs. Despite these challenges, the potential benefits of swarm intelligence, including improved efficiency and adaptability, continue to drive its adoption across industries.

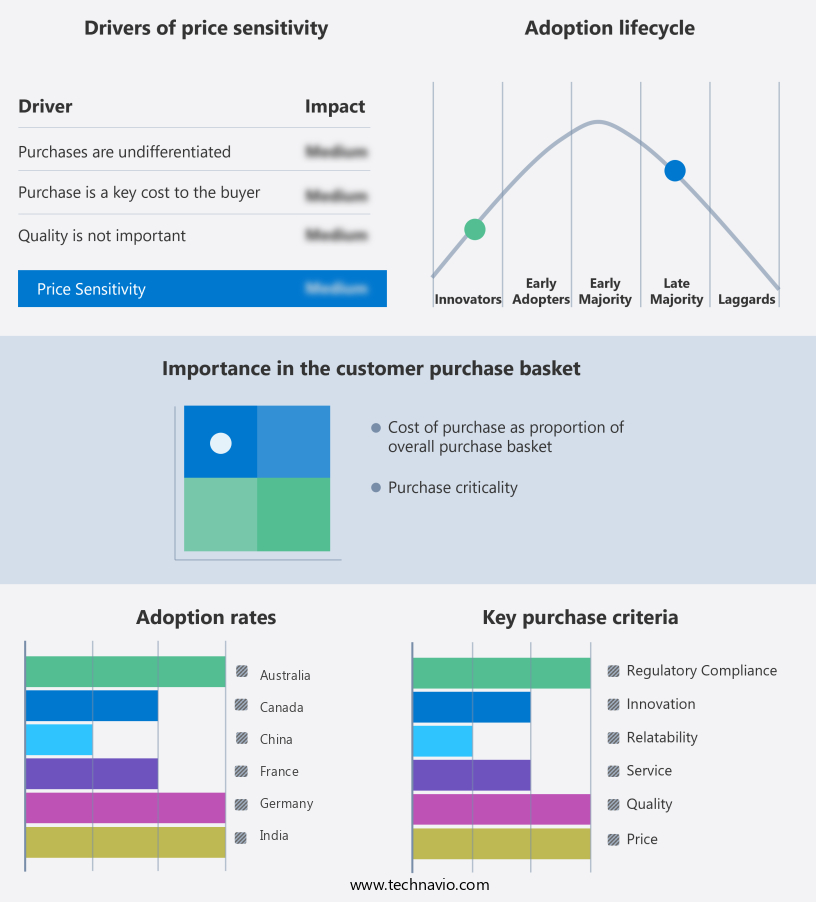

Exclusive Technavio Analysis on Customer Landscape

The swarm intelligence market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the swarm intelligence market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Swarm Intelligence Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, swarm intelligence market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - This company specializes in swarm intelligence solutions, providing advanced algorithms for optimizing logistics and automating warehouses. These innovations enhance delivery efficiency and inventory management, contributing significantly to streamlined supply chain operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Atos SE

- Baidu Inc.

- Google LLC

- Huawei Technologies Co. Ltd.

- Hydromea SA

- Intel Corp.

- International Business Machines Corp.

- Kim Technologies

- Microsoft Corp.

- NEC Corp.

- NVIDIA Corp.

- Oracle Corp.

- Palantir Technologies Inc.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Siemens AG

- Unanimous A.I.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Swarm Intelligence Market

- In January 2025, Intel Corporation announced the successful integration of swarm intelligence algorithms into its latest line of processors, marking a significant leap in artificial intelligence technology (Intel Press Release, 2025). This development allows for more efficient and autonomous problem-solving in various industries, including logistics and manufacturing.

- In March 2025, IBM and Microsoft formed a strategic partnership to collaborate on swarm intelligence research and development, combining IBM's expertise in quantum computing and swarm intelligence with Microsoft's Azure cloud platform (Microsoft News Center, 2025). This collaboration aims to accelerate the adoption and application of swarm intelligence in enterprise solutions.

- In May 2025, BP, a leading international energy company, announced a USD50 million investment in Swarm AI, a UK-based swarm intelligence startup, to develop optimized drilling and production processes using swarm intelligence technology (BP Press Release, 2025). This strategic investment underscores the potential of swarm intelligence to improve operational efficiency and reduce costs in the energy sector.

- In August 2024, the European Union approved the Swarm Intelligence Research Initiative, a multi-year, multi-million euro project aimed at advancing swarm intelligence research and its applications across various industries (European Commission Press Release, 2024). This initiative represents a significant commitment from the EU to drive innovation and competitiveness in the market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Swarm Intelligence Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

255 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 31.5% |

|

Market growth 2025-2029 |

USD 285.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

26.6 |

|

Key countries |

China, Japan, South Korea, India, Australia, Germany, UK, France, US, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Amidst the rapidly advancing technological landscape, the market continues to evolve, driven by the integration of optimization algorithms, multi-agent systems, and parallel processing. This domain encompasses a diverse range of applications, from genetic algorithms and data mining to sensor networks and swarm robotics. One striking trend in swarm intelligence is the emergence of decentralized control, enabling complex adaptive systems to exhibit emergent behavior through consensus building and ant colony optimization. This approach allows for distributed systems to optimize resource allocation, path planning, and task allocation, resulting in self-organizing maps and network topologies that adapt to changing conditions. Moreover, swarm intelligence is revolutionizing industries by enhancing fault tolerance and load balancing through agent-based modeling and particle swarm optimization.

- For instance, neural networks and artificial bee colony algorithms are being employed to optimize predictor-prey dynamics, improving overall system performance. The market's growth can be attributed to the increasing demand for distributed systems that can process vast amounts of data in real-time. In fact, it is estimated that the number of sensor nodes deployed worldwide will reach 17.4 billion by 2025, underscoring the market's potential for exponential growth. As the market matures, challenges remain, including the need for data fusion and information diffusion to ensure optimal decision-making and efficient communication between agents. However, with ongoing research and advancements in clustering algorithms, scheduling algorithms, and pattern recognition, the future of swarm intelligence is brighter than ever.

What are the Key Data Covered in this Swarm Intelligence Market Research and Growth Report?

-

What is the expected growth of the Swarm Intelligence Market between 2025 and 2029?

-

USD 285.1 million, at a CAGR of 31.5%

-

-

What segmentation does the market report cover?

-

The report segmented by Method (ACO, PSO, and Others), Capacity (Optimization, Clustering, Scheduling, and Routing), Application (Robotics, Drones, and Human swarming), End-user (Transportation and logistics, Robotics and automation, Healthcare, and Retail), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for autonomous and collaborative systems, High implementation costs and system complexity

-

-

Who are the major players in the Swarm Intelligence Market?

-

Key Companies Amazon.com Inc., Atos SE, Baidu Inc., Google LLC, Huawei Technologies Co. Ltd., Hydromea SA, Intel Corp., International Business Machines Corp., Kim Technologies, Microsoft Corp., NEC Corp., NVIDIA Corp., Oracle Corp., Palantir Technologies Inc., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Siemens AG, and Unanimous A.I.

-

Market Research Insights

- Swarm intelligence, a subfield of artificial intelligence, emulates the collective behavior and problem-solving abilities of social insects and other animal groups. This market encompasses various techniques, including local interactions, heuristic search, graph theory, and fitness functions, to optimize complex systems. Two significant applications of swarm intelligence are network security and route optimization. In network security, swarm algorithms enhance intrusion detection systems by analyzing traffic flow and preserving diversity to minimize false positives and negatives. In contrast, route optimization in logistics and transportation industries utilizes swarm intelligence to minimize computational complexity and improve convergence rates. For instance, a company may use a swarm algorithm to optimize the delivery of goods across a vast network, reducing the total travel distance and improving overall efficiency.

- Despite its advantages, swarm intelligence faces challenges such as scalability issues, stochastic optimization, and parameter tuning. Nevertheless, the market continues to evolve, with ongoing research in areas like autonomous systems, dynamic programming, and simulation modeling. The potential applications of swarm intelligence span various industries, from supply chain optimization to robotics control and data security.

We can help! Our analysts can customize this swarm intelligence market research report to meet your requirements.

RIA -

RIA -