Thin Client Market Size 2026-2030

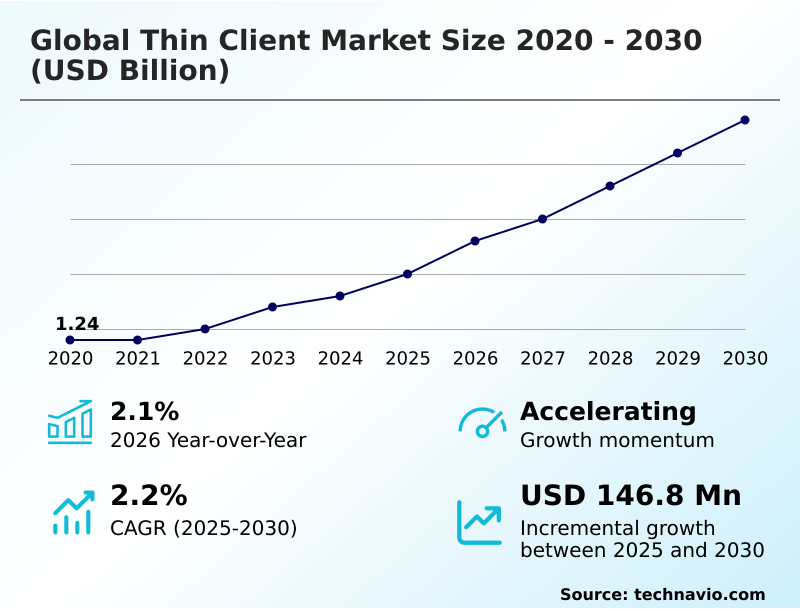

The thin client market size is valued to increase by USD 146.8 million, at a CAGR of 2.2% from 2025 to 2030. Increasing adoption of hybrid and remote work models will drive the thin client market.

Major Market Trends & Insights

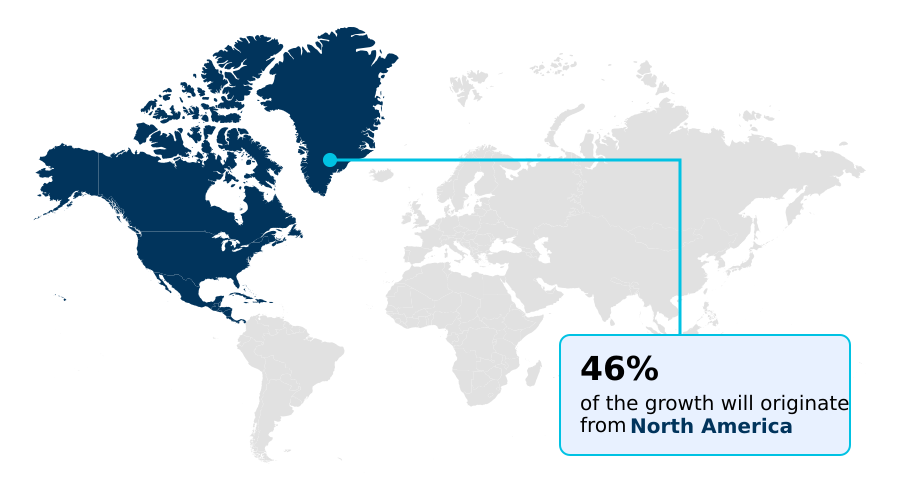

- North America dominated the market and accounted for a 46.1% growth during the forecast period.

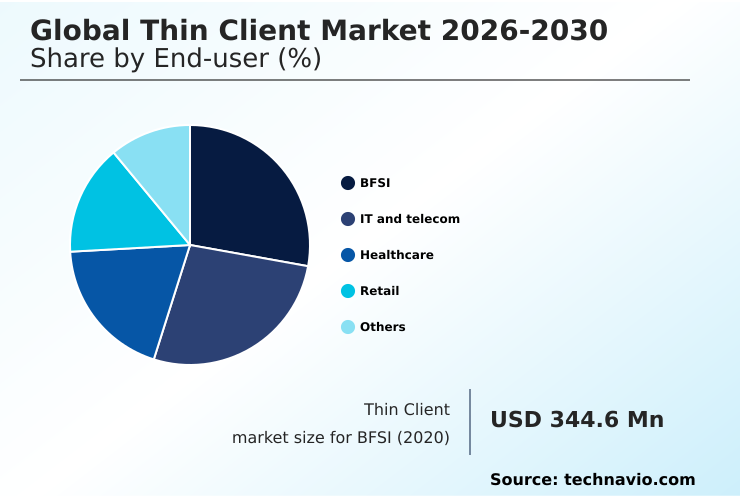

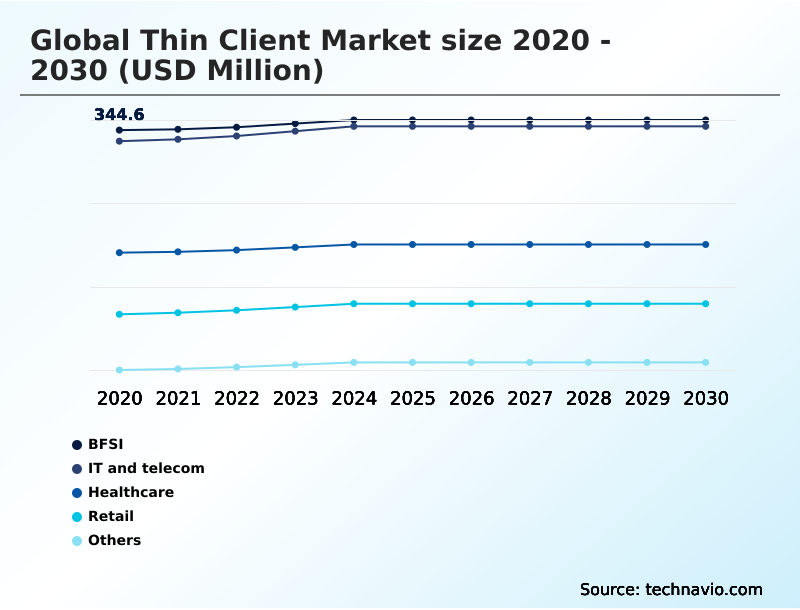

- By End-user - BFSI segment was valued at USD 353.4 million in 2024

- By Form Factor - Standalone segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 206.5 million

- Market Future Opportunities: USD 146.8 million

- CAGR from 2025 to 2030 : 2.2%

Market Summary

- The thin client market is defined by its role in bolstering cybersecurity and enhancing operational efficiency within modern IT infrastructures. The fundamental shift towards centralized computing architectures is driven by the imperative to secure data and streamline management, particularly for distributed workforces.

- Organizations are replacing traditional PCs with endpoint computing devices that rely on a remote server, effectively moving the attack surface away from the user's desk and into a controlled data center.

- This architecture is crucial in industries like finance, where a firm might deploy thin clients on its trading floors to ensure that no sensitive transactional data is stored locally, thereby mitigating risks of data leakage and simplifying regulatory compliance. The adoption of desktop as a service (DaaS) further accelerates this trend, lowering the barrier to entry for virtual desktop infrastructure.

- While the technology offers a lower total cost of ownership through reduced energy consumption and longer hardware lifecycles, its performance is intrinsically tied to network quality.

- The evolution of virtualization protocols and AI-driven management tools continues to address these challenges, broadening the applicability of thin clients from task-based roles to more demanding knowledge worker environments, reinforcing their strategic value in the enterprise.

What will be the Size of the Thin Client Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Thin Client Market Segmented?

The thin client industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- BFSI

- IT and telecom

- Healthcare

- Retail

- Others

- Form factor

- Standalone

- With monitor

- Mobile

- Business model

- Large enterprises

- Small and medium enterprises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

The BFSI sector remains a primary adopter of thin client technology, driven by non-negotiable requirements for data security and stringent regulatory compliance.

Financial institutions leverage virtual desktop infrastructure to protect vast quantities of sensitive customer information, ensuring data privacy and strengthening their overall security posture.

By centralizing data on servers, endpoint computing devices running secure operating systems like thinos significantly reduce the endpoint attack surface, a critical factor for meeting regulations like PCI DSS.

Centralized management software simplifies IT administration, allowing for rapid deployment of security patches.

Features such as encrypted data transmission and support for smart card readers are integral to this secure architecture, with some institutions reporting a 40% reduction in endpoint-related security incidents after implementing a zero trust security model with thin clients.

The BFSI segment was valued at USD 353.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Thin Client Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is diverse, led by North America's mature adoption driven by advanced server based infrastructure and a focus on security.

Europe follows, with strong demand in Germany and the UK, influenced by stringent data privacy regulations and government digitalization projects.

The APAC region presents the highest growth potential, fueled by the expansion of BPO industries in India and government-led digital initiatives in China. These developing markets are often leapfrogging traditional PC deployments in favor of more cost-effective vdi deployment.

In these regions, the adoption of zero client technology is particularly notable in large-scale educational and government projects, with deployments achieving up to a 20% improvement in resource optimization for virtual desktops.

The success of these installations often hinges on effective workload distribution to handle graphics intensive applications, showcasing the global applicability of this technology in creating a modern digital workspace.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic IT decisions increasingly involve a detailed analysis of thin client vs traditional pc security, where the centralized nature of thin clients offers a clear advantage. For organizations enabling a flexible workforce, a thin client for remote work setup provides a secure and manageable solution.

- The rise of cloud computing has made desktop as a service endpoint devices a popular choice, though success hinges on following vdi deployment best practices. This includes leveraging cloud based thin client management platforms for streamlined administration. A common misconception involves performance, but modern approaches to optimizing thin client for graphics are making them viable for more demanding roles.

- The financial argument, often framed as a total cost of ownership thin client vs pc comparison, consistently favors thin clients due to lower energy use and longer lifecycles. This is especially true in specialized fields; for instance, thin client in healthcare data security is critical for HIPAA compliance.

- The concept of a secure endpoint for hybrid workforce is a core market driver. Use cases like a thin client for financial trading floors demonstrate their reliability in high-stakes environments. Many organizations are now implementing zero trust with thin client architectures to further harden their security.

- The resulting thin client energy consumption savings contribute to both fiscal and sustainability goals, with some firms reporting energy cost reductions of over 30% compared to equivalent PC fleets. While managing vdi with proprietary software can create lock-in, the benefits often outweigh the drawbacks. Emerging applications, such as a thin client for industrial iot, are expanding the market's reach.

- As businesses evaluate their endpoint strategy, the DaaS vs VDI endpoint strategy debate continues, with the choice often depending on specific infrastructure and management preferences. Other considerations include upgrading PCs with PC repurposing software, the thin client vs chromebook for education debate, securing endpoints in BFSI sector, and deploying mobile thin client for sales teams, all showcasing the technology's versatility.

What are the key market drivers leading to the rise in the adoption of Thin Client Industry?

- The increasing adoption of hybrid and remote work models serves as a primary driver for the thin client market, creating sustained demand for secure, manageable IT solutions for a distributed workforce.

- The primary driver for market adoption remains the compelling value proposition of enhanced security and improved operational efficiency.

- The adoption of desktop as a service (DaaS) offerings, often based on a subscription based licensing model, has made this technology accessible to a wider range of businesses.

- By deploying a stateless computing device, organizations ensure all processing occurs in a secure data center, not on the endpoint. This architecture, fortified by secure boot processes and a locked down operating system, drastically reduces security vulnerabilities.

- The lower total cost of ownership is a significant factor, with some deployments achieving over 40% savings in energy costs alone.

- Furthermore, the ability to extend the life of existing hardware through pc repurposing offers a cost-effective path to modern endpoint management, supporting multi monitor setups and unified communications through efficient use of the remote desktop protocol.

What are the market trends shaping the Thin Client Industry?

- A prominent market trend is the accelerating adoption of cloud-based thin clients. This shift is driven by organizational needs for scalable, centrally managed endpoints that seamlessly integrate with cloud applications and virtual desktop services.

- The market is increasingly shaped by the trend toward cloud based management and software-defined endpoints. Organizations are leveraging an agile management console to orchestrate deployments across diverse environments, transforming any x86-64 device into a secure, cloud native endpoint.

- This shift is highlighted by the rise of AI-powered security analytics and machine learning algorithms for predictive maintenance, which can reduce endpoint downtime by up to 30%. While some solutions rely on proprietary management software, the industry is moving toward open standards and flexible connection management platforms.

- This focus on software enhances the user experience and supports sustainability goals through green computing. The role of the remote access provider is also evolving, with deep integrations that simplify secure access and management, reducing IT intervention for common issues by 25%.

What challenges does the Thin Client Industry face during its growth?

- A significant challenge impacting market growth is the inherent dependence on stable, high-performance network connectivity for a satisfactory user experience.

- A key challenge is the complete reliance on robust network connectivity and back-end server infrastructure. Any latency or outage directly impacts productivity, making the endpoint device unusable. While advancements in hyperconverged infrastructure have simplified on-premises deployments, the initial investment can be substantial.

- Performance can also be a hurdle, as the central processing units in the data center must handle the load from all users. Ensuring a seamless user experience with features like session roaming requires careful optimization of virtualization protocols. Furthermore, managing application virtualization in complex multi cloud environments presents a challenge for IT teams.

- In response, vendors are developing more resilient thin client operating systems and cyber immunity solutions to function in less-than-ideal network conditions, but the fundamental dependency on a high-performance connection to the virtualpccenter platform remains a significant consideration for deployment.

Exclusive Technavio Analysis on Customer Landscape

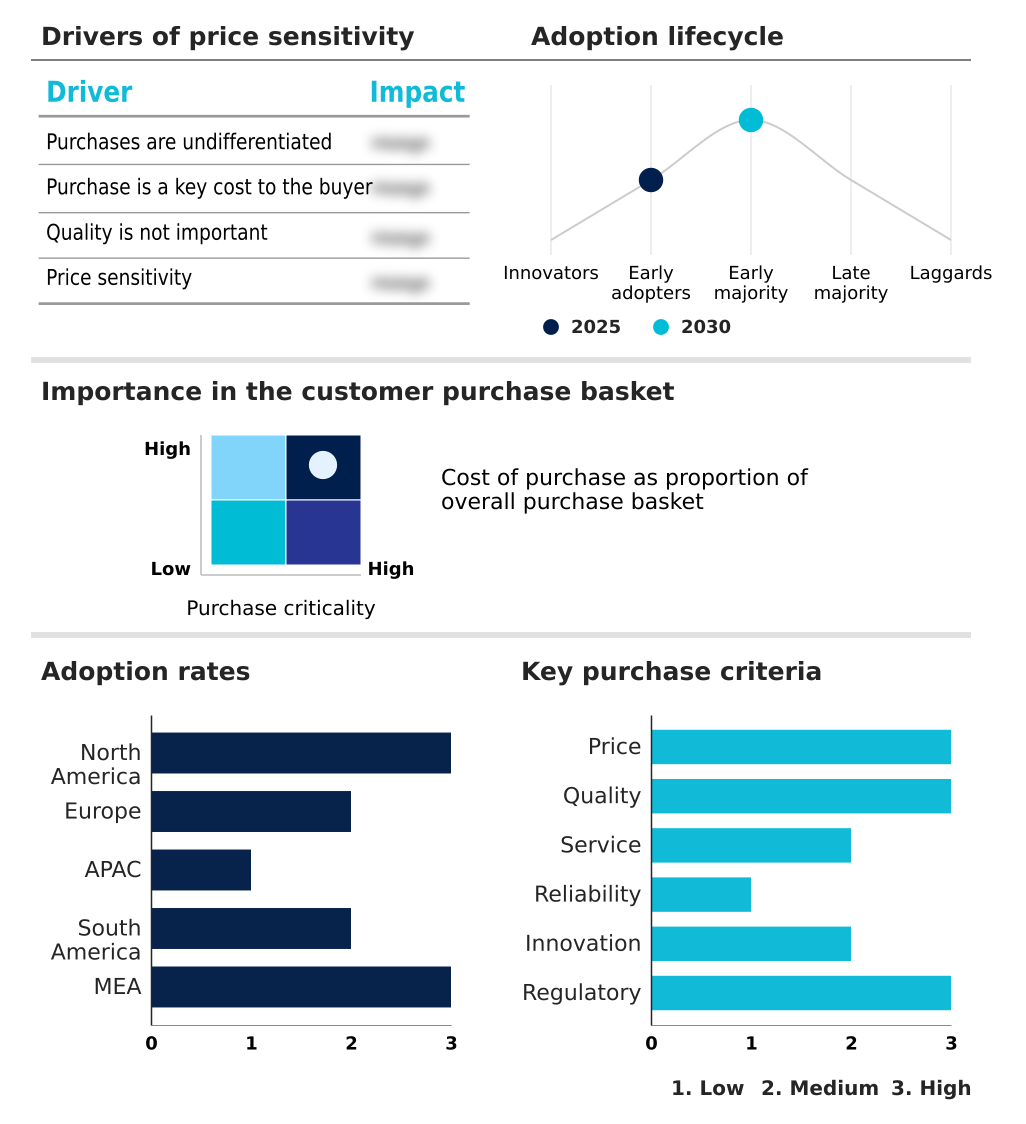

The thin client market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thin client market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Thin Client Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, thin client market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

10ZiG Technology Inc. - Delivering advanced thin client solutions with multi-display support and centralized management software, designed to optimize virtual desktop infrastructure environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 10ZiG Technology Inc.

- Acer Inc.

- Advantech Co. Ltd.

- ASUSTeK Computer Inc.

- Chip PC Technologies

- Cisco Systems Inc.

- Dell Technologies Inc.

- Devon IT

- Fujian Centerm Co. Ltd.

- Fujitsu Ltd.

- HP Inc.

- IGEL

- INP Computer Technology

- Lenovo Group Ltd.

- LG Electronics Inc.

- Ncomputing Co. Ltd.

- NEC Corp.

- Samsung Electronics Co. Ltd.

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Thin client market

- In September 2024, Dell Technologies announced its next-generation Wyse thin clients, featuring an AI-powered security suite and native optimization for multi-cloud VDI environments.

- In November 2024, IGEL and Amazon Web Services revealed a deepened strategic partnership to deliver a fully integrated solution for Amazon WorkSpaces, enhancing the IGEL OS for seamless cloud-native endpoint management.

- In February 2025, HP Inc. acquired a leading PC repurposing software company to expand its HP Wolf Security portfolio, strengthening its ability to convert existing hardware into secure, managed endpoints.

- In May 2025, Lenovo Group Ltd. launched a new line of mobile thin clients specifically designed for manufacturing and logistics, featuring ruggedized chassis and enhanced support for industrial IoT protocols.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Thin Client Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.2% |

| Market growth 2026-2030 | USD 146.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.1% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The thin client market continues its evolution, driven by the enterprise-wide adoption of virtual desktop infrastructure and desktop as a service models. This transition is fundamentally about centralizing control and minimizing risk at the network edge. Organizations are deploying endpoint computing devices, including those utilizing zero client technology, to create a secure, server based infrastructure.

- These stateless computing devices connect to a remote server or data center, ensuring that all data and applications remain firewalled. The core technology stack includes specialized thin client operating systems like thinpro os or thinos and robust centralized management software.

- Modern devices incorporate secure boot processes and encrypted data transmission as standard, running a locked down operating system to mitigate threats. Companies report that such endpoint security measures can reduce device provisioning times by as much as 75%. Innovations like cyber immunity solutions and next gen edge os are further hardening these systems.

- The ability to perform a hardware refresh with minimal disruption, coupled with an agile management console and pc repurposing options, underscores the technology’s strategic value in today's IT landscape.

What are the Key Data Covered in this Thin Client Market Research and Growth Report?

-

What is the expected growth of the Thin Client Market between 2026 and 2030?

-

USD 146.8 million, at a CAGR of 2.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, IT and telecom, Healthcare, Retail, and Others), Form Factor (Standalone, With monitor, and Mobile), Business Model (Large enterprises, and Small and medium enterprises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of hybrid and remote work models, Dependence on network connectivity

-

-

Who are the major players in the Thin Client Market?

-

10ZiG Technology Inc., Acer Inc., Advantech Co. Ltd., ASUSTeK Computer Inc., Chip PC Technologies, Cisco Systems Inc., Dell Technologies Inc., Devon IT, Fujian Centerm Co. Ltd., Fujitsu Ltd., HP Inc., IGEL, INP Computer Technology, Lenovo Group Ltd., LG Electronics Inc., Ncomputing Co. Ltd., NEC Corp., Samsung Electronics Co. Ltd. and Siemens AG

-

Market Research Insights

- The market is characterized by a strategic shift toward architectures that prioritize a robust security posture and enhanced operational efficiency. Organizations are achieving significant gains; for instance, the adoption of virtual desktops accessed via secure endpoint devices has been shown to reduce IT administration overhead by up to 40%.

- This is driven by the need to manage a distributed workforce while maintaining stringent regulatory compliance. The focus on total cost of ownership remains critical, with deployments demonstrating a 25% lower energy consumption compared to traditional PCs. As businesses migrate to multi-cloud environments, the demand for endpoints that support diverse virtualization protocols and deliver a superior user experience is paramount.

- This transition is not just about cost savings but is a fundamental re-evaluation of the digital workspace to ensure data privacy and business continuity.

We can help! Our analysts can customize this thin client market research report to meet your requirements.

RIA -

RIA -