Tissue Engineering And Regeneration Market Size 2024-2028

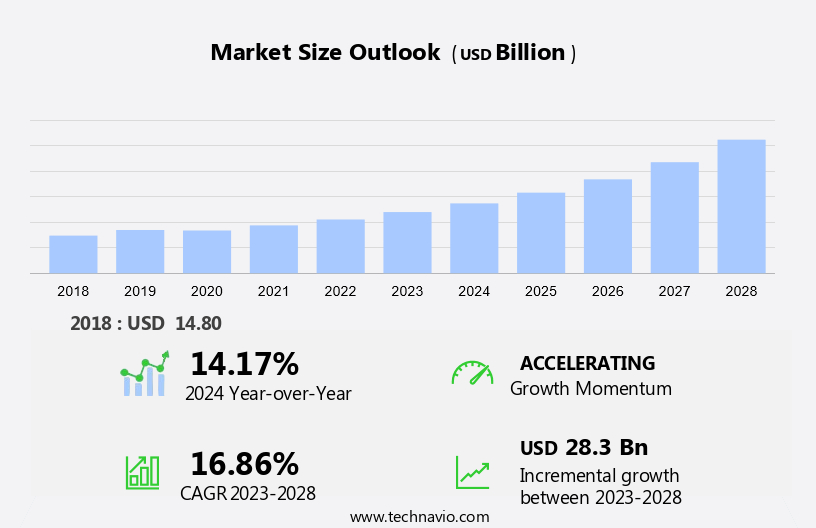

The tissue engineering and regeneration market size is forecast to increase by USD 28.3 billion at a CAGR of 16.86% between 2023 and 2028. The market is experiencing significant growth due to the increasing prevalence of chronic diseases such as orthopedic disorders, musculoskeletal disorders, dental disorders, cardiovascular diseases, and dermatology conditions, including diabetes. Technological advances, including the use of scaffolds in tissue grafting and stem cell research, are driving innovation in tissue engineering solutions. This technology enables the creation of complex tissue structures using living cells and biomaterials. However, uncertain regulatory approval processes pose a challenge to market growth. Regulatory authorities are closely monitoring the development and application of gene editing techniques in tissue engineering and regeneration products to ensure safety and efficacy. The market is expected to continue expanding as these challenges are addressed, providing opportunities for companies to offer innovative solutions in this field. The application of advanced technologies, such as 3D bioprinting, stem cell research, and gene editing techniques, further enhances the potential of tissue engineering to revolutionize the healthcare industry.

The market is witnessing significant advancements in the realm of life sciences, focusing on the development of biological replacements for various organs and tissues. This market encompasses the use of scaffolds, cells, and biomolecules to stimulate the growth and regeneration of living tissues. The application of tissue engineering is vast and spans across multiple domains, including chronic diseases, trauma crises, and degenerative conditions. Chronic diseases such as cardiovascular diseases and diabetes are major areas of focus, as tissue engineering solutions offer potential alternatives to organ transplantation techniques. Trauma crises, including road accidents and traumatic brain injury, can also benefit from these advancements, as tissue engineering can help restore damaged tissues and organs.

Moreover, three-dimensional (3D) bioprinting is a cutting-edge technology that plays a crucial role in the market. It holds immense potential for the development of regenerative medicines, particularly for conditions such as spinal cord injury and orthopedic disorders. The field of tissue engineering is not limited to the creation of complex organs. It also extends to the realm of dermatology and wound care, where it offers innovative solutions for the treatment of chronic wounds and skin disorders. The use of stem cell research and gene editing techniques further enhances the capabilities of tissue engineering.

Furthermore, these technologies enable the manipulation of cells at a genetic level, opening up new possibilities for the creation of customized tissue replacements. The market is poised for growth, driven by the increasing prevalence of chronic diseases and trauma crises. The potential to develop effective solutions for these conditions using tissue engineering techniques is a significant draw for investors and researchers alike. In conclusion, the market represents a dynamic and innovative field in the life sciences sector. It offers promising solutions for the treatment of various conditions, including cardiovascular diseases, diabetes, orthopedic disorders, and wound care.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

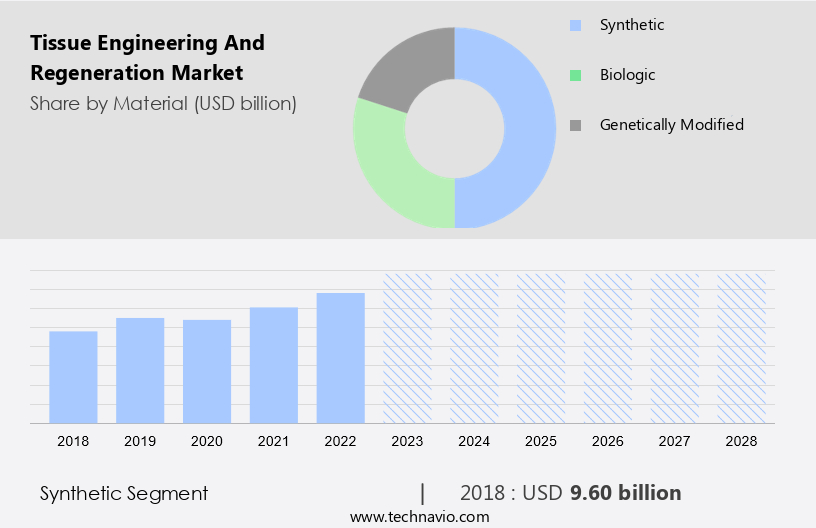

- Material

- Synthetic

- Biologic

- Genetically modified

- Application

- Orthopedic musculoskeletal and spine

- Dermatology

- Neurology

- Others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

By Material Insights

The synthetic segment is estimated to witness significant growth during the forecast period. The synthetic segment of The market involves the utilization of synthetic materials and constructs for tissue engineering and regeneration applications. Synthetic materials present several advantages, such as controllable properties, customizable structures, and a reduced risk of immune rejection. This segment comprises a vast array of products and materials, including scaffolds, polymers, hydrogels, and nanomaterials. Scaffolds represent a crucial product category in synthetic tissue engineering. These three-dimensional structures serve as a framework for cells to attach, proliferate, and differentiate. Synthetic scaffolds can be engineered using polymers like poly (lactic-co-glycolic acid) (PLGA), polycaprolactone (PCL), and polyethylene glycol (PEG). These polymers offer unique properties that facilitate tissue growth and regeneration.

Furthermore, in the realm of tissue engineering, life science innovations continue to advance, addressing chronic diseases, trauma crises, and the need for biological replacements. Regenerative medicine and tissue signaling play pivotal roles in the development of synthetic tissue engineering solutions. Vascularization, a critical aspect of tissue engineering, ensures the growth and survival of engineered tissues. Organ transplants remain a significant challenge due to the limited availability of donor organs. Synthetic tissue engineering offers a promising alternative, providing customizable, biocompatible solutions. The market is expected to grow, driven by the increasing prevalence of chronic diseases and trauma crises. Biomolecules, such as growth factors and cytokines, are essential components in tissue engineering, enhancing cellular processes and promoting tissue regeneration.

Get a glance at the market share of various segments Request Free Sample

The Synthetic segment was valued at USD 9.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

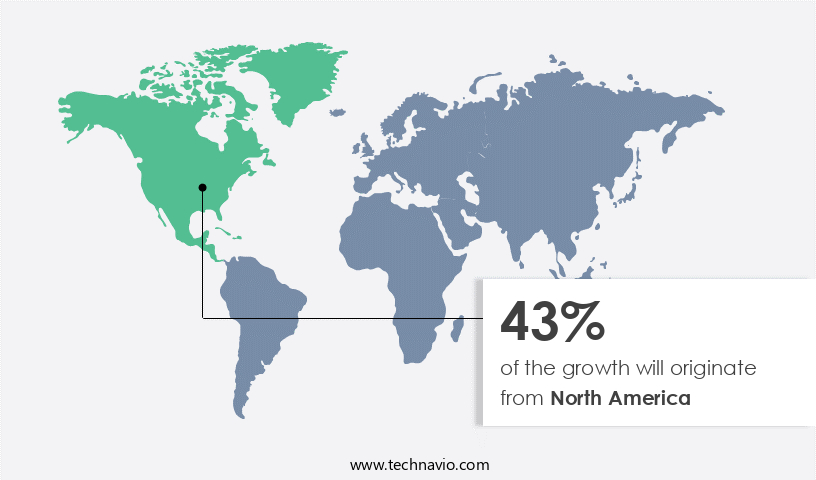

North America is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the market holds a significant share of the global industry. Key players, such as Smith & Nephew, RTI Surgical, and Integra Lifesciences, contribute significantly to the region's market dominance. These companies are expanding their product portfolios and enhancing their sales efforts to boost their market presence in North America. The US and Canada are the primary contributors to the North American market, driven by factors like the high prevalence of acute and chronic diseases, a rapidly aging population, and substantial investments in regenerative medicine. Bioresorbable solutions are gaining popularity in various medical fields, including orthopedics and musculoskeletal, neurology, cardiovascular, skin and integumentary, dental, ophthalmology, gastrointestinal disorders, obstetrics, and soft tissues. In ocular tissue engineering, innovative approaches are being developed to address conditions like glaucoma, corneal disease, and ocular cancer. North America's advanced healthcare infrastructure and regulatory framework support the growth of these advanced technologies, ensuring the region's continued leadership in The market.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Increasing prevalence of chronic diseases is the key driver of the market. The prevalence of chronic diseases, including diabetes and cancer, in the US has led to a heightened demand for cell-based therapies. Chronic diseases, such as cancer, cardiovascular diseases (CVDs), autoimmune disorders, and infectious diseases, pose significant challenges to healthcare systems. Tissue engineering and regeneration technology are essential in developing innovative treatments for these conditions. Chronic wounds, in particular, pose a significant burden on patients, healthcare professionals, and the healthcare system. Tissue engineering and regeneration techniques, including the use of stem cells and 3D bioprinting, offer promising solutions for wound healing.

Furthermore, regenerative medicines, which utilize living cells, biomaterials, and the body's own healing process, are increasingly being used to treat various degenerative diseases. Advancements in tissue engineering and regeneration technology have the potential to revolutionize organ transplantation techniques. Hospitals, specialty clinics, ambulatory surgical centers, and transplant centers are increasingly adopting these technologies to provide better patient care. For instance, 3D bioprinting can be used to create complex tissues and organs, reducing the waitlist for organ transplants. Traumatic injuries, such as those resulting from road accidents, can also benefit from tissue engineering and regeneration technology. These injuries can lead to significant tissue damage and long-term disability.

Market Trends

Emerging technological advances is the upcoming trend in the market. The market is experiencing significant progress with the development of advanced technologies for addressing various clinical disorders. One of the notable applications is the regeneration of complex structures like spinal cord injured segments using tissue engineered bladders and other organs. Three-dimensional (3D) tissue engineering has emerged as a promising approach, with the utilization of 3D bioprinters enabling the creation of human tissue with precise control over size, shape, pore size, geometry, and mechanical properties.

Furthermore, this technology offers potential benefits in cancer research, as it enables researchers to study the effects of drugs and treatments on human tissue. Additionally, it holds promise for musculoskeletal disorders such as rheumatoid arthritis and cardiovascular disorders. Gene therapy is another area of focus, with ongoing clinical studies exploring its potential in tissue regeneration. The market is witnessing increased investment in research and development, driven by the potential to address unmet medical needs and improve patient outcomes. Key players in the market include companies focusing on stem cell therapies and tissue engineering solutions.

Market Challenge

Uncertain regulatory approval in tissue engineering and regeneration products is a key challenge affecting the market growth. Tissue engineering and regenerative medicine have seen significant advancements over the past few decades, with cell therapy and gene therapy being key areas of focus. However, the clinical application of these technologies is still evolving, particularly in the context of various diseases, including orthopedic disorders, musculoskeletal disorders, dental disorders, cardiovascular diseases, and dermatology. Wound care and diabetes are also areas of interest. Regulatory authorities play a crucial role in the development and commercialization of tissue engineering solutions.

However, the regulatory approval process can be lengthy and uncertain, posing challenges for companies. Tissue grafts, a significant segment of the tissue engineering market, must undergo rigorous testing and regulatory approval before use. Key disease areas, such as orthopedic disorders and cardiovascular diseases, are expected to drive market growth. Stem cell research and gene editing techniques are also contributing to the advancement of tissue engineering and regenerative medicine. Despite these advancements, there are still regulatory and ethical considerations that must be addressed to ensure the safety and efficacy of these products.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

3M Co. - The company offers tissue engineering and regeneration products such as the 3M Veraflo Cleanse Choice Complete Dressing Kit and 3M Smart Instil for Veraflo Therapy.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- AbbVie Inc.

- Astellas Pharma Inc.

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Co.

- CO.DON GmbH

- Cook Group Inc.

- Integra Lifesciences Corp.

- Johnson and Johnson Services Inc.

- Medtronic Plc

- Organogenesis Holdings Inc.

- Plus Therapeutics Inc.

- REPROCELL Inc.

- RTI Surgical Inc.

- Smith and Nephew plc

- Stryker Corp.

- Tissue Regenix Group Plc

- Vericel Corp.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Tissue engineering, a branch of life science, focuses on creating biological replacements for organs and complex tissues using scaffolds, cells, and biomolecules. This field has gained significant attention due to the increasing prevalence of chronic diseases, trauma crises, and organ failures. Tissue engineering offers promising solutions for various medical conditions, including orthopedics and musculoskeletal disorders, neurology, cardiovascular diseases, skin and integumentary issues, dental disorders, ophthalmology, gastrointestinal disorders, obstetrics, and soft tissues. The market for tissue engineering is vast and diverse, encompassing various applications and segments. Scaffolds, made from synthetic and natural materials like collagen, alginate, proteoglycans, chitin, agarose, matrigel, chitosan, xenogeneic materials, and synthetic biomaterials, serve as the foundation for tissue regeneration.

Moreover, microstructures of these materials can be bioinert, bioactive, or bioresorbable, depending on the specific application. Tissue engineering has the potential to revolutionize medical therapy for numerous conditions, including trauma injuries, accidents, burn injuries, and accidental deaths caused by motor vehicle accidents. The use of living cells, organ transplantation techniques, and medical equipment such as surgical tools and sterile environments are essential components of this field. The regenerative medicine sector, which includes tissue engineering, is experiencing rapid growth due to advancements in medical automation technology and the monopolistic environment created by regulatory authorities. This field holds immense promise for the development of original organs and complex tissues, including human liver prototypes, and the treatment of degenerative diseases, such as cancer, spinal cord injury, and rheumatoid arthritis.

Furthermore, clinical studies and gene editing techniques are also playing a crucial role in the advancement of tissue engineering and regenerative medicines. 3D bioprinting and stem cell therapies are some of the latest innovations in this field, offering potential solutions for ocular tissue engineering, glaucoma, corneal disease, ocular cancer, and other clinical disorders. In conclusion, tissue engineering and regenerative medicine hold immense potential for addressing various medical challenges and improving the quality of life for patients. The market for tissue engineering is diverse and expansive, encompassing numerous applications and segments, and is poised for significant growth in the coming years.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.86% |

|

Market growth 2024-2028 |

USD 28.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.17 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 43% |

|

Key countries |

US, Germany, UK, Canada, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3M Co., AbbVie Inc., Astellas Pharma Inc., B.Braun SE, Baxter International Inc., Becton Dickinson and Co., CO.DON GmbH, Cook Group Inc., Integra Lifesciences Corp., Johnson and Johnson Services Inc., Medtronic Plc, Organogenesis Holdings Inc., Plus Therapeutics Inc., REPROCELL Inc., RTI Surgical Inc., Smith and Nephew plc, Stryker Corp., Tissue Regenix Group Plc, Vericel Corp., and Zimmer Biomet Holdings Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -