Unified Communication And Collaboration Market Size 2025-2029

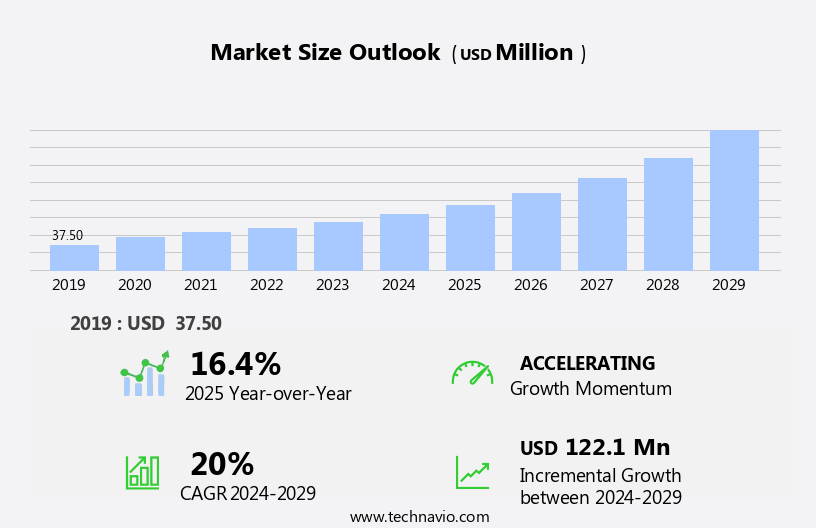

The unified communication and collaboration market size is forecast to increase by USD 122.1 million, at a CAGR of 20% between 2024 and 2029.

- The Unified Communication and Collaboration (UCC) market is experiencing significant growth, driven by the increasing demand for video and voice conferencing solutions. The flexibility and convenience offered by these technologies are increasingly essential in today's remote and hybrid work environments. AI-powered assistants, analytics and reporting, and file sharing contribute to an enhanced digital workplace experience. This not only enhances productivity but also reduces the need for organizations to invest in additional hardware. However, the UCC market also faces challenges, primarily related to data privacy and security concerns.

- With the increasing use of cloud-based solutions and the growing amount of sensitive data being shared, ensuring the security of communications and collaboration platforms is paramount. Companies must invest in robust security measures to protect their data and mitigate the risk of cyber attacks. Additionally, ensuring compliance with various data protection regulations, such as GDPR and HIPAA, is a significant challenge. API management and scalability testing enable efficient integration and expansion.

What will be the Size of the Unified Communication And Collaboration Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic applications across various sectors. Team collaboration tools facilitate real-time project management and document sharing, enabling remote teams to work together seamlessly. Video conferencing solutions enable face-to-face communication, while instant messaging and presence management keep teams connected. Maintenance contracts ensure system reliability, while access control maintains security. Integration services connect various applications, enabling a cohesive workflow. Screen sharing and application sharing enhance collaboration, while video conferencing hardware caters to larger meetings. Cloud-based UCaaS and collaboration platforms offer flexibility and scalability, while on-premise UC solutions provide greater control. Hybrid UC solutions offer the best of both worlds.

Regulatory standards ensure compliance, and mobile access and meeting scheduling enhance productivity. API integrations and transcription services streamline workflows, while data encryption ensures data security. Call center software offers advanced call routing and queuing capabilities. Digital whiteboards enable brainstorming sessions, and training programs ensure user adoption. Web conferencing and audio conferencing cater to different communication needs. Workflow automation enhances productivity, and virtual desktops offer remote access to applications and data. The market's continuous dynamism underlines the importance of staying informed and adaptable.

How is this Unified Communication And Collaboration Industry segmented?

The unified communication and collaboration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Enterprise collaboration

- Enterprise telephony

- Contact center

- End-user

- Enterprise

- Government

- Sector

- Large Enterprises

- Small and medium-sized enterprises (SMEs)

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

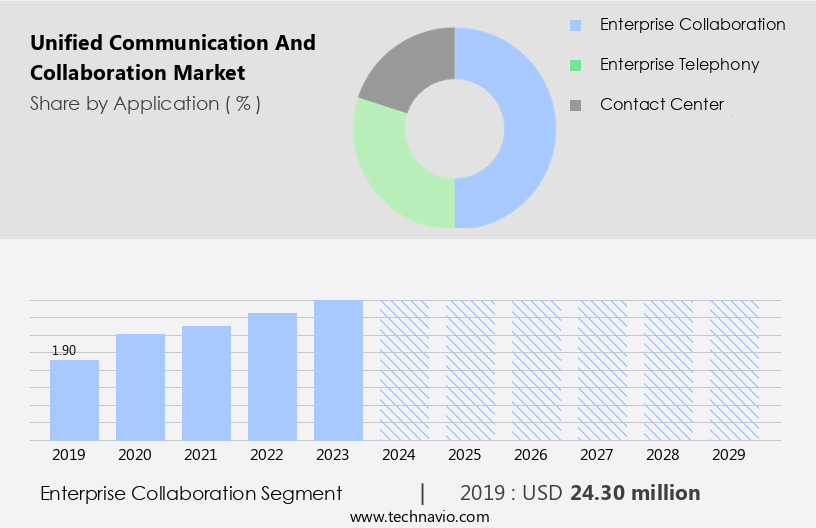

The enterprise collaboration segment is estimated to witness significant growth during the forecast period. In the business landscape of 2024, small and medium-sized enterprises (SMEs) are increasingly adopting advanced communication and collaboration (UC and C) solutions to optimize workflows and improve customer engagement. These tools encompass email, unified messaging, mobile UC, instant messaging, and more, becoming more user-friendly, cost-effective, and integrated into daily business processes. The fusion of collaborative applications like email, calendaring, and social media with core business functions is gaining momentum, fueled by the demand for automation and real-time responsiveness. Unified communications remain a pivotal aspect of enterprise collaboration strategies. Among these, audio and web conferencing solutions lead the way due to their flexibility and cost savings compared to traditional in-person meetings.

Transcription services and virtual desktops offer additional functionality. Team collaboration, call queuing, and video conferencing are essential for remote and distributed teams. Another key trend is the adoption of the Bring Your Own Device (BYOD) concept, which allows employees to use their personal devices for work-related communication and collaboration. Deployment models range from cloud-based to hybrid, catering to diverse business needs. Overall, the UC and C market continues to evolve, driven by the need for efficient, cost-effective, and integrated communication and collaboration solutions. To capitalize on market opportunities and navigate these challenges effectively, organizations must prioritize security and privacy in their UCC strategies, while also leveraging the latest technologies to enhance productivity and collaboration.

The Enterprise collaboration segment was valued at USD 24.30 million in 2019 and showed a gradual increase during the forecast period.

File sharing, document collaboration, and knowledge sharing are also essential components, enabling teams to work together seamlessly. Presence management, call center software, and team collaboration tools further enhance productivity and efficiency. Cloud-based UCaaS and on-premise UC solutions offer flexibility in deployment models. API integrations and screen sharing facilitate seamless application sharing during meetings. Regulatory standards ensure data encryption and access control for secure information exchange. Instant messaging, meeting scheduling, remote access, and call routing streamline communication processes. Project management tools, video conferencing hardware, and training programs ensure user adoption and workforce productivity. Maintenance contracts and integration services provide ongoing support and ensure seamless integration with existing systems.

Regional Analysis

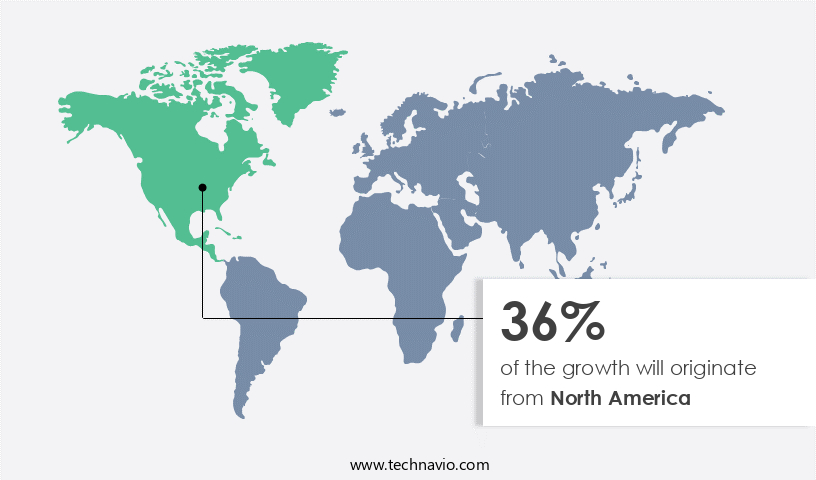

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth due to the increasing demand for cost-effective and user-friendly browser-based solutions. The widespread adoption of communications and collaboration platforms in enterprises is fueling this demand. Large enterprises, with their extensive digitalization efforts, are leading the way in implementing unified communication and collaboration solutions. Moreover, as the number of mobile workers rises, organizations are utilizing these solutions to manage and optimize their tasks and workflows. Presence management, instant messaging, call routing, and call queuing are key features that enhance workforce productivity. Cloud-based UCaaS and on-premise UC solutions offer flexibility in deployment models.

API integrations, document collaboration, and knowledge sharing facilitate seamless workflow automation. Data encryption ensures security, while user adoption and access control promote efficient team collaboration. Video conferencing, audio conferencing, and web conferencing enable remote access and virtual meetings. Training programs and maintenance contracts ensure smooth implementation and continued support. The presence of major market players in the US and Canada further strengthens the market's growth.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Unified Communication And Collaboration Industry?

- The increasing need for remote communication solutions, as evidenced by the growing demand for video and voice conferencing, is a primary market driver. The Unified Communications and Collaboration (UCC) market continues to gain traction in 2024, with voice and video conferencing remaining essential components of IT infrastructure and business operations. The shift towards hybrid and remote work models has popularized personal video solutions, particularly in industries focusing on knowledge processing and customer support. Unified Communications (UC) and Contact Center (CC) technologies are becoming essential tools for businesses seeking to improve communication and collaboration among employees, suppliers, and clients.

- Cloud-based UCC solutions, such as collaboration platforms, have gained prominence due to their ease of remote access and scalability. Data encryption ensures secure communication, while call center software and application sharing cater to specific business needs. UCC platforms have evolved into comprehensive ecosystems, offering P2P voice and video interactions, enhanced with AI-driven features like real-time transcription, language translation, and automated meeting summaries. These advancements boost meeting productivity while lessening cognitive burden on participants.

What are the market trends shaping the Unified Communication And Collaboration Industry?

- The BYOD (Bring Your Own Device) concept is gaining significant traction in the market, with an increasing number of organizations adopting this trend. This shift towards allowing employees to use their personal devices for work purposes reflects a growing trend in modern business practices. The Unified Communication and Collaboration (UCC) market is witnessing significant growth due to the increasing adoption of Bring Your Own Device (BYOD) policies in workplaces. Approximately one-third of employers worldwide provide devices, and over half encourage their employees to use their own devices for work. UCC solutions cater to the professional standards of interactions and workflow across various remote devices, making them increasingly popular among end-users.

- These features enhance user adoption and workforce productivity by streamlining communication and collaboration processes. For instance, web conferencing enables remote teams to conduct virtual meetings, while call routing and queuing facilitate efficient call handling. Moreover, digital whiteboards offer a collaborative workspace where team members can brainstorm ideas and share visual content in real-time. Transcription services enable users to convert audio recordings into text, making it easier to search for specific information. These platforms adjust the frame rate and resolution based on the device used, ensuring high-quality experiences. UCC solutions encompass various features such as workflow automation, audio conferencing, virtual desktops, transcription services, web conferencing, digital whiteboards, call routing, and call queuing.

What challenges does the Unified Communication And Collaboration Industry face during its growth?

- Data privacy and security concerns represent a significant challenge to the industry's growth, necessitating rigorous measures to protect sensitive information and maintain trust with customers. Cloud-based Unified Communication and Collaboration (UCC) solutions have gained significant traction among businesses due to their cost-effectiveness and ease of accessibility. These solutions offer team collaboration features such as instant messaging, access control, project management, and integration services. Video conferencing hardware is also available for enhanced functionality.

- Cloud-based UCC platforms provide streamlined software maintenance, reducing capital expenditure for businesses. They offer scalable infrastructure, adapting to evolving administrative demands. Government agencies, in particular, have been migrating sensitive data to cloud environments due to the need for centralized data management, seamless collaboration, and operational efficiency. In 2024, federal, state, and local government agencies worldwide continue this trend, ensuring their IT infrastructure remains agile and responsive to changing needs. Integration with various business applications is another advantage of cloud-based UCC solutions, ensuring a cohesive and efficient workflow.

Exclusive Customer Landscape

The unified communication and collaboration market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the unified communication and collaboration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, unified communication and collaboration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

8x8 Inc. - The company delivers integrated communication and collaboration solutions, encompassing voice, video, messaging, and meeting functionalities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 8x8 Inc.

- AT and T Inc.

- Atos SE

- Avaya LLC

- BT Group Plc

- Cisco Systems Inc.

- GoTo Technologies USA Inc.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Intrado Life and Safety Inc.

- Microsoft Corp.

- Mitel Networks Corp.

- NEC Corp.

- Nippon Telegraph and Telephone Corp.

- RingCentral Inc.

- SANGOMA TECHNOLOGIES CORP.

- Verizon Communications Inc.

- Vonage Holdings Corp.

- Zoho Corp. Pvt. Ltd.

- Zoom Video Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Unified Communication And Collaboration Market

- In January 2024, Microsoft Teams, a leading player in the Unified Communication and Collaboration (UCC) market, introduced new features to enhance its virtual meeting capabilities. The tech giant launched "Microsoft Teams Live Events," enabling organizations to host large-scale webinars and live broadcasts for up to 10,000 attendees (Microsoft Press Release).

- In March 2024, Cisco Systems and Google Cloud announced a strategic partnership to integrate Cisco Webex with Google Workspace. This collaboration aimed to provide seamless communication and collaboration experiences for users, combining the strengths of both platforms (Cisco Press Release).

- In May 2024, Zoom Video Communications raised USD 1 billion in a secondary offering, demonstrating strong investor confidence in the UCC market's growth potential. The company plans to use the proceeds for working capital and general corporate purposes (SEC Filing).

- In April 2025, Slack Technologies, a major UCC player, acquired Rimeto, a startup specializing in organizational intelligence and people search. The acquisition aimed to strengthen Slack's offerings in the areas of team management and productivity (Slack Press Release).

Research Analyst Overview

The unified communication and collaboration (UCC) market is experiencing significant growth, driven by increasing bandwidth requirements for real-time data transfer and the need for seamless software upgrades. Single sign-on (SSO) and system integration have become essential for businesses seeking to streamline processes and improve user experience. Quality of service, supported by advanced technologies like artificial intelligence (AI) and machine learning (ML), is a key differentiator. Change management and multi-factor authentication ensure security and minimize disruptions during software updates. Disaster recovery and high availability solutions mitigate risks, while packet loss and voice recognition technologies enhance user experience.

Cost optimization, user training, and company management are crucial for effective UCC implementation. Technical support and customer service, underpinned by directory services and business continuity plans, are essential for maintaining user satisfaction. Network infrastructure plays a pivotal role in enabling reliable and efficient UCC services. The Unified Communication and Collaboration Market is expanding swiftly as organizations prioritize seamless connectivity and real-time collaboration. Centralized vendor management is becoming a strategic focus, ensuring reliability and consistency across communication platforms and third-party integrations. Enhanced support services are crucial in maintaining uptime, resolving technical issues swiftly, and delivering a frictionless user experience. Meanwhile, the integration of sentiment analysis tools is revolutionizing internal communications and customer interactions by gauging tone, engagement, and satisfaction.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Unified Communication And Collaboration Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

218 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20% |

|

Market growth 2025-2029 |

USD 122.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

16.4 |

|

Key countries |

US, China, Canada, UK, India, Germany, Japan, France, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Unified Communication And Collaboration Market Research and Growth Report?

- CAGR of the Unified Communication And Collaboration industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the unified communication and collaboration market growth of industry companies

We can help! Our analysts can customize this unified communication and collaboration market research report to meet your requirements.

RIA -

RIA -