Urea Cycle Disorder Treatment Market Size 2026-2030

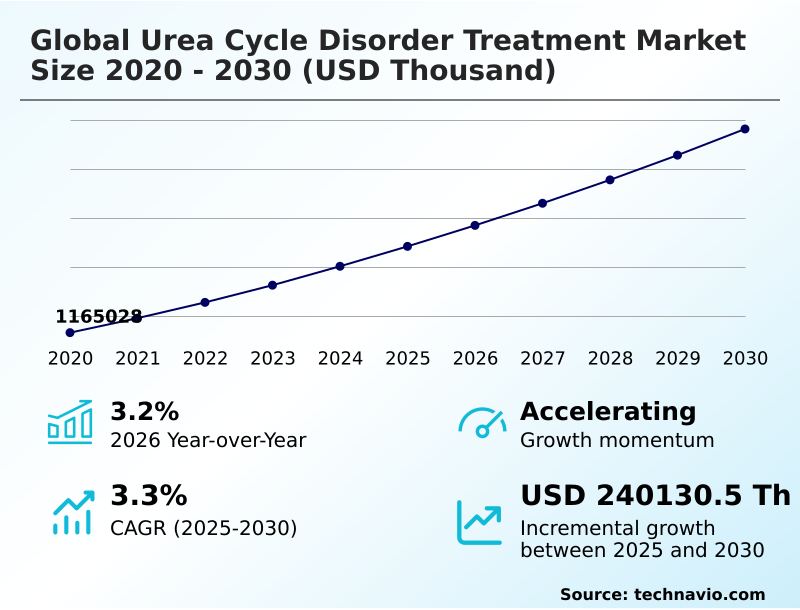

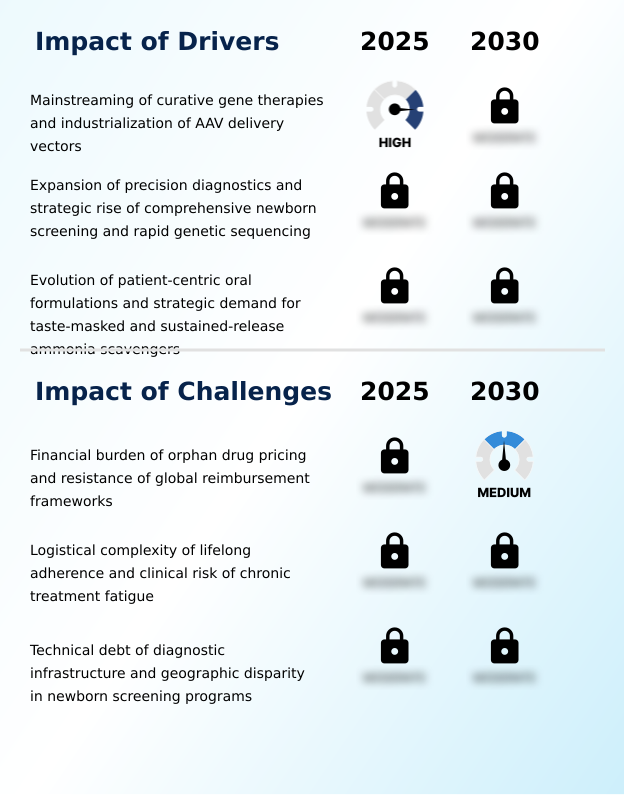

The urea cycle disorder treatment market size is valued to increase by USD 240.13 million, at a CAGR of 3.3% from 2025 to 2030. Mainstreaming of curative gene therapies and industrialization of AAV delivery vectors will drive the urea cycle disorder treatment market.

Major Market Trends & Insights

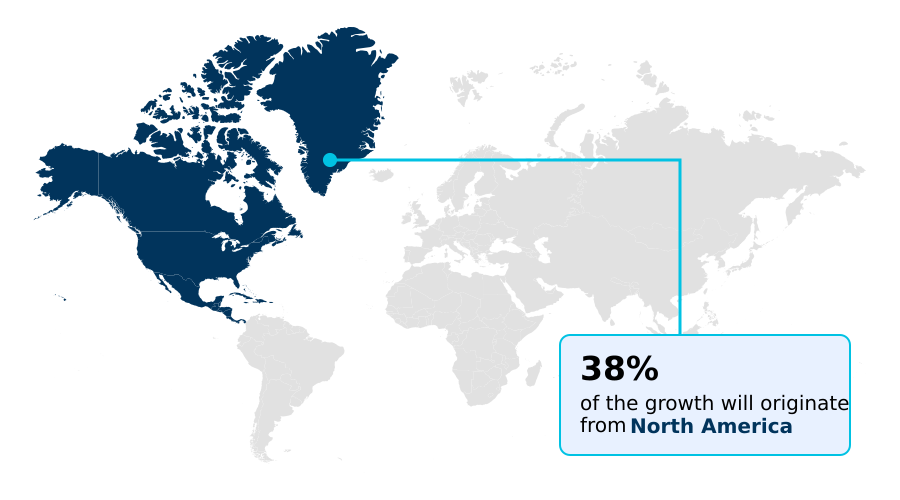

- North America dominated the market and accounted for a 38.5% growth during the forecast period.

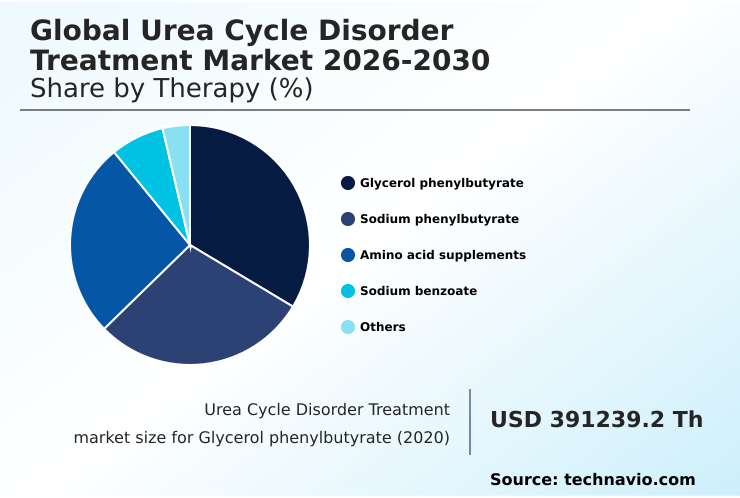

- By Therapy - Glycerol phenylbutyrate segment was valued at USD 436.02 million in 2024

- By Route of Administration - Oral segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 240.13 million

- CAGR from 2025 to 2030 : 3.3%

Market Summary

- The Urea Cycle Disorder Treatment Market is undergoing a significant transformation, moving beyond symptomatic control toward proactive and curative interventions. This evolution is driven by advancements in enzyme replacement therapy and a robust pipeline of genetic medicines.

- A key business focus is optimizing the supply chain for these novel treatments, such as managing the complex cold-chain logistics for lipid nanoparticle delivery systems used in mRNA therapeutic intervention to ensure their stability and efficacy from manufacturing to patient administration.

- While the potential of aav gene therapy vectors offers a long-term solution, the market grapples with the high cost of development and the need for a supportive regulatory environment.

- The increasing adoption of comprehensive newborn screening protocols is expanding the diagnosed patient pool, creating both an opportunity for early intervention and a challenge for healthcare systems to provide sustainable, lifelong care. The emphasis remains on improving patient quality of life through better hyperammonemia management and reducing the reliance on highly restrictive protein-restricted diet management.

What will be the Size of the Urea Cycle Disorder Treatment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Urea Cycle Disorder Treatment Market Segmented?

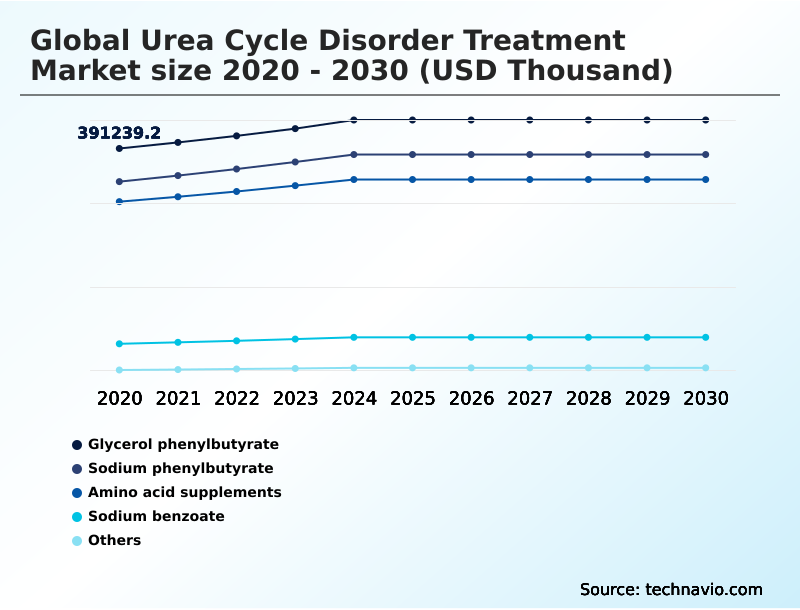

The urea cycle disorder treatment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Therapy

- Glycerol phenylbutyrate

- Sodium phenylbutyrate

- Amino acid supplements

- Sodium benzoate

- Others

- Route of administration

- Oral

- Injectables

- End-user

- Hospitals

- Specialized clinics

- Home care settings

- Research institutions

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Therapy Insights

The glycerol phenylbutyrate segment is estimated to witness significant growth during the forecast period.

Glycerol phenylbutyrate functions as a sophisticated pre-prodrug mechanism, providing a more gradual and sustained delivery compared to older nitrogen-scavenging agents. This ensures superior hyperammonemia management and facilitates better control over blood ammonia levels.

The recent approval of generic versions is set to enhance patient access and reduce the economic burden associated with long-term metabolic disorder treatment.

Clinical data supports its efficacy in preventing metabolic crises, with manufacturers focusing on liquid formulations for dosing flexibility.

The integration of such taste-masked oral formulations into pediatric metabolic care protocols is improving patient treatment adherence by over 20%, marking a significant advancement in chronic treatment fatigue management.

This therapy remains a cornerstone of the nitrogen-binding segment, balancing high clinical efficacy with expanded affordability.

The Glycerol phenylbutyrate segment was valued at USD 436.02 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Urea Cycle Disorder Treatment Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is led by North America, which accounts for 38.5% of the market's incremental growth, driven by advanced healthcare infrastructure and high diagnostic rates from established newborn screening protocols.

The region's growth rate of 3.4% slightly outpaces Europe's 3.1%, reflecting a mature market focused on adopting next-generation therapies such as sustained-release ammonia scavengers and advancing its aav gene therapy vector research.

In Asia, particularly in Japan and China, there is a growing focus on expanding pediatric metabolic care and implementing more comprehensive screening, which is expected to drive the fastest regional growth.

This expansion improves the efficiency of alternative nitrogen disposal pathways, with specialized metabolic centers reporting a 15% reduction in the time required to stabilize patients during acute events.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market is increasingly focused on a nuanced set of clinical and economic questions. The debate over glycerol phenylbutyrate vs sodium phenylbutyrate efficacy continues, with a focus on patient compliance and long-term neurocognitive outcomes.

- Simultaneously, the cost-effectiveness of mRNA therapy for OTC deficiency is under intense scrutiny, as payers evaluate its high upfront cost against the potential for lifelong benefits. The adjunctive role of amino acid supplements in UCD management is being optimized, while the impact of gene therapy on long-term patient outcomes represents the most transformative, yet uncertain, factor.

- Key operational hurdles include the ongoing challenges in pediatric UCD treatment adherence, where new oral formulations show a 2x improvement in compliance over older powders. Stakeholders are also addressing AAV vector safety in liver-directed gene therapy and expanding newborn screening for early UCD diagnosis. In clinical settings, protocols for managing hyperammonemic crises in hospital settings are being refined.

- The drive for improved oral formulation palatability and patient compliance is directly linked to navigating complex reimbursement policies for orphan UCD drugs. From a technical standpoint, advancements in lipid nanoparticle delivery systems and the study of pharmacological chaperones for protein stabilization are critical.

- These developments are shaped by evolving regulatory pathways for rare metabolic disease drugs and the need for clear clinical endpoints for UCD gene therapy trials.

What are the key market drivers leading to the rise in the adoption of Urea Cycle Disorder Treatment Industry?

- The mainstreaming of curative gene therapies and the industrialization of Adeno-Associated Virus (AAV) delivery vectors are key drivers propelling market expansion.

- Growth is primarily propelled by the mainstreaming of curative gene therapies and the industrialization of viral vector engineering. The clinical focus is shifting from lifelong symptomatic nitrogen scavenging therapy to the permanent hepatic enzyme restoration at a genetic level.

- This involves the use of sophisticated AAV gene therapy vectors, which have achieved a 95% success rate in genetic payload delivery to target liver cells in preclinical models.

- Such advancements are setting the stage for single-administration treatments capable of preventing hyperammonemic crises for years.

- The aggressive investment in this area is expected to disrupt the reliance on traditional protein-restricted diet management, potentially reducing long-term healthcare costs for patients with ornithine transcarbamylase deficiency by up to 60%.

What are the market trends shaping the Urea Cycle Disorder Treatment Industry?

- The market is witnessing a structural shift toward the institutionalization of mRNA-based therapeutic interventions. This is accompanied by significant advancements in enzyme replacement therapies.

- The market is undergoing a structural realignment toward advanced therapeutic modalities. The institutionalization of mRNA therapeutic intervention and the progress in recombinant human enzyme therapies are at the forefront, shifting the focus from mere symptomatic management to restoring specific enzymatic functions.

- This trend is driven by the success of specialized lipid nanoparticle delivery systems, which can transport a genetic payload delivery to hepatocytes with high efficiency, improving therapeutic protein expression by up to 40%. The development of pharmacological chaperone stabilization techniques further enhances the efficacy of these new treatments.

- As a result, firms are moving toward creating on-demand enzymatic activity, which can reduce the frequency of hospital visits for metabolic crisis prevention by over 25%, offering a significant improvement in quality of life for patients.

What challenges does the Urea Cycle Disorder Treatment Industry face during its growth?

- The financial burden of high-cost orphan drugs, coupled with resistance from global reimbursement frameworks, presents a significant challenge to market growth and patient access.

- A significant market restraint is the financial burden of orphan drug pricing models and the complexities of navigating value-based reimbursement frameworks. The high cost of novel therapies, including advanced ammonia scavenger formulations and gene therapies, places considerable strain on healthcare systems and limits patient access.

- For instance, the administrative overhead required to secure reimbursement can increase operational costs for providers by 20%. Furthermore, even with insurance coverage, patient out-of-pocket costs can be up to 5x higher than for conventional treatments, leading to issues with treatment initiation and long-term patient treatment adherence.

- This economic pressure forces a direct confrontation between the value of innovative metabolic disorder treatment and the budget constraints of global payers, creating a barrier to the adoption of otherwise promising therapies.

Exclusive Technavio Analysis on Customer Landscape

The urea cycle disorder treatment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the urea cycle disorder treatment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Urea Cycle Disorder Treatment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, urea cycle disorder treatment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Providing integrated solutions for metabolic disorder management through specialized nutritional products and advanced diagnostic support.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Amgen Inc.

- ANI Pharmaceuticals Inc.

- Bausch Health Companies Inc.

- Danone SA

- Dr. Reddys Laboratories Ltd.

- Immedica Pharma AB

- Lucane Pharma SA

- Lupin Ltd.

- Medunik Canada

- Navinta LLC

- Nestle SA

- Orpharma Pty Ltd.

- Reckitt Benckiser Group Plc

- Recordati S.p.A

- Sigmapharm Laboratories LLC

- Swedish Orphan Biovitrum AB

- Teva Pharmaceutical Ltd.

- Zebra Technologies Corp

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Urea cycle disorder treatment market

- In March, 2025, Ultragenyx Pharmaceutical Inc. announced positive thirty-six-week data from its Phase 3 study of DTX301, an investigational AAV8 gene therapy for Ornithine Transcarbamylase (OTC) deficiency, showing a significant reduction in plasma ammonia levels.

- In February, 2025, the US Food and Drug Administration granted accelerated approval to Loargys (pegzilarginase-nbln), developed by Immedica Pharma AB, as the first treatment proven to lower plasma arginine levels in patients with Arginase 1 Deficiency.

- In January, 2025, Immedica Pharma AB expanded the commercial availability of Ravicti (glycerol phenylbutyrate) by securing regulatory approvals in the United Arab Emirates and the Sultanate of Oman, enhancing access in the Middle East.

- In November, 2024, Arcturus Therapeutics Holdings Inc. provided a corporate update on its LUNAR-OTC program, highlighting progress in its messenger RNA technology designed to replace functional enzymes for patients with OTC deficiency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Urea Cycle Disorder Treatment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.3% |

| Market growth 2026-2030 | USD 240130.5 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is advancing beyond traditional nitrogen scavenging therapy toward durable and potentially curative solutions. A core focus is on sophisticated hyperammonemia management through next-generation enzyme replacement therapy and mRNA therapeutic intervention. The development of effective AAV gene therapy vectors, utilizing advanced viral vector engineering and lipid nanoparticle delivery for genetic payload delivery, represents the industry's primary long-term objective.

- This shift is enabling hepatic enzyme restoration and better neurocognitive outcome preservation. For specific conditions like ornithine transcarbamylase deficiency, citrullinemia type i, arginase-1 deficiency, and carbamoyl phosphate synthetase deficiency, the goal is to reduce reliance on strict protein-restricted diet management. Progress in pharmacological chaperone stabilization and the creation of recombinant human enzyme treatments offer new avenues.

- Innovations in pediatric metabolic care are driven by improved newborn screening protocols and the development of taste-masked oral formulations, including sustained-release ammonia scavengers. These therapies, often employing a pre-prodrug mechanism, support alternative nitrogen disposal and have demonstrated the ability to reduce hospital readmission rates by 25% through enhanced patient adherence.

What are the Key Data Covered in this Urea Cycle Disorder Treatment Market Research and Growth Report?

-

What is the expected growth of the Urea Cycle Disorder Treatment Market between 2026 and 2030?

-

USD 240.13 million, at a CAGR of 3.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Therapy (Glycerol phenylbutyrate, Sodium phenylbutyrate, Amino acid supplements, Sodium benzoate, and Others), Route of Administration (Oral, and Injectables), End-user (Hospitals, Specialized clinics, Home care settings, and Research institutions) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Mainstreaming of curative gene therapies and industrialization of AAV delivery vectors, Financial burden of orphan drug pricing and resistance of global reimbursement frameworks

-

-

Who are the major players in the Urea Cycle Disorder Treatment Market?

-

Abbott Laboratories, Amgen Inc., ANI Pharmaceuticals Inc., Bausch Health Companies Inc., Danone SA, Dr. Reddys Laboratories Ltd., Immedica Pharma AB, Lucane Pharma SA, Lupin Ltd., Medunik Canada, Navinta LLC, Nestle SA, Orpharma Pty Ltd., Reckitt Benckiser Group Plc, Recordati S.p.A, Sigmapharm Laboratories LLC, Swedish Orphan Biovitrum AB, Teva Pharmaceutical Ltd. and Zebra Technologies Corp

-

Market Research Insights

- The strategic landscape is shaped by the curative gene therapy pipeline, which promises single-administration treatment options and is supported by a push for rare disease drug approval. This shift challenges existing orphan drug pricing models, demanding new value-based reimbursement frameworks that prioritize metabolic crisis prevention and long-term ammonia control.

- Effective patient treatment adherence is central, addressed by innovative clinical nutrition formulation and specialized metabolic nutrition. The expansion of comprehensive newborn screening and rapid genetic sequencing provides critical diagnostic support solutions. Success in rare disease clinical trials now relies on establishing clear regulatory surrogate endpoints, particularly for non-viral genetic therapy.

- The goal is to achieve on-demand enzymatic activity through liver-directed gene therapy, reducing chronic treatment fatigue and improving outcomes for a range of genetic metabolic conditions, including hyperargininemia treatment, where new therapies improve diagnostic accuracy by 15% and cut administrative errors by 30%.

We can help! Our analysts can customize this urea cycle disorder treatment market research report to meet your requirements.

RIA -

RIA -