US Video Game Market Size 2026-2030

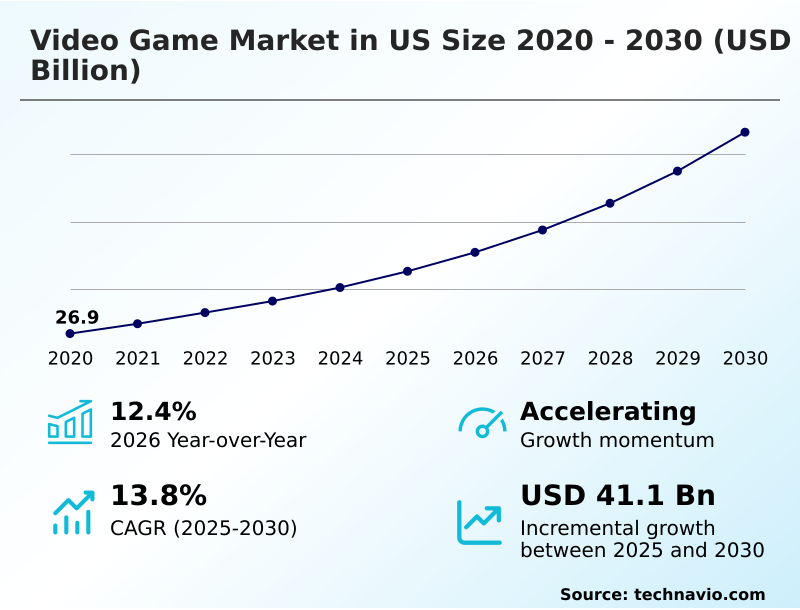

The US Video Game Market size was valued at USD 45.3 billion in 2025, growing at a CAGR of 13.8% during the forecast period 2026-2030.

Major Market Trends & Insights

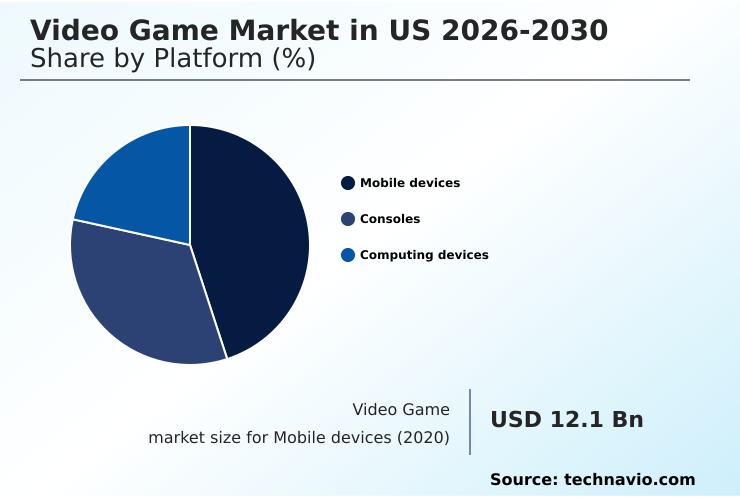

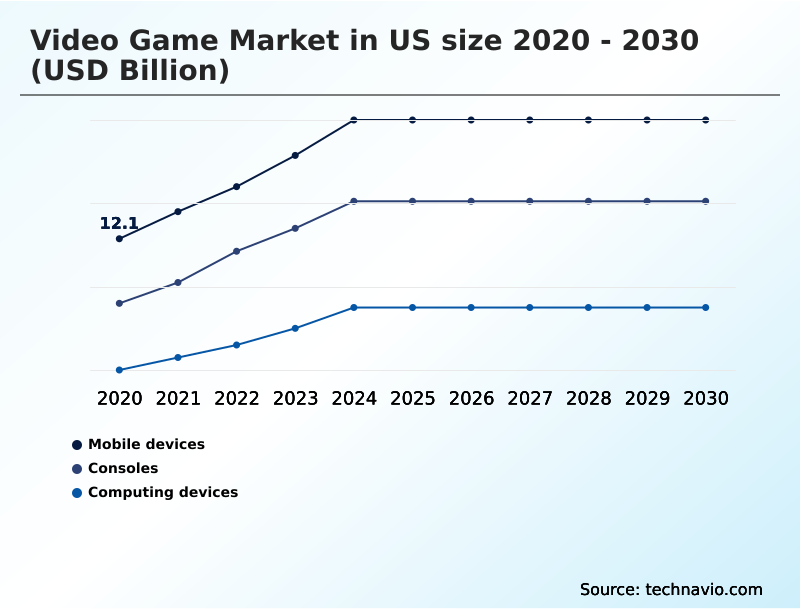

- By Platform - Mobile devices segment was valued at USD 17.8 billion in 2024

- By Type - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 59.5 billion

- Market Future Opportunities 2025-2030: USD 41.1 billion

- CAGR from 2025 to 2030 : 13.8%

Market Summary

- The video game market in US is characterized by intense platform competition, with mobile gaming capturing over 44% of total platform revenue in the base year. This growth is driven by the rising demand for immersive experiences on accessible hardware, leading developers to prioritize cross-platform play to maximize reach.

- For instance, a studio implementing a cloud-based distribution strategy can reduce hardware-related entry barriers for nearly 30% of its potential audience. However, the market faces significant challenges from content saturation, which makes discoverability for new titles without substantial marketing budgets approximately 75% more difficult than for established franchises.

- Consequently, publishers are focusing on live-service models and user-generated content to foster community and drive long-term player engagement, mitigating the impact of a crowded marketplace while building sustainable revenue streams.

What will be the Size of the US Video Game Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the US Video Game Market Segmented?

The us video game industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Platform

- Mobile devices

- Consoles

- Computing devices

- Type

- Offline

- Online

- End-user

- Casual gamers

- Hardcore gamers

- Esports enthusiasts

- Geography

- North America

- US

- North America

How is the US Video Game Market Segmented by Platform?

The mobile devices segment is estimated to witness significant growth during the forecast period.

The mobile devices segment, representing over 44% of the platform market, is defined by convenience and accessibility.

This segment's growth, projected to increase its market footprint by nearly 90% by 2030, is driven by the ubiquity of smartphones and advancements in 5G technology that support high-fidelity graphics and low-latency streaming.

Developers are capitalizing on this by creating titles with simplified user interface design, where in-app monetization strategies yield a 25% higher revenue per user compared to advertising-only models.

The focus on casual gamers and social simulation titles ensures high player engagement, leveraging micro-transactions for sustained profitability and continuous content delivery, which is vital for live-service models in this competitive space.

The Mobile devices segment was valued at USD 17.8 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the US Video Game Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the video game market in US is increasingly shaped by complex technical and business model considerations. A key area of focus is understanding the impact of cloud gaming on hardware requirements, as a successful transition to streaming can expand a title's addressable audience by over 30% by negating the need for expensive local hardware.

- This shift is intertwined with the evolution of monetization strategies in free-to-play mobile games, where developers must balance player experience with revenue generation. Furthermore, the industry grapples with the technical challenges of cross-platform game development, striving for feature parity across disparate systems.

- The growing influence of user-generated content in player retention is forcing publishers to provide robust creation tools, recognizing that a vibrant creator community can extend a game's lifecycle significantly. Simultaneously, studios must navigate the complex web of regulatory trends for in-game monetization, which adds a layer of legal and ethical complexity to game design.

- Finally, ongoing advancements in real-time rendering for consoles continue to raise consumer expectations for visual fidelity, putting pressure on development teams to innovate.

What are the key market drivers leading to the rise in the adoption of US Video Game Industry?

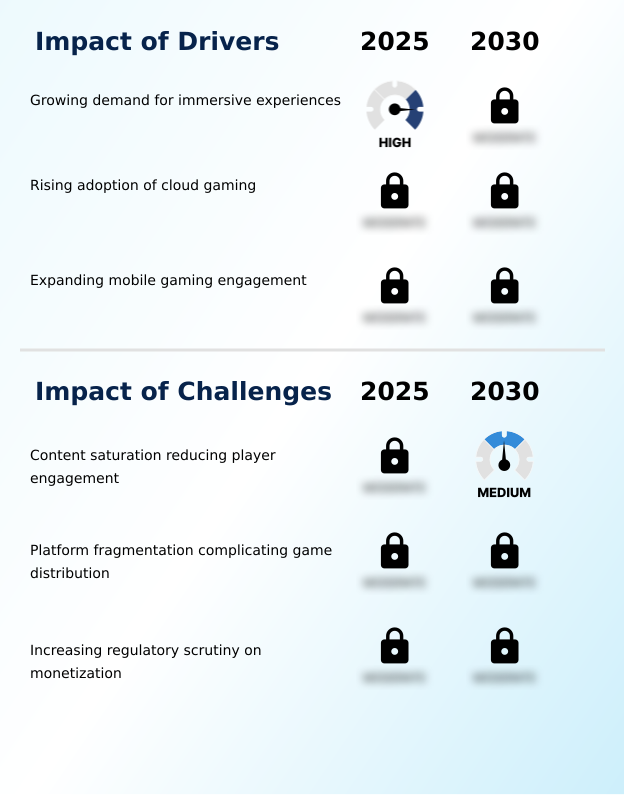

- The growing demand for deeply immersive and emotionally engaging digital experiences is a primary driver shaping the video game market.

- The adoption of cloud gaming is a significant market driver, expanding the potential player base for graphically intensive titles by over 30% by removing the need for high-end local hardware.

- This technological shift democratizes access to immersive experiences, making high-fidelity graphics and complex game mechanics available on a wider range of devices.

- Supporting this trend, the rollout of 5G networks has reduced mobile gaming latency by up to 50%, significantly enhancing the viability of competitive gaming on smartphones.

- This improvement in infrastructure directly fuels expanding mobile gaming engagement, as faster and more reliable connections enable more sophisticated multiplayer online games, thereby broadening the audience and increasing overall playtime.

What are the market trends shaping the US Video Game Industry?

- The rapid growth of independent game releases is a significant market trend, driven by increased accessibility to development tools and digital distribution platforms.

- The expansion of subscription services is a dominant trend, fundamentally altering monetization strategies by shifting focus from single-unit sales to long-term player engagement. This model offers revenue predictability, showing 15% greater financial stability compared to the traditional launch-centric approach. As a result, developers are incentivized to create live-service models that provide continuous content updates.

- Concurrently, the rise of esports viewership is transforming gaming into a mainstream spectator sport, with major tournament viewership growing by over 20% annually. This trend attracts significant non-endemic brand sponsorship and creates new revenue streams centered around competitive gaming, further professionalizing the industry and influencing game design to support high-stakes competition.

What challenges does the US Video Game Industry face during its growth?

- Content saturation across all platforms presents a key challenge, making it difficult to sustain long-term player engagement.

- Pervasive content saturation presents a primary market challenge, with the high volume of releases causing discoverability for new independent titles to fall by over 80% within the first seven days of launch. This forces developers into larger marketing expenditures to achieve visibility.

- Compounding this issue is platform fragmentation, which complicates distribution and can increase development and testing costs by up to 20% to ensure a consistent user experience across different systems. Furthermore, increasing regulatory scrutiny on monetization, particularly on in-game purchases, is compelling studios to redesign revenue systems.

- This shift toward greater transparency, while beneficial for consumers, adds a layer of complexity and potential cost to game design and live service management.

Exclusive Technavio Analysis on Customer Landscape

The us video game market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us video game market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Video Game Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us video game market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apple Inc. - Analysis indicates key offerings encompass a diverse portfolio of interactive entertainment, from cinematic RPGs to competitive online titles, leveraging iconic franchises and new intellectual property.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apple Inc.

- BANDAI NAMCO Europe S.A.S

- Electronic Arts Inc.

- Embracer Group AB

- Epic Games Inc.

- Konami Group Corp.

- NEXON Co. Ltd.

- Nintendo Co. Ltd.

- Roblox Corp.

- Sega Corp.

- Sony Interactive Entertainment

- Square Enix Limited

- Take Two Interactive Software

- Ubisoft Entertainment SA

- Xbox Game Studios

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Movies and Entertainment industry, the widespread adoption of subscription-based streaming services has created a consumer expectation for on-demand access to large content libraries, directly accelerating the growth of video game subscription services and influencing player engagement.

- The increasing trend of leveraging major film and television intellectual properties to create interconnected transmedia universes has led to a surge in high-budget, narrative-driven video games designed to deepen brand immersion and capitalize on established fan bases.

- Heightened government regulation concerning digital content, consumer data privacy, and online advertising in the broader entertainment sector has set a precedent for the increasing regulatory scrutiny applied to video game monetization strategies and in-game economies.

- Persistent challenges with digital piracy and copyright enforcement have driven innovation in secure cloud-based distribution and digital rights management technologies, which are now foundational to the video game market's digital-first sales and live-service models.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Video Game Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 178 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.8% |

| Market growth 2026-2030 | USD 41.1 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.4% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The video game market in US operates as a complex ecosystem where casual gamers constitute over 70% of the player base, primarily engaging through mobile devices. The value chain begins with technology suppliers providing essential components like high-performance semiconductors and game engines, which are critical for achieving high-fidelity graphics.

- Publishers and developers, from large AAA studios to small indie developers, create the interactive content. This content is then delivered to consumers through a fragmented network of digital distribution storefronts and subscription services. The console segment, accounting for over 30% of hardware-related revenue, heavily influences hardware advancement cycles. Regulatory bodies are increasingly involved, shaping monetization strategies and ensuring consumer protection.

- The entire system is supported by a vibrant community of content creators and esports organizations that drive player engagement and long-term market vitality.

What are the Key Data Covered in this US Video Game Market Research and Growth Report?

-

What is the expected growth of the US Video Game Market between 2026 and 2030?

-

The US Video Game Market is expected to grow by USD 41.1 billion during 2026-2030, registering a CAGR of 13.8%. Year-over-year growth in 2026 is estimated at 12.4%%. This acceleration is shaped by growing demand for immersive experiences, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Platform (Mobile devices, Consoles, and Computing devices), Type (Offline, and Online), End-user (Casual gamers, Hardcore gamers, and Esports enthusiasts) and Geography (North America). Among these, the Mobile devices segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America. Country-level analysis includes US, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing demand for immersive experiences, which is accelerating investment and industry demand. The main challenge is content saturation reducing player engagement, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the US Video Game Market?

-

Key vendors include Apple Inc., BANDAI NAMCO Europe S.A.S, Electronic Arts Inc., Embracer Group AB, Epic Games Inc., Konami Group Corp., NEXON Co. Ltd., Nintendo Co. Ltd., Roblox Corp., Sega Corp., Sony Interactive Entertainment, Square Enix Limited, Take Two Interactive Software, Ubisoft Entertainment SA and Xbox Game Studios. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- With mobile gaming projected to capture over 44% of platform revenue, the competitive landscape is defined by a strategic push toward accessibility and cross-platform ecosystems. This focus has prompted major publishers such as Ubisoft Entertainment SA to align their development pipelines with cross-platform play, ensuring titles are available across console, PC, and mobile.

- These initiatives directly address the challenge of platform fragmentation, which can increase development costs by up to 15%. Other vendors, including hardware manufacturers, are introducing new gaming-specific product lines to capitalize on the growth of competitive gaming and esports.

- Such developments reflect a market-wide adaptation to evolving consumer behavior, where convenience, community, and continuous content are essential for capturing and retaining player engagement in a saturated entertainment environment.

We can help! Our analysts can customize this us video game market research report to meet your requirements.

RIA -

RIA -