Water And Wastewater Pipe Market Size 2026-2030

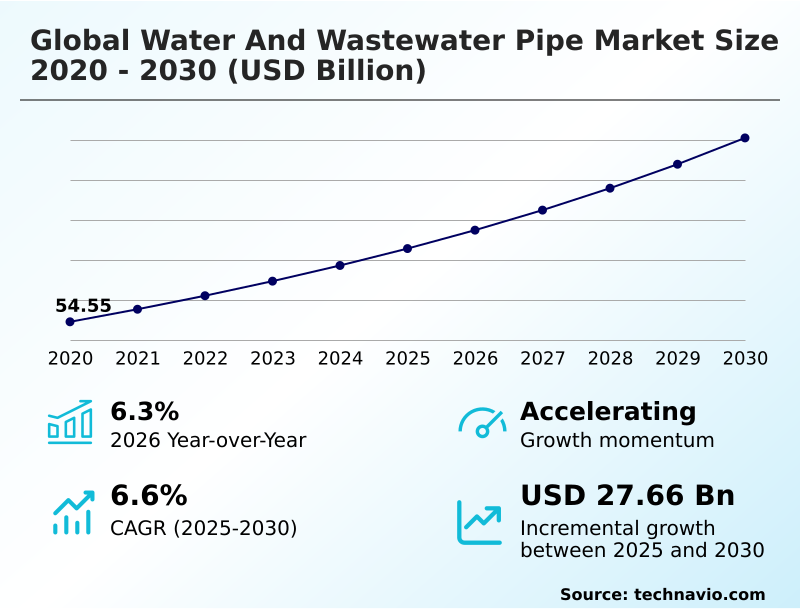

The water and wastewater pipe market size is valued to increase by USD 27.66 billion, at a CAGR of 6.6% from 2025 to 2030. Critical imperative for rehabilitating aging infrastructure will drive the water and wastewater pipe market.

Major Market Trends & Insights

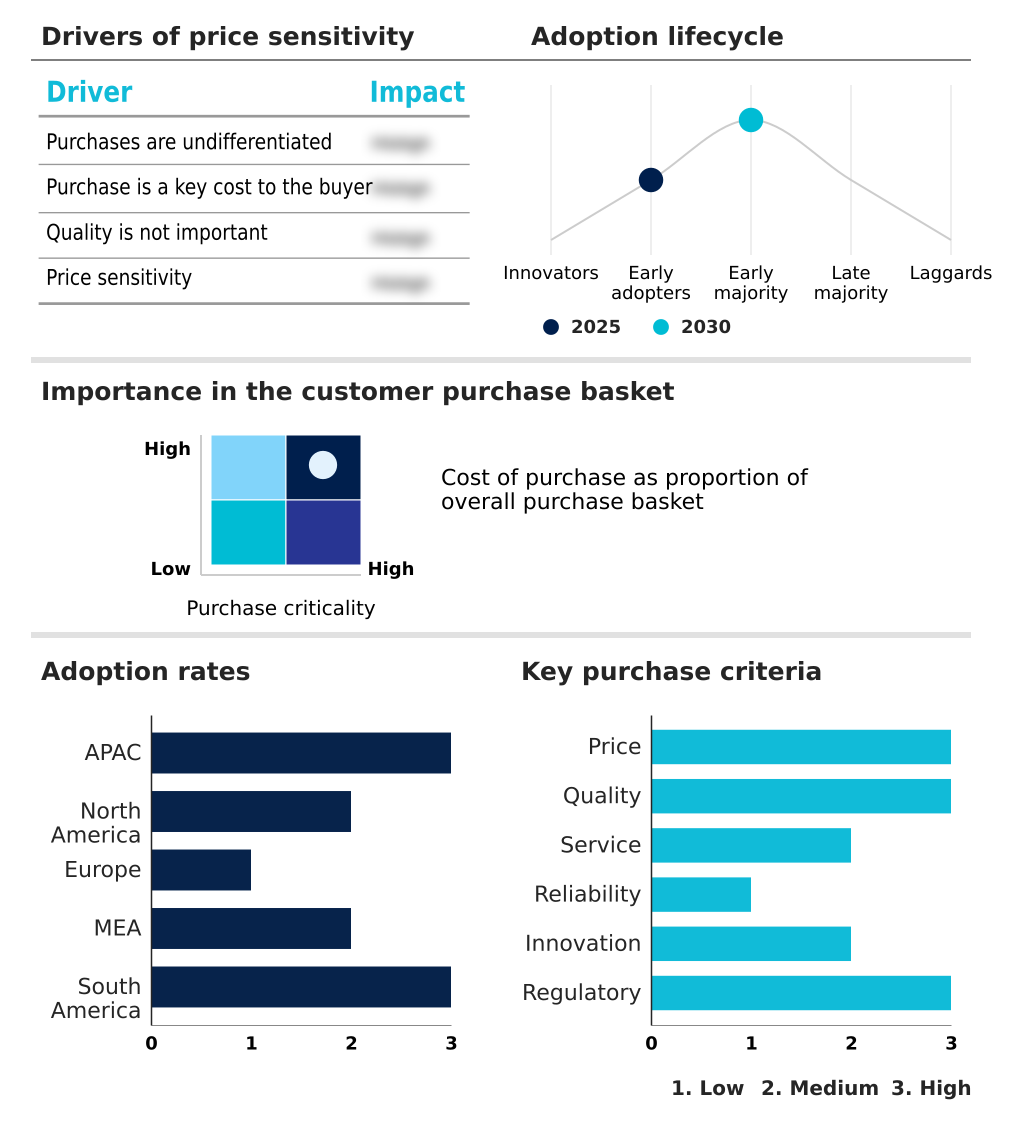

- APAC dominated the market and accounted for a 52.8% growth during the forecast period.

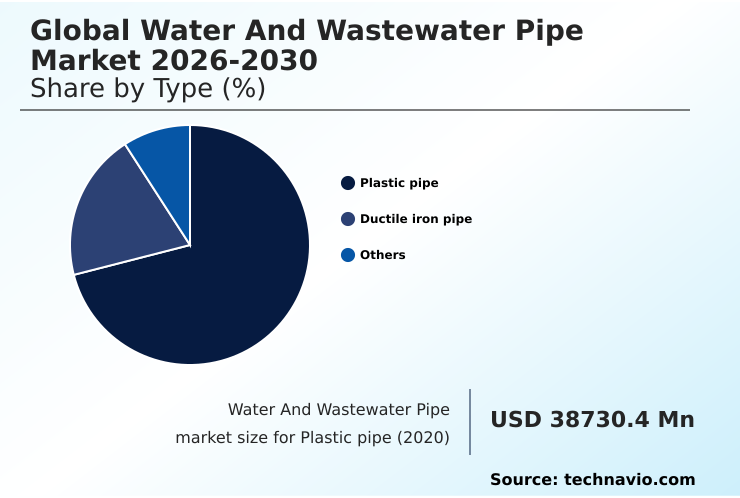

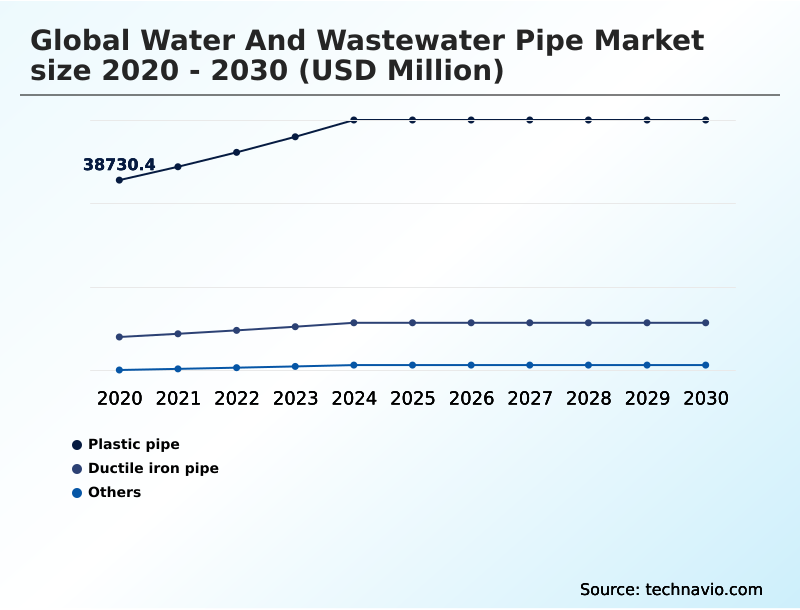

- By Type - Plastic pipe segment was valued at USD 49.42 billion in 2024

- By Application - Water supply and distribution segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 45.97 billion

- Market Future Opportunities: USD 27.66 billion

- CAGR from 2025 to 2030 : 6.6%

Market Summary

- The water and wastewater pipe market is fundamentally shaped by the dual imperatives of modernizing aging infrastructure and expanding service to growing urban populations. In developed economies, the focus is on pipe rehabilitation and replacement, addressing issues like non-revenue water and structural failures in decades-old water distribution networks.

- This drives demand for durable materials like ductile iron pipe and advanced solutions such as trenchless rehabilitation technologies. Conversely, in developing regions, relentless urbanization fuels greenfield infrastructure development, requiring the mass installation of new wastewater collection systems.

- Across all geographies, a prominent trend is the shift toward materials science, with high-density polyethylene (hdpe) and polyvinyl chloride (pvc) gaining favor for their corrosion resistance and ease of installation. For instance, a municipal utility facing budget constraints can leverage smart pipe technology for leak detection to build a digital twin for water networks.

- This allows for a proactive maintenance model, optimizing capital allocation by targeting the most critical segments for pipeline asset management and improving overall operational efficiency improvements.

What will be the Size of the Water And Wastewater Pipe Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Water And Wastewater Pipe Market Segmented?

The water and wastewater pipe industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Plastic pipe

- Ductile iron pipe

- Others

- Application

- Water supply and distribution

- Wastewater management

- End-user

- Municipal

- Industrial

- Agricultural

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The plastic pipe segment is estimated to witness significant growth during the forecast period.

The market is segmented by type, application, end-user, and geography, including key regions such as North America and Europe.

The plastic pipe segment, featuring materials like high-density polyethylene (HDPE) and polyvinyl chloride (PVC), is expanding its market share due to superior corrosion resistance and installation efficiencies.

The use of trenchless installation methods compatible with these materials significantly minimizes public disruption in dense urban environments. This approach to pipe rehabilitation has been shown to reduce project timelines by as much as 30% compared to traditional open-cut methods.

This efficiency, combined with lower lifecycle cost analysis, is driving adoption in both water distribution networks and wastewater collection systems, especially for lead service line replacement and managing sanitary sewer overflows.

The Plastic pipe segment was valued at USD 49.42 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Water And Wastewater Pipe Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the water and wastewater pipe market is sharply divided between rehabilitation-driven demand in mature economies and greenfield projects in developing nations.

Regions like North America and Europe focus on pipeline rehabilitation to address aging infrastructure, with government initiatives like the Bipartisan Infrastructure Law channeling funds into capital improvement programs.

In contrast, APAC accounts for over 52% of incremental growth, fueled by massive urbanization and the need to build out new urban water infrastructure.

In these greenfield projects, the use of lightweight plastic pipes can reduce transportation and handling costs by over 15% compared to traditional materials.

This demand is for foundational water distribution networks and wastewater collection systems to serve millions in new urban centers. This global dichotomy creates distinct opportunities, from high-specification, intelligent piping solutions in developed markets to cost-effective, scalable systems in high-growth regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Modern pipeline asset management for utilities requires a sophisticated approach, starting with comparing hdpe and ductile iron pipes for different pressure and soil conditions. For critical public health initiatives, selecting appropriate lead service line replacement materials is paramount.

- The decision to use hdpe pipe for trenchless installation in dense urban areas is often driven by the need to minimize disruption and cost. For wastewater applications, understanding the long-term corrosion resistance in wastewater pipes is key, sometimes leading to the specification of vcp for aggressive sewer environments.

- Meanwhile, the integration of smart pipe technology for leak detection is becoming standard for improving pressure management in distribution networks and managing non-revenue water with technology. However, the impact of raw material costs remains a persistent issue, creating significant funding challenges for water infrastructure projects.

- Planners also evaluate grp for large diameter pipelines and consider ductile iron pipe seismic performance in vulnerable zones. To advance the role of pipes in circular economy, designing dual-pipeline systems for water reuse is gaining traction.

- The adoption of trenchless technology for urban areas is not just a trend but a necessity, with projects leveraging these methods often seeing completion schedules shortened by 10-15% compared to traditional open-trench methods. Innovations in pipe jointing technology further enhance system integrity, making it a crucial element in future-proofing water networks.

What are the key market drivers leading to the rise in the adoption of Water And Wastewater Pipe Industry?

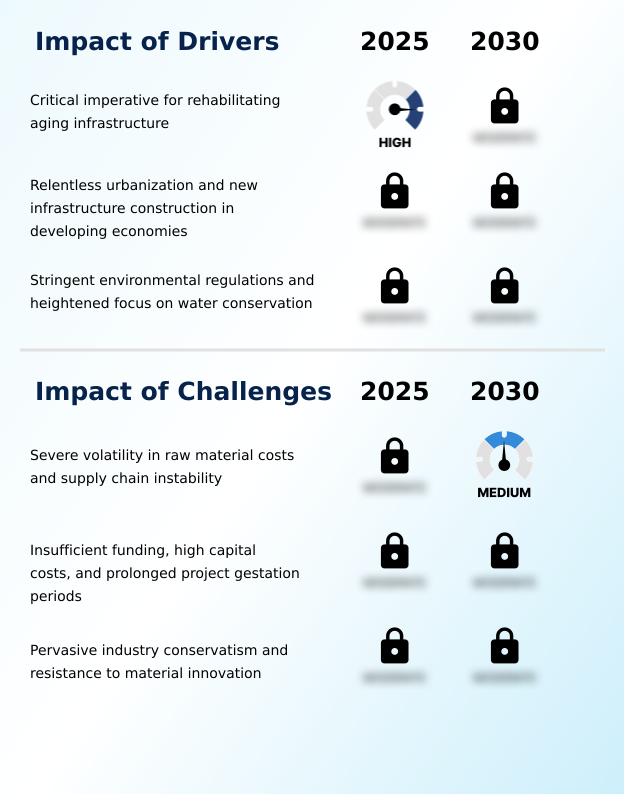

- The critical imperative to rehabilitate aging and deteriorating water and wastewater infrastructure stands as a primary market driver.

- Market growth is propelled by the non-negotiable need for aging infrastructure replacement and large-scale greenfield infrastructure development. In developed nations, capital improvement programs are focused on replacing deteriorating pipelines to enhance system reliability and comply with stringent environmental regulations.

- In rapidly urbanizing regions, demand for foundational urban water infrastructure is increasing by double-digits annually in some cities, creating a massive requirement for new water conveyance systems.

- Stricter environmental regulations compliance is also compelling investment, with mandates to reduce sanitary sewer overflows by up to 90% in certain watersheds.

- These public works projects, often backed by long-term infrastructure investment, provide a stable and predictable demand stream for a wide range of pipe products, from potable water distribution lines to large-diameter sewer mains.

What are the market trends shaping the Water And Wastewater Pipe Industry?

- The accelerated adoption of plastic and composite piping solutions is a key trend. This shift is driven by their superior performance characteristics and lifecycle cost advantages over traditional materials.

- A primary trend is the pronounced shift in pipe material science toward advanced composite materials and high-performance plastics. This evolution is driven by a focus on long-term performance and lower lifecycle costs. The adoption of intelligent piping solutions is also accelerating, transforming passive networks into responsive assets.

- The integration of smart sensors into pipelines has enabled some utilities to pinpoint leaks with 98% accuracy, drastically reducing water loss. Concurrently, the development of dual-pipeline systems is becoming central to the implementation of a circular water economy, with recycled water infrastructure representing a significant new growth area.

- These purple pipe systems, which keep non-potable recycled water separate, are now a standard requirement in many new urban developments, with adoption rates in water-stressed regions increasing by over 20% in recent years.

What challenges does the Water And Wastewater Pipe Industry face during its growth?

- Severe volatility in raw material costs, coupled with ongoing supply chain instability, presents a significant challenge to market growth and profitability.

- The market faces persistent headwinds from raw material price volatility, which can swing project costs by as much as 20% within a single fiscal year, disrupting financial planning for manufacturers and public utilities alike. This is compounded by supply chain instability, which can delay projects and increase operational expenses.

- Furthermore, systemic issues such as insufficient funding and the long gestation periods of public works projects create an unpredictable demand cycle. Industry conservatism also presents a barrier; the approval process for innovative materials can be three to five times longer than for traditional products, slowing the adoption of technologies that could offer significant long-term benefits.

- These factors collectively constrain growth and pressure profit margins across the sector.

Exclusive Technavio Analysis on Customer Landscape

The water and wastewater pipe market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the water and wastewater pipe market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Water And Wastewater Pipe Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, water and wastewater pipe market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Drainage Systems Inc - Offerings include essential conduits for water supply and wastewater management, forming the critical infrastructure for municipal, industrial, and agricultural fluid transportation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Drainage Systems Inc

- Aliaxis Holdings SA

- Astral Ltd.

- China Lesso Group Holdings

- Geberit International AG

- Georg Fischer Ltd.

- ISCO Industries, Inc.

- JM Eagle Inc.

- Logan Clay Products LLC

- McWane Inc.

- Mueller Water Products Inc

- Nippon Steel Corp.

- Northwest Pipe Co

- Pipelife International GmbH

- Saudi Arabian Amiantit Co.

- Sekisui Chemical Co. Ltd.

- Tata Steel Ltd.

- Tenaris SA

- Tessenderlo Group NV

- Wavin BV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Water and wastewater pipe market

- In May, 2025, Georg Fischer Ltd. announced the acquisition of a specialized European smart valve manufacturer, expanding its portfolio of intelligent piping solutions for proactive pressure management systems in urban water infrastructure.

- In March, 2025, Advanced Drainage Systems Inc. completed construction of a new manufacturing plant in the southeastern US, increasing its production capacity for HDPE pipes by 20% to meet escalating demand from municipal capital improvement programs.

- In January, 2025, the European Investment Bank launched a multi-billion euro fund aimed at accelerating lead service line replacement and upgrading wastewater collection systems across member states, directly driving demand for modern pipe materials.

- In October, 2024, Aliaxis Holdings SA introduced a new line of PVC pipes featuring integrated fiber optic sensing capabilities, designed for real-time leak detection and enhanced pipeline integrity management in water distribution networks.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Water And Wastewater Pipe Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.6% |

| Market growth 2026-2030 | USD 27656.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.3% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The water and wastewater pipe market is undergoing a significant transformation, moving beyond the supply of passive conduits to providing integrated systems for intelligent water management. Core components like ductile iron pipe, high-density polyethylene (hdpe), and polyvinyl chloride (pvc) are now being enhanced with advanced technologies.

- The deployment of a digital twin for water networks, fed by data from fiber optic sensing and other leak detection systems, is a critical boardroom-level consideration, directly influencing capital allocation for pipeline asset management. Utilities deploying these technologies have reported a reduction in unplanned downtime by over 30%.

- This evolution is redefining the value proposition, where materials like glass reinforced plastic (grp), pre-stressed concrete cylinder pipe (pccp), and vitrified clay pipe (vcp) are selected based on their performance within a managed system.

- Innovations such as geohazard resistant steel pipe and seismic resistant pipes address specialized environmental risks, while technologies like pipe bursting technology and trenchless installation offer less disruptive methods for pipe rehabilitation.

- This shift demands a focus on holistic solutions, including cement mortar lining for durability and advanced push-on joint systems or heat fusion jointing for ensuring the integrity of water distribution networks and wastewater collection systems.

What are the Key Data Covered in this Water And Wastewater Pipe Market Research and Growth Report?

-

What is the expected growth of the Water And Wastewater Pipe Market between 2026 and 2030?

-

USD 27.66 billion, at a CAGR of 6.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Plastic pipe, Ductile iron pipe, and Others), Application (Water supply and distribution, and Wastewater management), End-user (Municipal, Industrial, and Agricultural) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Critical imperative for rehabilitating aging infrastructure, Severe volatility in raw material costs and supply chain instability

-

-

Who are the major players in the Water And Wastewater Pipe Market?

-

Advanced Drainage Systems Inc, Aliaxis Holdings SA, Astral Ltd., China Lesso Group Holdings, Geberit International AG, Georg Fischer Ltd., ISCO Industries, Inc., JM Eagle Inc., Logan Clay Products LLC, McWane Inc., Mueller Water Products Inc, Nippon Steel Corp., Northwest Pipe Co, Pipelife International GmbH, Saudi Arabian Amiantit Co., Sekisui Chemical Co. Ltd., Tata Steel Ltd., Tenaris SA, Tessenderlo Group NV and Wavin BV

-

Market Research Insights

- Market dynamics are increasingly influenced by a strategic pivot toward long-term asset management strategy and sustainability. The focus on aging infrastructure replacement is driving significant capital improvement programs, with project approvals often contingent on lifecycle cost analysis. This favors materials and technologies that promise extended service life and operational efficiency improvements.

- For example, adopting leak-free jointing systems has been shown to reduce physical water losses by up to 25% in rehabilitated zones. Concurrently, the push for a circular water economy is creating new demand for specialized pipeline networks.

- A shift toward proactive maintenance models, enabled by intelligent piping solutions, has lowered emergency repair costs by 40% for some utilities, underscoring the financial benefits of long-term infrastructure investment and environmental regulations compliance.

We can help! Our analysts can customize this water and wastewater pipe market research report to meet your requirements.

RIA -

RIA -