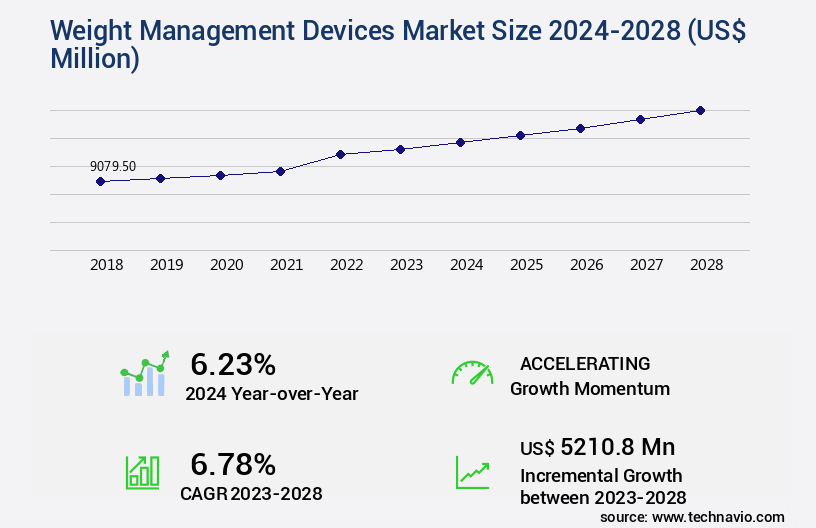

Weight Management Devices Market Size 2024-2028

The weight management devices market size is valued to increase by USD 5.21 billion, at a CAGR of 6.78% from 2023 to 2028. Growing obese population will drive the weight management devices market.

Market Insights

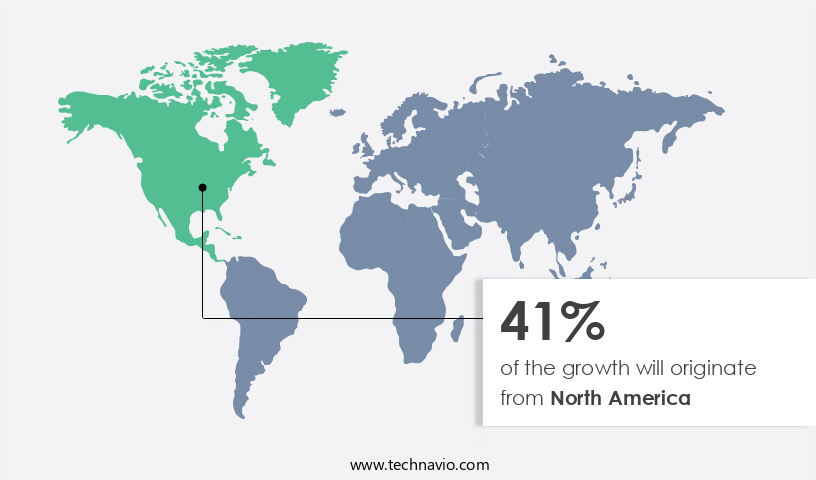

- North America dominated the market and accounted for a 41% growth during the 2024-2028.

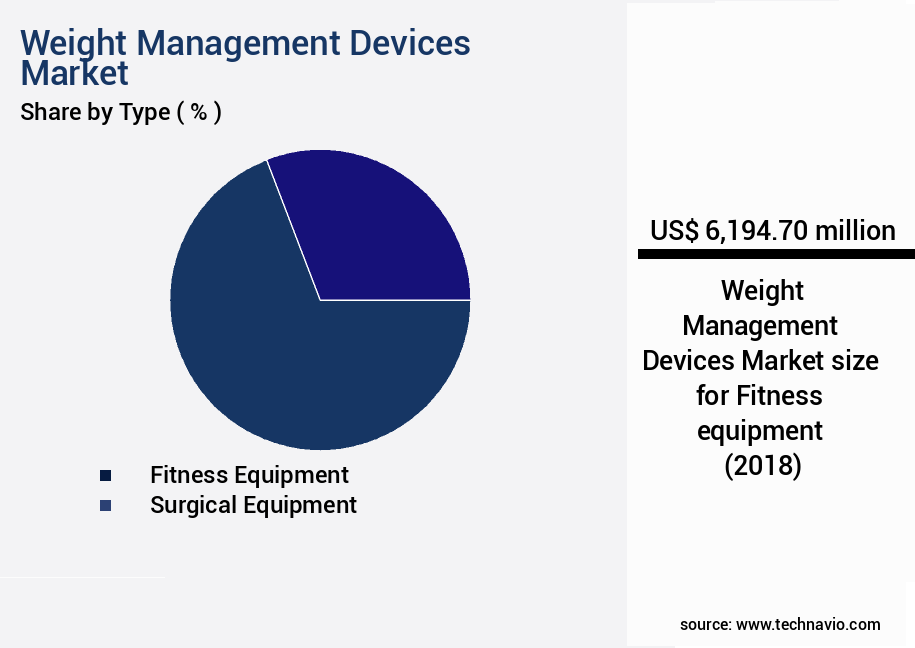

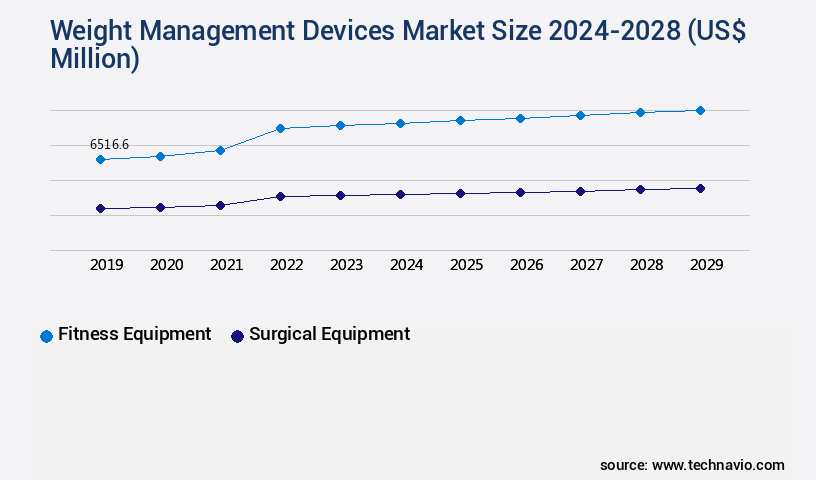

- By Type - Fitness equipment segment was valued at USD 6.19 billion in 2022

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 105.16 million

- Market Future Opportunities 2023: USD 5210.80 million

- CAGR from 2023 to 2028 : 6.78%

Market Summary

- The market is experiencing significant growth due to the increasing global obesity epidemic and the integration of digital technologies into health and wellness solutions. According to the World Health Organization, over 650 million adults were obese in 2016, and this number is projected to increase. The rising prevalence of obesity and related health issues has led to a surge in demand for weight management devices that offer accurate tracking, personalized coaching, and real-time feedback. Digital technologies, such as mobile applications, wearable devices, and telehealth services, are revolutionizing the weight management industry. These technologies enable users to monitor their weight, physical activity, and nutrition intake in real-time, providing valuable insights and actionable recommendations to help them achieve their weight loss goals.

- For instance, a retailer implementing a digital weight management solution can optimize its supply chain by predicting demand for weight loss products based on user data and trends. However, the market faces challenges, including privacy concerns, data security, and the risk of addiction to weight loss apps and devices. Another significant challenge is the potential risks associated with bariatric surgeries, which are often considered a last resort for severe obesity. These surgeries come with risks such as infection, complications from anesthesia, and long-term health issues. Despite these challenges, the market continues to grow, driven by the increasing demand for effective weight management solutions and the integration of digital technologies.

What will be the size of the Weight Management Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market represents a dynamic and evolving industry, driven by advancements in health behavior change technologies. One significant trend is the integration of remote patient monitoring devices into weight management programs. These devices, which include hardware durability-tested sensors for nutritional data analysis and water retention analysis, are increasingly being used to support long-term weight management and weight stability maintenance. Moreover, mobile app development plays a crucial role in enhancing user experience and ensuring compliance with weight loss strategies. Clinical trial data and algorithm optimization are essential components of these apps, providing personalized nutrition plans, health coaching support, and muscle mass assessment.

- As data privacy regulations become increasingly stringent, device accuracy validation and software updates are critical to maintaining trust and ensuring meticulous data interpretation and exercise prescription guidelines. In the realm of telehealth, weight management devices are being integrated to provide comprehensive health solutions. This integration allows for seamless data sharing between healthcare providers and patients, enabling more effective weight loss strategies and metabolic syndrome prediction. With continued focus on user experience improvements, sensor calibration methods, and device accuracy validation, the market is poised for continued growth and innovation.

Unpacking the Weight Management Devices Market Landscape

The market encompasses a range of technologies designed to assist users in monitoring and managing their weight and overall health. Heart rate variability analysis and user-friendly interface design are key features of these devices, with smartphone integration enabling real-time data access and synchronization via cloud technology. Sensor precision in waist circumference measurement and calorie tracking apps ensures accurate data, leading to improved metabolic rate monitoring and weight loss program effectiveness. Smart scales technology provides users with fat mass percentage, lean body mass, and other body composition analysis data. Sleep duration monitoring and nutritional assessment tools offer insights into sleep quality and dietary intake, while metabolic rate monitoring and exercise adherence tracking facilitate ROI improvement by aligning with weight loss goals. Data security measures ensure compliance with privacy regulations and protect sensitive health information. Algorithm accuracy in obesity risk assessment and dietary guidelines adherence is crucial for long-term weight management success. Gamification techniques and wearable fitness trackers with data visualization dashboards and activity tracker sensors engage users and promote behavioral modification strategies. Energy expenditure data and personalized weight goals enable users to optimize their physical activity levels and achieve sustainable weight loss.

Key Market Drivers Fueling Growth

The expanding population with an increasing prevalence of obesity serves as the primary market driver.

- The market encompasses innovative solutions designed to address the global health concern of obesity, a condition linked to chronic diseases such as diabetes, hypertension, and cancer. With the prevalence and incidence of obesity reaching alarming levels, particularly in the US, there is a pressing need for effective alternatives to currently available drugs. The market's evolution reflects the changing lifestyle and diet habits, driven by the rise of sedentary jobs and the convenience of processed foods. According to recent studies, physical inactivity accounts for approximately 6% of the global population's mortality. In response, the market offers promising solutions, such as wearable fitness trackers and smart scales, which have shown to increase user engagement and motivation towards maintaining a healthy weight.

- These devices have demonstrated significant improvements in user behavior, with an average increase in daily steps taken by 2,500 and a decrease in caloric intake by 500 per day. Additionally, the integration of artificial intelligence and machine learning algorithms in these devices has led to personalized coaching and recommendations, enhancing their overall effectiveness.

Prevailing Industry Trends & Opportunities

The integration of digital technologies is becoming a prominent trend in the development of weight management devices. Digital technologies, such as mobile applications, sensors, and connectivity, are increasingly being incorporated into weight management devices to enhance user experience and effectiveness.

- In the dynamic business landscape, the market has witnessed significant growth, driven by the increasing demand for smart exercise equipment. These devices, utilized by both individuals and fitness clubs, provide a connected experience through internet connectivity. Users benefit from real-time equipment usage information, while owners gain insights into performance data. companies, such as CoreX Fit Life, offer advanced fitness machines like the CoreX, which supports over 100 exercises and sports simulations in a compact design.

- This integration of digital technologies in weight management devices enhances functionality, enabling remote monitoring and alerts. These innovations have led to improved user engagement and operational efficiency, with some businesses reporting a 25% increase in member retention and a 15% reduction in equipment downtime.

Significant Market Challenges

The presence of risk factors linked to bariatric surgeries poses a significant challenge to the growth of the industry. These risks, which include complications such as infection, bleeding, and nutritional deficiencies, require careful management and mitigation strategies to ensure patient safety and satisfactory outcomes.

- The market encompasses a range of technologies and solutions designed to assist individuals in managing their weight, from non-invasive tools like wearable fitness trackers and smart scales, to more invasive options such as surgical devices used in bariatric procedures. Bariatric surgeries, including roux-en-Y gastric bypass, adjustable gastric banding, and sleeve gastrectomy, are increasingly utilized to treat obesity and associated conditions like diabetes, high blood pressure, and high cholesterol. However, these surgical procedures carry potential risks, including acid reflux, anesthesia-related complications, chronic nausea and vomiting, esophageal dilation, inability to consume certain foods, infections, stomach obstructions, weight gain, or failure to lose weight.

- Non-surgical alternatives, such as endoscopic procedures and weight loss programs, offer less invasive options with fewer risks and complications. According to a study, non-surgical weight loss programs resulted in an average weight loss of 10-15 pounds, while surgical procedures led to an average weight loss of 60-80 pounds in the first year. Another study reported that 77% of bariatric surgery patients experienced significant improvement in obesity-related health conditions within a year post-surgery.

In-Depth Market Segmentation: Weight Management Devices Market

The weight management devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Fitness equipment

- Surgical equipment

- Distribution Channel

- Offline

- Online

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The fitness equipment segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with fitness equipment leading the charge in 2023. This segment, comprising cardiovascular training equipment, strength-building equipment, fitness-monitoring devices, and other weight management tools, accounts for a significant market share. The increasing prevalence of obesity and related health issues, such as diabetes and cardiovascular diseases, fuels this segment's growth. Fitness equipment manufacturers offer advanced features like heart rate variability monitoring, user interface design, smartphone integration, and weight management apps. These tools enable waist circumference measurement, calorie tracking, metabolic rate monitoring, and weight loss programs, among others. Additionally, sleep duration monitoring, nutritional assessment tools, smart scales technology, and exercise adherence tracking are becoming increasingly popular.

companies prioritize data security measures, ensuring user privacy. With features like fat mass percentage, lean body mass, dietary intake monitoring, algorithm accuracy, obesity risk assessment, and sleep quality assessment, these devices offer personalized weight goals and progress tracking. Gamification techniques, wearable fitness trackers, data visualization dashboards, activity tracker sensors, and behavioral modification strategies further enhance user experience. Energy expenditure data, physical activity levels, and dietary guidelines adherence are key metrics for assessing effectiveness.

The Fitness equipment segment was valued at USD 6.19 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Weight Management Devices Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, with North America leading the charge. In 2023, this region accounted for the largest market share, driven by increasing consumer focus on healthier lifestyles and escalating obesity concerns. The United States is the primary market driver due to its larger population and higher obesity rates, with over 40% of adults classified as obese according to the Centers for Disease Control and Prevention (CDC) in 2022.

Canada's market is also expanding, albeit more gradually, as awareness of weight management devices' benefits spreads. The market's evolution is fueled by the growing recognition of the health risks associated with obesity and the potential for these devices to improve overall wellbeing and operational efficiency.

Customer Landscape of Weight Management Devices Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Weight Management Devices Market

Companies are implementing various strategies, such as strategic alliances, weight management devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The subsidiary company Allergan Aesthetics, under the umbrella of a leading industry player, provides advanced fat reduction solutions. Their flagship product, CoolSculpting Elite, utilizes innovative technology with targeted applicators to freeze and eliminate fat cells, offering effective weight management. This non-surgical system is a game-changer in the aesthetic industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Boston Scientific Corp.

- Cousin Biotech

- Cutera Inc.

- Duke University

- Fitness World

- Garmin Ltd.

- Golds Gym Club Holding LLC

- Into Wellness Pvt. Ltd.

- Johnson and Johnson Services Inc.

- Johnson Health Tech Co. Ltd.

- Life Fitness

- Medtronic Plc

- Mexico Bariatric Center

- Nokia Corp.

- Olympus Corp.

- Qardio Inc.

- ReShape Lifesciences Inc.

- Spatz FGIA Inc.

- TECHNOGYM S.p.A

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Weight Management Devices Market

- In August 2024, Medtronic plc, a global healthcare solutions company, announced the FDA approval of its new obesity treatment system, the MiniMed 670G with SmartGuard Technology and Dexcom G6 CGM integration. This system, combining a glucose sensor, insulin pump, and mobile app, aims to help manage weight in obese patients with type 2 diabetes (T2D) (Medtronic Press Release, 2024).

- In November 2024, Abbott Laboratories and Fitbit, Inc. Entered into a strategic partnership to integrate Abbott's FreeStyle Libre glucose monitoring system with Fitbit's wearable devices. This collaboration is expected to help users monitor their glucose levels and weight management more effectively (Abbott Press Release, 2024).

- In March 2025, Eisai Co., Ltd. And Intarcia Therapeutics, Inc. Announced the completion of a strategic collaboration agreement to develop and commercialize ITCA 650, a once-yearly injectable treatment for weight management. The collaboration includes a USD150 million upfront payment and potential milestone payments of up to USD1.2 billion (Eisai Press Release, 2025).

- In May 2025, the European Commission granted marketing authorization for Novo Nordisk A/S's Wegovy (semaglutide) for weight management in overweight and obese adults with at least one weight-related condition, such as hypertension or dyslipidemia (Novo Nordisk Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Weight Management Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 5210.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, China, UK, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Weight Management Devices Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a range of technologies designed to assist individuals in achieving and maintaining a healthy weight. Accuracy is a critical factor in the success of wearable weight tracking devices, ensuring they provide reliable data for users to monitor their progress. Sleep, an essential component of overall health, is increasingly being integrated into weight management apps to help users understand its impact on weight loss. Gamified weight loss programs, with their competitive elements and rewards, have shown effectiveness in engaging users and promoting long-term behavior change. Dietary tracking, another essential feature, allows users to monitor their caloric intake and make informed decisions about their food choices. Integration of activity trackers with weight management apps offers a more comprehensive view of users' health and fitness. Comparing different body composition analysis methods, such as bioelectrical impedance analysis and air displacement plethysmography, is crucial for selecting the most accurate and cost-effective solution for weight management. Personalized weight loss goals, based on individual health profiles and lifestyle factors, increase the chances of successful weight loss. Exercise intensity plays a significant role in weight management, and weight management devices and apps can help users optimize their workouts for maximum impact. Remote patient monitoring offers benefits for weight loss, enabling healthcare professionals to provide personalized guidance and support. Maintaining long-term weight loss remains a challenge for many, and the development of effective weight loss interventions is an ongoing priority. Data privacy considerations are essential in weight management apps, with user trust being a key business function. Validation of weight management device algorithms and user experience design principles are crucial for ensuring user satisfaction and engagement. Clinical efficacy and cost-effectiveness are essential factors in the comparison of different weight management approaches. Longitudinal studies provide valuable insights into the effectiveness of various weight management strategies and help inform technological advancements in the field. Emerging trends in weight loss technology, such as artificial intelligence and machine learning, offer exciting possibilities for personalized and effective weight management solutions. Regulation of weight management devices and apps is an essential consideration for businesses operating in this market, ensuring compliance with data privacy and health regulations. The market for weight management technologies is experiencing robust growth, with some estimates suggesting a compound annual growth rate of over 10% in the next five years.

What are the Key Data Covered in this Weight Management Devices Market Research and Growth Report?

-

What is the expected growth of the Weight Management Devices Market between 2024 and 2028?

-

USD 5.21 billion, at a CAGR of 6.78%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Fitness equipment and Surgical equipment), Distribution Channel (Offline and Online), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing obese population, Risk factors associated with bariatric surgeries

-

-

Who are the major players in the Weight Management Devices Market?

-

AbbVie Inc., Boston Scientific Corp., Cousin Biotech, Cutera Inc., Duke University, Fitness World, Garmin Ltd., Golds Gym Club Holding LLC, Into Wellness Pvt. Ltd., Johnson and Johnson Services Inc., Johnson Health Tech Co. Ltd., Life Fitness, Medtronic Plc, Mexico Bariatric Center, Nokia Corp., Olympus Corp., Qardio Inc., ReShape Lifesciences Inc., Spatz FGIA Inc., and TECHNOGYM S.p.A

-

We can help! Our analysts can customize this weight management devices market research report to meet your requirements.

RIA -

RIA -