Adtech Market Size 2025-2029

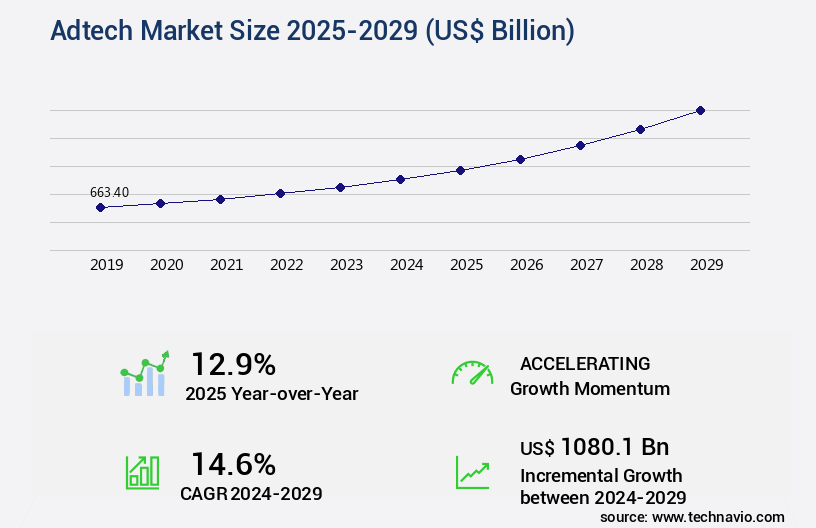

The adtech market size is valued to increase USD 1080.1 billion, at a CAGR of 14.6% from 2024 to 2029. Increasing Internet and smartphone penetration will drive the adtech market.

Major Market Trends & Insights

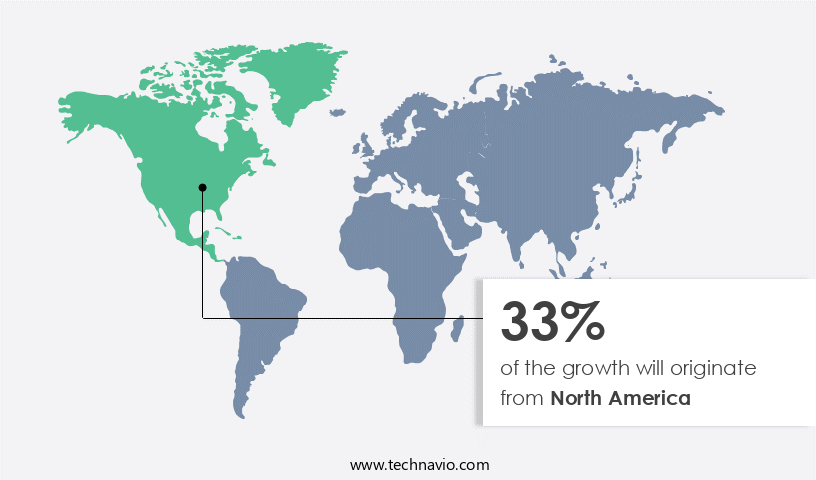

- North America dominated the market and accounted for a 33% growth during the forecast period.

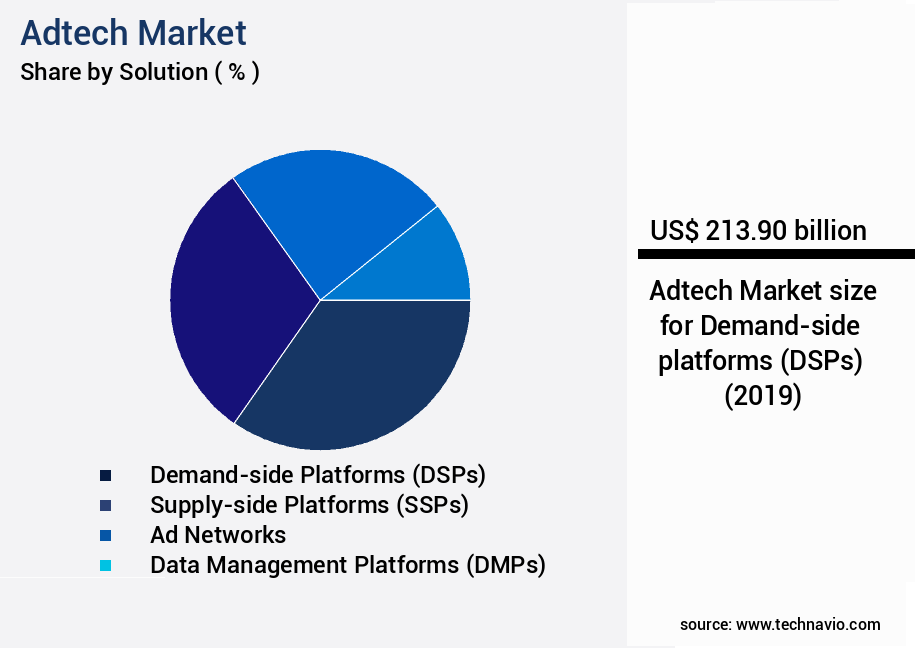

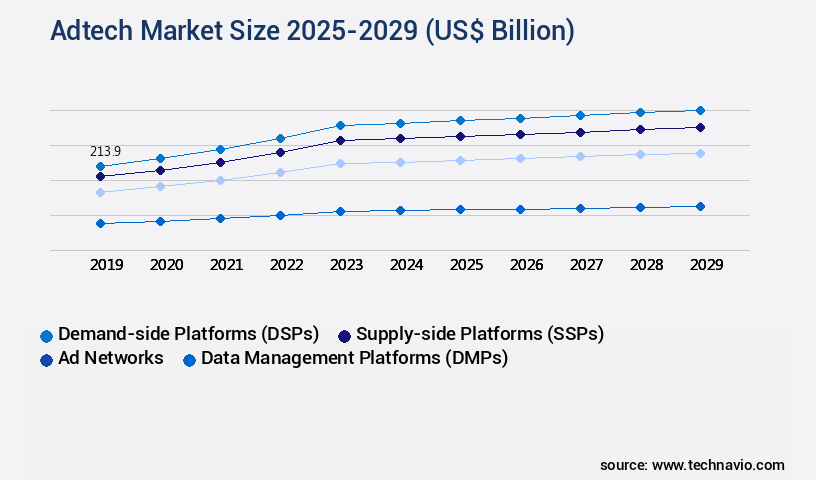

- By Solution - Demand-side platforms (DSPs) segment was valued at USD 213.90 billion in 2023

- By Platform - Mobile Ad segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 229.45 billion

- Market Future Opportunities: USD 1080.10 billion

- CAGR : 14.6%

- North America: Largest market in 2023

Market Summary

- The market represents a dynamic and continually evolving landscape, driven by the integration of advanced technologies and shifting consumer behaviors. Core technologies, such as AI and machine learning (ML), are increasingly shaping the industry, enabling targeted advertising, personalized content delivery, and advanced analytics. Meanwhile, applications of these technologies span various sectors, including digital advertising, programmatic advertising, and mobile advertising. Despite these opportunities, the market faces challenges, including the growing adoption of ad-blocker solutions and heightened regulatory scrutiny.

- In this context, the market is poised for ongoing transformation, with increasing Internet and smartphone penetration fueling demand for more sophisticated and personalized advertising solutions. As of 2021, approximately 67% of the global population uses the Internet, and this number is projected to reach 75% by 2025. The market's evolution underscores the importance of staying informed about the latest trends, regulations, and technologies shaping the Adtech landscape.

What will be the Size of the Adtech Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Adtech Market Segmented and what are the key trends of market segmentation?

The adtech industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Solution

- Demand-side platforms (DSPs)

- Supply-side platforms (SSPs)

- Ad networks

- Data management platforms (DMPs)

- Others

- Platform

- Mobile Ad

- Desktop Ad

- Digital TV

- End-User

- Retail & E-Commerce

- BFSI

- Media & Entertainment

- Healthcare

- Others

- Deployment Type

- Cloud-Based

- On-Premises

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Solution Insights

The demand-side platforms (DSPs) segment is estimated to witness significant growth during the forecast period.

The market trends encompass various aspects, including brand safety, display advertising, contextual targeting, programmatic advertising, attribution modeling, predictive modeling, native advertising, search engine marketing, conversion tracking, campaign management, A/B testing, ad fraud detection, mobile advertising, social media advertising, supply-side platforms, ad networks, data analytics, cost per click, video advertising, real-time bidding, demand-side platforms, click-through rates, ad exchange platforms, ad servers, creative optimization, data management platforms, behavioral targeting, impression metrics, ad verification, and audience targeting. Programmatic advertising platforms, such as Demand-Side Platforms (DSPs), are transforming the industry by enabling advertisers to automate their ad buying process. DSPs facilitate mobile advertising, allowing marketers to purchase high-quality traffic at scale with minimal effort.

This automation saves time and resources, enabling user acquisition professionals to focus on optimizing user segments for improved long-term performance. The adoption of programmatic advertising has seen significant growth, with 78% of US digital display ad spending transacted programmatically in 2020. Furthermore, the programmatic video advertising market is projected to reach USD 50.18 billion by 2023, growing at a steady pace. The integration of data analytics, real-time bidding, and automation in ad buying processes is driving this growth. Additionally, the mobile advertising sector is experiencing rapid expansion, with mobile ad spending surpassing desktop ad spending for the first time in 2016.

The Demand-side platforms (DSPs) segment was valued at USD 213.90 billion in 2019 and showed a gradual increase during the forecast period.

By 2021, mobile advertising is expected to account for 72% of all digital ad spending. Social media advertising is another key segment, with 90% of marketers using social media for advertising, and 71% of consumers more likely to make a purchase based on social media referrals. As businesses continue to leverage technology to reach their target audiences more effectively, the market will continue to evolve, offering new opportunities for growth and innovation.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Adtech Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant growth due to the widespread use of smartphones and robust broadband infrastructure. Mobile ad spending is a major driver, as consumers increasingly engage with digital content on mobile devices. According to recent statistics, mobile ad spending in the region reached USD 50.47 billion in 2020, representing a 22.2% share of total digital ad spending. Furthermore, manufacturers are expected to increase their investments in internet advertising, as digital/online advertising proves to be more economical compared to traditional options.

In 2021, digital ad spending in North America is projected to reach USD 129.34 billion, with mobile accounting for approximately USD 72.22 billion. These trends reflect the continuous evolution of the market and its increasing importance for businesses in the region.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and intricate ecosystem that facilitates real-time bidding strategies for mobile advertising and effective programmatic direct campaign management. This marketplace is characterized by the implementation of header bidding for increased yield, addressing data privacy regulations and ad tech compliance. Cross-device tracking solutions are a crucial aspect, enabling enhanced targeting and improving return on investment through attribution modeling techniques. Advanced analytics for programmatic advertising optimization and openRTB protocol implementation bring benefits, such as automated bidding strategies for performance marketing. Ad fraud detection and prevention techniques are essential to maintain trust and transparency, while creative optimization strategies contribute to improved click-through rates.

Audience segmentation and targeting are key to effective campaigns, and advanced campaign reporting and analysis tools provide valuable insights. Supply-side platform integration for publishers and demand-side platform selection criteria are critical considerations. Data management platform implementation brings numerous benefits, including streamlined ad server management and optimization. Viewability metrics and improvement strategies are essential for maximizing ad impact, with brand safety guidelines and implementation ensuring a positive user experience. Performance-based advertising strategies are on the rise, with more than 60% of marketers adopting this approach compared to traditional cost-per-click models. This shift underscores the importance of adtech in delivering targeted, measurable, and effective advertising solutions.

What are the key market drivers leading to the rise in the adoption of Adtech Industry?

- The significant expansion of Internet and smartphone usage is the primary catalyst fueling market growth.

- The market has experienced significant expansion as Internet and smartphone penetration increases globally. With more people gaining access to these technologies, adtech platforms have become increasingly convenient for both buyers and sellers. This trend is driven by the growing number of individuals using smartphones to browse and post ads. In response, adtech platform providers have invested heavily in mobile applications to cater to this demographic. The continuous advancement of technology further fuels this growth, as users seek more targeted and personalized advertising experiences.

- This dynamic market is characterized by ongoing innovation and evolving patterns, making it a highly competitive and rapidly changing landscape. Adtech platforms have become essential tools for businesses looking to reach and engage with their audiences effectively. The market is expected to continue growing as technology progresses and Internet and smartphone penetration increases further.

What are the market trends shaping the Adtech Industry?

- The integration of artificial intelligence (AI) and machine learning (ML) is an emerging market trend.

- The integration of artificial intelligence (AI) and machine learning in adtech platforms is a significant trend, enhancing search results, suggesting relevant listings, and automating various functions. AI algorithms analyze user behavior, preferences, and search history to offer personalized ad and product recommendations. Machine learning optimizes ad targeting and pricing based on user engagement and conversion rates. This technology-driven approach boosts user experience, competitiveness, and attracts more users and advertisers, fueling the expansion of the market. AI's role in adtech is continuously evolving, with applications extending to fraud detection, ad placement, and content generation.

- This technological shift is transforming the industry, making adtech platforms more efficient and responsive to user needs. Adoption rates vary across sectors, with digital media, e-commerce, and marketing leading the way. This data-driven narrative underscores the importance of AI in adtech and its potential impact on the business landscape.

What challenges does the Adtech Industry face during its growth?

- The increasing utilization of ad-blocking technologies poses a significant challenge to the expansion of the industry, as more users opt to restrict or eliminate advertisements from their online experiences.

- The market faces a significant challenge with the escalating usage of ad-blocking technologies. According to recent studies, the number of ad-blocker users worldwide is projected to reach 750 million by 2025, representing a substantial increase from the current figure. This trend poses a significant threat to the adtech industry, as it impedes advertisers' ability to reach their target audiences and negatively impacts publishers' revenue streams. Ad-blockers' popularity stems from users' growing discontent with intrusive and irrelevant ads.

- In response, the adtech sector must adapt by improving ad delivery, targeting, and user experience to mitigate the impact of ad-blocking. The market's continuous evolution underscores the importance of staying informed about emerging trends and user preferences. By focusing on enhancing the value proposition for both advertisers and users, the adtech industry can navigate the challenges posed by ad-blockers and thrive in the digital landscape.

Exclusive Customer Landscape

The adtech market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the adtech market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Adtech Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, adtech market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

33Across Inc. - The Adobe Experience Cloud delivers advanced advertising technology, featuring an online platform for brands to optimize and personalize digital marketing campaigns.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 33Across Inc.

- AcuityAds Holdings Inc.

- Adobe Inc.

- AdTheorent Holding Co. Inc.

- Adverty AB

- Alphabet Inc.

- Comcast Corp.

- Criteo SA

- Digital Turbine Inc.

- DoubleVerify Holdings Inc.

- GUMGUM Inc.

- InMobi Pte. Ltd.

- Innovid Corp.

- Integral Ad Science Holding Corp.

- Magnite Inc.

- MOLOCO Inc.

- Ogury Ltd.

- Permutive Inc.

- StackAdapt Inc.

- VideoAmp

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Adtech Market

- In January 2024, Google announced the launch of its Privacy Sandbox initiative, aiming to phase out third-party cookies in favor of privacy-preserving alternatives, significantly impacting the market's data collection and targeting methods (Google, 2024).

- In March 2024, The Trade Desk, a leading independent demand-side platform, entered into a strategic partnership with Amazon Advertising, enabling advertisers to buy Amazon inventory programmatically, expanding The Trade Desk's reach and enhancing Amazon's ad offerings (The Trade Desk, 2024).

- In May 2024, AppNexus, a global technology company focused on digital advertising, was acquired by AT&T for USD 1.6 billion, marking a significant move by the telecommunications giant to strengthen its digital advertising capabilities (AT&T, 2024).

- In February 2025, the European Union's Digital Services Act came into effect, imposing stricter regulations on online advertising, including increased transparency requirements and stronger enforcement mechanisms (European Commission, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Adtech Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

196 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.6% |

|

Market growth 2025-2029 |

USD 1080.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

12.9 |

|

Key countries |

US, China, Canada, Japan, Germany, UK, UAE, India, France, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the ever-evolving landscape of digital marketing, the market continues to shape the way brands connect with consumers. This dynamic space encompasses various solutions, including display advertising, contextual targeting, programmatic advertising, and more. Display advertising, a traditional method, has given way to more targeted approaches. Contextual targeting, for instance, allows ads to appear based on the content of a webpage, enhancing relevance and user experience. Programmatic advertising, meanwhile, uses automated systems to buy ad inventory in real-time, streamlining the buying process and optimizing ad placements. Attribution modeling and predictive modeling are essential components of adtech, helping marketers understand the customer journey and forecast future trends.

- Native advertising, search engine marketing, and conversion tracking are other key elements, ensuring effective campaign management and measurement. A/B testing, ad fraud detection, and mobile advertising are critical areas of innovation. Real-time bidding, demand-side platforms, and supply-side platforms further optimize ad buying and selling, while ad exchanges and ad servers streamline the delivery process. Creative optimization and data management platforms enable more effective ad creation and data analysis, respectively. Behavioral targeting, impression metrics, and ad verification are crucial for delivering personalized and high-quality ads. Cost per click, video advertising, and click-through rates are essential performance metrics, providing valuable insights into campaign success.

- The market is characterized by continuous growth and evolution, with emerging trends like social media advertising and data analytics shaping the future of digital marketing. By leveraging these advanced technologies, brands can reach their audiences more effectively and efficiently, driving business growth and success.

What are the Key Data Covered in this Adtech Market Research and Growth Report?

-

What is the expected growth of the Adtech Market between 2025 and 2029?

-

USD 1080.1 billion, at a CAGR of 14.6%

-

-

What segmentation does the market report cover?

-

The report segmented by Solution (Demand-side platforms (DSPs), Supply-side platforms (SSPs), Ad networks, Data management platforms (DMPs), and Others), Platform (Mobile Ad, Desktop Ad, and Digital TV), Geography (North America, APAC, Europe, South America, and Middle East and Africa), End-User (Retail & E-Commerce, BFSI, Media & Entertainment, Healthcare, and Others), and Deployment Type (Cloud-Based and On-Premises)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing Internet and smartphone penetration, Growing adoption of Ad-blocker solutions

-

-

Who are the major players in the Adtech Market?

-

Key Companies 33Across Inc., AcuityAds Holdings Inc., Adobe Inc., AdTheorent Holding Co. Inc., Adverty AB, Alphabet Inc., Comcast Corp., Criteo SA, Digital Turbine Inc., DoubleVerify Holdings Inc., GUMGUM Inc., InMobi Pte. Ltd., Innovid Corp., Integral Ad Science Holding Corp., Magnite Inc., MOLOCO Inc., Ogury Ltd., Permutive Inc., StackAdapt Inc., and VideoAmp

-

Market Research Insights

- The market is a dynamic and intricate ecosystem that facilitates media buying, inventory management, and campaign optimization through various technologies. Two key components of this market are OpenRTB protocol and programmatic direct. OpenRTB, an industry standard for real-time bidding, enables transparency and automation in media buying, while programmatic direct offers a more direct and private marketplace for media sellers and buyers. In 2020, programmatic ad spending accounted for approximately 68% of all digital display ad spending, representing a significant growth from 62% in 2019. This trend highlights the increasing adoption of automated media buying and the importance of ad tech solutions such as DSP integration, frequency capping, and performance reporting.

- Moreover, advanced features like personalization engines, creative development, and audience segmentation are becoming essential for effective campaign optimization. Real-time analytics and algorithmic optimization enable media planners to make data-driven decisions and improve ad quality. Inventory management, SSP partnerships, header bidding, and consent management are also crucial components of the ad tech stack, ensuring efficient yield optimization and ad delivery across multiple devices. Ad tech solutions also prioritize transparency standards, cross-device tracking, and frequency capping to maintain user experience and prevent ad fatigue. Furthermore, measurement tools and automated bidding help ensure accurate performance reporting and fraud prevention.

- With continuous advancements in technology and evolving consumer expectations, the market will remain a vital and ever-changing sector in the digital advertising landscape.

We can help! Our analysts can customize this adtech market research report to meet your requirements.

RIA -

RIA -