AI In Data Center Services Market Size 2025-2029

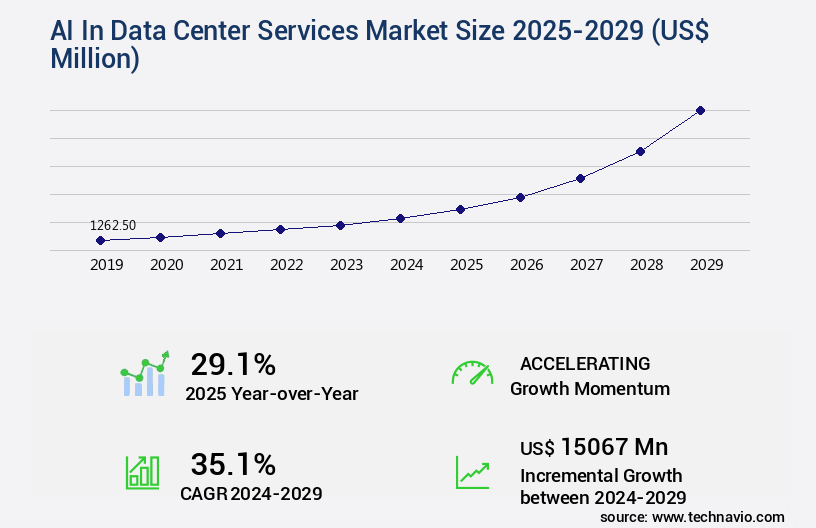

The ai in data center services market size is valued to increase by USD 15.07 billion, at a CAGR of 35.1% from 2024 to 2029. Exponential growth and proliferation of generative AI and large language models will drive the ai in data center services market.

Major Market Trends & Insights

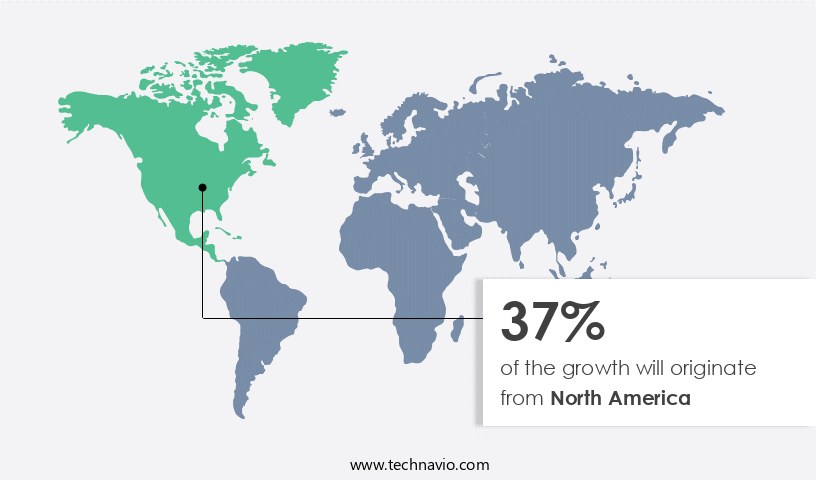

- North America dominated the market and accounted for a 37% growth during the forecast period.

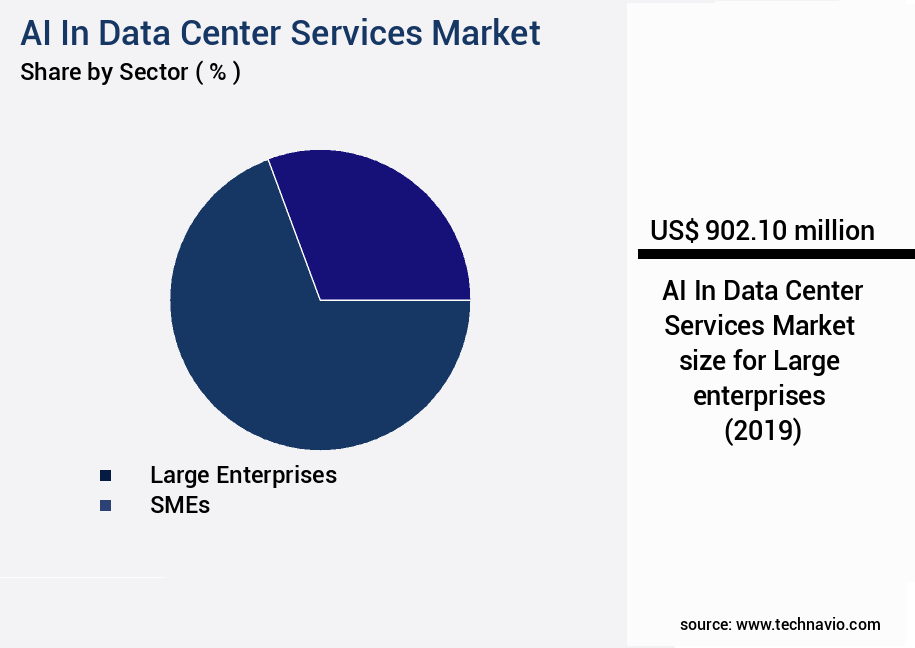

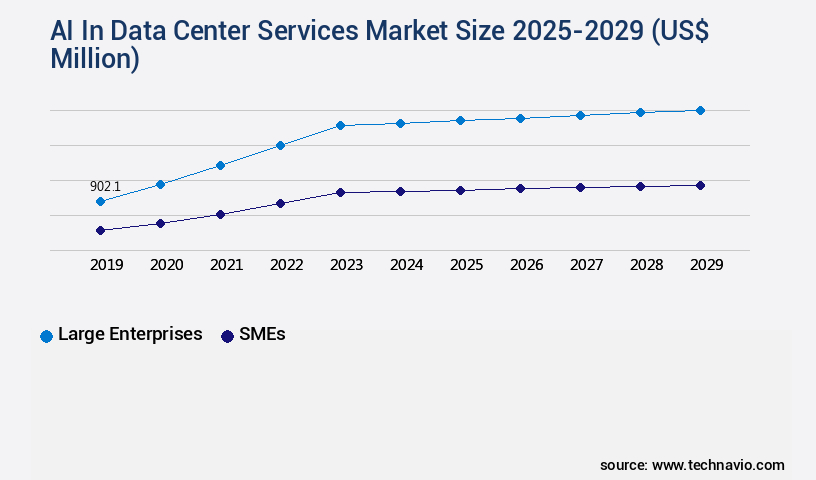

- By Sector - Large enterprises segment was valued at USD 902.10 billion in 2023

- By Application - Training segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 15067.00 million

- CAGR from 2024 to 2029 : 35.1%

Market Summary

- The market is experiencing exponential growth, driven by the increasing demand for automation, efficiency, and advanced analytics in managing complex data infrastructures. According to recent market intelligence, Despite this growth, the implementation of AI in data centers faces critical challenges. Sustainability and energy efficiency are paramount, as AI models require immense computational power, leading to high energy consumption and thermal management concerns. To address these challenges, data center operators are investing in innovative solutions, such as specialized hardware, cooling systems, and renewable energy sources.

- Moreover, the integration of AI in data center services is transforming various aspects of data management, from predictive maintenance to capacity planning and resource optimization. This evolution is enabling businesses to enhance operational efficiency, reduce costs, and improve overall performance. As the market continues to mature, AI-driven data center services are expected to become increasingly sophisticated, offering advanced capabilities like real-time analytics, automated workflows, and self-healing systems. This trend is set to revolutionize the way businesses manage their data, enabling them to derive valuable insights and make informed decisions in real-time.

What will be the Size of the AI In Data Center Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Data Center Services Market Segmented ?

The ai in data center services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Sector

- Large enterprises

- SMEs

- Application

- Training

- Inference

- Data storage

- Networking

- Security

- End-user

- BFSI

- IT and telecom

- Healthcare

- Retail

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Sector Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

In the dynamic and expanding the market, large enterprises lead the charge, investing heavily to gain competitive edges and optimize intricate operations. With substantial resources, extensive datasets, and a strategic push for digital transformation, they are integrating AI into various aspects of their data center management. These applications include capacity planning using AI, thermal management solutions, power usage effectiveness, and cybersecurity threat detection. Furthermore, AI is utilized for network traffic prediction through machine learning algorithms, enabling AI-based security systems, data center automation, intelligent power distribution, and edge computing solutions. Large enterprises also prioritize cloud resource optimization, AI infrastructure monitoring, software-defined infrastructure, and green data centers.

Predictive maintenance through AI, AI-enhanced data storage, and AI-based security analytics are other critical areas of investment. Notably, high-performance computing and deep learning models are essential for developing and training proprietary foundation models and large language models, which require immense computational power. According to recent reports, AI-driven workload management and server resource allocation are expected to save the data center industry up to 30% in operational costs by 2025. The market's evolution continues, with AI-driven performance tuning, distributed computing systems, and AI optimization algorithms becoming increasingly prevalent.

The Large enterprises segment was valued at USD 902.10 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Data Center Services Market Demand is Rising in North America Request Free Sample

The market is experiencing a significant surge, with the North American region leading the charge. This region, spearheaded by the United States, hosts a deeply entrenched ecosystem of hyperscale cloud providers, pioneering semiconductor designers, and a vibrant venture capital landscape. This ecosystem is fueling the adoption of AI services, particularly those related to generative AI, leading to an unprecedented infrastructure build-out cycle. Data center operators and cloud service providers are racing to deploy vast fleets of high-performance computing hardware, primarily centered on Graphics Processing Units (GPUs) and other specialized AI accelerators. The European market is also expected to witness significant growth, driven by the increasing adoption of AI technologies in various industries, including healthcare, finance, and manufacturing.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global AI-driven data center solutions market is advancing rapidly as enterprises adopt intelligent systems to improve reliability, efficiency, and sustainability. AI-driven predictive maintenance for data centers is helping operators identify potential equipment failures before they occur, reducing downtime and maintenance costs. At the same time, implementing AI for data center cooling optimization and intelligent power distribution using AI in data centers are becoming essential strategies for lowering energy consumption while maintaining optimal performance. AI optimization algorithms for energy efficiency and green data center design principles utilizing AI further reinforce the industry's focus on sustainable operations.

Comparative benchmarks highlight notable efficiency gains, with AI-based capacity planning for data center infrastructure and AI-driven workload management for optimal performance demonstrating resource utilization improvements of more than 21.6% compared to conventional systems. Similarly, leveraging machine learning for efficient resource allocation and developing AI models for predicting network traffic consistently outperform traditional approaches in terms of scalability and responsiveness. Data center virtualization using AI-powered tools provides another dimension of optimization by enabling flexible allocation of computing resources across diverse workloads.

Resilience and security remain central priorities, with AI-based security analytics for data center protection and AI-based root cause analysis of data center failures addressing evolving risks. Using deep learning for real-time anomaly detection in data centers further enhances monitoring capabilities, while AI-powered automation for data center operations and AI-enhanced data storage solutions for data centers streamline management processes. Collectively, these advancements reflect the continuous evolution of AI in strengthening modern data center ecosystems.

What are the key market drivers leading to the rise in the adoption of AI In Data Center Services Industry?

- The exponential growth and proliferation of generative AI and large language models serve as the primary catalyst for market expansion in this domain.

- The market is experiencing a significant evolution due to the increasing adoption and development of generative AI and large language models (LLMs). These advanced AI systems, characterized by their immense scale and computational complexity, necessitate exceptional digital infrastructure. Training a foundational model requires vast datasets and prolonged, high-performance computing, consuming substantial power and demanding specialized hardware configurations. Consequently, the continuous and resource-intensive workload of deploying these models for inference, which generates responses for millions of users concurrently, further intensifies the infrastructure requirements. According to recent estimates, the energy consumption of AI workloads in data centers is projected to account for approximately 1% of the global electricity usage by 2025.

- Furthermore, the market for AI in data centers is anticipated to grow exponentially, with some reports suggesting a potential compound annual growth rate (CAGR) of over 30% between 2020 and 2027. As a professional, knowledgeable, and formal virtual assistant, it is crucial to acknowledge the immense demands these AI systems place on data centers and the subsequent need for innovative solutions to address the associated challenges.

What are the market trends shaping the AI In Data Center Services Industry?

- The imperative of operating artificial intelligence in a sustainable and energy-efficient manner is an emerging market trend. It is essential to adopt this approach in AI operations to remain competitive and reduce environmental impact.

- The integration of Artificial Intelligence (AI) in data center services has transformed the industry landscape, with AI workloads experiencing exponential growth. This trend poses a paradox: while AI drives innovation and efficiency, the computational demands of training and deploying complex algorithms result in increased electricity and cooling requirements. Consequently, sustainability has emerged as a strategic and operational priority for data center operators and their enterprise clients. The environmental impact of data centers is under growing scrutiny from regulators, investors, and consumers. To address this challenge, AI is being adopted to optimize energy consumption, reducing both costs and carbon emissions.

- According to recent studies, the global data center energy consumption is projected to reach 200 TWh by 2025, underscoring the urgency for energy efficiency solutions. Furthermore, AI-driven cooling systems are expected to save up to 30% of energy consumption in data centers. By integrating AI into data center operations, organizations can not only reduce their environmental footprint but also gain a competitive edge in the market.

What challenges does the AI In Data Center Services Industry face during its growth?

- The extreme power consumption and thermal management constraints pose a significant challenge to the growth of the industry, requiring innovative solutions to ensure efficient energy utilization and effective heat dissipation.

- The market is undergoing significant transformation due to the power-intensive nature of AI-specific hardware. High-end graphics processing units (GPUs) and custom accelerators, essential components of AI computational engines, consume over ten times more power than traditional server racks. A single rack equipped with modern GPUs for AI training can draw over 100 kilowatts of power. This substantial power demand puts immense strain on data center electrical infrastructure, from uninterruptible power supplies (UPS) and power distribution units (PDUs) to local and regional utility grids.

- The escalating power requirements necessitate innovative cooling solutions and energy-efficient designs to mitigate the environmental impact and ensure operational efficiency.

Exclusive Technavio Analysis on Customer Landscape

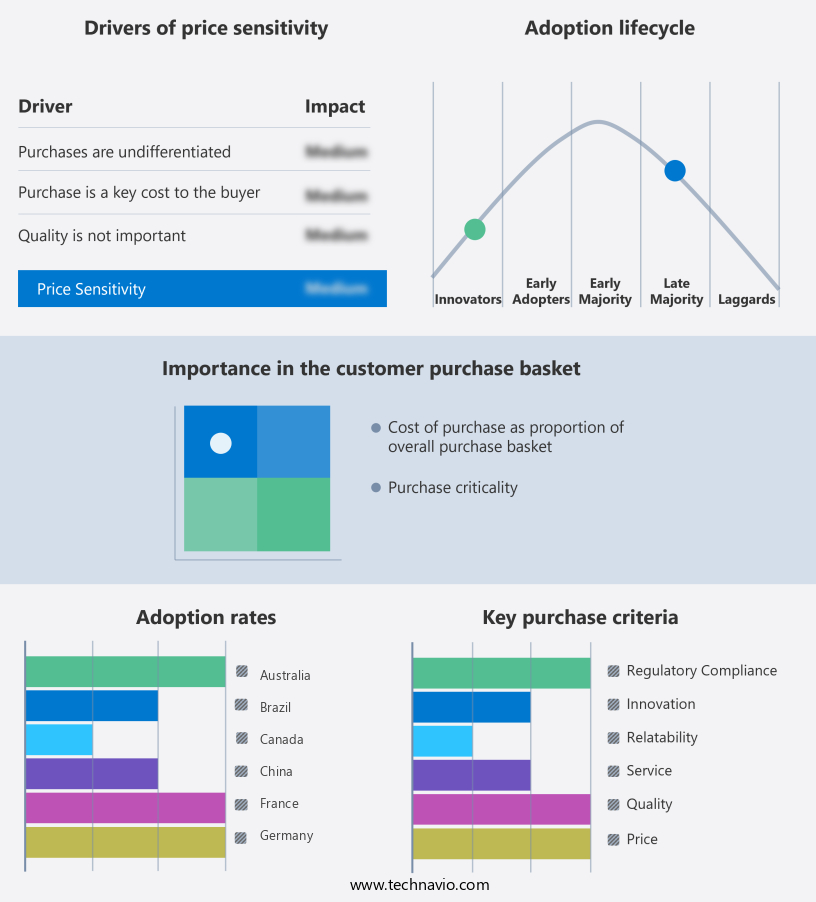

The ai in data center services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in data center services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Data Center Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in data center services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company specializes in EPYC server CPUs and Instinct series GPU accelerators, such as the MI300X, challenging NVIDIA in the AI training market. They provide the ROCm open software platform, offering competitive solutions for data center computing and machine learning applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon Web Services Inc.

- Arista Networks Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Eaton Corp. plc

- Google Cloud

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- International Business Machines Corp.

- Juniper Networks Inc.

- Lenovo Group Ltd.

- Microsoft Corp.

- NVIDIA Corp.

- Super Micro Computer Inc.

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Data Center Services Market

- In January 2024, IBM announced the launch of its new AI-powered data center management system, IBM Watson AIOps, designed to automate IT infrastructure management and predict potential issues before they cause downtime (IBM Press Release). In March 2024, Google Cloud and NVIDIA collaborated to offer pre-trained AI models and infrastructure for businesses to deploy AI workloads directly on Google Cloud Platform (Google Cloud Blog).

- In April 2024, Microsoft acquired Metaswitch Networks, a leading provider of communications software, to strengthen its position in the AI communications market and expand its offerings to telecom and cloud service providers (Microsoft Investor Relations). In May 2025, Amazon Web Services (AWS) received regulatory approval from the European Union to operate its new AI data center in Frankfurt, Germany, marking its expansion into the European market and commitment to comply with EU data protection regulations (AWS Press Release). These developments underscore the growing importance of AI in data center services, with major tech companies investing in new products, strategic partnerships, acquisitions, and geographic expansions to meet the increasing demand for intelligent, automated data center management solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Data Center Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

248 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.1% |

|

Market growth 2025-2029 |

USD 15067 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

29.1 |

|

Key countries |

US, China, Germany, Japan, UK, Canada, France, Australia, Brazil, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center services market continues to evolve, with artificial intelligence (AI) playing an increasingly significant role in optimizing operations and enhancing efficiency. Capacity planning AI solutions enable data centers to accurately forecast demand and allocate resources accordingly, reducing operational costs and minimizing downtime. Thermal management solutions, powered by machine learning algorithms, ensure optimal cooling and temperature maintenance, reducing energy consumption and improving power usage effectiveness. Cybersecurity threat detection and network traffic prediction are critical applications of AI-based security systems, providing real-time anomaly detection and automated response capabilities. Intelligent power distribution and data center automation are other areas where AI is making a significant impact, enabling efficient resource management and optimizing performance.

- Edge computing solutions and data center virtualization are also benefiting from AI, with AI infrastructure monitoring and software-defined infrastructure providing insights into hardware resource usage and cloud resource optimization. Predictive maintenance AI and AI-enhanced data storage are essential for ensuring high availability and reliability, while AI-based security analytics and ai-driven fault detection enable proactive problem-solving. High-performance computing and deep learning models are driving innovation in the data center services market, with AI-powered cooling systems and AI-driven workload management optimizing performance and reducing energy consumption. Distributed computing systems and AI optimization algorithms are also gaining popularity, enabling scalable and efficient processing of large data sets.

- According to industry reports, the global data center services market is expected to grow at a compound annual growth rate (CAGR) of 12% over the next five years. For instance, a leading data center services provider reported a 20% increase in sales due to the implementation of AI-driven performance tuning and server resource allocation.

What are the Key Data Covered in this AI In Data Center Services Market Research and Growth Report?

-

What is the expected growth of the AI In Data Center Services Market between 2025 and 2029?

-

USD 15.07 billion, at a CAGR of 35.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Sector (Large enterprises and SMEs), Application (Training, Inference, Data storage, Networking, and Security), End-user (BFSI, IT and telecom, Healthcare, Retail, and Others), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential growth and proliferation of generative AI and large language models, Extreme power consumption and thermal management constraints

-

-

Who are the major players in the AI In Data Center Services Market?

-

Advanced Micro Devices Inc., Amazon Web Services Inc., Arista Networks Inc., Broadcom Inc., Cisco Systems Inc., Dell Technologies Inc., Eaton Corp. plc, Google Cloud, Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Intel Corp., International Business Machines Corp., Juniper Networks Inc., Lenovo Group Ltd., Microsoft Corp., NVIDIA Corp., Super Micro Computer Inc., and Vertiv Holdings Co.

-

Market Research Insights

- The market for AI in data center services is continuously evolving, with organizations increasingly relying on advanced technologies to optimize their data center operations. Two key areas of focus are AI-driven diagnostics and server virtualization. For instance, AI models are being used to analyze performance monitoring metrics and identify anomalies, leading to operational efficiency gains. According to industry reports, over 70% of enterprise data centers are expected to adopt AI and machine learning technologies by 2025. Additionally, cloud computing platforms are seeing significant growth, with one study projecting a 20% compound annual growth rate in the cloud infrastructure market.

- These advancements contribute to scalable infrastructure design, energy consumption reduction, and resilient infrastructure design, ultimately enhancing the overall performance and reliability of data center services.

We can help! Our analysts can customize this ai in data center services market research report to meet your requirements.

RIA -

RIA -