AI Data Center Market Size 2026-2030

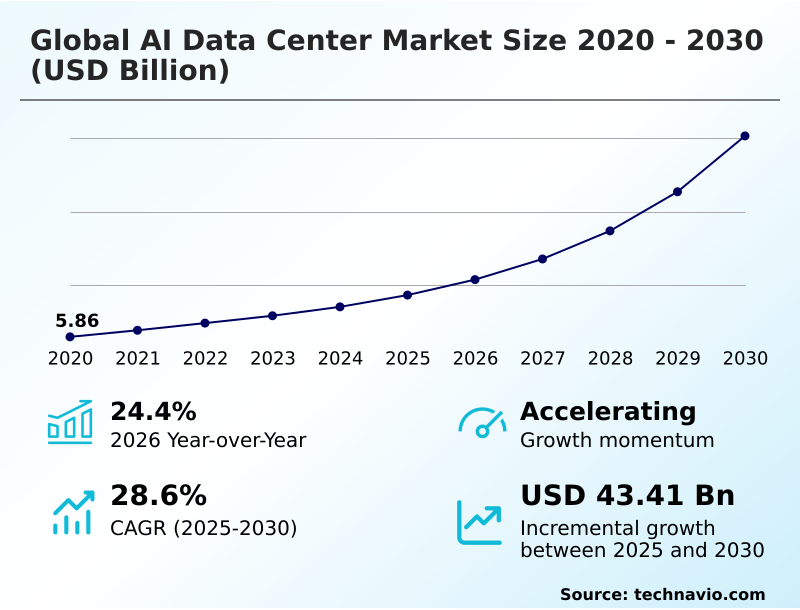

The ai data center market size is valued to increase by USD 43.41 billion, at a CAGR of 28.6% from 2025 to 2030. Exponential growth of big data and demand for sophisticated computational analysis will drive the ai data center market.

Major Market Trends & Insights

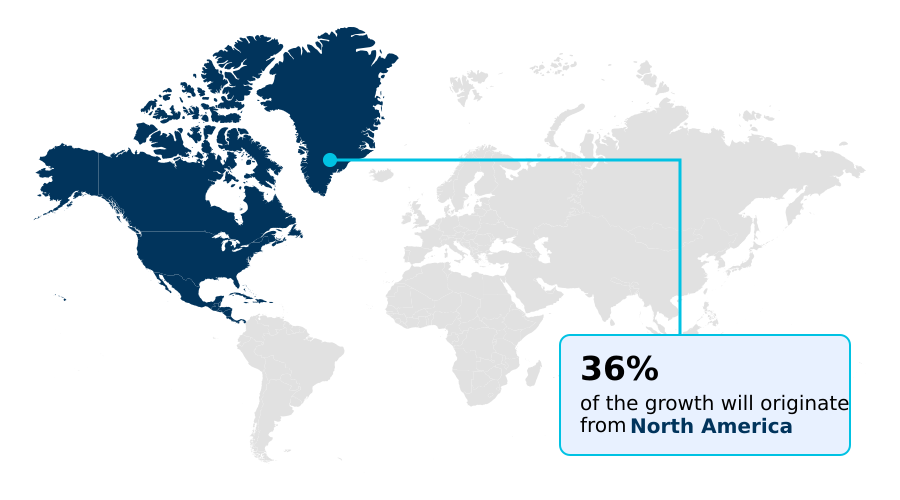

- North America dominated the market and accounted for a 35.7% growth during the forecast period.

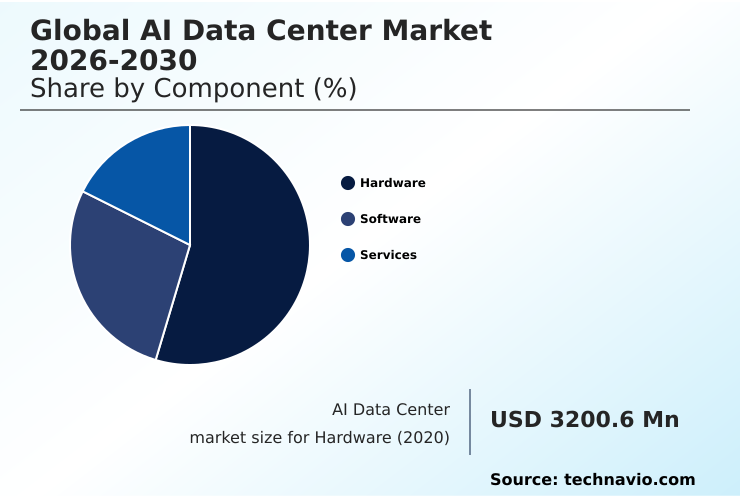

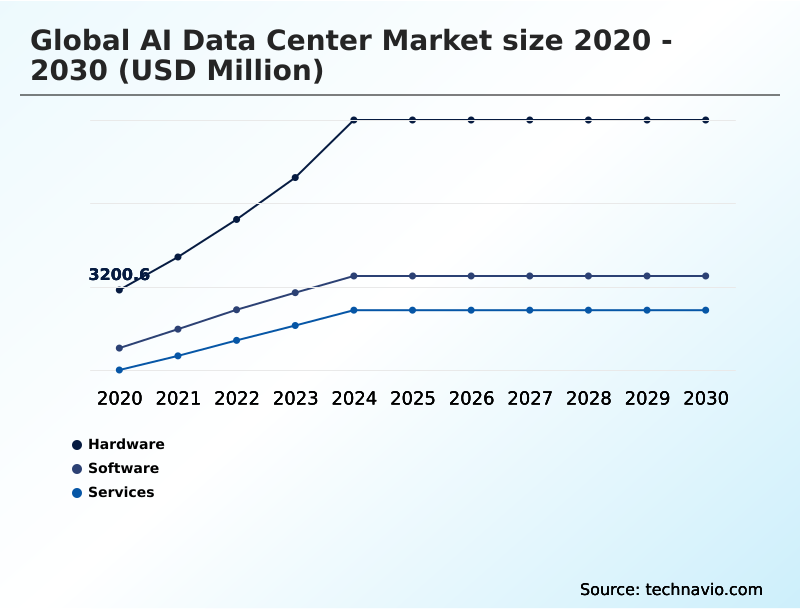

- By Component - Hardware segment was valued at USD 7.81 billion in 2024

- By Type - Hyperscale data centers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 54.80 billion

- Market Future Opportunities: USD 43.41 billion

- CAGR from 2025 to 2030 : 28.6%

Market Summary

- The AI data center market is built on highly specialized facilities engineered for the extreme computational demands of machine learning workloads. Unlike traditional data centers, these environments are architected for high-density, parallel processing using thousands of interconnected AI accelerators like graphics processing units. This infrastructure is supported by high-bandwidth, low-latency networking and high-performance storage capable of managing massive datasets.

- The evolution of these facilities is driven by the enterprise-wide adoption of AI to gain competitive advantages, from optimizing supply chains to powering algorithmic trading in financial markets, where processing speed directly impacts profitability.

- Key trends shaping the market include the adoption of advanced liquid cooling to manage thermal output and a strategic move toward edge computing to reduce latency for real-time applications. However, this expansion faces significant headwinds from power grid limitations and an increasingly complex global regulatory landscape focused on sustainability and data sovereignty.

- The industry's trajectory hinges on balancing insatiable computational demand with these critical operational and environmental constraints.

What will be the Size of the AI Data Center Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Data Center Market Segmented?

The ai data center industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Services

- Type

- Hyperscale data centers

- Edge data centers

- Colocation data centers

- Deployment

- Cloud-based

- On-premises

- Hybrid cloud

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment is the foundational layer of AI data centers, comprising the physical infrastructure purpose-built for high-performance computing (HPC) and machine learning.

This includes specialized AI accelerators such as graphics processing units and application-specific integrated circuits engineered for parallel processing architecture. These are housed in high-density compute racks and supported by AI-optimized storage and high-bandwidth memory (HBM).

To facilitate distributed training frameworks, low-latency interconnect fabrics are essential. Managing the significant thermal design power (TDP) from this hardware necessitates advanced thermal management solutions like direct-to-chip liquid cooling.

The effective integration of these components underpins the computational density and overall efficiency of the infrastructure, where optimized designs can lower power usage effectiveness (PUE) by over 15% compared to legacy systems.

This focus on hardware is critical for both large language model (LLM) training and AI-as-a-Service (AIaaS) delivery.

The Hardware segment was valued at USD 7.81 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Data Center Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is undergoing a significant transformation, moving beyond traditional hubs. North America remains dominant, projected to contribute over 35% of incremental growth, driven by massive capital expenditure on AI model training infrastructure and custom silicon development.

In contrast, the APAC region is the fastest-growing theater, with an expansion rate nearing 29%, fueled by digital transformation and national AI strategies.

Europe's growth is shaped by stringent environmental regulations and a focus on sustainable data center operations and data sovereignty.

Emerging regions like the Middle East and South America are becoming strategic frontiers, leveraging renewable energy power purchase agreements to attract investment.

This global redistribution is creating a more resilient network, supported by automated provisioning systems and advanced data center infrastructure management (DCIM) to ensure consistent performance across diverse regulatory and operational environments.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the AI data center landscape requires a holistic understanding of its entire lifecycle, from conception to operation. Key considerations begin with energy efficiency in AI data center design and extend to the total cost of ownership for AI hardware.

- The intense heat generated by modern processors necessitates advanced solutions like liquid cooling for high-density GPU clusters, which must be addressed through detailed thermal modeling for AI rack layouts. Managing hardware obsolescence in AI data centers is a perpetual challenge, compounded by persistent supply chain risks for AI accelerators.

- Operationally, effective AI workload scheduling and resource management are critical for maximizing the ROI analysis of custom silicon vs GPUs. Optimizing network fabrics for distributed training is paramount, as it can reduce model completion times by more than half compared to unoptimized architectures. Furthermore, the network latency impact on distributed AI models cannot be overstated.

- From a strategic perspective, data sovereignty and cloud infrastructure choices are increasingly intertwined with regulatory compliance for AI data processing. Organizations must also develop robust security protocols for multi-tenant AI environments and comprehensive disaster recovery planning for AI clusters.

- These complexities are amplified by the power and cooling requirements for LLM training and the external impact of grid stability on AI data centers, making hybrid cloud strategies for AI workloads and overcoming the challenges of scaling on-premises AI infrastructure key strategic imperatives.

What are the key market drivers leading to the rise in the adoption of AI Data Center Industry?

- The exponential growth of big data, coupled with the demand for sophisticated computational analysis, serves as a primary driver for the market.

- Market expansion is propelled by several interconnected drivers. The exponential growth of enterprise data necessitates a move toward AI inference acceleration and sophisticated computational analysis, with businesses reporting over 25% improvement in forecast accuracy by leveraging AI.

- This enterprise-wide adoption is a second major driver, as companies integrate AI to optimize operations and create new revenue streams, fueling demand for both on-premises and cloud-based AI infrastructure. The third pillar is the rapid pace of hardware innovation.

- The performance of new AI accelerators has increased by over 300% in just two years, enabling the development of more complex models.

- This symbiotic evolution between hardware and software, including fault-tolerant system design and MLOps platforms, creates a powerful growth dynamic, justifying massive investment in server rack power density and the underlying energy-efficient computing architecture.

What are the market trends shaping the AI Data Center Industry?

- The integration of liquid cooling technologies is emerging as a critical trend to support the thermal demands of high-density compute loads. This shift addresses the limitations of traditional air cooling in advanced AI data centers.

- Key trends are reshaping the operational and architectural fabric of the market. The shift toward advanced cooling is paramount, with immersion cooling systems and other liquid-based methods improving power usage effectiveness by up to 20% compared to legacy air-cooled designs.

- This drive for efficiency is coupled with a strategic focus on sustainability, where the adoption of modular data center design and waste heat recovery systems supports corporate environmental goals. The proliferation of edge computing inference represents another critical trend, pushing processing closer to data sources.

- This decentralization can reduce application latency by over 50%, enabling real-time analytics processing and supporting generative AI workloads that require instantaneous responses. These trends highlight an industry-wide move toward more efficient, sustainable, and responsive AI infrastructure, integrating AI-powered cybersecurity to protect distributed assets.

What challenges does the AI Data Center Industry face during its growth?

- Significant power constraints and grid stability limitations present a key challenge affecting industry growth.

- The market's rapid growth is tempered by significant operational and logistical challenges. The foremost issue is power; projects in major hubs are facing grid connection delays of up to 36 months, severely constraining expansion. This is compounded by escalating regulatory scrutiny over environmental impact, forcing operators to navigate complex AI ethics and governance frameworks and invest heavily in sustainability.

- Another critical hurdle is supply chain volatility. Lead times for essential components like high-capacity transformers and switchgear have increased by over 50%, elevating construction costs and creating project uncertainty. This scarcity of specialized hardware, from predictive maintenance for infrastructure sensors to core processors, makes it difficult to scale and exposes the market to geopolitical disruptions.

- These challenges require new strategies in confidential computing environments and federated learning infrastructure to mitigate risks.

Exclusive Technavio Analysis on Customer Landscape

The ai data center market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai data center market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Data Center Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai data center market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Provides hyperscale cloud infrastructure with custom GPU and ASIC accelerators, designed for large-scale model training and high-throughput inference operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Baidu Inc.

- CyrusOne LLC

- Dell Technologies Inc.

- Digital Realty Trust Inc.

- Equinix Inc.

- Google LLC

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Intel Corp.

- Iron Mountain Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NTT Communications Corp.

- NVIDIA Corp.

- Oracle Corp.

- Quanta Computer Inc.

- Salesforce Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai data center market

- In August 2025, Saudi Arabia's Humain announced plans to construct new data centers in Riyadh and Dammam, which will be equipped with advanced AI chips from leading US manufacturers.

- In April 2025, Microsoft announced a strategic plan to invest $80 billion in its AI data center infrastructure during its 2025-2026 fiscal year to meet escalating demand for cloud and AI services.

- In February 2025, Brookfield Infrastructure Partners and Data4 revealed a joint investment of over $20.7 billion to develop AI-specific infrastructure across France over the next five years, focusing on energy-efficient designs.

- In January 2025, Microsoft disclosed a $1.5 billion investment aimed at establishing sovereign-cloud zones in Thailand to serve the country's finance and public-sector clients with localized AI infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Data Center Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 28.6% |

| Market growth 2026-2030 | USD 43405.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 24.4% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI data center market is an ecosystem defined by relentless innovation in high-performance computing (HPC). Its foundation is built on specialized AI accelerators, including graphics processing units, tensor processing units, and application-specific integrated circuits, all designed for parallel processing architecture.

- This hardware is deployed in high-density compute racks connected by low-latency interconnect fabrics, forming the backbone of AI model training infrastructure. Effective AI workload management is achieved through sophisticated workload orchestration software, which handles resource pooling and scheduling across distributed training frameworks.

- The immense computational density of this hardware creates significant thermal design power (TDP), making advanced cooling like direct-to-chip liquid cooling and immersion cooling systems essential for maintaining operational stability. Consequently, metrics such as power usage effectiveness (PUE) and total cost of ownership (TCO) are central to boardroom decisions regarding infrastructure investment and achieving goals for sustainable data center operations.

- Implementing this AI-optimized storage and high-bandwidth memory (HBM) can reduce model inference times by over 60%, directly impacting business agility. Data center infrastructure management (DCIM) and automated provisioning systems are vital for managing this complexity, especially with the adoption of containerization technologies for AI and virtual machine optimization for energy-efficient computing.

- Security is also paramount, with a focus on secure multi-tenancy, data encryption at rest, and fault-tolerant system design through technologies like software-defined networking (SDN) and network function virtualization (NFV).

What are the Key Data Covered in this AI Data Center Market Research and Growth Report?

-

What is the expected growth of the AI Data Center Market between 2026 and 2030?

-

USD 43.41 billion, at a CAGR of 28.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Type (Hyperscale data centers, Edge data centers, and Colocation data centers), Deployment (Cloud-based, On-premises, and Hybrid cloud) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Exponential growth of big data and demand for sophisticated computational analysis, Significant power constraints and grid stability limitations

-

-

Who are the major players in the AI Data Center Market?

-

Amazon Web Services Inc., Baidu Inc., CyrusOne LLC, Dell Technologies Inc., Digital Realty Trust Inc., Equinix Inc., Google LLC, Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., IBM Corp., Intel Corp., Iron Mountain Inc., Meta Platforms Inc., Microsoft Corp., NTT Communications Corp., NVIDIA Corp., Oracle Corp., Quanta Computer Inc. and Salesforce Inc.

-

Market Research Insights

- The market is defined by a dynamic interplay between technological innovation and strategic infrastructure deployment. The rise of sovereign AI infrastructure is compelling organizations to prioritize data sovereignty compliance, often leading to the adoption of hybrid cloud AI deployment models. This approach allows enterprises to balance security with the scalability of AI-as-a-Service (AIaaS) offerings.

- On the operational front, advanced thermal management solutions are critical; implementing rear-door heat exchangers can improve power usage effectiveness by over 15% compared to conventional cooling methods. Concurrently, the expansion of edge computing inference is transforming application delivery, with localized processing reducing latency by more than 60%, a crucial factor for real-time industrial automation and autonomous systems.

- These shifts reflect a sophisticated market adapting to diverse performance, security, and efficiency demands.

We can help! Our analysts can customize this ai data center market research report to meet your requirements.

RIA -

RIA -