Air Conditioner Market for Transportation Size 2024-2028

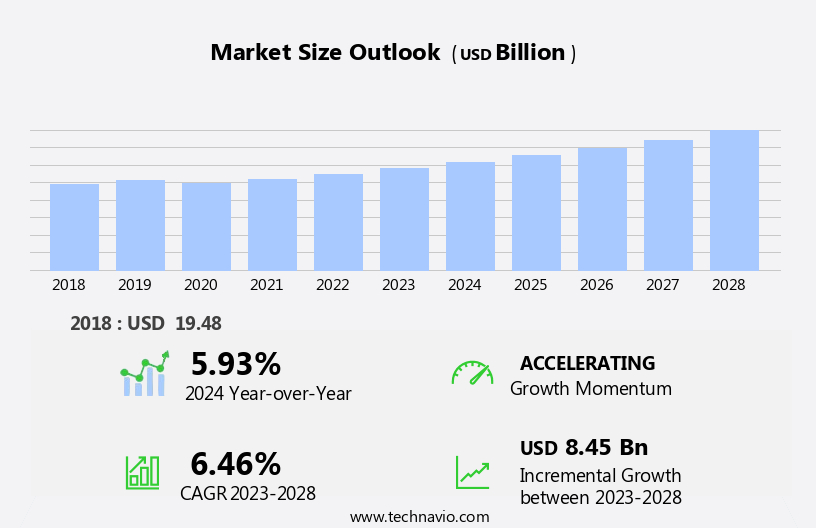

The air conditioner market for transportation size is forecast to increase by USD 8.45 billion at a CAGR of 6.46% between 2023 and 2028.

What will be the Size of the Air Conditioner Market for Transportation During the Forecast Period?

How is this Air Conditioner for Transportation Industry segmented and which is the largest segment?

The air conditioner for transportation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Automatic

- Manual

- Application

- Automotive

- Railway

- aerospace

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- North America

- US

- South America

- Middle East and Africa

- APAC

By Technology Insights

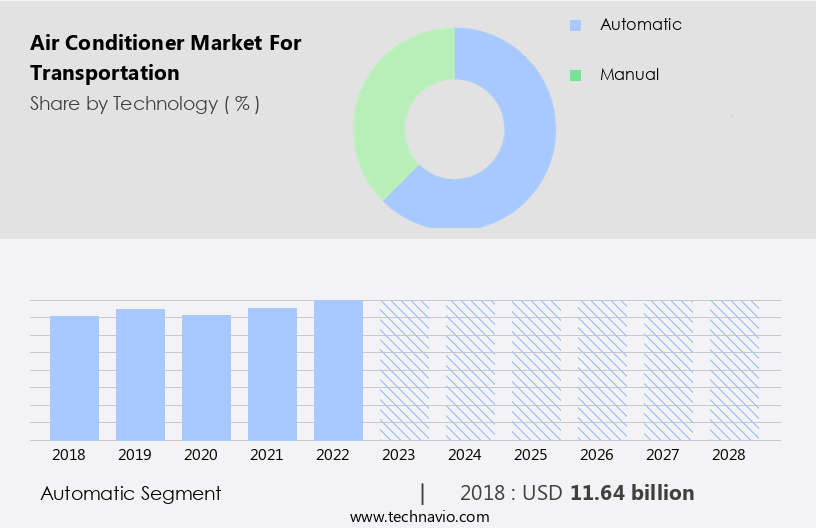

The automatic segment is estimated to witness significant growth during the forecast period. Air conditioning systems in passenger and commercial vehicles have become essential comfort features, enhancing the driving experience through automatic climate control. Advanced technologies, including sensors, electronic controls, and algorithms, enable these systems to regulate temperature, airflow, and humidity. Real-time monitoring of internal and external conditions allows for instant adjustments, while dual-zone and multi-zone control cater to individual passenger preferences. Climate mapping technology considers external factors like sunlight and vehicle speed for optimal air distribution. Energy-efficient systems and environmentally optimized products are crucial considerations In the market, with the Inverter and Unitary segments leading the way. The Middle East, particularly Gulf countries, have significant demand due to urbanization, climate change, and increasing consumer income levels.

The Automotive HVAC market is expected to grow due to safety concerns, vehicle electrification, and the use of eco-friendly refrigerants. Major manufacturers focus on technological improvements, such as compressor design, evaporator, receiver, and condenser innovations, to meet customer expectations. Competition is intense, with emerging service distinctions and client loyalty becoming key differentiators. Rapid industrialization, air pollution levels, and increasing commuting populations drive market growth. Auto windows, wind resistance, vehicle efficiency, and fuel savings are essential factors In the market. Vehicle type, passenger car and commercial vehicle, and automobile models influence HVAC markets, with passenger car sales and global economic activities impacting the market significantly.

Carbon dioxide emissions and the environment are major concerns, leading to a focus on fuel savings and energy efficiency.

Get a glance at the market report of various segments Request Free Sample

The Automatic segment was valued at USD 11.64 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

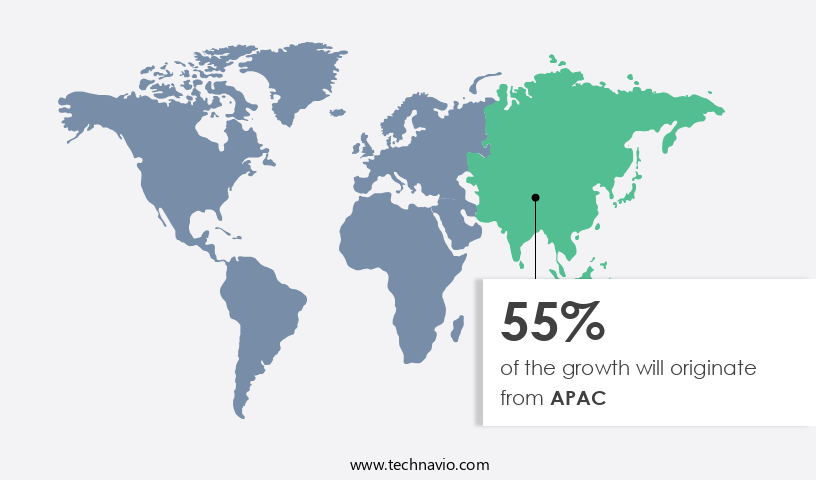

APAC is estimated to contribute 55% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The transportation air conditioner market in APAC experienced notable expansion in 2023, driven by several influential factors. The burgeoning automotive industry in APAC countries is a significant contributor, as economic growth raises consumer income levels and increases demand for passenger cars and commercial vehicles. This, in turn, leads to a higher adoption rate of air conditioning systems In the transportation sector. Urbanization and the subsequent rise in traffic congestion have further fueled the demand for climate-controlled vehicles, as commuters seek comfort during their daily journeys. Energy-efficient systems, such as those with inverter technology, and environmentally optimized products have gained popularity due to concerns over climate change and air pollution.

The market also caters to the needs of various vehicle segments, including rooftop ACs, unitary segment, and portable systems, for both residential and commercial applications. Technological advancements, such as eco-friendly refrigerants, sensors, and electronics, have improved the performance and cost-effectiveness of these systems. The market size, weight, and fuel savings offered by these systems are essential considerations for both passenger vehicles and commercial vehicles. The competition In the automotive HVAC market is intense, with major manufacturers continually introducing technological improvements to enhance the cabin experience and differentiate themselves from competitors. The market also serves the off-highway application sector, catering to the comfort needs of operators in harsh operating conditions.

Despite the benefits, the high cost remains a major constraint for some consumers, particularly in emerging markets. The market is expected to continue growing as the world adapts to shifting lifestyles, rapid industrialization, and increasing travel distances. Auto windows, wind resistance, and vehicle efficiency are also important factors influencing the market's growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Air Conditioner for Transportation Industry?

- Comfort and passenger experience in transportation sector is the key driver of the market.The market sector is driven by the prioritization of comfort and passenger experience across various modes of transportation, including cars and railways. In the automotive industry, advanced climate control systems have become a crucial differentiator for manufacturers, with features like multi-zone climate control, air purification, and personalized settings enhancing the overall driving experience. For instance, Mercedes-Benz focuses on these features to cater to its luxury vehicle consumers. In the railway industry, effective air conditioning is increasingly becoming an essential onboard amenity, with companies like Bombardier Transportation prioritizing passenger comfort In their trains. Energy efficiency and environmental optimization are also significant factors influencing the market.

Energy-efficient systems, such as those In the inverter segment, are gaining popularity due to their reduced power consumption and fuel savings. Additionally, the use of eco-friendly refrigerants is a growing trend, as concerns over climate change and air pollution levels continue to rise. Portable systems are another segment experiencing growth, particularly in regions with extreme climates, such as the Gulf countries. These systems offer flexibility and convenience, making them popular among both residential and commercial consumers. The competition In the market is fierce, with major manufacturers continually innovating to meet evolving consumer expectations and lifestyles. Technological improvements, such as the integration of electronics, sensors, and automation, are key areas of focus.

The market's dynamics are influenced by various factors, including urbanization, consumer income levels, middle-class population growth, and shifting lifestyles. The automotive HVAC market is also impacted by vehicle electrification, vehicle type, size, weight, passenger vehicles, commercial vehicles, and automobile models. Despite the challenges, such as harsh operating conditions and the major constraint of compressor power consumption, the market for automotive air conditioning continues to grow, driven by the need for interior comfort and safety in various transportation applications.

What are the market trends shaping the Air Conditioner for Transportation market?

- Adoption of alternative refrigerants for air conditioning systems is the upcoming market trend.The market is witnessing significant growth due to the increasing demand for environmentally optimized and energy-efficient systems. In the transportation sector, both portable and rooftop ACs are popular choices In the unitary segment. The Inverter and non-inverter segments cater to varying consumer income levels and lifestyles, with thermal comfort being a key consideration. Climate change and urbanization have led to a growing focus on automotive HVAC market safety, system size, weight, and fuel efficiency in passenger vehicles. Electronics, sensors, and cost are major factors influencing the market. Vehicle electrification and the use of eco-friendly refrigerants are emerging trends. Major manufacturers, such as Honeywell International Inc.,

are addressing environmental concerns by developing and incorporating alternative refrigerants into their products. For instance, Honeywell International Inc. Introduced Solstice yf, a low-global-warming-potential refrigerant, as a sustainable solution for automotive air conditioning systems. The market dynamics are influenced by factors such as consumer expectations, harsh operating conditions, and competition. The market is also driven by the shifting lifestyles and rapid industrialization, which have led to increased air pollution levels and commuting populations. Auto windows, wind resistance, vehicle efficiency, acceleration, fuel savings, and technological improvements are key considerations In the automotive air conditioning market. The market is segmented based on vehicle type, including passenger cars and commercial vehicles, and automobile models.

The major constraint In the market is the high cost of these advanced systems. However, the growing importance of interior comfort and customer experience is expected to drive market growth. Off-highway applications, such as tractors, are also a significant part of the air conditioning market. In conclusion, the market is witnessing significant growth due to the increasing demand for environmentally optimized and energy-efficient systems. Alternative refrigerants and technological improvements are key trends In the market. Major manufacturers are addressing consumer expectations and harsh operating conditions by developing advanced systems, despite the high cost.

What challenges does the Air Conditioner for Transportation Industry face during its growth?

- Difficulty in meeting energy consumption and efficiency balance in air conditioning systems is a key challenge affecting the industry growth.The market is driven by the increasing demand for environmentally optimized and energy-efficient systems. With urbanization and climate change, there is a growing focus on providing thermal comfort in vehicles, particularly in Gulf countries where extreme temperatures are common. Both the passenger and commercial vehicle segments, including unitary segment (Rooftop ACs) and inverter segment, are experiencing significant growth. In the residential and commercial sectors, consumer income levels and lifestyles have led to a preference for portable systems. However, In the transportation sector, safety, system size, weight, and passenger vehicles' cabin experience are crucial factors. Energy efficiency, fuel savings, and customer expectation are major concerns as the automotive HVAC market evolves.

Emerging technologies, such as electronics, sensors, and eco-friendly refrigerants, are driving technological improvements in compressors, evaporators, receivers, and condensers. The market is also influenced by factors like vehicle electrification, vehicle type (passenger car and commercial vehicle), automobile models, HVAC markets, passenger car sales, and global economic activities. Air pollution levels, particularly in cities like Beijing, have led to concerns about hazardous air and airborne infections. Commuting populations and travel distances are increasing, making air conditioning a necessity. Automotive air conditioning systems' compressor's power consumption, fuel savings, and cost are major considerations. Off-highway applications, including tractors and off-highway vehicles, also require air conditioning systems to operate efficiently in harsh conditions.

Operator efficiency and comfort are essential, as is addressing the major constraint of meeting energy efficiency standards while providing adequate cooling. Competition In the market is fierce, with major manufacturers continually striving to differentiate themselves through customer experience, innovation, and emerging service distinctions. Shifting lifestyles and rapid industrialization are further driving demand for air conditioning systems in various modes of transportation.

Exclusive Customer Landscape

The air conditioner market for transportation forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the air conditioner market for transportation report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, air conditioner market for transportation forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Amber Enterprises India Ltd. - The transportation sector relies heavily on efficient air conditioning systems to ensure passenger comfort and productivity. The market caters to various modes, including railway, metro, and buses. Railway air conditioners are integral to long-distance travel, ensuring a comfortable journey for passengers despite extreme temperatures. Metro air conditioners maintain optimal indoor climate in densely populated urban areas, enhancing the commuting experience. Bus air conditioners enable operators to cater to diverse climate conditions, expanding their serviceability and customer base. This market segment continues to evolve, driven by advancements in energy efficiency, filtration technologies, and connectivity solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amber Enterprises India Ltd.

- Area Cooling Solutions

- Bergstrom Climate Control Systems

- Daikin Industries Ltd.

- Danfoss AS

- Eberspacher Gruppe GmbH and Co.KG

- Guchen Industry

- Henan kingclima industry co. ltd.

- JTAC

- Liebherr International Deutschland GmbH

- MAHLE GmbH

- Mitsubishi Electric Corp.

- Rifled Air Conditioning

- Sphere Therm

- Subros Ltd.

- Suzhou New Tongchuang Auto Air Conditioning Co. Ltd.

- The Chemours Co.

- ThermaGroup Ltd.

- Trane Technologies Plc

- Valeo SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The transportation sector continues to evolve, with a growing emphasis on environmentally optimized products and energy-efficient systems. The automotive HVAC market is a significant contributor to this trend, as consumers demand improved thermal comfort and cabin experience in both passenger vehicles and commercial applications. Urbanization and climate change have led to increased air pollution levels and rising consumer income levels, particularly in middle-class populations. These factors have driven the demand for energy-efficient air conditioning systems, as individuals seek to enhance their lifestyles and maintain a comfortable interior environment. Portable systems have gained popularity in various transportation applications due to their flexibility and ease of use.

However, rooftop ACs remain a dominant force In the market, with the unitary segment and inverter segment leading the charge in terms of technological improvements and energy efficiency. The automotive HVAC market is influenced by several factors, including safety, system size, weight, passenger vehicles, electronics, sensors, cost, and vehicle electrification. Major manufacturers are continually innovating to meet these demands, with a focus on eco-friendly refrigerants and emerging service distinctions to enhance customer experience and loyalty. Shifting lifestyles and rapid industrialization have led to longer commutes and increased travel distances. As a result, thermal comfort has become a crucial consideration for both passengers and operators.

The automotive air conditioning system's size, weight, and fuel savings are essential factors in vehicle efficiency, acceleration, and pick-up. The compressor is a critical component of the air conditioning system, with its power consumption and fuel savings being major concerns for manufacturers. The automotive HVAC market's technological improvements include advancements in compressors, evaporators, receivers, and condensers, as well as the integration of sensors and electronics to optimize performance and reduce costs. The market for air conditioning systems in transportation applications is diverse, with passenger cars, commercial vehicles, and off-highway vehicles all requiring unique solutions. OEMs are continually seeking lighter, more efficient, and smaller systems to meet the demands of various vehicle types and applications.

The automotive HVAC market's growth is influenced by several factors, including passenger car sales, economic activities, and auto sales. The global epidemic has also had an impact on market dynamics, with increased focus on safety and eco-friendly solutions. Despite the challenges posed by harsh operating conditions and major constraints such as cost and competition, the automotive air conditioning market continues to evolve, driven by consumer expectations and the need for innovative, efficient, and eco-friendly solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.46% |

|

Market growth 2024-2028 |

USD 8.45 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.93 |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Air Conditioner Market for Transportation Research and Growth Report?

- CAGR of the Air Conditioner for Transportation industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the air conditioner market for transportation growth of industry companies

We can help! Our analysts can customize this air conditioner market for transportation research report to meet your requirements.

RIA -

RIA -