Aircraft Engine Compressor Market Size 2025-2029

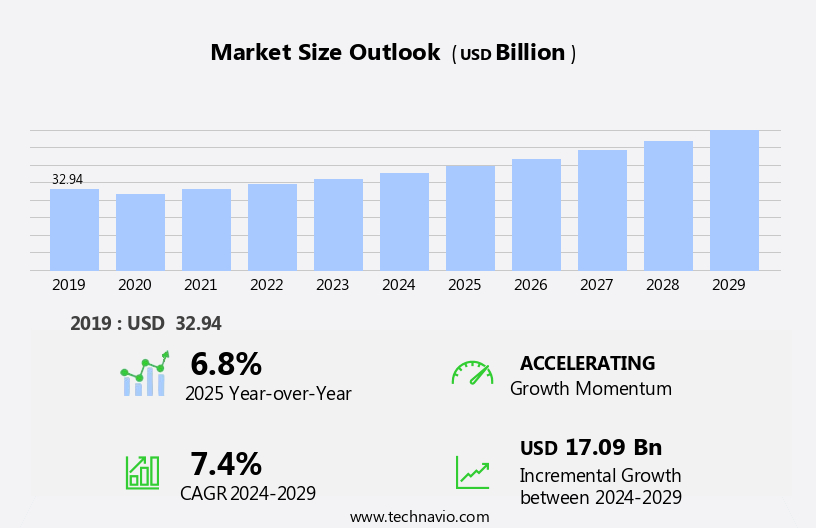

The aircraft engine compressor market size is forecast to increase by USD 17.09 billion, at a CAGR of 7.4% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing demand for new aircraft deliveries. According to industry data, aircraft manufacturers are ramping up production to meet the surging demand for air travel, leading to a corresponding increase in engine orders. This trend is expected to continue, with the number of aircraft deliveries projected to reach new heights in the coming years. Another key driver for the market is the development of electric and hybrid aircraft. As the aviation industry seeks to reduce its carbon footprint and improve fuel efficiency, there is growing interest in alternative propulsion systems.

- Compressors play a crucial role in these new technologies, as they are responsible for compressing air for the engines. This presents both opportunities and challenges for market participants, as they will need to adapt to new design requirements and manufacturing processes. However, the market also faces several challenges. One major obstacle is the technical issues associated with compressor design and manufacturing. The complexity of compressor blades, which must be lightweight, durable, and able to withstand extreme temperatures and pressures, makes their production a challenging and costly process. Additionally, compressor failures can result in significant downtime and maintenance costs for airlines, further adding to the pressure on engine manufacturers to improve reliability and reduce maintenance requirements.

What will be the Size of the Aircraft Engine Compressor Market during the forecast period?

- The market continues to evolve, driven by the dynamic interplay of various factors. Propulsion systems in the aviation sector are undergoing significant changes, with a focus on noise reduction and emission reduction in response to environmental regulations. Compressor technologies, such as high-bypass turbofans and centrifugal compressors, are at the forefront of these advancements, with engine manufacturers continually pushing the boundaries of fuel consumption and thrust-to-weight ratio. Component manufacturers are innovating with lightweight materials like nickel alloys and composites, while sensor technology and data analytics enable predictive maintenance and condition-based services. The aftermarket sector is also transforming, with suppliers offering engine upgrades and remote monitoring services to enhance engine performance and optimize life cycle cost.

- Military aircraft and business aviation segments are adopting these trends, with a growing emphasis on fuel efficiency improvement and engine upgrades. The oil and gas industry is exploring aero-derivative gas turbines for power generation, further expanding the market's reach. Advanced materials, such as titanium alloys and additive manufacturing, are revolutionizing rotor blade design and blade manufacturing processes. Machine learning and artificial intelligence are also being integrated into compressor systems to optimize engine performance and improve stall margin. The ongoing unfolding of these market activities highlights the continuous dynamism of the market, with new applications and innovations shaping its future.

How is this Aircraft Engine Compressor Industry segmented?

The aircraft engine compressor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Heavy duty

- Medium

- Light

- Application

- CBA

- Military aircraft

- Product Type

- Centrifugal compressors

- Axial compressors

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- The Netherlands

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Type Insights

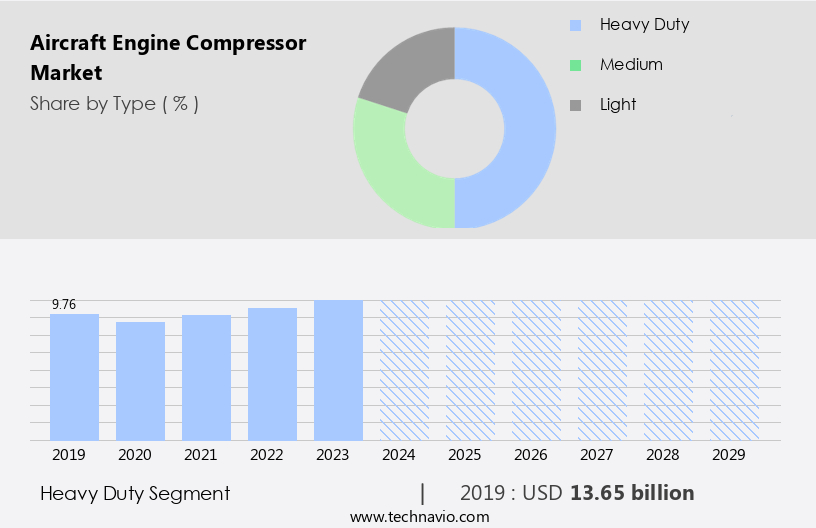

The heavy duty segment is estimated to witness significant growth during the forecast period.

The market is experiencing substantial growth due to the increasing demand for fuel-efficient and high-performance engines in both civil aviation and military sectors. Jet engines, a primary application for these compressors, are subject to stringent environmental regulations, necessitating the development of quieter and cleaner propulsion systems. In response, engine manufacturers are focusing on noise reduction technologies and emission reduction strategies, such as advanced materials like nickel alloys and composite materials, and the implementation of artificial intelligence (AI) and machine learning (ML) for predictive maintenance and engine performance optimization. Component manufacturers are also innovating with lightweight materials, such as titanium alloys and advanced materials, to improve thrust-to-weight ratios and reduce fuel consumption.

Three-dimensional (3D) printing technology is being utilized for the production of inlet guide vanes and rotor blades, allowing for greater design flexibility and customization. Aftermarket suppliers are offering condition-based maintenance services and digital twins for remote monitoring and engine upgrades. The high-bypass turbofan engines, such as the GE9X engine by General Electric Aviation, are leading the market with their impressive fuel efficiency improvements and high pressure ratio. These engines, which power modern commercial aircraft, incorporate centrifugal compressors and axial compressors, as well as advanced blade designs and stall margin technologies. Turboshaft engines and aero-derivative gas turbines are also gaining popularity in the business aviation and power generation sectors.

Military aircraft are also driving market growth with their requirement for high-performance and reliable compressors. Predictive maintenance and condition-based monitoring are essential for ensuring the longevity and reliability of these engines. Additive manufacturing, or 3D printing, is being employed for the production of engine components, allowing for faster turnaround times and reduced costs. The market for aircraft engine compressors is expected to continue growing, as the demand for more efficient and environmentally friendly engines increases. The integration of AI, ML, and sensor technology will enable real-time data analytics and engine performance optimization, further enhancing the value proposition for both engine manufacturers and operators.

The Heavy duty segment was valued at USD 13.65 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

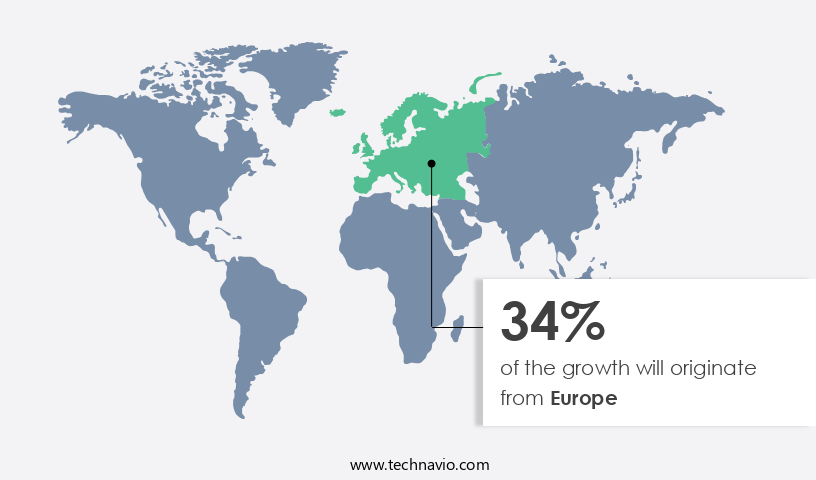

Europe is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The European aircraft industry is a significant player in the global market, encompassing the production of jet engines, commercial and military aircraft, helicopters, and components. Major European manufacturers, including Airbus with locations in France, Germany, Spain, and the UK, contribute to the region's high demand for aircraft. Europe's well-established airport infrastructure further boosts this demand, with the European Commission reporting 820 million passengers using commercial aircraft within the EU during the second half of 2022, marking an increase of 119%. Noise reduction and environmental regulations are key considerations in the development of propulsion systems for both commercial and business aviation.

Gas turbine engines, such as those used in jet engines and turboshaft engines, are undergoing advancements to improve fuel efficiency and reduce emissions. These engines incorporate compressor stages, axial and centrifugal, which are being optimized through blade design and material innovations using nickel alloys, composite materials, and advanced materials. Component manufacturers are focusing on life cycle cost reduction and aftermarket services, with condition-based maintenance and predictive maintenance strategies gaining traction. Digital twins, remote monitoring, and data analytics are essential tools in these efforts, as well as the implementation of machine learning algorithms for engine performance optimization. Military aircraft and helicopters also benefit from these advancements, with additive manufacturing and 3D printing playing a role in producing lightweight components and engine upgrades.

The aviation sector is also exploring the integration of artificial intelligence and sensor technology to enhance engine performance and improve safety. Inlet guide vanes, a critical component in gas turbine engines, are being redesigned to increase stall margin and thrust-to-weight ratio. These improvements are not only relevant to civil aviation but also to business aviation, general aviation, and oil and gas industries, where aero-derivative gas turbines and turboprop engines are utilized. The focus on emission reduction and fuel consumption improvement is driving innovation in the aircraft engine market. Pressure ratio, a critical factor in engine efficiency, is being increased through the development of high-bypass turbofans.

Engine manufacturers are collaborating with suppliers to develop more efficient and sustainable propulsion systems, while also considering the integration of electric or hybrid systems in the future. In summary, the European aircraft engine market is witnessing significant advancements in technology and innovation, driven by the need for noise reduction, environmental regulations, and fuel efficiency improvements. The integration of digital technologies, advanced materials, and manufacturing techniques is transforming the industry, with a focus on improving engine performance, reducing life cycle costs, and enhancing safety.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Aircraft Engine Compressor Industry?

- The significant rise in aircraft deliveries serves as the primary market catalyst.

- The market is experiencing significant growth due to the increasing demand for more fuel-efficient and environmentally friendly propulsion systems in both civil and business aviation. Noise reduction and compliance with stringent environmental regulations are key priorities for engine manufacturers. In response, there is a focus on the development of advanced technologies such as 3D printing, lightweight materials, and improved inlet guide vanes. These innovations aim to reduce fuel consumption and enhance overall engine performance. Component manufacturers are investing heavily in research and development to meet the evolving needs of commercial and business aviation sectors. The demand for jet engines is expected to remain robust, driven by the expansion of air travel markets in emerging economies and the growing popularity of business aviation.

- The emphasis on life cycle cost and component reliability is also influencing market dynamics. Overall, the market is poised for steady growth during the forecast period.

What are the market trends shaping the Aircraft Engine Compressor Industry?

- The emerging trend in the aerospace industry is the development of electric and hybrid aircraft. This innovative technology is gaining significant attention due to its potential for reducing emissions and increasing fuel efficiency.

- The market is experiencing significant growth due to the increasing focus on fuel efficiency and emission reduction in the aviation industry. Advanced technologies, such as gas turbine engines with high pressure ratios and compressor stages, are being adopted to enhance engine performance. Artificial intelligence (AI) is also being integrated into compressor systems to optimize performance and improve condition-based maintenance. Turboshaft engines and aero-derivative gas turbines are other types of engines that are gaining popularity for their high thrust-to-weight ratio and fuel efficiency. The market is driven by the increasing demand for compressor components from aftermarket suppliers and the growing number of applications in general aviation and military aircraft.

- Additionally, the development of electric and hybrid aircraft, such as the Pipistrel Velis Electro and Ampaire Electric EEL, is expected to further propel market growth. Boeing and Airbus are among the leading players investing in electric vertical takeoff and landing (eVTOL) aircraft to cater to the emerging urban air mobility market.

What challenges does the Aircraft Engine Compressor Industry face during its growth?

- The compressor's technical issues, including complexity in blade manufacturing, poses a significant challenge to the industry's growth.

- Aircraft engine compressors are crucial components that require high precision in design and manufacturing to ensure optimal performance and safety. Compressor blades, or airfoils, are subjected to aerodynamic principles and play a significant role in airflow. The angle of attack, formed between the air strike direction and the compressor blade cord line, impacts compressor efficiency. Variations in angle of attack can lead to compressor stalling, causing an imbalance between air supply and demand. To enhance compressor performance and prevent potential failures, engine manufacturers incorporate advanced technologies such as data analytics, sensor technology, and composite materials. Nickel alloys and centrifugal compressors are commonly used due to their high strength-to-weight ratio and ability to withstand extreme temperatures.

- Moreover, engine upgrades, aftermarket services, and remote monitoring have become essential in the aviation industry for predictive maintenance and cost savings. The adoption of additive manufacturing in producing engine components further improves efficiency and reduces production time. Military aircraft and high-bypass turbofans require robust compressor systems to meet stringent performance requirements. Sensor technology and real-time data analytics enable predictive maintenance, reducing downtime and maintenance costs. In conclusion, the market is driven by the need for high-performance, lightweight, and reliable components. The integration of advanced technologies, such as data analytics, sensor technology, composite materials, and additive manufacturing, plays a vital role in enhancing compressor efficiency, reliability, and safety.

Exclusive Customer Landscape

The aircraft engine compressor market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aircraft engine compressor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aircraft engine compressor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bet Shemesh Engines Ltd. - The company specializes in providing advanced aircraft engine compressor solutions, including the PT6A 114A, PT6A 67D, and PT6A 34AG models. These engines are renowned for their exceptional performance and reliability in powering various aircraft types. With a focus on innovation and quality, the company's offerings enhance aircraft efficiency and reduce maintenance costs for aviation clients worldwide. The PT6A series engines are recognized for their robust design and versatility, making them a preferred choice for operators seeking optimal performance and longevity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bet Shemesh Engines Ltd.

- Bharat Forge Ltd.

- Compressed Air Systems Inc

- EuroJet Turbo GmbH

- General Electric Co.

- Honeywell International Inc.

- IHI Corp.

- JSC Klimov

- Melrose Industries Plc

- MTU Aero Engines AG

- OC Oerlikon Corp. AG

- RTX Corp.

- Rolls Royce Holdings Plc

- Safran SA

- The Williams Co. Inc

- Turbocam Inc.

- UEC Aviadvigatel JSC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aircraft Engine Compressor Market

- In February 2023, Rolls-Royce, a leading aircraft engine manufacturer, announced the successful ground testing of its Advanced Open Rotor (AOR) technology, marking a significant technological advancement in aircraft engine compressors. This new design aims to improve fuel efficiency by up to 25% compared to traditional turbofans (Rolls-Royce press release).

- In May 2024, Honeywell Aerospace and Pratt & Whitney, two major aircraft engine compressor manufacturers, formed a strategic partnership to develop and market hybrid-electric propulsion systems for regional aircraft. This collaboration is expected to accelerate the adoption of electric propulsion in the aviation industry (Honeywell press release).

- In August 2024, GE Aviation secured a USD1.1 billion contract from Boeing to supply LEAP-1B engines for 100 737 MAX aircraft. This deal underscores the continued demand for fuel-efficient aircraft engines and strengthens GE Aviation's position in the market (Boeing press release).

- In November 2025, Safran Aircraft Engines announced the successful certification of its LEAP-X engine by the European Union Aviation Safety Agency (EASA). This milestone marks the entry of the LEAP-X engine into the European market, expanding Safran's customer base and market share (Safran Aircraft Engines press release).

Research Analyst Overview

The market is witnessing significant advancements, driven by the integration of smart technologies and alternative fuels. Vibration analysis, a key aspect of compressor maintenance, is being enhanced through the use of advanced sensors and predictive analytics. Smart materials, such as variable geometry and high-temperature alloys, are improving compressor efficiency and reducing noise certification requirements. Cooling systems and thermal management solutions are addressing the challenges of high-temperature operations. Noise abatement procedures are being augmented with active control technology and blade tip shrouds. Compressor surge and rotating stall are being mitigated through blade tip clearance optimization and variable stator vanes. Carbon offsetting initiatives are driving the adoption of energy efficiency standards and green aviation practices.

Reliability analysis, failure analysis, and performance curve optimization are essential for data-driven decision-making. Seal technology and lubrication systems are being enhanced for improved corrosion resistance and longer maintenance intervals. Environmental impact assessments are crucial for minimizing the industry's carbon footprint and ensuring sustainable growth.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aircraft Engine Compressor Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.4% |

|

Market growth 2025-2029 |

USD 17.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.8 |

|

Key countries |

US, Germany, UK, Canada, China, Italy, The Netherlands, France, India, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aircraft Engine Compressor Market Research and Growth Report?

- CAGR of the Aircraft Engine Compressor industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aircraft engine compressor market growth of industry companies

We can help! Our analysts can customize this aircraft engine compressor market research report to meet your requirements.

RIA -

RIA -