Alternative Credentials For Higher Education Market Size 2026-2030

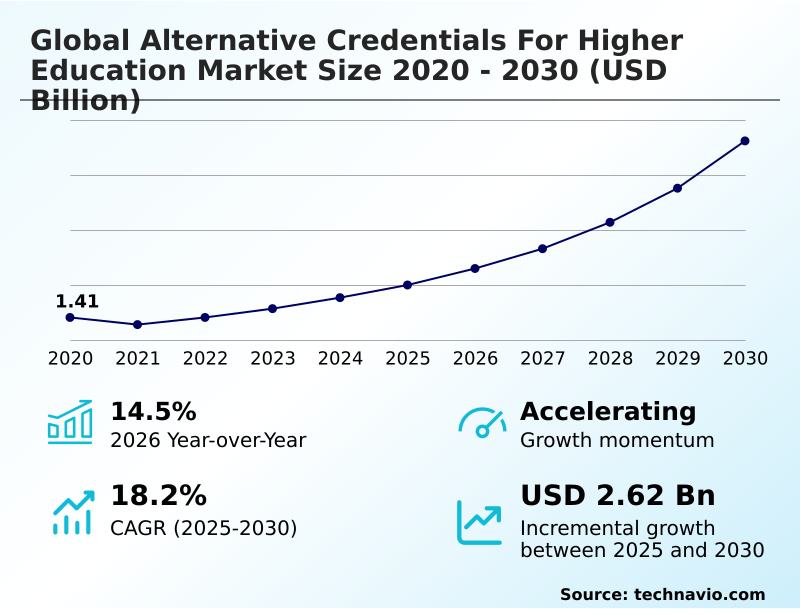

The alternative credentials for higher education market size is valued to increase by USD 2.62 billion, at a CAGR of 18.2% from 2025 to 2030. Rising global skills gap and transition toward skill-based recruitment will drive the alternative credentials for higher education market.

Major Market Trends & Insights

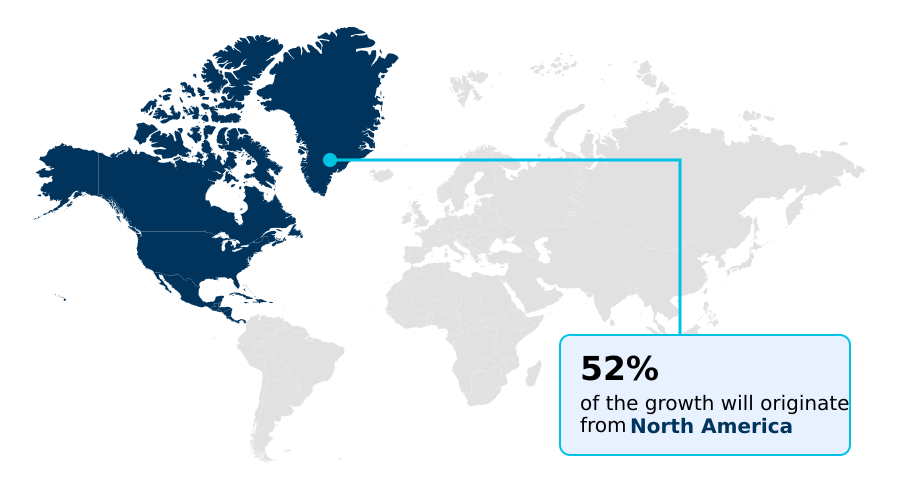

- North America dominated the market and accounted for a 51.8% growth during the forecast period.

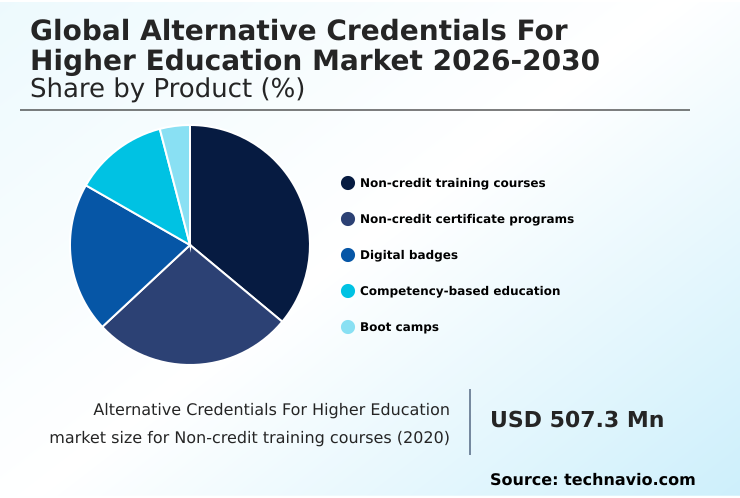

- By Product - Non-credit training courses segment was valued at USD 641.9 million in 2024

- By Type - Online segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.21 billion

- Market Future Opportunities: USD 2.62 billion

- CAGR from 2025 to 2030 : 18.2%

Market Summary

- The alternative credentials for higher education market is undergoing a profound transformation, shifting focus from traditional multi-year degrees to a more agile, skill-centric model. This evolution is driven by the urgent need for upskilling and reskilling in a workforce disrupted by rapid technological advancements.

- Learners and employers alike are embracing modular education, including micro-credentials and digital badges, as a means to validate specific competencies. The integration of technologies like blockchain verification provides a secure and portable method for individuals to showcase their achievements in a digital portfolio, enhancing trust and transparency.

- For instance, a multinational logistics company can implement a custom upskilling program using stackable credentials to train its workforce on new supply chain automation software, ensuring its team has industry-recognized credentials without the downtime of traditional courses. However, the market grapples with challenges such as the fragmentation of quality assurance frameworks and the risk of credential inflation.

- Addressing these issues through standardized credit transfer frameworks and a commitment to lifelong learning pathways will be critical for sustained adoption and ensuring these credentials hold long-term value in the global labor market, supported by robust learning management system.

What will be the Size of the Alternative Credentials For Higher Education Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Alternative Credentials For Higher Education Market Segmented?

The alternative credentials for higher education industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

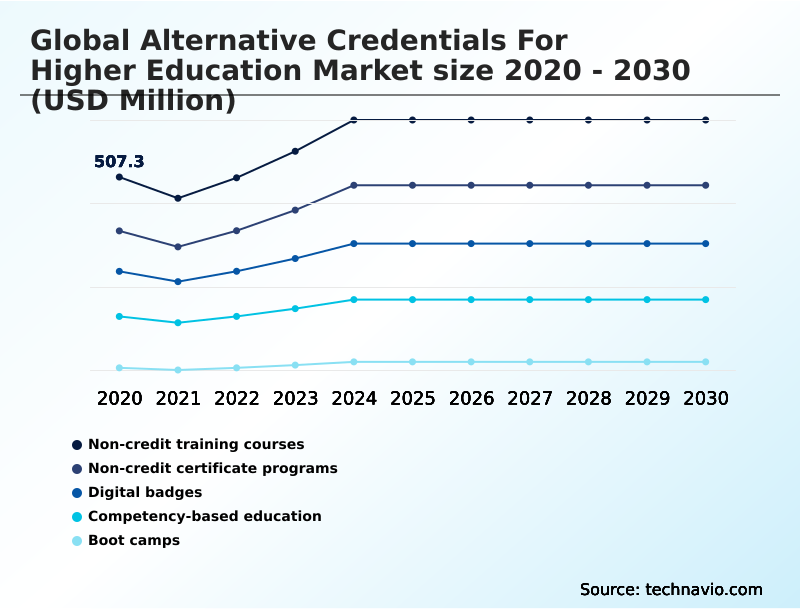

- Non-credit training courses

- Non-credit certificate programs

- Digital badges

- Competency-based education

- Boot camps

- Type

- Online

- Blended

- Face to face

- End-user

- Working professionals

- Students

- Lifelong learners

- Government and institutional

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Product Insights

The non-credit training courses segment is estimated to witness significant growth during the forecast period.

The non-credit training courses segment is a vital component of the modern educational ecosystem, offering rapid, focused learning opportunities that do not lead to traditional degrees.

These courses cater to professionals seeking to update specific skill sets through competency-based education, a key part of workforce development. The demand is driven by rapid technological change, necessitating continuous upskilling and reskilling to maintain professional relevance.

Institutions and e-learning platforms offer these courses to bridge the gap between formal education and immediate labor market needs, with learners reporting a 25% faster skill acquisition rate.

This flexibility in vocational training, supported by alternative credentialing platforms and robust learning management system integrations, is enhanced by online proctoring and certification preparation services.

The Non-credit training courses segment was valued at USD 641.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 51.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Alternative Credentials For Higher Education Market Demand is Rising in North America Get Free Sample

Geographically, North America dominates the market, accounting for 51.8% of the growth opportunity, driven by a mature corporate ecosystem and high institutional innovation.

Europe is distinguished by its strong emphasis on regulatory standards and cross-border portability, with a projected CAGR of 19.6%. The region's focus on quality assurance frameworks and institutional effectiveness supports the value of online degree programs.

The APAC region is characterized by rapid digital transformation and a demographic push toward skill-based employment, with governments integrating non-traditional education into national policies.

This focus on career-focused learning and educational technology helps address massive skills gaps, while South America and the Middle East and Africa are also embracing these models for economic empowerment and diversification.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of alternative credentials in corporate training hinges on resolving complex issues around their practical implementation and perceived value. Assessing the ROI of non-degree certifications is a critical exercise for organizations, as the impact of micro-credentials on employability becomes a key metric for both learners and hiring managers.

- This is driving the integration of professional certifications into university curricula, creating hybrid models where academic theory meets practical skill. The role of AI in personalized learning pathways is transformative, tailoring education to individual needs, yet it raises questions about quality assurance in online certification programs.

- Concurrently, blockchain in higher education credentialing offers a technical solution to trust and verification, helping individuals learn how to build a verifiable digital portfolio. However, challenges in cross-border recognition of micro-credentials persist. The success of stackable credentials for career advancement depends on government frameworks for digital identity in education, which can standardize recognition.

- Ultimately, the debate over competency-based education versus traditional degrees is being reshaped by effective blended learning models for professional development, which are showing over 20% higher completion rates than purely online formats by combining flexibility with structured, hands-on engagement, thus addressing the core need for alternative credentials for workforce reskilling.

What are the key market drivers leading to the rise in the adoption of Alternative Credentials For Higher Education Industry?

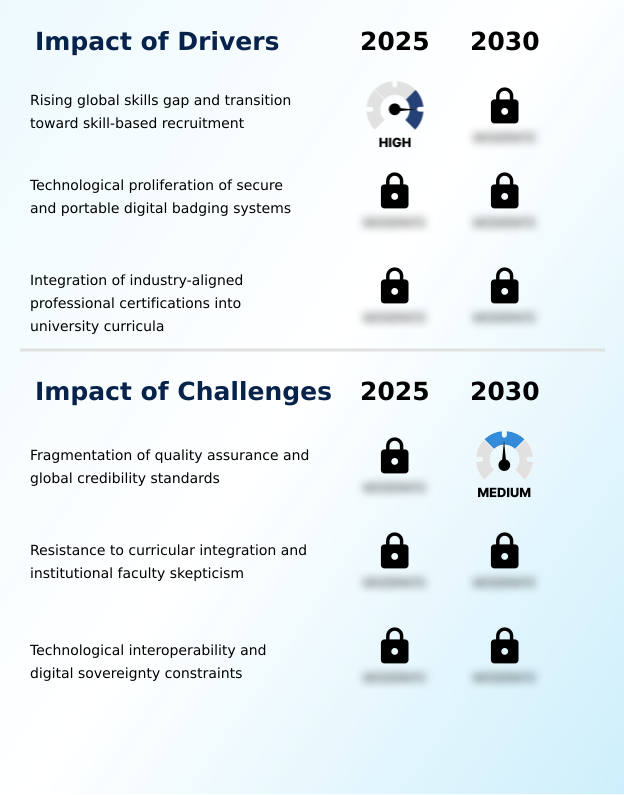

- The market's growth is primarily driven by the rising global skills gap and the corresponding transition toward skill-based recruitment practices.

- The primary driver is the widening disconnect between traditional academic output and modern labor force requirements, fueling a shift toward skill-based hiring. Alternative credentials, including professional certifications, offer a rapid solution to talent shortages.

- Secure digital badging systems, leveraging the open badges standard and blockchain, ensure the security and portability of educational achievements, increasing trust by 40% among recruiters. This allows learners to build a verifiable digital credentials portfolio.

- Furthermore, the integration of industry-aligned professional certifications into university curricula through blended learning models enhances student employability. These corporate training solutions ensure graduates possess the precise skills required, promoting lifelong learning pathways.

What are the market trends shaping the Alternative Credentials For Higher Education Industry?

- A key market trend is the integration of generative AI to create hyper-personalized credentialing pathways. This enables adaptive learning experiences tailored to individual skill levels and career goals.

- A pivotal trend is the use of generative AI for hyper-personalized credentialing pathways, creating bespoke learning experiences. This personalized learning approach moves beyond static curricula, with platforms curating module sequences based on existing knowledge, boosting learning efficiency by up to 30%.

- The rise of stackable credentials and credit transfer frameworks allows small, discrete certifications to be accumulated for formal academic credit. This modular education approach, supported by government-led national frameworks and digital sovereignty registries using blockchain verification, enhances the value of nanodegree programs.

- This institutionalization of skill-based learning and theoretical education, supported by digital learning courses, is making alternative credentials a dynamic tool for career management and talent development.

What challenges does the Alternative Credentials For Higher Education Industry face during its growth?

- A key challenge impeding market growth is the fragmentation of quality assurance and the absence of unified global credibility standards for credentials.

- A primary challenge is the absence of unified quality assurance frameworks, leading to confusion and the risk of credential inflation. This fragmentation makes it difficult for institutions to assess the rigor of certifications and for learners to navigate a saturated market. Institutional resistance and faculty skepticism slow the integration of micro-credentials into academic curricula.

- From a corporate perspective, many applicant tracking systems are still programmed to prioritize traditional degrees, creating a disconnect that hinders skill validation. This requires an overhaul of hiring protocols, where some firms have seen a 15% improvement in hiring diversity by adjusting filters.

- Finally, technological fragmentation and a lack of interoperability between continuing education units and student information systems create data silos, impeding the portability of a learner's complete academic transcripts.

Exclusive Technavio Analysis on Customer Landscape

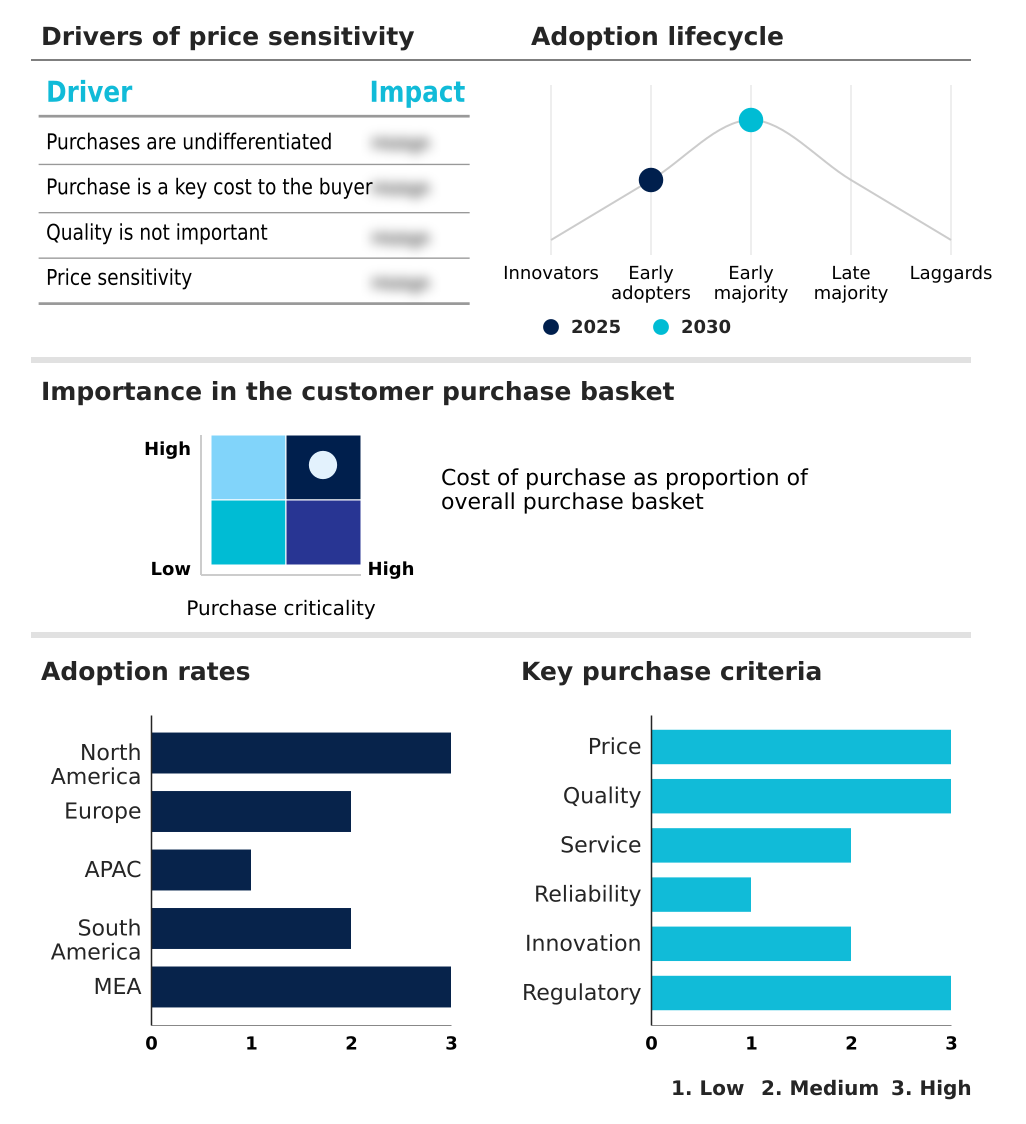

The alternative credentials for higher education market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the alternative credentials for higher education market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Alternative Credentials For Higher Education Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, alternative credentials for higher education market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

2U Inc. - Vendors provide diverse online degrees, professional certificates, and micro-credentials, meeting demands for lifelong learning and targeted workforce upskilling.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2U Inc.

- Accredible

- Anthology Inc.

- Coursera Inc.

- D2L Corp.

- Degreed Inc.

- Emeritus

- FutureLearn Ltd.

- Guild Education Inc.

- HolonIQ

- Instructure Holdings Inc.

- OpenClassrooms SAS

- Parchment Inc.

- Pearson Plc

- Pluralsight LLC

- Simplilearn Solutions Pvt. Ltd

- Skillsoft Corp.

- Udacity Inc.

- Udemy Inc.

- University of Michigan

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Alternative credentials for higher education market

- In February 2025, Microsoft Corporation launched a major initiative in North America that integrated its proprietary AI skill certifications directly into the hiring pipeline for its global partner network.

- In April 2025, Coursera, a major provider based in North America, introduced an advanced AI-powered Career Navigator tool.

- In March 2025, Coursera collaborated with the University of Melbourne to introduce a suite of stackable micro-credentials focused on climate resilience and sustainable infrastructure.

- In May 2025, 2U Inc. announced a new blended learning initiative in partnership with the University of North Carolina at Chapel Hill that combines online data science modules with mandatory monthly in-person laboratory sessions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Alternative Credentials For Higher Education Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.2% |

| Market growth 2026-2030 | USD 2616.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, South Africa, UAE, Saudi Arabia, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly maturing beyond a niche concept into a critical component of lifelong learning pathways and workforce development. The core of this transition is the demand for verifiable proof of skills, moving away from traditional proxies for competency.

- Key offerings like micro-credentials and digital badges, often secured through blockchain verification, are becoming standard elements of an individual's digital portfolio. This shift is driven by the need for continuous upskilling and reskilling in a dynamic job market. Institutions are responding by adopting more flexible models, including competency-based education and credit transfer frameworks that recognize non-traditional education.

- The integration of professional certifications into formal academic transcripts is a key development, often managed through a sophisticated learning management system with features like online proctoring. However, this proliferation creates challenges related to quality assurance frameworks and the potential for credential inflation, which can undermine trust in skill-based hiring.

- The move towards open badges standard and digital sovereignty shows a commitment to creating a more learner-centric ecosystem that bypasses outdated applicant tracking systems.

What are the Key Data Covered in this Alternative Credentials For Higher Education Market Research and Growth Report?

-

What is the expected growth of the Alternative Credentials For Higher Education Market between 2026 and 2030?

-

USD 2.62 billion, at a CAGR of 18.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Non-credit training courses, Non-credit certificate programs, Digital badges, Competency-based education, and Boot camps), Type (Online, Blended, and Face to face), End-user (Working professionals, Students, Lifelong learners, and Government and institutional) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising global skills gap and transition toward skill-based recruitment, Fragmentation of quality assurance and global credibility standards

-

-

Who are the major players in the Alternative Credentials For Higher Education Market?

-

2U Inc., Accredible, Anthology Inc., Coursera Inc., D2L Corp., Degreed Inc., Emeritus, FutureLearn Ltd., Guild Education Inc., HolonIQ, Instructure Holdings Inc., OpenClassrooms SAS, Parchment Inc., Pearson Plc, Pluralsight LLC, Simplilearn Solutions Pvt. Ltd, Skillsoft Corp., Udacity Inc., Udemy Inc. and University of Michigan

-

Market Research Insights

- Market dynamics are defined by a shift toward measurable skill validation, where verifiable digital credentials are a key currency. The adoption of alternative credentialing platforms has led to a 30% increase in engagement for corporate training solutions.

- This move toward career-focused learning is not just a trend but a response to employers' needs for specific competencies, with organizations that prioritize skill-based hiring reporting a 25% improvement in employee retention. The ecosystem, encompassing e-learning platforms and comprehensive student information systems, supports this transition.

- Institutional effectiveness is now partly measured by the ability to offer modular education, integrating digital learning courses and mentor-guided learning to prepare a job-ready workforce, enhancing alumni support services and overall talent development.

We can help! Our analysts can customize this alternative credentials for higher education market research report to meet your requirements.

RIA -

RIA -