Aluminum Cans Market Size 2024-2028

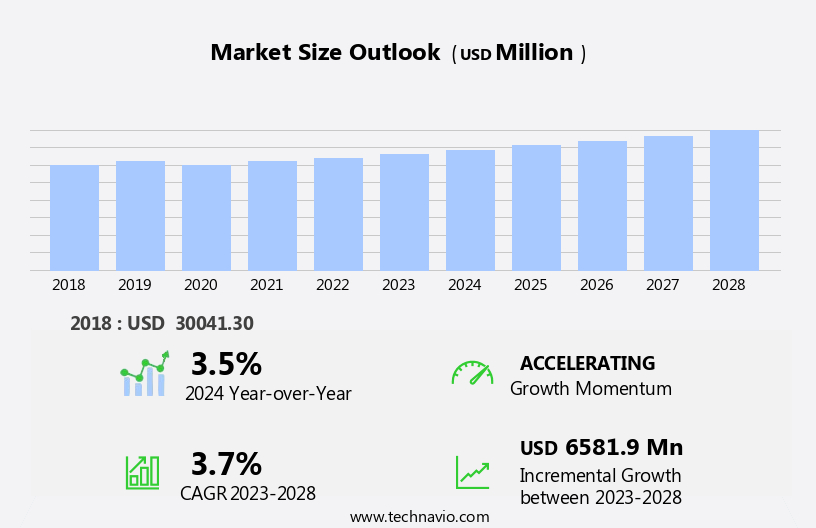

The aluminum cans market size is forecast to increase by USD 6.58 billion, at a CAGR of 3.7% between 2023 and 2028.

- The market is driven by the high recycling rate of aluminum, which makes it an attractive choice for beverage packaging due to its sustainability and environmental benefits. The increasing awareness of ready-to-drink (RTD) beverages, particularly in the health-conscious consumer segment, is a significant trend boosting market growth. However, the availability of substitutes, such as plastic and glass bottles, poses a challenge for aluminum can manufacturers. To capitalize on market opportunities, companies must focus on enhancing the unique selling propositions of aluminum cans, such as their lightweight, portable, and recyclable nature.

- Additionally, investments in research and development to create innovative designs and functionalities can help differentiate products and cater to evolving consumer preferences. Navigating the challenges of competition from substitutes requires strategic pricing and marketing efforts, as well as continuous improvement in production efficiency and sustainability initiatives.

What will be the Size of the Aluminum Cans Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and shifting consumer preferences. Protective coatings and surface treatments enhance can durability, ensuring superior corrosion resistance and impact resistance. Recycling processes, including post-consumer recycling, play a crucial role in the market's sustainability, with recycling rates reaching new heights. Manufacturing efficiency is a key focus, with innovations in can forming, printing processes, and can sizes streamlining production. Three-piece cans and two-piece cans each offer unique advantages, catering to various sectors such as beverage packaging and pharmaceutical packaging. Food safety remains a top priority, with stringent leakage testing and internal coatings ensuring product integrity.

Flexographic printing and digital printing offer versatility in decorating technologies, while distribution networks optimize supply chain efficiency. Aluminum alloys and can shapes are continually evolving to meet the demands of various industries, from aerosol cans to chemical packaging. Manufacturing processes, such as epoxy resins and lacquer application, contribute to the production of high-quality can bodies and can ends. Waste management and carbon footprint reduction are essential considerations, with ongoing research into more efficient can manufacturing and waste recycling methods. The market's continuous dynamism is further reflected in the adoption of advanced technologies, such as gravure printing, offset printing, and warehouse management systems, to enhance production capacity and shelf life.

How is this Aluminum Cans Industry segmented?

The aluminum cans industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Beverages

- Food

- Pharmaceuticals

- Chemical

- Others

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

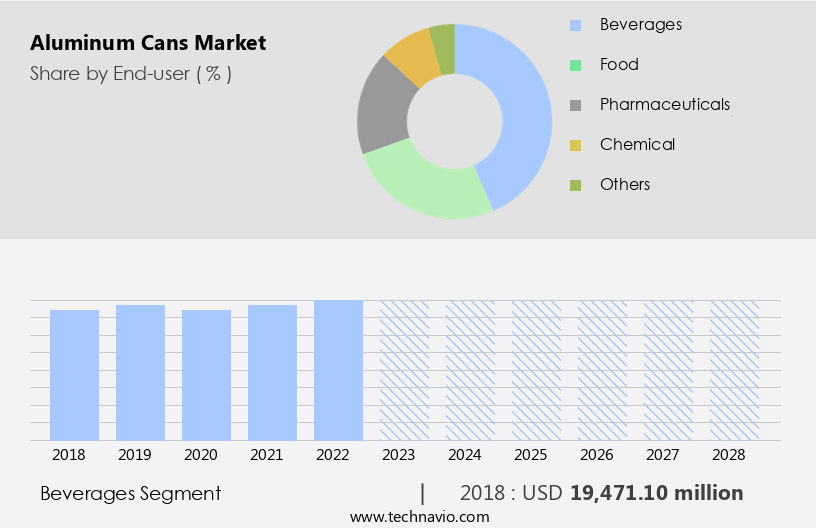

By End-user Insights

The beverages segment is estimated to witness significant growth during the forecast period.

The market experiences substantial growth, particularly in the food and beverage industry. Aluminum's inherent properties, such as lightweight, recyclability, and corrosion resistance, contribute to its popularity. In the beverage segment, aluminum cans account for a substantial market share, with carbonated soft drinks, beer, energy drinks, and ready-to-drink beverages leading the demand. Consumer preferences lean towards sustainable packaging solutions, making aluminum cans an attractive choice due to their high recyclability and ability to be reused without loss of quality. Furthermore, the convenience and portability of aluminum cans cater to modern consumers' active lifestyles, especially among younger demographics. Manufacturing processes, such as end forming, printing, and surface treatment, ensure the production of high-quality aluminum cans.

Protective coatings and can coatings enhance the cans' durability and resistance to external factors. Leakage testing guarantees the integrity of the containers, while food safety regulations ensure the safety of the contents. Recycling processes play a crucial role in the market, with post-consumer recycling contributing significantly to the supply chain. Waste management and inventory management systems optimize the recycling process, increasing recycling rates and reducing the need for new aluminum ingots. Aerosol cans and three-piece cans also contribute to the market's growth, with applications in various industries, including pharmaceuticals, food, and household products. Product lifecycle management and can manufacturing processes ensure efficient production and timely delivery.

In the food packaging sector, aluminum cans' impact resistance, manufacturing efficiency, and stacking strength make them an ideal choice for various applications. Flexographic and gravure printing techniques allow for intricate designs and branding, while offset printing offers cost-effective mass production. Shelf life and distribution networks are essential considerations for the market, with epoxy resins and can lids contributing to extended product life and improved preservation. Can sizes and shapes cater to diverse consumer preferences, with two-piece and three-piece cans offering various advantages. The aluminum recycling process reduces the carbon footprint and environmental impact, making it an eco-friendly alternative to traditional packaging materials.

Material science advancements continue to improve aluminum's properties, enhancing its appeal in various industries.

The Beverages segment was valued at USD 19.47 billion in 2018 and showed a gradual increase during the forecast period.

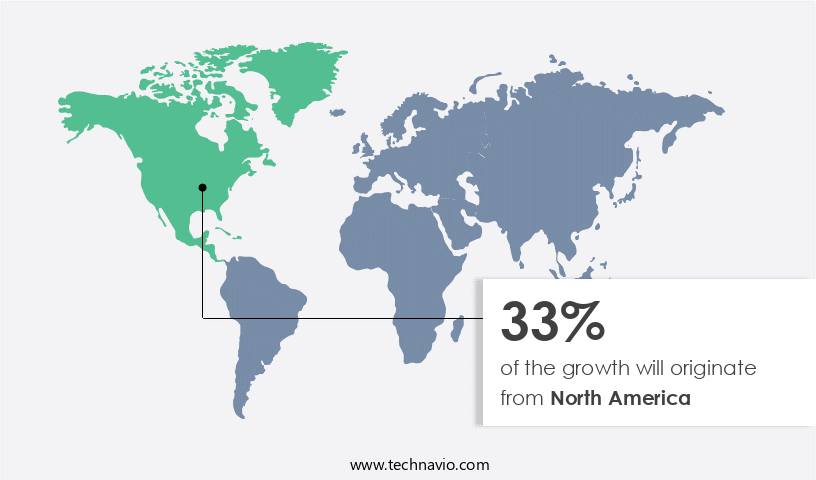

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American the market holds significant weight in the global aluminum packaging industry, fueled by the strong demand for beverage containers. This region is marked by an advanced aluminum can manufacturing infrastructure and a sizable consumer base that favors aluminum packaging, notably for beverages like soft drinks, beer, and energy drinks. The increasing consciousness towards environmental concerns has instigated a notable shift in consumer preferences towards eco-friendly packaging alternatives, thereby amplifying the demand for aluminum cans. Consumers' growing inclination towards reducing plastic usage is further fueling the popularity of aluminum cans across various beverage categories. Protective coatings and surface treatments ensure food safety and impact resistance, while manufacturing efficiency is a critical factor in maintaining competitiveness.

Can shapes and sizes cater to diverse consumer preferences and product requirements. Post-consumer recycling plays a vital role in the market's sustainability, with recycling rates continuing to rise. Advanced printing techniques, such as flexographic, gravure, offset, and digital printing, offer various decorating options for can bodies and ends. Waste management and inventory management systems optimize production capacity and distribution networks. Aerosol cans and epoxy resins contribute to the market's versatility, with product lifecycle management ensuring consistent quality and innovation. Aluminum alloys, can lids, and aluminum ingots form the market's raw material base. Corrosion resistance and internal coatings are essential for maintaining the longevity and functionality of aluminum cans.

Pharmaceutical and beverage packaging applications expand the market's scope, with production capacity and stacking strength crucial factors in meeting demand. Consumer preferences and material science continue to influence market trends, with can manufacturing processes evolving to meet these demands. The supply chain encompasses various stakeholders, from raw material suppliers to distributors and retailers. Two-piece and three-piece cans cater to different market segments, with shelf life and carbon footprint becoming increasingly important considerations. Decorating technologies and packaging design play a significant role in product differentiation and consumer appeal. The market's evolving dynamics reflect the ongoing innovation and adaptability of aluminum can manufacturing.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Aluminum Cans Industry?

- The high recycling rate of aluminum plays a pivotal role in driving the market for this metal due to its sustainability and cost-effectiveness in production.

- The market experiences steady growth due to several factors. One of the most significant drivers is the high recycling rate of aluminum cans, which positively impacts the industry. Globally, aluminum cans have one of the highest recycling rates, with the US rate at approximately 69% and Europe's exceeding 73%. This impressive performance is due to aluminum's economic viability as a valuable material that can be recycled repeatedly without losing quality. Another factor contributing to the market's growth is the development of advanced can bodies, ends, and distribution networks. These innovations have led to improvements in can sizes, shelf life, and decorating technologies, making aluminum cans an increasingly popular choice for packaging various beverages and food products.

- Furthermore, the focus on reducing carbon footprint and utilizing chemical packaging alternatives has led to increased demand for aluminum cans. Aluminum recycling not only benefits the environment but also enhances market prospects by reducing the need for new raw materials and energy consumption in the supply chain.

What are the market trends shaping the Aluminum Cans Industry?

- The awareness of RTD beverages is gaining significant momentum in the market. It is an emerging trend for professionals to prioritize convenient and on-the-go consumption options, making RTD beverages an increasingly popular choice.

- The market experiences significant growth due to the increasing popularity of ready-to-drink (RTD) beverages. Consumers' shifting preferences towards convenience and innovative offerings have driven the RTD beverage sector's explosive growth in recent years. This trend is particularly noticeable among younger demographics, such as millennials and Gen Z, who prioritize convenience and quality in their beverage choices. One of the primary factors fueling the rise of RTD beverages is the growing emphasis on convenience. With consumers leading increasingly busy lives, there is a strong demand for products that fit seamlessly into their routines. Aluminum cans offer several advantages in this regard, including protective coatings for preserving the product's taste and freshness, efficient end forming and printing processes, and impact resistance for on-the-go consumption.

- Recycling processes also play a crucial role in the market, as sustainability becomes an increasingly important consideration for consumers. The recycling process for aluminum cans is cost-effective and environmentally friendly, making it an attractive choice for both manufacturers and consumers. Surface treatment and can coatings are essential components of the manufacturing process, ensuring food safety and leakage testing. Flexographic printing processes enable high-quality, vibrant graphics on the cans, enhancing their appeal to consumers. Manufacturing efficiency is another critical factor, as aluminum cans offer faster production times compared to glass or plastic containers. Effective waste management is also a priority in the market, as sustainability becomes a more significant concern for consumers and governments.

- Aluminum cans are infinitely recyclable, making them an attractive choice for environmentally-conscious consumers and manufacturers alike.

What challenges does the Aluminum Cans Industry face during its growth?

- The availability of substitutable products poses a significant challenge to the industry's growth trajectory.

- The market faces challenges from substitutes, primarily PET plastic, which could negatively impact its growth and market share. Aluminum cans have gained popularity due to their recyclability and protective qualities in the beverage industry. However, PET bottles offer advantages such as lightweight nature, lower production costs, and perceived environmental benefits. Advancements in PET technology have led to the development of sustainable options, like bottles made from recycled materials, making them increasingly attractive. Recycling rates play a crucial role in the market dynamics, with gravure printing and offset printing used in can manufacturing. Warehouse management, inventory management, and product lifecycle management are essential for optimizing operations in the industry.

- Aluminum alloys and can shapes vary, with aerosol cans and can lids requiring specific considerations. Epoxy resins are used in can coatings to improve durability and protect against corrosion. Demand forecasting is essential to ensure adequate inventory levels and meet customer needs while minimizing waste.

Exclusive Customer Landscape

The aluminum cans market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aluminum cans market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aluminum cans market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Amcor, a leading packaging solutions provider, innovatively manufactures aluminum cans through the integration of multiple substrates and polymers, ensuring efficient production. The easy-peel membrane, a distinctive feature under the Amcor brand, offers both consumer convenience and product integrity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Ardagh Group SA

- Ball Corp.

- BangkokCan Manufacturing Co. Ltd.

- Baosteel Group Corp.

- CANPACK SA

- COFCO Corp.

- Crown Holdings Inc.

- Envases Group

- GZ Industries Ltd.

- Hindalco Industries Ltd.

- Kian Joo Can Factory Bhd

- Mahmood Saeed Co. Ltd.

- Nampak Ltd.

- Norsk Hydro ASA

- Orora Ltd.

- Resonac Holdings Corp.

- Silgan Containers LLC

- SWAN Industries Thailand Ltd.

- The Aluminum Association

- Toyo Seikan Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aluminum Cans Market

- In January 2024, Ball Corporation, a leading aluminum packaging solutions provider, announced the expansion of its beverage can production line in Thailand. The USD150 million investment was aimed at increasing the company's annual production capacity by 12 billion cans (Ball Corporation Press Release, 2024).

- In March 2024, Novelis, the world's largest aluminum rolling and recycling company, and Coca-Cola European Partners (CCEP), one of the world's largest Coca-Cola bottlers, formed a strategic partnership to advance the circular economy for aluminum beverage cans in Europe. The collaboration aimed to increase the use of recycled aluminum in CCEP's cans (Novelis Press Release, 2024).

- In May 2024, Ardagh Metal Packaging, a global metal packaging solutions provider, completed the acquisition of Constellation Brands' metal beverage can business. The deal expanded Ardagh's North American footprint and added significant beverage can manufacturing capacity (Ardagh Metal Packaging Press Release, 2024).

- In February 2025, the European Union (EU) approved a new regulation to reduce the use of single-use plastics, including plastic beverage bottles, by 25% by 2025. The regulation is expected to drive significant growth in the aluminum can market due to their recyclability and sustainability advantages (European Commission Press Release, 2025).

Research Analyst Overview

- In the dynamic the market, sustainability and social responsibility are increasingly shaping consumer behavior. Brands prioritize sustainable packaging solutions, such as aluminum cans, which offer excellent recyclability and reduced environmental impact. Can sealing and testing play crucial roles in maintaining product quality and ensuring regulatory compliance. Automated systems and advanced packaging machinery minimize energy consumption and optimize cost, while supplier relationships are vital for securing high-quality alloys and raw materials. Defect detection and quality control are essential to prevent production line disruptions and maintain brand loyalty. The circular economy and regulatory compliance drive innovation in areas like electrolytic coating, emission reduction, and water usage.

- Can fillers and material sourcing strategies are under scrutiny, with a focus on reducing waste and improving production efficiency. The aluminum can market continues to evolve, with ongoing advancements in packaging technology, such as UV curing and printing inks, and the implementation of stringent transport regulations. Price sensitivity remains a key consideration, as cost optimization strategies and metal fabrication techniques, like powder coating, are adopted to remain competitive.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aluminum Cans Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.7% |

|

Market growth 2024-2028 |

USD 6581.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.5 |

|

Key countries |

US, China, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aluminum Cans Market Research and Growth Report?

- CAGR of the Aluminum Cans industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aluminum cans market growth of industry companies

We can help! Our analysts can customize this aluminum cans market research report to meet your requirements.

RIA -

RIA -