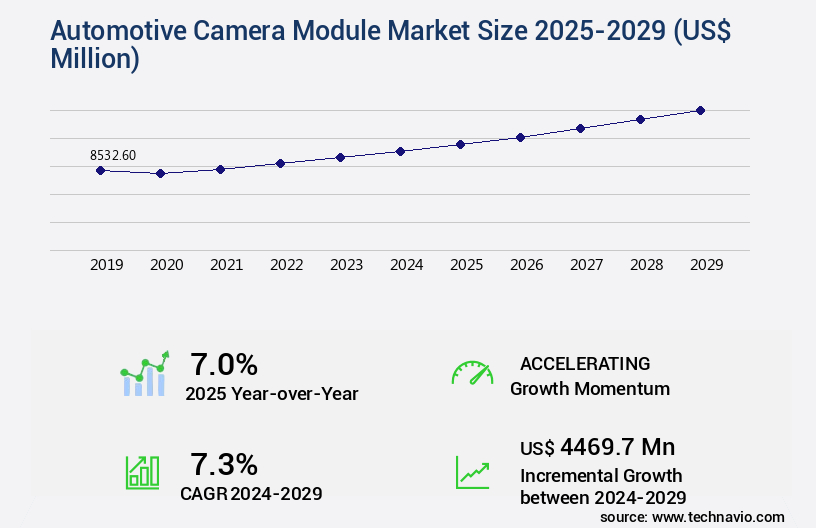

Automotive Camera Module Market Size 2025-2029

The automotive camera module market size is valued to increase USD 4.47 billion, at a CAGR of 7.3% from 2024 to 2029. Rising demand for ADAS will drive the automotive camera module market.

Major Market Trends & Insights

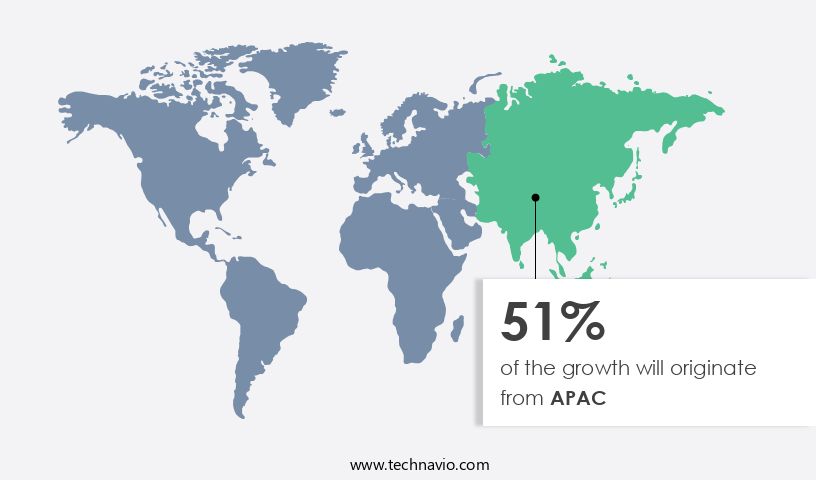

- APAC dominated the market and accounted for a 51% growth during the forecast period.

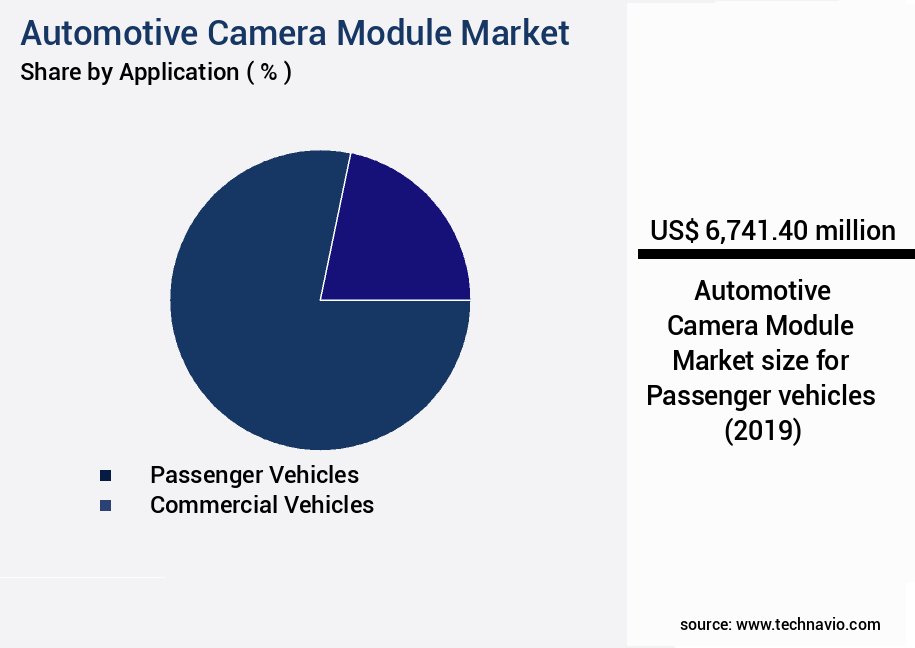

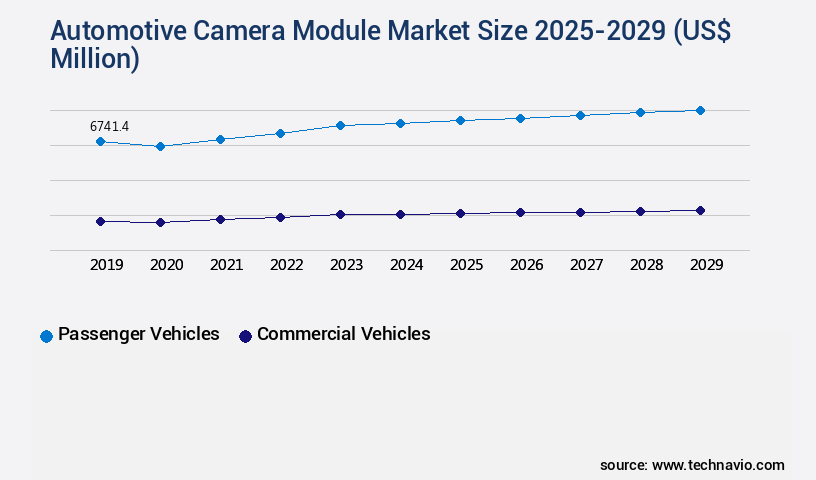

- By Application - Passenger vehicles segment was valued at USD 6.74 billion in 2023

- By Technology - Mono camera segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 76.61 million

- Market Future Opportunities: USD 4469.70 million

- CAGR : 7.3%

- APAC: Largest market in 2023

Market Summary

- The market represents a dynamic and evolving industry, driven by the increasing demand for advanced driver-assistance systems (ADAS) and the emphasis on safety and convenience in modern vehicles. Core technologies, such as image processing algorithms and high-definition sensors, continue to advance, enabling superior image quality and real-time data processing. Applications, including surround view systems, lane departure warnings, and blind spot detection, are gaining traction, leading to a growing market. Service types, including design, manufacturing, and integration, are also experiencing innovation, with an emphasis on new product launches and customization. Regulations, such as the European Union's General Safety Regulation, further fuel market growth by mandating the installation of specific safety features.

- Despite these opportunities, challenges persist, including supply chain and semiconductor shortages. According to recent reports, the market is expected to account for over 25% of the total ADAS market by 2025, underscoring its significance in the automotive industry. Related markets such as the LiDAR and Radar Sensor Market also show promising growth.

What will be the Size of the Automotive Camera Module Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive Camera Module Market Segmented and what are the key trends of market segmentation?

The automotive camera module industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Passenger vehicles

- Commercial vehicles

- Technology

- Mono camera

- Stereo camera

- Infrared camera

- Thermal camera

- Type

- Park assist cameras

- Surround view cameras

- Driver monitoring cameras

- Blind spot detection cameras

- Forward collision warning cameras

- Geography

- North America

- US

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The passenger vehicles segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, with passenger vehicles leading the application segment. This dominance is driven by escalating consumer demands for advanced safety and convenience features, coupled with regulatory mandates promoting the integration of camera-based systems in various vehicle classes. In 2024, global passenger car sales surged by 2.5%, reaching 74.6 million units, as reported by the European Automobile Manufacturers Association. Regional markets demonstrated varying growth trends, with Europe recording a 3.9% increase to 16.1 million units, the United States expanding by 3.1% to 12.7 million units, and India witnessing a 4% growth to 3.8 million units.

Key features of automotive camera modules include shutter speed control, blind spot detection, aperture control systems, power consumption metrics, image compression techniques, automotive camera calibration, depth sensing technology, automated emergency braking, image sensor technology, ADAS camera systems, waterproof camera modules, optical image stabilization, computer vision systems, lane departure warning, low-light image quality, electromagnetic shielding, focus mechanisms, vibration resistance, night vision performance, parking assist systems, object detection algorithms, surround view systems, lens module designs, automotive camera testing, automotive camera housing, temperature compensation, high-resolution imaging, CMOS image sensors, image distortion correction, infrared imaging technology, camera module integration, real-time image processing, driver monitoring systems, image signal processing, and forward collision warning.

Moreover, the market anticipates continuous innovation in areas such as advanced image processing techniques, enhanced sensor technologies, and sophisticated software algorithms. These advancements are expected to fuel future growth, with industry experts projecting a 15% increase in demand for automotive camera modules by 2028. Furthermore, the integration of camera modules in electric and autonomous vehicles is poised to create new opportunities, as these vehicles rely heavily on advanced imaging technologies for navigation and safety systems.

The Passenger vehicles segment was valued at USD 6.74 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 51% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Camera Module Market Demand is Rising in APAC Request Free Sample

The Asia-Pacific (APAC) region is currently leading The market, driven by stringent government regulations, rapid electric vehicle (EV) adoption, cost-effective manufacturing, and technological innovation. China, Japan, South Korea, India, and emerging ASEAN markets are key contributors to this dominance. Government regulations, such as China's GB standards, mandate the inclusion of automatic emergency braking (AEB), lane-keeping assist, and rearview cameras in all new vehicles from 2025. APAC is both the largest manufacturing hub and the fastest-growing consumer base for camera-based automotive safety systems. With over 60% market share, China is at the forefront of this trend, followed by Japan and South Korea.

India and ASEAN markets are also witnessing significant growth, driven by increasing demand for advanced safety features. As of 2021, APAC accounted for approximately 65% of the global production volume of camera modules. This trend is expected to continue, with the region's market size projected to reach 25.4 billion USD by 2026, growing at a steady pace.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for advanced driver-assistance systems (ADAS) and driver monitoring systems (DMS) in modern vehicles. High-resolution CMOS image sensors are becoming the norm in automotive applications, necessitating thermal management solutions to ensure optimal performance and reliability. Integrating these cameras into ADAS and DMS poses challenges, requiring sophisticated image signal processing algorithms for real-time object detection and low-light performance optimization. Functional safety requirements for automotive camera systems mandate stringent environmental testing procedures, including wide dynamic range imaging techniques and image distortion correction methods. Power consumption reduction strategies and cost-effective manufacturing are also critical factors driving market growth.

Infrared imaging technology and depth sensing technology are gaining popularity in advanced parking assist systems and ADAS, respectively. Advanced image processing algorithms, such as software-defined architectures and high-speed data transmission, enable real-time object detection and improved reliability. Functional safety and cybersecurity measures are essential to ensure data privacy and vehicle safety. According to recent market research, thermal management solutions accounted for 15% of the market in 2020, with a projected CAGR of 12% from 2021 to 2026. In contrast, image signal processing algorithms are expected to grow at a CAGR of 18% during the same period.

These trends reflect the market's dynamics, with a focus on enhancing safety, reliability, and efficiency in automotive camera systems.

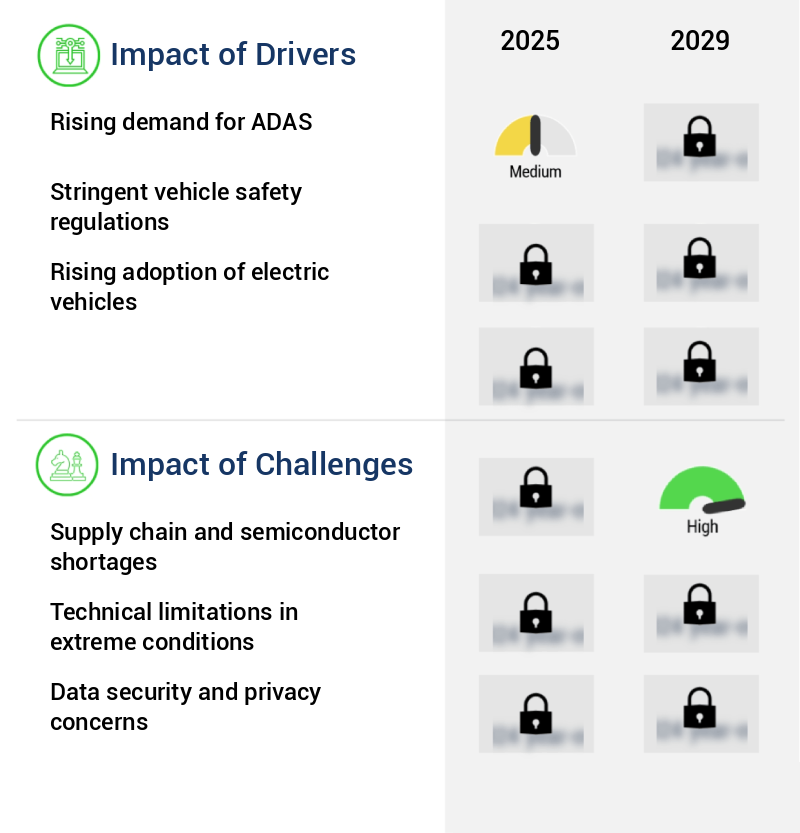

What are the key market drivers leading to the rise in the adoption of Automotive Camera Module Industry?

- The increasing demand for Advanced Driver-Assistance Systems (ADAS) serves as the primary market driver.

- Advanced Driver Assistance Systems (ADAS) have gained significant traction in the automotive industry due to the increasing prioritization of road safety and accident prevention. These systems leverage automotive camera modules and camera-based technologies to monitor a vehicle's surroundings, enabling features like lane departure warning, adaptive cruise control, traffic sign recognition, and automatic emergency braking. The widespread adoption of these technologies is not confined to premium vehicles alone; mid-range and economy models increasingly incorporate camera-based safety features, signifying a shift in consumer preferences.

- As ADAS technologies continue to evolve and become more accessible, they offer enhanced safety and convenience across various vehicle segments. The integration of these advanced systems is a testament to the industry's commitment to improving road safety and meeting evolving consumer demands.

What are the market trends shaping the Automotive Camera Module Industry?

- The emphasis on new product launches represents the current market trend. New product launches are a significant focus in today's business landscape.

- The global automotive camera market is experiencing significant innovation, with a focus on new product launches. Manufacturers are introducing advanced camera modules, integrating high-resolution sensors and dynamic range technology for use in autonomous driving platforms. In September 2024, SENSING unveiled the SG3-AR0341C-G2F-H190X, an ultra-compact 3MP camera module. Featuring a 150 dB high dynamic range, LED flicker mitigation, and ultra-low power consumption, this module is optimized for advanced driver-assistance systems (ADAS) and autonomous driving systems.

- Its compatibility with NVIDIA DRIVE AGX Orin and Jetson AGX Orin platforms enables seamless integration into intelligent vehicle architectures. This trend underscores the continuous evolution of automotive imaging technology and the growing importance of camera modules in the development of advanced driving systems.

What challenges does the Automotive Camera Module Industry face during its growth?

- The semiconductor supply chain shortages pose a significant challenge to the industry's growth. This issue, which has gained prominence in recent times, hinders the expansion and productivity of various sectors that heavily rely on semiconductors, including technology, automotive, and healthcare industries. The ripple effect of this challenge is felt in the form of increased production costs, delayed product releases, and decreased competitiveness for businesses. Addressing this complex issue requires collaborative efforts from all stakeholders, including governments, manufacturers, and consumers, to ensure a sustainable and resilient semiconductor supply chain.

- The market faces persistent challenges from supply chain disruptions and semiconductor shortages. These issues have significant implications for production timelines and cost structures. Camera modules require specialized components, such as high-resolution CMOS image sensors, automotive-grade processors, and precision optical lenses. The availability of these components is limited due to semiconductor fabrication capacity constraints and geopolitical trade tensions. The COVID-19 pandemic highlighted the risks of just-in-time manufacturing models, with extended lead times for certain chips reaching up to 24 months. By 2024, legacy process nodes like 40nm to 90nm, commonly used in automotive-grade chips, will remain in short supply.

- Foundries prioritize advanced nodes for consumer electronics and artificial intelligence applications. Despite these challenges, the market continues to evolve, with advancements in technologies like LiDAR and computer vision driving demand for more sophisticated camera modules in autonomous vehicles. The market's dynamics are influenced by factors such as increasing regulatory focus on safety features and growing consumer preferences for advanced driver assistance systems.

Exclusive Customer Landscape

The automotive camera module market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive camera module market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Camera Module Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive camera module market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ambarella Inc. - This company specializes in manufacturing advanced automotive camera modules, including front ADAS cameras, enhancing vehicle safety systems for various automobile manufacturers. Their cutting-edge technology ensures superior image quality and reliable performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ambarella Inc.

- ams OSRAM AG

- Aptiv Plc

- ASMPT Ltd.

- Astemo Ltd

- Continental AG

- DENSO Corp.

- Kappa optronics GmbH

- KYOCERA Corp.

- LG Innotek Co. Ltd.

- Magna International Inc.

- Mcnex Co. Ltd.

- Motherson Group

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- Stonkam Co. Ltd.

- Valeo SA

- Veoneer Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Camera Module Market

- In January 2024, Magna International, a leading automotive technology supplier, announced the launch of its new advanced driver assistance system (ADAS) camera module, "VistaPro," which features a high-resolution fish-eye camera and a wide-angle monocle camera. This innovative solution enhances object detection and recognition capabilities, improving overall vehicle safety (Magna International Press Release).

- In March 2024, Continental AG and Aptiv, two leading automotive technology companies, announced a strategic partnership to develop and manufacture integrated driver assistance systems (ADAS) and autonomous driving technologies. This collaboration combines Continental's expertise in ADAS and Aptiv's experience in vehicle electrification and connectivity, aiming to create a comprehensive, end-to-end solution for advanced driver assistance and autonomous driving systems (Continental AG Press Release).

- In May 2024, Bosch Sensortec, a leading sensor technology provider, secured a €150 million investment from the European Investment Bank (EIB) to expand its production capacity for automotive sensors, including camera modules. This investment supports the growing demand for advanced driver assistance systems (ADAS) and autonomous driving technologies (European Investment Bank Press Release).

- In April 2025, the European Union (EU) passed the "Regulation on Type Approval of Motor Vehicles with respect to Automated Driving Systems" (R167). This regulation sets safety and performance standards for automated driving systems, including the use of multiple cameras for object detection and recognition. The regulation is expected to significantly boost the demand for advanced camera modules in European automotive markets (European Parliament Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Camera Module Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

244 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.3% |

|

Market growth 2025-2029 |

USD 4469.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.0 |

|

Key countries |

China, US, Japan, Germany, South Korea, France, India, UK, Mexico, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive camera market is a dynamic and evolving landscape, with ongoing advancements shaping the industry's future. Shutter speed control and aperture control systems are increasingly integrated into automotive camera modules to enhance image quality, particularly in low-light conditions. Power consumption metrics are a critical concern, with image compression techniques and automotive camera calibration playing essential roles in optimizing energy efficiency. Depth sensing technology, such as LiDAR and radar, complements traditional camera systems, enabling advanced driver assistance systems (ADAS) like blind spot detection, lane departure warning, and automated emergency braking. Waterproof camera modules and optical image stabilization ensure reliable performance in various weather conditions and during vehicle movement.

- Computer vision systems and object detection algorithms are at the forefront of innovation, enabling features like parking assist systems and surround view systems. Lens module design, automotive camera testing, and housing are crucial aspects of ensuring robustness and durability, with temperature compensation and electromagnetic shielding addressing environmental challenges. High-resolution imaging, achieved through CMOS image sensors and real-time image processing, is a key differentiator in the market. Infrared imaging technology offers additional benefits, such as night vision performance and driver monitoring systems. Image signal processing and focus mechanism enhancements contribute to improved image quality and vibration resistance. The ongoing integration of camera modules into various vehicle systems continues to expand, with ongoing research in areas like image distortion correction and camera module integration.

- The future of the automotive camera market lies in the convergence of advanced technologies, enabling safer, more efficient, and more comfortable driving experiences.

What are the Key Data Covered in this Automotive Camera Module Market Research and Growth Report?

-

What is the expected growth of the Automotive Camera Module Market between 2025 and 2029?

-

USD 4.47 billion, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Passenger vehicles and Commercial vehicles), Technology (Mono camera, Stereo camera, Infrared camera, and Thermal camera), Type (Park assist cameras, Surround view cameras, Driver monitoring cameras, Blind spot detection cameras, and Forward collision warning cameras), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for ADAS, Supply chain and semiconductor shortages

-

-

Who are the major players in the Automotive Camera Module Market?

-

Key Companies Ambarella Inc., ams OSRAM AG, Aptiv Plc, ASMPT Ltd., Astemo Ltd, Continental AG, DENSO Corp., Kappa optronics GmbH, KYOCERA Corp., LG Innotek Co. Ltd., Magna International Inc., Mcnex Co. Ltd., Motherson Group, Panasonic Holdings Corp., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Sony Group Corp., Stonkam Co. Ltd., Valeo SA, and Veoneer Inc.

-

Market Research Insights

- The market is characterized by continuous innovation and advancement, driven by the increasing demand for enhanced safety and driver assistance systems in vehicles. Two key performance indicators underscore this trend. First, the number of camera modules per vehicle has risen from an average of 2.5 in 2015 to an estimated 5.5 in 2025. Second, the average resolution of these modules has increased from 1.3 megapixels to 12 megapixels over the same period. To meet the stringent requirements of the automotive industry, camera modules must offer superior dynamic range expansion, data security features, power efficiency, and reliability.

- Manufacturers employ various techniques, such as pixel binning, sharpness enhancement, and contrast enhancement, to improve image quality. Additionally, functional safety standards, such as ISO 26262, mandate rigorous testing for durability, motion blur reduction, and thermal management. Camera modules must also comply with various environmental and ingress protection ratings, as well as data transmission protocols like CAN bus and Lin bus interfaces. Processing power, memory capacity, and system latency are critical factors, as real-time image processing is essential for effective driver assistance. Furthermore, camera lens coatings, sensor noise reduction, and HDR image processing contribute to improved image quality under various lighting conditions.

- In summary, the market is marked by a relentless pursuit of technological advancements, with a focus on enhancing image quality, power efficiency, and safety features. These innovations are driven by the growing demand for advanced driver assistance systems and the evolving regulatory landscape.

We can help! Our analysts can customize this automotive camera module market research report to meet your requirements.

RIA -

RIA -