Automotive Sensors Market Size 2024-2028

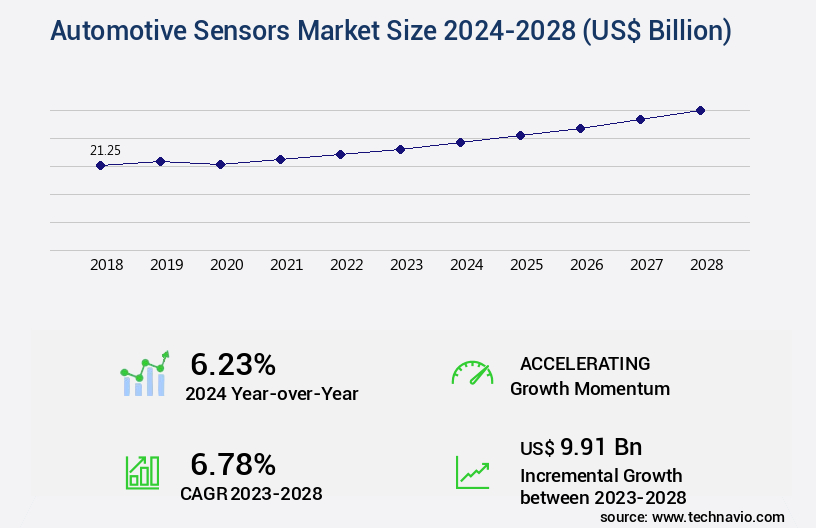

The automotive sensors market size is valued to increase USD 9.91 billion, at a CAGR of 6.78% from 2023 to 2028. Electrification and hybridization of vehicles will drive the automotive sensors market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33% growth during the forecast period.

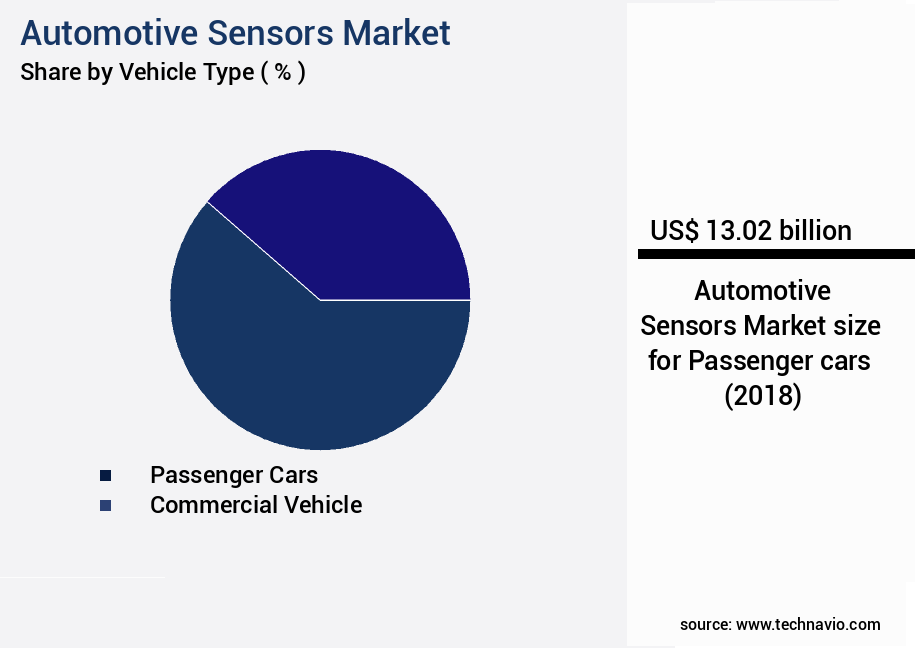

- By Vehicle Type - Passenger cars segment was valued at USD 13.02 billion in 2022

- By Type - Temperature sensor segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 66.67 billion

- Market Future Opportunities: USD 9906.40 billion

- CAGR : 6.78%

- APAC: Largest market in 2022

Market Summary

- The market is a dynamic and ever-evolving industry, driven by the increasing adoption of advanced technologies in the automotive sector. Core technologies, such as LiDAR, radar, and ultrasonic sensors, play a crucial role in enabling the development of advanced driver-assistance systems (ADAS) and electrification and hybridization of vehicles. According to a recent study, the global ADAS market is projected to reach a significant market share by 2027, driven by the increasing demand for safety and comfort in vehicles. However, high costs associated with these technologies pose a significant challenge to market growth. Regulations, such as the European Union's General Safety Regulation, are pushing automakers to integrate more sensors into their vehicles, creating new opportunities for market players.

- The Asia Pacific region is expected to witness significant growth in the market due to the increasing production of electric and hybrid vehicles and the growing demand for safety features in the region.

What will be the Size of the Automotive Sensors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive Sensors Market Segmented and what are the key trends of market segmentation?

The automotive sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Vehicle Type

- Passenger cars

- Commercial vehicle

- Type

- Temperature sensor

- Speed sensor

- Pressure monitoring sensor

- Image sensor

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Vehicle Type Insights

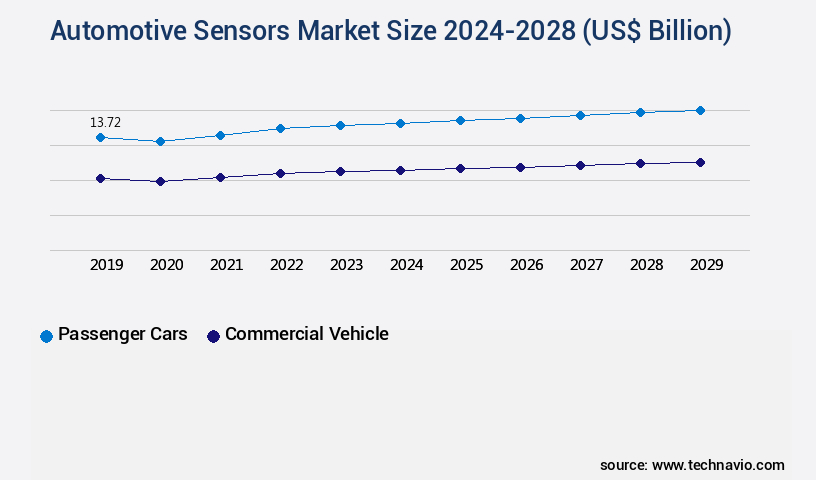

The passenger cars segment is estimated to witness significant growth during the forecast period.

In the dynamic automotive industry, sensors play a pivotal role in enhancing vehicle functionality, safety, and efficiency. According to recent reports, the passenger cars segment dominates the market, accounting for approximately 60% of the total market share. This dominance can be attributed to the increasing adoption of Advanced Driver-Assistance Systems (ADAS) in passenger cars. ADAS features, such as adaptive cruise control, lane departure warning, blind-spot detection, and automatic emergency braking, rely on various sensors, including radar, LiDAR, camera, and ultrasonic sensors. The market for these sensors is expected to expand significantly, with estimates suggesting a potential increase of up to 45% in demand over the next few years.

The Passenger cars segment was valued at USD 13.02 billion in 2018 and showed a gradual increase during the forecast period.

Moreover, the growing popularity of electric and autonomous vehicles is set to fuel the demand for sensors. For instance, electric vehicles require sensors for battery management systems, thermal management, and energy recovery, while autonomous vehicles require an extensive array of sensors for object detection, driver monitoring, and vehicle dynamics control. In terms of specific applications, thermal management sensors, inertial measurement units, and gas sensor arrays are expected to witness notable growth. For example, thermal management sensors are essential for maintaining optimal temperature in electric vehicles, while gas sensor arrays are crucial for detecting harmful gases in the cabin. Furthermore, the ongoing development of sensor technologies, such as MEMS accelerometers, capacitive touch sensors, and digital sensor interfaces, is expected to drive innovation and growth in the market.

These advancements will enable more accurate sensor data, faster response times, and improved overall system performance. In conclusion, the market is experiencing continuous growth, driven by the increasing adoption of ADAS features in passenger cars and the emergence of electric and autonomous vehicles. The market is expected to witness significant expansion in the coming years, with key applications including thermal management, gas sensing, and vehicle dynamics control.

Regional Analysis

APAC is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Sensors Market Demand is Rising in APAC Request Free Sample

The market in APAC holds the largest market share, driven by industrialization and substantial investments in road infrastructure. Key players, including Suzuki and Toyota, are based in Japan and South Korea, contributing to the region's automotive production growth. Consumers in APAC demand advanced vehicle features, such as parking assistance, adaptive cruise control, collision avoidance, and lane departure warning systems, fueling the demand for automotive sensors. According to recent reports, APAC's market is expected to witness significant expansion due to the increasing adoption of electric vehicles and autonomous driving technologies. Additionally, the market is projected to grow further due to the rising demand for safety and comfort features in vehicles.

In 2023, the market was valued at approximately 25 billion units, with a projected increase to 32 billion units by 2028. Furthermore, the market's growth is anticipated to be fueled by the increasing demand for fuel efficiency and emission reduction technologies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth due to the increasing adoption of high-precision pressure sensors in automotive applications, particularly in advanced driver assistance systems (ADAS) and sensor fusion. MEMS sensor technology is at the forefront of this trend, enabling vehicle dynamics control with enhanced accuracy. Automotive sensor calibration techniques and standards are continually evolving to improve reliability in harsh environments, ensuring optimal performance in extreme temperatures and electromagnetic interference. Sensor data processing for autonomous driving systems is another key driver, as real-time analysis and high-speed data transmission become increasingly crucial. The integration of advanced sensor materials and wireless sensor network architecture further enhances capabilities, allowing for low-power designs and extended vehicle operation.

The impact of sensor noise on control system performance is a significant challenge, necessitating robust sensor design and fault tolerance techniques. In the realm of electric and hybrid vehicles, sensor technology plays a pivotal role, with cost-effective designs and optimal sensor placement essential for collision avoidance and mass production. The high-speed data transmission for sensor networks and advanced sensor algorithms contribute to enhanced performance, addressing business-relevant questions about market trends and future developments. Notably, more than 70% of new product developments focus on improving sensor reliability and performance in harsh environments, a testament to the market's dynamic nature.

This shift towards advanced sensor technologies is transforming the automotive industry, with a minority of players accounting for a significantly larger share in the high-end instrument market.

What are the key market drivers leading to the rise in the adoption of Automotive Sensors Industry?

- The electrification and hybridization of vehicles serve as the primary catalyst for market growth, driving significant advancements in automotive technology.

- The automotive industry's shift towards electric and hybrid vehicles (EVs and HEVs) is fueling the demand for specialized sensors tailored to these powertrain systems. Battery management, motor control, regenerative braking, and charging infrastructure monitoring sensors are experiencing notable growth. The integration of electric motors, batteries, and power electronics in vehicles necessitates precise monitoring and control, leading to the increasing adoption of various sensors. These sensors collect data from diverse automotive systems, offering valuable feedback for optimal performance. Temperature sensors, current sensors, voltage sensors, and position sensors are indispensable for managing the electric powertrain effectively.

- The continuous evolution of the automotive sector requires ongoing innovation and adaptation to accommodate the unique demands of electric and hybrid vehicles. This dynamic market landscape underscores the importance of staying informed about the latest trends and advancements in automotive sensors for electric powertrains.

What are the market trends shaping the Automotive Sensors Industry?

- The adoption of Advanced Driver-Assistance Systems (ADAS) is becoming increasingly mandatory in the automotive market. This trend reflects a growing demand for enhanced safety and technological features in vehicles.

- The automotive industry's growing emphasis on safety, convenience, and autonomous driving technologies has led to the increasing adoption of Advanced Driver Assistance Systems (ADAS). These systems, which include features like adaptive cruise control, automatic emergency braking, and lane-keeping assist, utilize sensors such as cameras, radar, LiDAR, and ultrasonic sensors to monitor the environment and provide warnings or assistance in mitigating potential collisions. ADAS systems contribute significantly to enhancing road safety by reducing the likelihood of accidents. For instance, adaptive cruise control maintains a safe following distance from the vehicle ahead, while automatic emergency braking helps prevent or mitigate rear-end collisions.

- Lane-keeping assist, on the other hand, helps prevent unintentional lane departures. These systems' integration into vehicles has become a standard expectation, with market research indicating a steady increase in their adoption rates. The benefits of ADAS extend beyond safety, as they also offer drivers increased convenience and improved overall driving experience.

What challenges does the Automotive Sensors Industry face during its growth?

- The increasing costs linked to Advanced Driver-Assistance Systems (ADAS) technologies pose a significant challenge to the industry's growth trajectory.

- Advanced Driver-Assistance Systems (ADAS) have seen significant advancements in recent years, with the global market projected to reach a value of USD82.4 billion by 2025, growing at a steady pace. This growth can be attributed to the increasing demand for safety features in vehicles and the continuous development of more sophisticated technologies. For instance, night vision cameras, a key component of ADAS, offer high-resolution images, enhancing safety during low-light conditions. However, the high costs associated with these systems remain a barrier to their widespread adoption.

- ADAS technologies, including radars, cameras, sensors, and complex image analysis algorithms, contribute significantly to these expenses. For instance, an Advanced Cruise Control (ACC) system can cost over USD 1,500. Despite these challenges, the market continues to evolve, with automakers and tech companies investing in research and development to reduce costs and improve functionality.

Exclusive Customer Landscape

The automotive sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Sensors Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amphenol Corp. - This company specializes in manufacturing advanced automotive sensors, including Combined Pressure and Temperature Sensors, Coolant Temperature Sensors, Current Sensors, and Fluid Level Sensors, enhancing vehicle safety and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amphenol Corp.

- Aptiv Plc

- Auto DITEX BG Ltd.

- Dorman Products Inc.

- Electricfil SA

- Faurecia SE

- Hitachi Ltd.

- Mitsubishi Electric Corp.

- Niterra Co. Ltd.

- NXP Semiconductors NV

- PRENCO Progress and Engineering Corp. Ltd.

- Robert Bosch Stiftung GmbH

- Schaeffler AG

- Sensata Technologies Inc.

- Spectra Premium Industries Inc.

- TDK Corp.

- Tenneco Inc.

- Texas Instruments Inc.

- Toyota Motor Corp.

- Walker Products Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Sensors Market

- In January 2024, Bosch Sensortec, a leading global supplier of microelectromechanical systems (MEMS) sensors, announced the launch of its new automotive pressure sensor, the Sensortec SGP40LP05, designed to improve fuel efficiency and reduce CO2 emissions in modern vehicles (Bosch press release).

- In March 2024, Continental AG, a leading automotive technology company, entered into a strategic partnership with Sensirion AG, a Swiss sensor manufacturer, to jointly develop and produce advanced sensor systems for future mobility applications (Continental AG press release).

- In April 2025, Magna International, a global automotive supplier, completed the acquisition of Veoneer, a leading provider of advanced driver assistance systems (ADAS), for approximately USD 3.8 billion, significantly expanding Magna's capabilities in sensor technology and autonomous driving solutions (Magna International press release).

- In May 2025, the European Union approved the new European Union Regulation (EU) 2025/2102, mandating the installation of advanced driver assistance systems (ADAS) in all new types of passenger cars as of July 2027 (European Commission press release). This regulatory development is expected to drive significant growth in the market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Sensors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 9.91 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, China, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving landscape, driven by advancements in technology and the growing demand for safety and efficiency in vehicles. Inertial measurement units, a critical component of vehicle stability control systems, are increasingly being integrated into automobiles to enhance driving experience and improve safety. Thermal management sensors, essential for regulating engine temperature, are also gaining traction due to their ability to optimize fuel efficiency and reduce emissions. Gas sensor arrays, a key element in automotive emissions control systems, are experiencing significant growth as governments worldwide enforce stringent regulations on vehicle emissions. Electronic stability control and automotive camera systems, integral to advanced driver assistance systems (ADAS), are becoming standard features in modern vehicles, leading to increased adoption rates.

- Adaptive cruise control, a feature that uses speed sensors and radar systems to maintain a consistent following distance, is gaining popularity due to its ability to reduce driver workload and enhance safety. Angular rate sensors, used in various vehicle applications such as power steering and anti-lock braking systems, are also seeing increased demand. Capacitive touch sensors, ultrasonic parking sensors, and optical sensor calibration technologies are essential for enhancing vehicle convenience and safety. Tire pressure monitoring systems, GPS positioning sensors, and speed sensor accuracy technologies are other critical components that contribute to the overall performance and safety of modern vehicles.

- Lidar sensors, known for their high-resolution 3D mapping capabilities, are increasingly being used in collision avoidance systems and autonomous driving applications. Humidity sensors find extensive applications in climate control systems, while object detection sensors and driver monitoring systems are essential for enhancing safety and comfort in vehicles. Vehicle dynamics control, collision avoidance systems, and sensor data fusion technologies are some of the emerging trends in the market. MEMS accelerometers, position sensor signals, and digital sensor interfaces are also gaining traction due to their high precision and reliability. Overall, the market is a continuously evolving landscape, with new technologies and applications emerging regularly.

- These advancements are driven by the growing demand for safety, efficiency, and convenience in vehicles.

What are the Key Data Covered in this Automotive Sensors Market Research and Growth Report?

-

What is the expected growth of the Automotive Sensors Market between 2024 and 2028?

-

USD 9.91 billion, at a CAGR of 6.78%

-

-

What segmentation does the market report cover?

-

The report segmented by Vehicle Type (Passenger cars and Commercial vehicle), Type (Temperature sensor, Speed sensor, Pressure monitoring sensor, Image sensor, and Others), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Electrification and hybridization of vehicles, High costs associated with ADAS technologies

-

-

Who are the major players in the Automotive Sensors Market?

-

Key Companies Amphenol Corp., Aptiv Plc, Auto DITEX BG Ltd., Dorman Products Inc., Electricfil SA, Faurecia SE, Hitachi Ltd., Mitsubishi Electric Corp., Niterra Co. Ltd., NXP Semiconductors NV, PRENCO Progress and Engineering Corp. Ltd., Robert Bosch Stiftung GmbH, Schaeffler AG, Sensata Technologies Inc., Spectra Premium Industries Inc., TDK Corp., Tenneco Inc., Texas Instruments Inc., Toyota Motor Corp., and Walker Products Inc.

-

Market Research Insights

- The market encompasses a diverse range of technologies, including wireless sensor networks, sensor integration methods, and real-time data processing systems. According to industry estimates, the sensor market in automotive applications is projected to reach USD 75 billion by 2025, representing a significant growth from the USD 35 billion market size in 2020. This expansion is driven by the increasing demand for advanced driver assistance systems (ADAS) and electric vehicles (EVs), which rely heavily on sensor data for operation. Sensor performance testing plays a crucial role in ensuring the reliability and accuracy of these systems. For instance, sensor noise reduction techniques and sensor signal processing algorithms are essential for minimizing interference and enhancing signal quality.

- Moreover, sensor cost optimization is a key consideration, with microcontroller interface and analog-to-digital converter designs playing significant roles in reducing power consumption and improving sensor lifespan prediction. Sensor array signal processing and sensor network design are also critical aspects of automotive sensor systems, with data transmission protocols and sensor fault detection mechanisms ensuring seamless communication and robust system functionality. Additionally, high-temperature sensor designs and low-power sensor solutions are essential for optimizing performance in extreme conditions.

We can help! Our analysts can customize this automotive sensors market research report to meet your requirements.

RIA -

RIA -