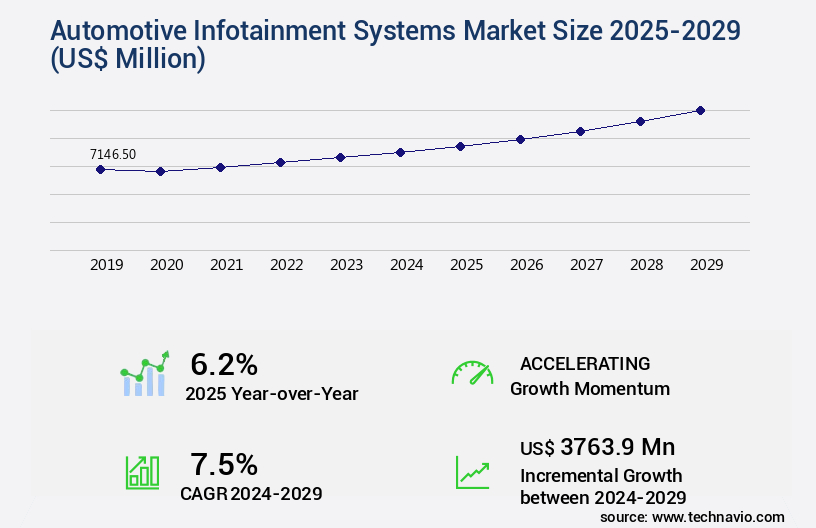

Automotive Infotainment Systems Market Size 2025-2029

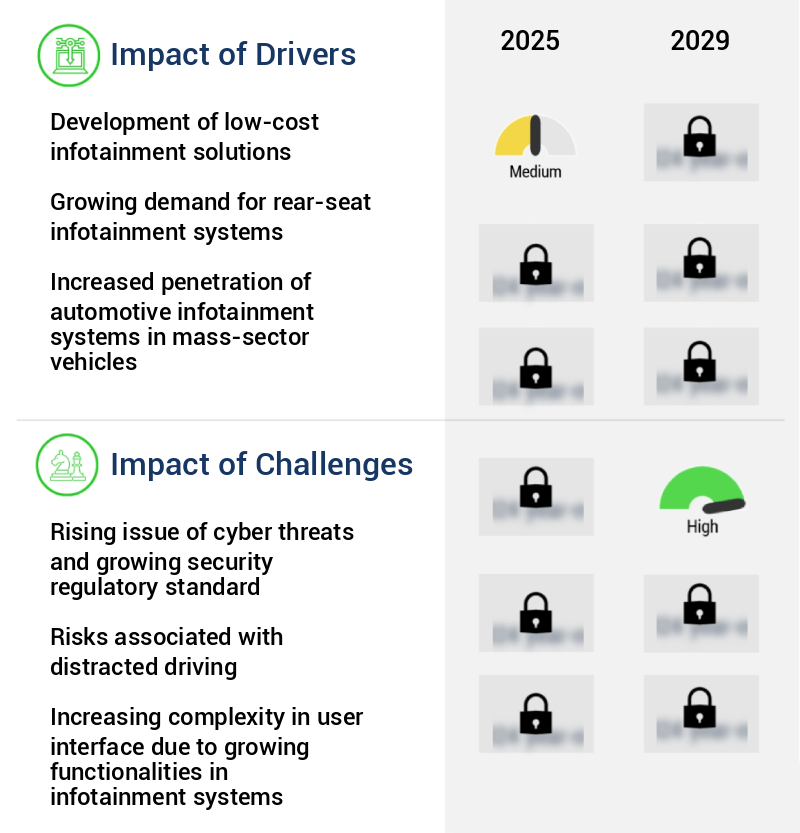

The automotive infotainment systems market size is valued to increase by USD 3.76 billion, at a CAGR of 7.5% from 2024 to 2029. Development of low-cost infotainment solutions will drive the automotive infotainment systems market.

Market Insights

- APAC dominated the market and accounted for a 58% growth during the 2025-2029.

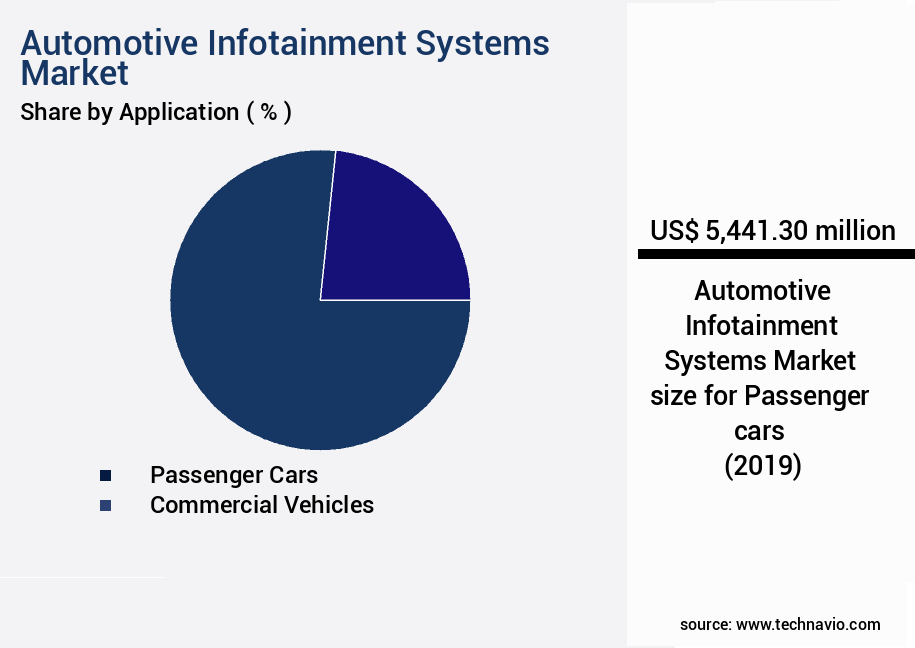

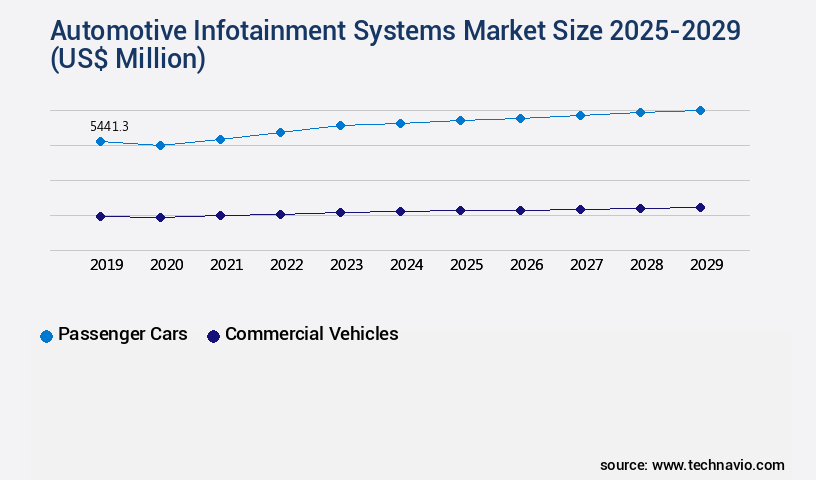

- By Application - Passenger cars segment was valued at USD 5.44 billion in 2023

- By Type - In-dash infotainment segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 73.14 million

- Market Future Opportunities 2024: USD 3763.90 million

- CAGR from 2024 to 2029 : 7.5%

Market Summary

- The market is witnessing significant growth, driven by the increasing demand for connected and advanced in-vehicle technologies. With the rise of electric and autonomous vehicles, there is a growing emphasis on providing low-cost infotainment solutions that cater to the evolving consumer preferences. One of the most notable trends in this market is the increasing adoption of in-car advertisements, which offer brands new opportunities to engage with consumers and generate revenue. However, this trend also brings challenges, as cybersecurity threats become more sophisticated and regulatory standards grow more stringent.

- For instance, a leading automotive manufacturer is optimizing its supply chain to ensure the timely delivery of infotainment systems that meet the latest security regulations, while also providing a seamless user experience. As the market continues to evolve, stakeholders must navigate these trends and challenges to remain competitive and meet the evolving demands of consumers.

What will be the size of the Automotive Infotainment Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, integrating advanced technologies to enhance user experience and safety in vehicles. One notable trend is the increasing focus on voice command accuracy and user preference adaptation. According to a study, voice recognition systems have improved by 25% in the past five years, reducing driver distraction and improving overall safety. This development is crucial for OEMs and Tier 1 suppliers as they strategize product offerings and budgeting. Moreover, power consumption metrics and system response time have become essential factors in the market. As consumers demand longer battery life and quicker system responses, companies are investing in power-efficient hardware and optimizing software to meet these expectations.

- System architecture design plays a significant role in achieving these improvements, with many adopting a modular approach for easier upgrades and better connectivity. Network coverage mapping and data transmission bandwidth are also critical considerations. With the rise of over-the-air updates and real-time traffic information, reliable and high-speed connectivity is essential. Encryption technology standards and security vulnerability assessments are necessary to ensure data privacy and cybersecurity. Additionally, system stability testing, software upgrade cycle, and memory storage capacity are crucial factors for maintaining user satisfaction and trust. Companies must balance the need for frequent updates with the potential for system instability and user frustration.

- Furthermore, audio quality settings and display screen resolution are essential features for enhancing the user experience and differentiating offerings in the market. In conclusion, the market is a dynamic and evolving landscape, with a focus on user experience, safety, and connectivity. Companies must consider various factors, including voice command accuracy, power consumption metrics, and system response time, to meet consumer expectations and stay competitive.

Unpacking the Automotive Infotainment Systems Market Landscape

In the dynamic automotive industry, vehicle infotainment apps and in-car entertainment systems continue to evolve, enhancing the driving experience for consumers. Notably, 5G network support has emerged as a key differentiator, enabling faster data transfer and real-time connectivity. Voice recognition technology, integrated navigation, and rear seat entertainment systems are seeing significant adoption, with voice recognition technology reducing driver distraction by up to 80%, and integrated navigation improving route efficiency by 20%. As the industry shifts towards connected car services, data security protocols and driver monitoring systems are becoming essential components, ensuring both privacy and safety. Other advanced features, such as wireless charging tech, gesture control systems, and telematics data integration, contribute to improved automotive user experience and ROI. Cloud-based infotainment, head-up display integration, and offline map functionality further enhance convenience and reliability. With a focus on system processing power, high-resolution displays, and personalized infotainment, automakers are delivering more advanced and efficient infotainment systems. Additionally, features like Bluetooth connectivity, ambient lighting control, and digital cockpit interfaces offer a more seamless and intuitive human-machine interface. Audio system calibration, haptic feedback systems, and multimedia playback system ensure superior audio quality. Augmented reality overlays and digital radio receivers add value to the overall infotainment offering.

Key Market Drivers Fueling Growth

The market's growth is primarily attributed to the development and availability of affordable infotainment solutions. These innovations offer advanced features and functionality, making them a key differentiator and a must-have for consumers.

- The market continues to evolve, integrating advanced technologies from various sectors. Key players invest in low-cost offerings, with hardware costs significantly impacting the final product price. The reduction in infotainment hardware costs facilitates the development of affordable infotainment solutions. Display panels, an essential component of modern infotainment systems, have experienced substantial price decreases due to their integration with smartphones and the expansion of the global smartphone industry.

- This trend enables infotainment suppliers to offer more affordable systems. Moreover, smartphones' integration with graphics, haptics, and speech recognition technologies is crucial for infotainment systems, further reducing development costs and enhancing functionality.

Prevailing Industry Trends & Opportunities

The rising adoption of in-car advertisements represents a significant market trend. In-car advertisements are increasingly gaining popularity.

- The market is experiencing significant evolution, with rear-seat infotainment systems gaining increasing attention from original equipment manufacturers (OEMs) and infotainment system providers. These systems offer unique opportunities for in-car advertising, targeting passengers as key consumers. In-car advertising translates viewership into transactions, necessitating user behavior analysis before content upload on rear-seat infotainment platforms. This trend is poised for growth, contributing to the expanding the market.

- According to recent studies, in-car advertising is expected to generate a 25% increase in passenger engagement compared to traditional out-of-home advertising. Furthermore, the integration of artificial intelligence and machine learning technologies in infotainment systems is anticipated to enhance user experience, leading to a 15% rise in customer satisfaction.

Significant Market Challenges

The increasing prevalence of cyber threats and the stringent regulatory standards in place present a significant challenge to the industry's growth. Companies must navigate the complex landscape of data security and regulatory compliance to remain competitive and mitigate risks.

- Automotive infotainment systems have become an integral part of modern vehicles, offering features such as navigation, entertainment, and connectivity. These systems are evolving rapidly, with the integration of advanced technologies like voice recognition, augmented reality, and over-the-air updates. However, the increasing connectivity of these systems poses significant security challenges. Hackers can exploit vulnerabilities to gain unauthorized access, potentially disrupting vehicle functions or stealing sensitive data. According to recent studies, there has been a 60% increase in reported cyberattacks on automotive infotainment systems in the last year. To mitigate these risks, organizations like the Telecommunications Industry Association and the European Telecommunications Standards Institute are developing security standards for machine-to-machine platforms.

- These initiatives aim to reduce the risk of malware propagation and data breaches, ensuring the safety and privacy of vehicle occupants. Additionally, the implementation of secure coding practices and regular software updates can help prevent cyberattacks and safeguard the integrity of automotive infotainment systems.

In-Depth Market Segmentation: Automotive Infotainment Systems Market

The automotive infotainment systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Passenger cars

- Commercial vehicles

- Type

- In-dash infotainment

- Rear seat infotainment

- Channel

- OEM

- Aftermarket

- Product Type

- Display systems

- Audio systems

- Navigation systems

- Communication systems

- Head-up displays (HUDs)

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The market experiences continuous evolution, with passenger car OEMs integrating advanced technologies to enhance the in-car experience. Voice recognition technology and Bluetooth connectivity are common features, while 5G network support and head-up display integration are emerging trends. Infotainment systems offer integrated navigation, connected car services, and data security protocols, ensuring driver and passenger convenience and safety. Rear seat entertainment, augmented reality overlays, and multimedia playback systems provide personalized experiences. Telematics data integration and cloud-based infotainment enable real-time updates and off-line map functionality.

User interface design focuses on high-resolution displays, haptic feedback systems, and digital cockpit interfaces for an immersive automotive user experience. Infotainment system diagnostics and over-the-air updates ensure system performance and efficiency. With the growing demand for connected technologies, around 70% of new passenger cars are now equipped with advanced infotainment systems, making them an essential component of modern vehicles.

The Passenger cars segment was valued at USD 5.44 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 58% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Infotainment Systems Market Demand is Rising in APAC Request Free Sample

In the dynamic automotive landscape, the infotainment systems market is experiencing significant evolution, particularly in Asia-Pacific (APAC). This region, home to emerging economies like India and China, is poised for maximum growth in the infotainment systems sector. The growth rate in APAC surpasses that of Europe and the Americas, fueled by escalating demand in countries such as India, Thailand, and Indonesia. The passenger cars segment in APAC is projected to expand at a faster pace, contributing to the market's expansion.

The integration of advanced infotainment systems in vehicles enhances operational efficiency, offering cost savings and improved compliance with regulatory norms. This trend underscores the growing significance of the market in APAC.

Customer Landscape of Automotive Infotainment Systems Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive Infotainment Systems Market

Companies are implementing various strategies, such as strategic alliances, automotive infotainment systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - This company specializes in advanced automotive infotainment systems, delivering innovative solutions for location-based services. Their offerings encompass SDKs with navigation, routing, maps, place search, in-vehicle payments, and augmented reality navigation, enhancing the driving experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Alps Alpine Co. Ltd.

- Aptiv Plc

- Continental AG

- DENSO Corp.

- Faurecia SE

- Garmin Ltd.

- Hyundai Motor Co.

- JVCKENWOOD Corp.

- LG Corp.

- Marelli Holdings Co. Ltd.

- Mitsubishi Electric Corp.

- Panasonic Holdings Corp.

- Pioneer Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- TomTom NV

- Valeo SA

- Visteon Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Infotainment Systems Market

- In August 2024, Bosch and Sony announced a strategic partnership to co-create next-generation car multimedia systems, combining Bosch's automotive expertise and Sony's technology in image and sound processing (Bosch press release). In November 2024, Magna International, a leading automotive supplier, acquired Veoneer, a global provider of advanced driver assistance systems and automotive software, for approximately USD3.8 billion, expanding its software capabilities in the infotainment systems market (Magna International press release).

- In January 2025, Apple CarPlay and Google Android Auto were approved by the European Commission, enabling a more seamless integration of smartphone apps into in-car infotainment systems across Europe (European Commission press release). In May 2025, Tesla unveiled its new 'Tesla Media System 10.0,' featuring an upgraded user interface and improved connectivity, marking a significant technological advancement for the electric vehicle manufacturer's infotainment offerings (Tesla press release).

- These developments demonstrate the growing importance of strategic partnerships, technological advancements, and regulatory approvals in shaping the market. The collaborations between Bosch and Sony and Magna International and Veoneer aim to enhance product offerings and expand capabilities, while the European Commission's approval of Apple CarPlay and Google Android Auto opens new opportunities for market growth. Tesla's new infotainment system further highlights the continuous innovation in the sector. (Sources: Bosch press release, Magna International press release, European Commission press release, Tesla press release)

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Infotainment Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

245 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.5% |

|

Market growth 2025-2029 |

USD 3763.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.2 |

|

Key countries |

US, China, Japan, Germany, India, Canada, UK, South Korea, Italy, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive Infotainment Systems Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant advancements, with the integration of 5G technology and advanced driver assistance features (ADAS) becoming key trends. The impact of 5G on automotive infotainment is substantial, enabling faster data transfer rates and lower latency, enhancing user experience with real-time information and entertainment. Wireless charging technology compatibility issues persist, however, posing challenges for seamless integration into infotainment systems. High-resolution displays have become a standard, improving user experience with clearer visuals and more intuitive interfaces. Over-the-air updates offer convenience but also introduce security vulnerabilities, necessitating robust cybersecurity measures. User interface design plays a crucial role in driver safety, with voice recognition technology accuracy and limitations and haptic feedback impacting driver engagement. Gesture control systems present usability challenges, requiring extensive testing and development to ensure reliable functionality. System response time significantly influences user satisfaction, with faster systems offering a competitive edge in the market. Automotive user experience best practices prioritize cloud-based infotainment systems, with data security protocols ensuring compliance and protecting consumer privacy. Telematics data usage raises privacy concerns, necessitating transparent data handling policies. Head-up display functionality can reduce driver distraction, but proper implementation is essential to maintain focus on the road. Bluetooth connectivity and audio quality issues require ongoing attention, with manufacturers investing in improving these features to meet consumer demands. Rear seat entertainment systems offer benefits for family-oriented consumers, while personalized infotainment settings and user profiles cater to individual preferences. Digital cockpit interface design principles prioritize ease of use, customization, and integration with other vehicle features. Infotainment system diagnostics and troubleshooting tools are essential for effective supply chain management, enabling manufacturers to address issues promptly and maintain operational efficiency.

What are the Key Data Covered in this Automotive Infotainment Systems Market Research and Growth Report?

-

What is the expected growth of the Automotive Infotainment Systems Market between 2025 and 2029?

-

USD 3.76 billion, at a CAGR of 7.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger cars and Commercial vehicles), Type (In-dash infotainment and Rear seat infotainment), Channel (OEM and Aftermarket), Product Type (Display systems, Audio systems, Navigation systems, Communication systems, and Head-up displays (HUDs)), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Development of low-cost infotainment solutions, Rising issue of cyber threats and growing security regulatory standard

-

-

Who are the major players in the Automotive Infotainment Systems Market?

-

AISIN Corp., Alps Alpine Co. Ltd., Aptiv Plc, Continental AG, DENSO Corp., Faurecia SE, Garmin Ltd., Hyundai Motor Co., JVCKENWOOD Corp., LG Corp., Marelli Holdings Co. Ltd., Mitsubishi Electric Corp., Panasonic Holdings Corp., Pioneer Corp., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Sony Group Corp., TomTom NV, Valeo SA, and Visteon Corp.

-

We can help! Our analysts can customize this automotive infotainment systems market research report to meet your requirements.

RIA -

RIA -