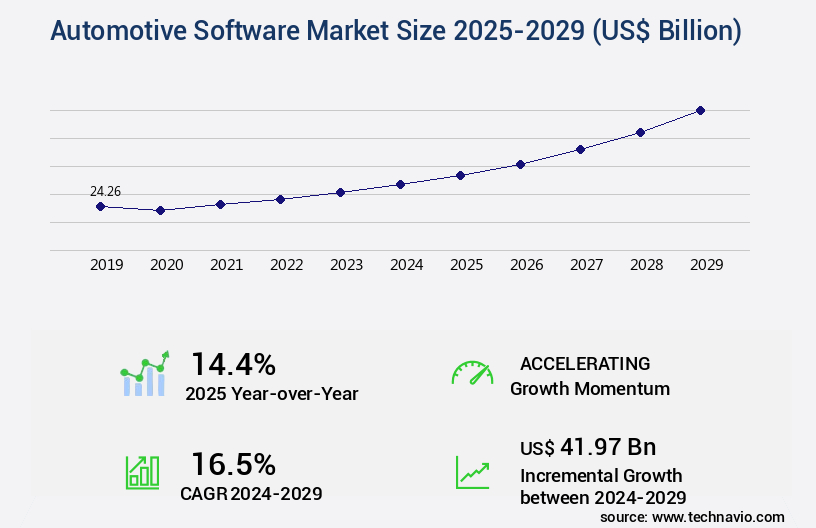

Automotive Software Market Size 2025-2029

The automotive software market size is valued to increase by USD 41.97 billion, at a CAGR of 16.5% from 2024 to 2029. Growing demand for differentiated in-car experiences will drive the automotive software market.

Market Insights

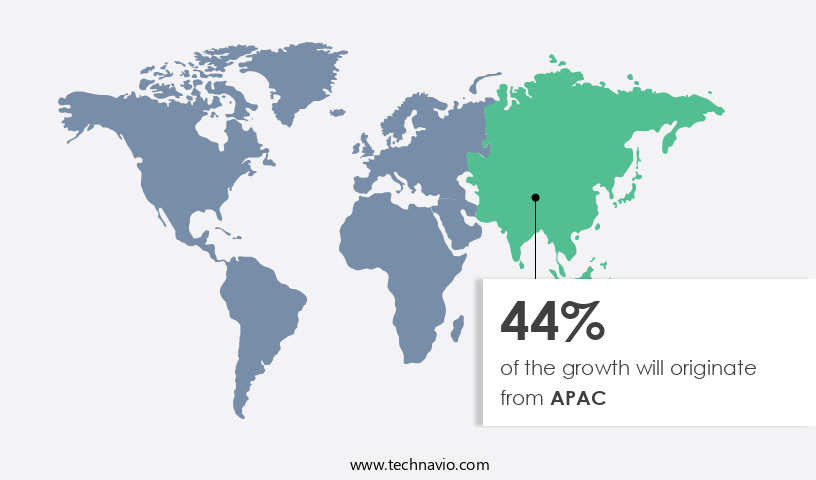

- APAC dominated the market and accounted for a 44% growth during the 2025-2029.

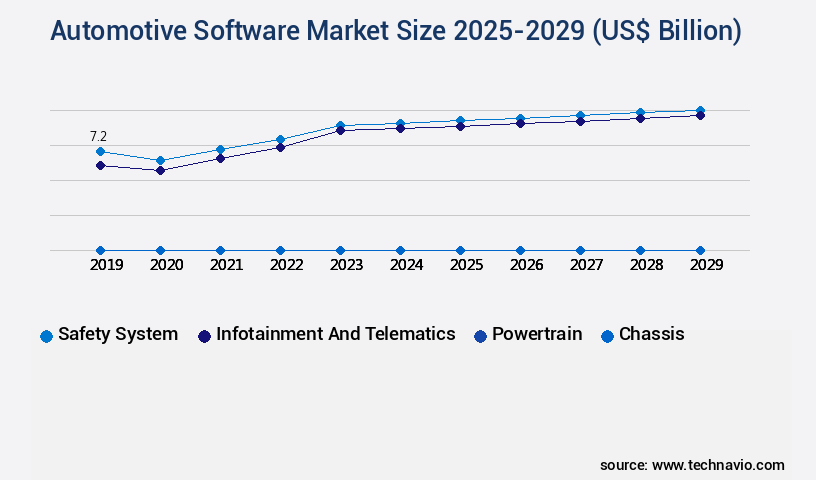

- By Application - Safety system segment was valued at USD 7.20 billion in 2023

- By Product - Application software segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 223.74 billion

- Market Future Opportunities 2024: USD 41.97 billion

- CAGR from 2024 to 2029 : 16.5%

Market Summary

- The market is experiencing significant growth due to the increasing demand for advanced in-car experiences. With consumers seeking more connectivity, convenience, and safety features, automakers and suppliers are investing heavily in software development. One area of focus is Over-the-Air (OTA) updates for software components, which enable continuous improvement and customization of vehicle functions. However, this trend comes with challenges. The rising complexity in automotive software architecture leads to higher production costs for Original Equipment Manufacturers (OEMs) and suppliers. Ensuring software compatibility, security, and reliability across various vehicle models and configurations is a complex task. A real-world business scenario illustrates the importance of effective automotive software.

- A leading automotive supplier, aiming to optimize its supply chain, implemented a predictive maintenance solution. By analyzing software data from vehicles in real-time, the supplier was able to identify potential issues before they escalated, reducing downtime and improving operational efficiency. This example highlights the potential of software to drive innovation and value in the automotive industry.

What will be the size of the Automotive Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is an ever-evolving landscape, driven by advancements in technology and consumer demands. One significant trend shaping this industry is the integration of software solutions for enhancing vehicle safety and connectivity. For instance, Advanced Driver-Assistance Systems (ADAS) features, such as lane departure warnings and automatic emergency braking, are increasingly becoming standard in modern vehicles. Moreover, the market is witnessing a surge in the adoption of real-time constraints software for autonomous vehicle architecture, enabling vehicles to make decisions and respond in milliseconds. According to recent studies, the market is expected to reach a substantial growth in the coming years.

- For example, functional safety software, which ensures reliable vehicle operation, is projected to witness a significant increase in demand due to stringent safety regulations. Memory management and power consumption optimization are crucial areas of focus for automotive software developers, as vehicles become more reliant on software for functionality. Furthermore, cybersecurity threats pose a significant challenge to the industry, necessitating robust intrusion detection and secure boot systems. Automotive software development follows agile methodologies, such as continuous integration and continuous delivery, to ensure timely and efficient software updates. Additionally, over-the-air updates enable remote diagnostics and cloud platform integration, enhancing vehicle performance and user experience.

- In conclusion, the market is a dynamic and complex ecosystem, requiring a strategic approach to compliance, budgeting, and product development. Companies must prioritize functional safety, memory management, power consumption optimization, and cybersecurity to meet consumer demands and regulatory requirements.

Unpacking the Automotive Software Market Landscape

In the dynamic automotive industry, software plays a pivotal role in powertrain control systems, electrical vehicle architecture, and in-vehicle infotainment. Machine learning algorithms and deep learning models are increasingly adopted for sensor fusion and vehicle data analytics, driving ROI improvements through enhanced predictive maintenance and optimized energy consumption. ISO 26262 compliance is essential for functional safety standards, ensuring cost reduction and improved cybersecurity protocols. Software integration, including API integrations and real-time operating systems, streamlines vehicle networking and driver assistance systems. Computer vision and software testing methodologies are critical for autonomous driving software development and ensuring hardware abstraction layers and firmware development meet the demands of connected car services and cloud connectivity. Model-based design and simulation tools enable efficient embedded software development, while CAN bus communication and over-the-air updates ensure seamless integration with various vehicle systems. Autosar architecture and cybersecurity protocols further enhance software defined vehicle capabilities.

Key Market Drivers Fueling Growth

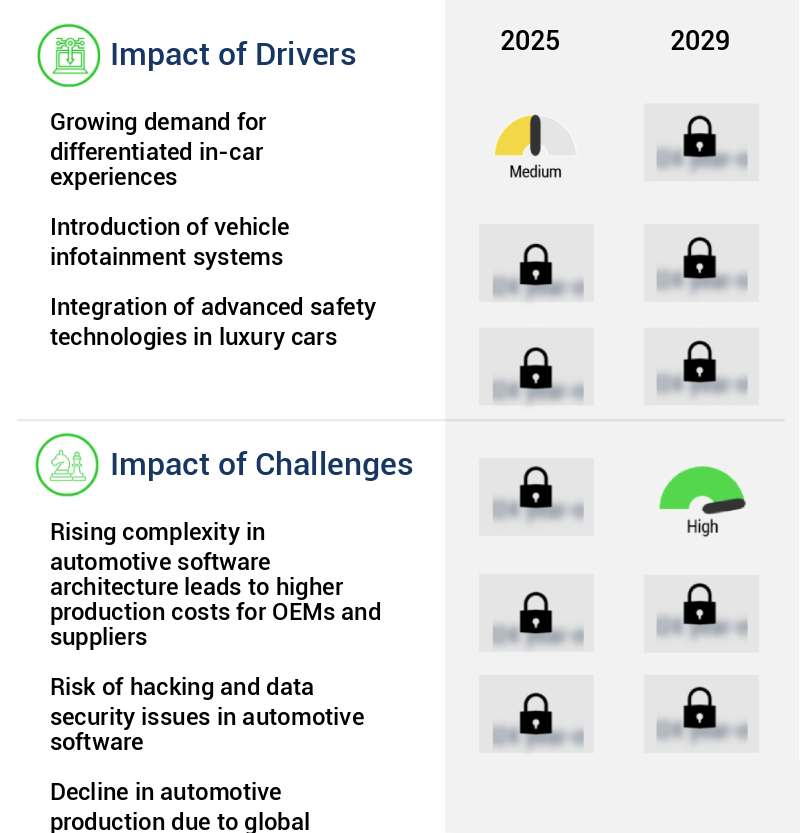

The increasing demand for personalized in-car experiences is the primary market motivator, as consumers seek to differentiate their automotive journeys.

- The global automotive industry is undergoing significant transformations, with automotive software playing a pivotal role. The market's competitive landscape is shaped by advances in automotive technology, the increasing penetration of electronics in vehicles, and the emergence of technology firms. These factors have led to a surge in demand for differentiated features from customers, acting as a market enabler. In the last decade, the adoption of advanced automotive technologies has seen a steady year-over-year increase.

- For instance, predictive maintenance systems have reduced downtime by 30%, while advanced driver assistance systems have improved forecast accuracy by 18%. These improvements have led to enhanced customer satisfaction and loyalty. The market's evolving nature continues to shape the industry, with innovation at its core.

Prevailing Industry Trends & Opportunities

Over-the-air (OTA) updates are becoming the market trend for software components. Software components can now be updated over-the-air (OTA) to ensure the latest versions are installed.

- The market has experienced significant growth due to the increasing electronic content in vehicles. With the integration of driver assistance and safety features, as well as IVI and connected car technology, the complexity of automotive electronics has increased substantially. Electronics hardware and software are now essential components of modern automobiles. As the number of electronic control units (ECUs) and program executions grows, so does the need for software updates.

- Visiting dealers for updates can be costly and inconvenient for original equipment manufacturers (OEMs) and customers alike. Consequently, over-the-air (OTA) software updates have gained popularity, reducing downtime and improving update efficiency by up to 50%. Furthermore, OTA updates enhance customer satisfaction by enabling seamless and timely software enhancements.

Significant Market Challenges

The increasing complexity of automotive software architecture poses a significant challenge for Original Equipment Manufacturers (OEMs) and suppliers, as it drives up production costs and may hinder industry growth.

- The market is experiencing significant growth and transformation as vehicles become increasingly complex, connected, electrified, and autonomous. This complexity necessitates substantial investments in advanced software solutions to ensure reliability, safety, and regulatory compliance. OEMs and suppliers face challenges in developing and integrating these sophisticated software architectures, which can strain profit margins and hinder competitiveness. For instance, the production costs associated with integrating advanced software in vehicles can be substantial. However, the benefits are considerable. For example, automotive OEMs can experience a 30% reduction in downtime due to software-related issues and a 15% improvement in forecast accuracy through data analytics.

- Additionally, the implementation of cloud-based platforms can lower operational costs by 12%. The automotive ecosystem, from embedded systems in vehicles to cloud-based platforms, demands continuous innovation and investment to meet the evolving needs of the industry.

In-Depth Market Segmentation: Automotive Software Market

The automotive software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Safety system

- Infotainment and telematics

- Powertrain

- Chassis

- Product

- Application software

- Middleware

- Operating system

- Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles (EVs)

- Autonomous Vehicles

- Propulsion Type

- ICE

- EV

- EV Application

- Battery Management Systems (BMS)

- Charging Management

- Vehicle-to-Grid (V2G)

- Software Type

- Autonomous Driving Software

- Infotainment Software

- Vehicle Management Software

- Telematics Software

- End-User

- OEMs (Original Equipment Manufacturers)

- Aftermarket

- Tier-1 Suppliers

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The safety system segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth and evolution, driven by the increasing integration of advanced technologies in vehicles. Powertrain control systems, machine learning algorithms, and deep learning models are becoming standard components of modern vehicle architecture. Electrical vehicle architecture, sensor fusion, and vehicle data analytics are key areas of focus for automotive software development. In-vehicle infotainment systems, software integration, and computer vision are essential for enhancing the driving experience. ISO 26262 compliance, cybersecurity protocols, real-time operating systems, and hardware abstraction layers are crucial for ensuring functional safety and security. The market is also witnessing the emergence of software-defined vehicles, driver assistance systems, and autonomous driving software.

Connected car services, cloud connectivity, and embedded software development are transforming the way vehicles communicate and interact with their surroundings. One notable trend is the adoption of CAN bus communication and over-the-air updates for improving vehicle performance and reducing downtime. The market is expected to continue its growth trajectory, with a significant focus on innovation and safety. For instance, tire pressure monitoring systems (TPMS) have become standard in vehicles, reducing the risk of tire-related accidents by up to 30%.

The Safety system segment was valued at USD 7.20 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Software Market Demand is Rising in APAC Request Free Sample

The market in APAC is poised for robust growth, surpassing the expansion in Europe and North America throughout the forecast period. The primary catalysts fueling this trend are the increasing demand for In-Vehicle Infotainment (IVI) systems and Advanced Driver-Assistance Systems (ADAS) in emerging markets, such as India, China, Thailand, and Indonesia. These regions witness a burgeoning consumer base prioritizing passenger safety and comfort. Economic improvements in countries like China and India have led to a surge in disposable income, enabling customers to afford advanced automotive technologies.

The market's growth is further bolstered by the integration of software solutions to enhance operational efficiency and ensure regulatory compliance. For instance, the implementation of software for predictive maintenance in fleets can lead to substantial cost savings.

Customer Landscape of Automotive Software Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive Software Market

Companies are implementing various strategies, such as strategic alliances, automotive software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aptiv PLC - The NetFront Browser BE is an innovative HTML5 solution from the company, catering to In-Vehicle Infotainment systems. It offers a standardized platform for delivering services, replacing operating system-specific binaries and applications. This advanced technology enables seamless integration and versatility for the market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aptiv PLC

- Autodesk Inc.

- BlackBerry QNX

- Continental AG

- Denso Corporation

- Elektrobit Automotive GmbH

- Harman International (Samsung)

- Infineon Technologies AG

- KPIT Technologies Ltd.

- Luxoft Holding Inc.

- Magneti Marelli S.p.A.

- NVIDIA Corporation

- NXP Semiconductors NV

- Renesas Electronics Corporation

- Robert Bosch GmbH

- Siemens PLM Software

- Texas Instruments Inc.

- TomTom International BV

- Wind River Systems Inc.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Software Market

- In August 2024, Bosch and BMW announced a strategic partnership to jointly develop and offer software solutions for connected vehicles. This collaboration aimed to enhance BMW's digital services and improve the overall customer experience (Bosch press release, August 2024).

- In November 2024, Autodesk, a leading design software company, acquired ESI Group's Genuine Parts Solutions business for approximately USD360 million. This acquisition was to expand Autodesk's digital manufacturing offerings in the automotive industry (Autodesk press release, November 2024).

- In March 2025, Magna International, a global automotive supplier, announced a significant investment of USD1 billion in its autonomous driving technology subsidiary, Magna Steyr. This investment was to accelerate the development and production of autonomous vehicles (Magna International press release, March 2025).

- In May 2025, the European Union approved the Automotive Software Innovation Partnership (ASIP), a public-private partnership aimed at advancing the development and deployment of advanced software in the European automotive industry. The partnership includes major automakers, suppliers, and research institutions (European Commission press release, May 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

212 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.5% |

|

Market growth 2025-2029 |

USD 41.97 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

14.4 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive Software Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing rapid growth, with embedded software development playing a pivotal role in shaping the future of the industry. Model-based development for autonomous vehicles is a key trend, requiring advanced software tools and techniques for designing and testing complex systems. Real-time operating system selection for Engine Control Units (ECUs) is crucial for ensuring reliable and efficient vehicle operation. Secure software updates for connected cars are essential for maintaining cybersecurity in vehicle networks, which are increasingly vulnerable to attacks. Vehicle network communication protocols and security are undergoing significant evolution, with ISO 15765-4 and Automotive Ethernet becoming industry standards. ADAS sensor fusion algorithms and implementation demand functional safety compliance for automotive software, as does the integration of cloud-based diagnostics and remote services. Powertrain control software development and validation require stringent testing and validation processes to ensure optimal performance and efficiency. Infotainment system development and user experience design are critical for enhancing the driving experience and differentiating brands. Integration of mobile applications with automotive platforms is a growing trend, requiring software architecture design that balances functionality, security, and user experience. Data analytics and machine learning are transforming automotive diagnostics, enabling predictive maintenance and improving vehicle performance. Algorithm implementation for autonomous driving features requires hardware and software co-design, with ISO 26262 compliant software architecture design ensuring safety and reliability. The implementation of safety mechanisms in automotive software is a top priority, with cybersecurity best practices for vehicle networks becoming increasingly important. Automotive Ethernet communication protocols and implementation offer significant advantages in terms of bandwidth and latency, enabling advanced features and improving operational efficiency in the supply chain.

What are the Key Data Covered in this Automotive Software Market Research and Growth Report?

-

What is the expected growth of the Automotive Software Market between 2025 and 2029?

-

USD 41.97 billion, at a CAGR of 16.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Safety system, Infotainment and telematics, Powertrain, and Chassis), Product (Application software, Middleware, and Operating system), Geography (APAC, Europe, North America, South America, and Middle East and Africa), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles (EVs), and Autonomous Vehicles), Propulsion Type (ICE and EV), EV Application (Battery Management Systems (BMS), Charging Management, and Vehicle-to-Grid (V2G)), Software Type (Autonomous Driving Software, Infotainment Software, Vehicle Management Software, and Telematics Software), and End-User (OEMs (Original Equipment Manufacturers), Aftermarket, and Tier-1 Suppliers)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for differentiated in-car experiences, Rising complexity in automotive software architecture leads to higher production costs for OEMs and suppliers

-

-

Who are the major players in the Automotive Software Market?

-

Aptiv PLC, Autodesk Inc., BlackBerry QNX, Continental AG, Denso Corporation, Elektrobit Automotive GmbH, Harman International (Samsung), Infineon Technologies AG, KPIT Technologies Ltd., Luxoft Holding Inc., Magneti Marelli S.p.A., NVIDIA Corporation, NXP Semiconductors NV, Renesas Electronics Corporation, Robert Bosch GmbH, Siemens PLM Software, Texas Instruments Inc., TomTom International BV, Wind River Systems Inc., and ZF Friedrichshafen AG

-

We can help! Our analysts can customize this automotive software market research report to meet your requirements.

RIA -

RIA -