Poland Automotive Parts Market Size 2025-2029

The Poland automotive parts market size is forecast to increase by USD 24.5 billion, at a CAGR of 14.5% between 2024 and 2029.

- The market is experiencing significant growth, driven by several key trends. The increasing average age of vehicles is leading to higher demand for replacement parts. Technological advancements, such as the integration of LIDAR and LED systems in autonomous vehicles and the adoption of internal combustion engines with improved fuel efficiency, are also fueling market growth. Additionally, the rise of e-commerce platforms is transforming the automotive aftermarket, enabling customers to easily purchase parts online and streamline logistics. Furthermore, the commercial vehicle sector is witnessing a shift towards electric vehicles with advanced battery systems, while 3D printing technology is revolutionizing the production of customized automotive parts. Overall, these trends present both opportunities and challenges for market participants, requiring a strategic approach to remain competitive.

What will be the Size of the market During the Forecast Period?

- The market is a dynamic and expansive industry, encompassing a diverse range of components for various vehicle types. With increasing focus on vehicle emissions and environmental sustainability, there is a growing demand for eco-friendly parts, such as those made from recycled materials or those designed to improve fuel efficiency. The regulatory environment continues to shape market trends, with stricter emissions standards driving innovation in areas like electric vehicles and advanced engine technologies.

- Emerging markets, particularly in Asia and South America, are experiencing significant growth due to increasing vehicle ownership and rising disposable income. Technological advancements, including 3D printing and the integration of electrical parts into traditional mechanical systems, are also transforming the industry. Overall, the automotive parts market is poised for continued growth and innovation, driven by a combination of consumer demand, regulatory requirements, and technological advancements.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle Type

- Passenger cars

- Commercial vehicles

- Distribution Channel

- Offline

- Online

- End-user

- OEM

- Aftermarket

- Geography

- Poland

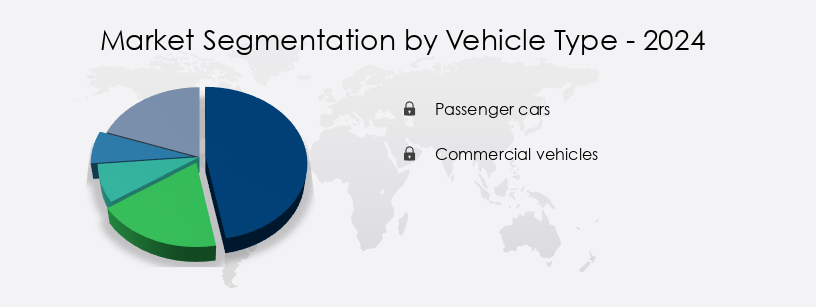

By Vehicle Type Insights

- The passenger cars segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth due to the high demand for passenger car parts. With a large population of hatchbacks, sedans, and estates, the segment accounts for a substantial portion of the market. The increasing sales of plug-in hybrid electric vehicles (PHEVs) and battery electric vehicles (BEVs) are further fueling the market's expansion. For instance, the number of BEVs in Poland's passenger car fleet reached 61,976 in June 2024, representing a 54% increase from the previous year. The regulatory environment, focusing on reducing vehicle emissions, is also contributing to the market's growth.

- Emerging markets, such as Poland, are adopting environmentally sustainable technologies, including electric drivetrains, batteries, charging infrastructure, and electrification. The market is witnessing advancements in cutting-edge technology, including sensors, radar systems, LIDAR technology, braking components, headlamps, and 3D printing technology. The market scope includes brake parts, electrical parts, fuel intake, ignition parts, A/C parts, suspension parts, exhaust parts, engine cooling parts, steering parts, wheels, tires, and passenger cars. The market is served through authorized dealers and e-commerce sites, with the offline and online segments experiencing increased demand.

Get a glance at the market report of the share of various segments Request Free Sample

Market Dynamics

Our Poland Automotive Parts Market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of the Poland Automotive Parts Market?

- Increasing average age of vehicles is the key driver of the market. The global automotive parts market is experiencing increased demand due to various factors, including the regulatory environment focusing on vehicle emissions and the shift towards environmentally sustainable transportation. Emerging markets, such as those in Asia and South America, are driving growth In the market, particularly in the areas of electric vehicles, electric drivetrains, batteries, charging infrastructure, and battery electric vehicles. The electrification trend is also leading to advancements in cutting-edge technology, such as autonomous vehicle technology, sensors, radar systems, and LIDAR technology. Brick-and-mortar stores and e-commerce platforms are both significant channels for the sale of automotive parts.

- The market scope includes brake parts, electrical parts, fuel intake, ignition parts, A/C parts, suspension parts, exhaust parts, engine cooling parts, steering parts, wheels, tires, and passenger cars. Despite the increasing cost of vehicles, people are holding onto their older vehicles for longer periods due to the high-quality parts used in their manufacturing. In Europe, for example, the average age of vehicles is increasing, particularly in countries like Poland. This trend is expected to continue, as the cost of new vehicles remains high. The market dynamics are influenced by changing economic conditions, with Lippert Components, the Auto Care Association, and the Automotive Suppliers Association playing significant roles in shaping the market.

What are the market trends shaping the Poland Automotive Parts Market?

- Technological advances in automotive smart seats are the upcoming trend in the market. In the automotive parts market, there is an increased demand for environmentally sustainable technologies due to regulatory requirements and consumer preferences for reducing vehicle emissions. One emerging trend is the electrification of vehicles, including electric drivetrains, batteries, and charging infrastructure. This shift is driving innovation in cutting-edge technology such as electric vehicle batteries, sensor systems like radar and LIDAR, and autonomous vehicle technology. Brake components, headlamps, and 3D printing technology are also areas of significant growth. For instance, automatic emergency braking systems, which utilize sensors and real-time driving data to improve safety and efficiency, are becoming standard in many vehicles.

- These systems use various types of onboard sensors, including radar, LiDAR, and cameras, to monitor driving conditions and apply brakes or boost braking power when necessary. The automotive aftermarket, which includes both offline segments such as brick-and-mortar stores and online segments like e-commerce sites, is a significant market for automotive parts. Key categories include brake parts, electrical parts, fuel intake, ignition parts, A/C parts, suspension parts, exhaust parts, engine cooling parts, steering parts, wheels, tires, and passenger cars. Authorized dealers and e-commerce sites are the primary channels for sales in this market. The regulatory environment is a critical factor influencing the automotive parts market.

What challenges does the Poland Automotive Parts Market face during the growth?

- Uncertain demand and high SKUs for automotive parts are a key challenge affecting the market growth. The market is experiencing increased demand due to various factors, including the regulatory environment focusing on vehicle emissions and the emergence of environmentally sustainable technologies such as electric vehicles (EVs), electric drivetrains, batteries, and charging infrastructure. This trend is driving innovation in cutting-edge technology areas like autonomous vehicle technology, sensors, radar systems, and LIDAR technology. Moreover, the market dynamics are influenced by changing economic conditions, leading to growth in both the offline and online segments.

- Despite the growth opportunities, the market faces challenges, such as precise demand forecasting for non-contract automotive parts supply chains. The unpredictable nature of demand and subsequent inaccurate forecasts can lead to financial consequences for OEMs and logistics companies. Additionally, the automotive parts SKU portfolio is expanding due to market-specific variants and various types of vehicles, including electric and autonomous vehicles. Effective supply chain management and demand forecasting are crucial to mitigate these challenges and ensure a smooth flow of parts to the market.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

BorgWarner Inc. - The company offers automotive parts such as AWD couplings, and turbochargers.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anwa Tech Sp. z o. o

- Dayco IP Holdings LLC

- Faurecia SE

- Hutchinson SA

- Inter Cars S.A

- Knauf Industries Polska Sp. Z OO

- LAMAR Sp. z o. o.

- Moderntech Sp. z o.o.

- Muhr und Bender KG

- Nexteer Automotive corp

- PGM Automotive sp. z o.o

- Pro Cars Group sp. z o.o.

- SOME Group

- TEDGUM

- TOMEX Brakes sp. z o.o. sp.k.

- TURBOJULITA SP Z O O

- Union Parts Sp. z o.o

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing demand for environmentally sustainable vehicles and the regulatory environment pushing for reduced emissions. This trend is particularly prominent in emerging markets where economic conditions continue to improve and consumers prioritize eco-friendly options. Electric vehicles (EVs) and electric drivetrains are at the forefront of this shift, with batteries and charging infrastructure being key components driving market expansion. The electrification of vehicles is leading to a rise in demand for advanced technology, such as sensors, radar systems, and lidar technology, which are essential for autonomous vehicle operation. Cutting-edge technology is also playing a crucial role in the development of new braking components, headlamps, and other automotive parts.

Further, traditional manufacturing methods are being replaced by innovative technologies like 3D printing, enabling faster production and customization. The market dynamics of the automotive parts industry are evolving, with the offline segment, including brick-and-mortar stores, facing increased competition from the online segment. E-commerce sites are gaining popularity due to their convenience and accessibility, offering a wider range of products and competitive pricing. The automotive aftermarket, which includes auto accessories and parts for passenger cars, is a significant contributor to the overall market. OEM suppliers are expanding their offerings to cater to the aftermarket, while suppliers associations and the Auto Care Association play a vital role in setting industry standards and promoting growth.

In addition, the accessory market scope is vast, encompassing various categories such as brake parts, electrical parts, fuel intake, ignition parts, A/C parts, suspension parts, exhaust parts, engine cooling parts, steering parts, wheels, tires, and more. The demand for these parts is influenced by vehicle type and consumer preferences. Authorized dealers remain an essential distribution channel for automotive parts, providing customers with genuine and high-quality products. However, the increasing popularity of e-commerce is disrupting traditional sales channels and forcing companies to adapt to the changing market landscape.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.5% |

|

Market growth 2025-2029 |

USD 24.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

11.1 |

|

Key countries |

Poland |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Poland

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -