Automotive Semiconductor Market Size 2024-2028

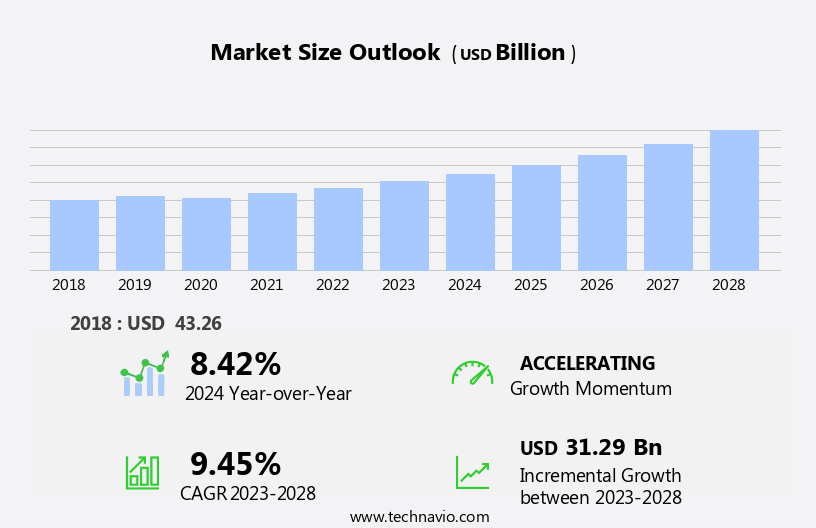

The automotive semiconductor market size is forecast to increase by USD 31.29 billion, at a CAGR of 9.45% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing adoption of Advanced Driver Assistance Systems (ADAS) in vehicles. This trend is fueled by consumer demand for enhanced safety features and government regulations mandating their implementation. Furthermore, advancements in semi-autonomous and autonomous vehicle technologies are accelerating the market's expansion. However, challenges persist, including the lack of standard protocols for these emerging technologies. This fragmentation hampers interoperability and may impede the market's growth potential.

- Companies must navigate these challenges by collaborating to establish industry-wide standards and investing in research and development to create innovative solutions. By capitalizing on these opportunities and addressing the challenges, market participants can position themselves for success in the evolving automotive semiconductor landscape.

What will be the Size of the Automotive Semiconductor Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

Functional safety, testing and validation, and product lifecycle management are essential aspects of semiconductor design and manufacturing processes. Over-the-air updates and electromagnetic compatibility ensure reliable and secure vehicle operation. Wire bonding and packaging technologies are essential for semiconductor fabrication and distribution channels. Real-time operating systems and machine learning algorithms are used in various applications, from infotainment systems to safety systems. Silicon carbide and gallium nitride are emerging materials for power electronics, offering improved efficiency and reliability. Manufacturing processes, thermal management, and supply chain optimization are ongoing concerns for semiconductor companies. Sensor fusion, image processing, and ADAS systems are critical components of modern vehicles, requiring sophisticated semiconductor solutions.

DC-DC converters and safety systems ensure reliable power supply and vehicle protection. In the ever-evolving automotive landscape, semiconductor technologies continue to play a vital role, enabling innovation and driving progress in areas such as electrification, connectivity, and autonomous driving.

How is this Automotive Semiconductor Industry segmented?

The automotive semiconductor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Telematics and infotainment

- Powertrain

- Safety

- Body electronics

- Chassis

- Vehicle Type

- Passenger vehicle

- Light commercial vehicle

- Heavy commercial vehicle

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

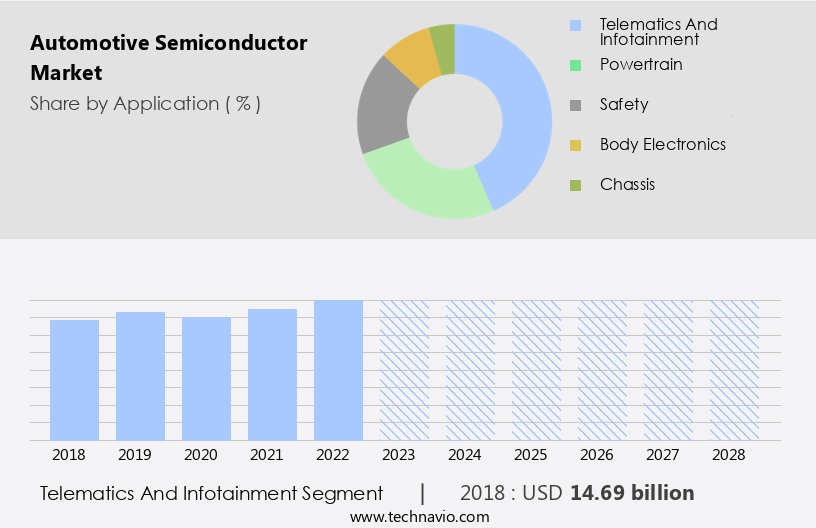

By Application Insights

The telematics and infotainment segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing emphasis on vehicle safety and advanced technologies. Telematics and infotainment systems, which rely on semiconductors, are becoming increasingly sophisticated. Real-time operating systems, machine learning, and artificial intelligence are being integrated to enhance passenger safety and provide features such as navigation, entertainment, and remote vehicle monitoring. Functional safety, electromagnetic compatibility, and emissions reduction are critical considerations in the automotive industry. Digital ICs, high-performance computing, and data analytics are essential for implementing advanced driver-assistance systems (ADAS), autonomous driving, and electric powertrains. High-voltage electronics, battery management systems, and power semiconductors are crucial components of electric and hybrid vehicles.

Over-the-air updates, vehicle networking, and sensor fusion enable continuous improvement and optimization of vehicle performance. Manufacturing processes, such as wafer processing, die attach, and packaging technologies, ensure the reliability and durability of semiconductor components. The supply chain and distribution channels are also essential for ensuring timely delivery and availability of semiconductors to automotive OEMs and Tier 1 suppliers. The integration of automotive ethernet, CAN bus, and LIN bus enables seamless communication between various vehicle systems. Motor control, power management, and thermal management are essential for optimizing vehicle performance and efficiency. Silicon carbide and gallium nitride are gaining popularity for their high power density and efficiency in power electronics applications.

Quality control and testing and validation are crucial for ensuring the reliability and safety of semiconductor components. Product lifecycle management and safety systems are essential for managing the development, production, and end-of-life disposal of semiconductor products. Image processing, ADAS systems, and infotainment systems are key applications of semiconductors in the automotive industry.

The Telematics and infotainment segment was valued at USD 14.69 billion in 2018 and showed a gradual increase during the forecast period.

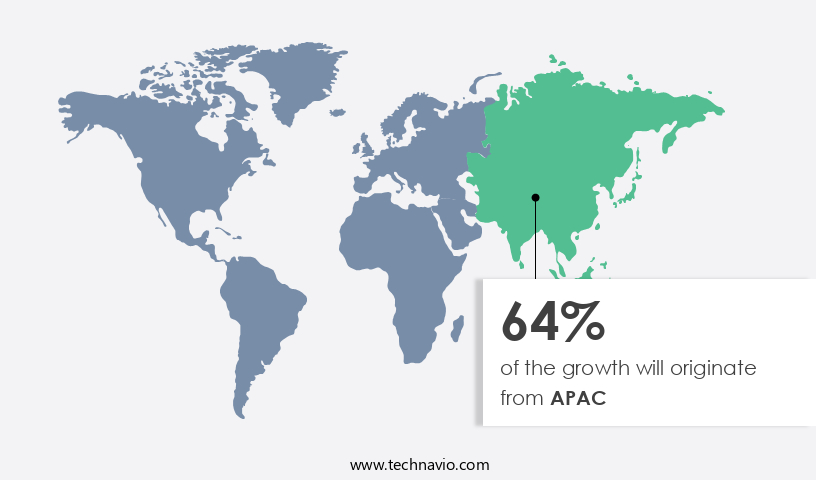

Regional Analysis

APAC is estimated to contribute 64% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in APAC is experiencing significant growth due to the increasing adoption of advanced technologies in the region's automotive industry. China, Japan, South Korea, and India are leading the way, with China being the largest market for automotive semiconductors in APAC. The growing presence of automotive manufacturers, expanding global footprint, and the adoption of advanced solutions such as digital ICs, functional safety, high-voltage electronics, over-the-air updates, electromagnetic compatibility, electric and hybrid vehicles, image processing, and autonomous driving are driving the market's growth. Moreover, the focus on product lifecycle management, quality control, charging infrastructure, thermal management, and manufacturing processes is leading to the integration of various technologies like high-performance computing, automotive ethernet, power semiconductors, sensor fusion, and real-time operating systems.

The increasing demand for emissions reduction, fuel efficiency, and battery management systems is also fueling the market's growth. The adoption of advanced driver-assistance systems (ADAS), power inverters, and safety systems is further boosting the market's growth. The integration of machine learning, artificial intelligence, and embedded software is enabling the development of software-defined vehicles and vehicle networking. Additionally, the use of gallium nitride, silicon carbide, and other advanced materials in power semiconductors and motor control is improving vehicle performance and efficiency. The market in APAC is expected to continue its growth trajectory due to the increasing focus on power management, data analytics, and the development of electric powertrains.

The supply chain and packaging technologies are also evolving to meet the demands of the automotive industry, with a focus on semiconductor fabrication, distribution channels, and automotive spice certification. Overall, the market in APAC is witnessing significant growth due to the increasing adoption of advanced technologies and the expanding automotive industry.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and innovative sector that designs, develops, and manufactures electronic components for the automotive industry. These semiconductors play a crucial role in enhancing vehicle performance, safety, and connectivity. Advanced driver-assistance systems (ADAS), electric vehicle (EV) technology, and infotainment systems are primary applications driving market growth. Semiconductor solutions enable features like lane departure warnings, automatic emergency braking, and adaptive cruise control, contributing to improved road safety. Moreover, semiconductors are essential for EV batteries, motor control, and charging infrastructure, propelling the electrification trend. The market's future lies in autonomous driving, where semiconductors will power sensors, process data, and enable real-time decision making. Additionally, the integration of 5G technology and the Internet of Things (IoT) in vehicles will further expand market opportunities. Overall, the market is poised for significant growth, fueled by technological advancements and evolving consumer expectations.

What are the key market drivers leading to the rise in the adoption of Automotive Semiconductor Industry?

- The increasing integration of Advanced Driver Assistance Systems (ADAS) in vehicles serves as the primary market catalyst.

- The market is experiencing significant growth due to the increasing adoption of advanced driver assistance systems (ADAS) in vehicles. The integration of software algorithms, processors, sensors, cameras, and mapping technologies has enhanced the capabilities of ADAS applications, making them an essential safety feature in modern vehicles. Governments worldwide are imposing stringent safety regulations on automotive manufacturers, requiring the production of vehicles equipped with ADAS features. For instance, the Indian government mandates the installation of a co-driver airbag in all vehicle segments, while the European Commission mandates the installation of a vehicle telematics system in all new vehicles.

- Moreover, the shift towards electric and hybrid vehicles is fueling the demand for high-voltage electronics, digital ICS, functional safety, product lifecycle management, electromagnetic compatibility, image processing, and over-the-air updates in the market. Quality control and charging infrastructure are other critical areas where semiconductors play a crucial role. Die attach technology ensures the reliable connection of semiconductors to the substrate, while ensuring harmonious and immersive user experiences remains a key focus area for automotive semiconductor manufacturers. Testing and validation are essential aspects of the market, ensuring the reliability and safety of semiconductor components in vehicles.

- The market's dynamics are influenced by various factors, including technological advancements, regulatory requirements, and consumer preferences. The adoption of these advanced technologies is expected to continue driving the growth of the market during the forecast period.

What are the market trends shaping the Automotive Semiconductor Industry?

- The trend in the automotive industry is shifting towards increasing advancements in semi-autonomous and autonomous vehicles. This development is mandatory for staying competitive in the upcoming market.

- Autonomous vehicles, also referred to as self-driving cars, are revolutionizing the automotive industry by merging computers, the Internet, smartphones, and advanced technologies with vehicles for automated driving operations. Rapid advancements in sensor-processing technologies, superior quality planning, adaptive algorithms, and communication technologies are propelling companies to expand their production capacities and elevate vehicle automation. The adoption of autonomous vehicles is expected to reduce vehicle operating costs, enhance travel convenience and comfort, and encourage long-distance commutes. High-performance computing, artificial intelligence, and data analytics play significant roles in enabling autonomous vehicles to read and sense their environments, make decisions, and communicate with other vehicles and infrastructure.

- Automotive Ethernet, CAN bus, and software-defined vehicles facilitate vehicle networking, while battery management systems and emissions reduction technologies contribute to improved fuel efficiency. Mixed-signal ICs are essential components in the development of autonomous vehicles due to their ability to process both analog and digital signals. Autonomous vehicles represent a major shift towards immersive, harmonious, and thematic experiences for drivers and passengers. Companies are investing heavily in research and development to create safer, more efficient, and more convenient transportation solutions. The future of the automotive industry lies in the integration of advanced technologies and the development of intelligent, connected vehicles.

What challenges does the Automotive Semiconductor Industry face during its growth?

- The absence of standardized protocols poses a significant challenge to the industry's growth trajectory. It is crucial to establish uniform procedures to ensure efficiency, consistency, and competitiveness within the sector.

- In the automotive industry, adhering to various regulations is a significant challenge. These regulations, designed to enhance safety, reduce thefts, and minimize environmental impact, can limit engineers' and designers' creativity. Each country or region sets its unique standards, necessitating automobile manufacturers to adapt their production processes to distribute their products globally. This regulatory complexity results in financial losses as companies must establish separate assembly units to comply with local requirements. Advanced technologies, such as power inverters, ADAS systems, thermal management, and motor control, are driving innovation in the market. Technologies like silicon carbide, gallium nitride, real-time operating systems, machine learning, embedded software, and analog ICs are essential components of these advanced systems.

- For instance, power inverters convert DC power to AC power, enabling the operation of various electrical systems in a vehicle. ADAS systems, which include features like lane departure warning, automatic emergency braking, and adaptive cruise control, rely on sensors and sophisticated algorithms to improve safety. Thermal management is crucial for maintaining optimal operating temperatures in electronic systems, ensuring their longevity and efficiency. Motor control technologies enable efficient power usage and improved performance in electric and hybrid vehicles. Machine learning and embedded software enable advanced features like predictive maintenance and driver behavior analysis. Gallium nitride and silicon carbide are gaining popularity due to their high power handling capabilities and efficiency.

- In conclusion, the market is undergoing significant changes, driven by the adoption of advanced technologies and evolving regulatory requirements. Manufacturers must navigate these challenges to stay competitive and meet the growing demand for safer, more efficient, and environmentally friendly vehicles.

Exclusive Customer Landscape

The automotive semiconductor market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive semiconductor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive semiconductor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allegro MicroSystems Inc. - This company specializes in advanced semiconductor solutions, engineered for powertrain, safety, and infotainment systems in the automotive sector. Designed with innovative technology, these semiconductors enhance vehicle performance and safety, while contributing to an optimized user experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allegro MicroSystems Inc.

- Analog Devices Inc.

- BorgWarner Inc.

- Continental AG

- DENSO Corp.

- Elmos Semiconductor AG

- Infineon Technologies AG

- Intel Corp.

- Microchip Technology Inc.

- Micron Technology Inc.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- ROHM Co. Ltd.

- Samsung Electronics Co. Ltd.

- STMicroelectronics International N.V.

- Texas Instruments Inc.

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Semiconductor Market

- In January 2024, Infineon Technologies AG, a leading automotive semiconductor supplier, announced the launch of its new AURIX TC3xx family of microcontrollers, designed to support advanced driver assistance systems (ADAS) and electric vehicle (EV) applications (Infineon Press Release, 2024). This expansion of their product portfolio underscores their commitment to the evolving automotive electronics market.

- In March 2024, NXP Semiconductors and Qualcomm entered into a strategic partnership to collaborate on automotive semiconductor solutions, combining NXP's automotive expertise with Qualcomm's connectivity and computing technologies (NXP Press Release, 2024). This alliance aims to address the growing demand for integrated, advanced driver assistance and connectivity systems in modern vehicles.

- In May 2024, Renesas Electronics Corporation completed the acquisition of Dialog Semiconductor, significantly expanding its power management and connectivity product offerings for the automotive market (Renesas Press Release, 2024). This strategic move positions Renesas as a leading provider of power management and connectivity solutions for the growing electric vehicle segment.

- In April 2025, Texas Instruments received regulatory approval for its new semiconductor manufacturing facility in Richardson, Texas, with an investment of USD3.1 billion (TI Press Release, 2025). This expansion will increase the company's production capacity for automotive semiconductors, enabling it to meet the surging demand for advanced driver assistance systems and electric vehicle components.

Research Analyst Overview

- The market is witnessing significant advancements, driven by the integration of various technologies such as Cellular V2X, image sensors, and ultrasonic sensors. These innovations are transforming vehicles into connected, intelligent systems that prioritize safety and efficiency. Industry standards and distribution networks play a crucial role in ensuring seamless integration of these advanced semiconductor solutions. V2X communication and parallel processing are essential for real-time data exchange between vehicles and their surroundings, enhancing on-board diagnostics (OBD) and aftermarket support. Technical specifications, hardware acceleration, and design verification are essential for optimizing performance and reducing costs. Inventory control, warranty claims, and supply chain management are key areas where semiconductor solutions contribute to improved system-on-a-chip (SoC) functionality and fault detection.

- The market continues to evolve, driven by the integration of advanced technologies and the dynamic needs of various sectors. Artificial intelligence (AI) and high-performance computing (HPC) are increasingly essential for autonomous driving and advanced driver-assistance systems (ADAS). Automotive Ethernet and vehicle networking facilitate seamless data transfer and communication between different vehicle systems. High-voltage electronics, power semiconductors, and power management ICs are crucial for electric and hybrid vehicles, enabling efficient energy conversion and management. Emissions reduction and fuel efficiency are key concerns, leading to the adoption of battery management systems and the development of more efficient motor control solutions. Data analytics and CAN bus help optimize vehicle performance and improve quality control.

- Cloud connectivity, low-power design, and performance optimization are essential trends, enabling the development of advanced embedded systems. Global standards bodies are instrumental in ensuring compatibility and interoperability, while system integration and wireless communication streamline service maintenance and fault detection. Parallel processing, on-board diagnostics, and image sensors are critical components in the market, driving innovation and growth. The focus on cost reduction, inventory control, and warranty claims is essential for maintaining a competitive edge in this dynamic industry.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Semiconductor Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

193 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.45% |

|

Market growth 2024-2028 |

USD 31.29 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.42 |

|

Key countries |

China, US, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Semiconductor Market Research and Growth Report?

- CAGR of the Automotive Semiconductor industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive semiconductor market growth of industry companies

We can help! Our analysts can customize this automotive semiconductor market research report to meet your requirements.

RIA -

RIA -