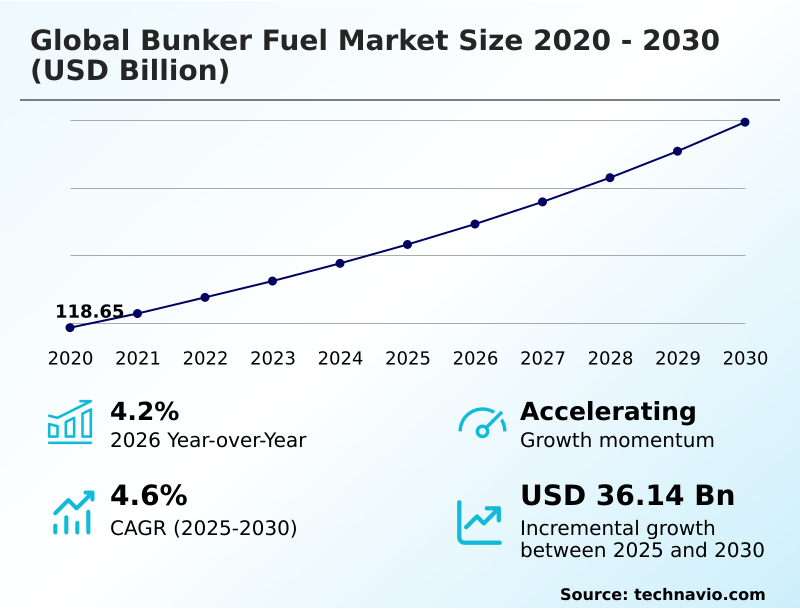

Bunker Fuel Market Size 2026-2030

The bunker fuel market size is valued to increase by USD 36.14 billion, at a CAGR of 4.6% from 2025 to 2030. Implementation of rigorous decarbonization mandates and standards will drive the bunker fuel market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 39.5% growth during the forecast period.

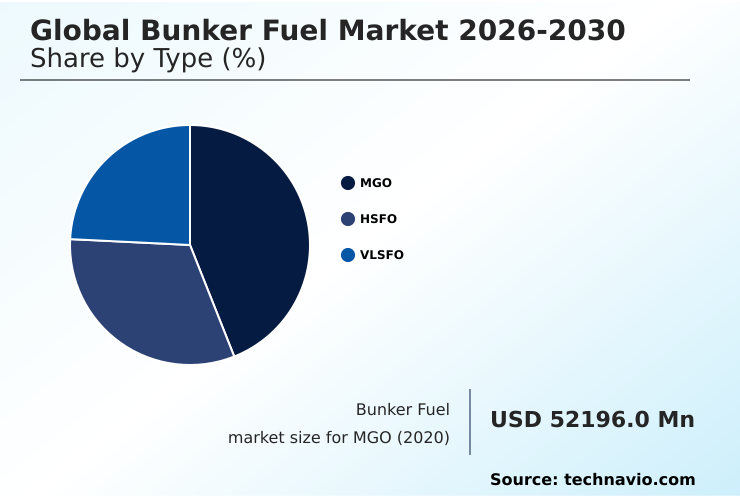

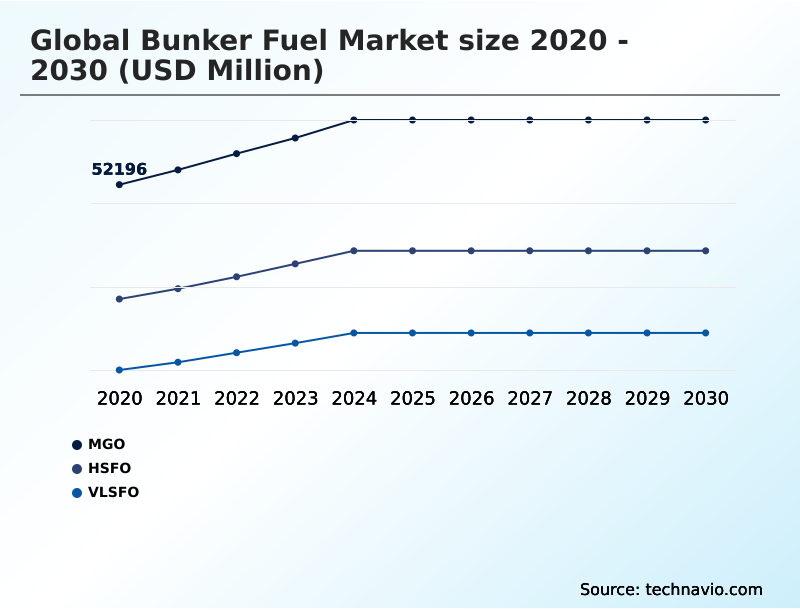

- By Type - MGO segment was valued at USD 60.38 billion in 2024

- By Application - Container segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 60.71 billion

- Market Future Opportunities: USD 36.14 billion

- CAGR from 2025 to 2030 : 4.6%

Market Summary

- The Bunker Fuel Market is in a period of unprecedented transformation, moving away from a single-fuel dependency toward a complex, multi-fuel ecosystem. This shift is driven by stringent decarbonization mandates, such as the carbon intensity indicator (CII) regulations and the EU ETS, which penalize greenhouse gas emissions.

- As a result, shipowners are compelled to explore a range of low-carbon alternatives, including LNG bunkering, biofuels, and green methanol. This transition creates significant challenges, from the high cost of alternative fuel infrastructure to the logistical complexities of a fragmented global supply chain.

- For instance, a container line planning a voyage from Asia to Europe must now consider not only the price but also the availability of compliant fuels like a B30 blend or VLSFO at various transshipment hubs, balancing the cost of carbon allowances against potential rerouting.

- The industry is responding with innovation, developing green maritime corridors and adopting digital tools like electronic bunker delivery notes (eBDN) to enhance transparency and efficiency. This dynamic environment demands a strategic approach to fuel procurement and vessel technology investment to maintain competitiveness while navigating the path to net-zero.

What will be the Size of the Bunker Fuel Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Bunker Fuel Market Segmented?

The bunker fuel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- MGO

- HSFO

- VLSFO

- Application

- Container

- Bulk carrier

- Oil tanker

- General cargo

- Chemical tanker

- Distribution channel

- IOC or NOC

- Large independent distributor

- Small independent distributor

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- The Netherlands

- UK

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The mgo segment is estimated to witness significant growth during the forecast period.

The marine gas oil (MGO) segment is a critical compliance pathway, serving vessels in Emission Control Areas (ECAs) with sulfur limits capped at 0.10%. Demand for this distillate, including various bio-distillates, is rising due to expanding regulations.

Its use simplifies onboard handling, and the market is adapting as smaller ports invest in storage, enhancing last-mile delivery.

The move towards bio-blending with components like Fatty Acid Methyl Esters (FAME) is vital for improving a vessel's Carbon Intensity Indicator (CII).

This shift, supported by ISO 8217 standards for fuel quality assurance, is driving investment in refining capacity for middle distillates and drop-in biofuels, moving MGO from a niche product to a strategic necessity.

The MGO segment was valued at USD 60.38 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 39.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Bunker Fuel Market Demand is Rising in APAC Get Free Sample

APAC is central to market dynamics, accounting for 39.5% of incremental growth. Singapore's mandate for mass flow meters has enhanced delivery accuracy by over 99%, setting a standard for the bunker supply chain.

Europe's market, operating within strict Emission Control Areas (ECA), leads the transition toward bio-blending solutions using FAME and HVO. However, this creates a risk of 'bunker tourism'.

The Middle East adapts to geopolitical shifts, with Fujairah expanding capacity, while African ports manage surges from rerouted vessels.

This global landscape requires advanced voyage optimization and robust bunkering safety protocols to manage a complex marine fuel logistics network, including the sourcing of products like a B24 blend.

Market Dynamics

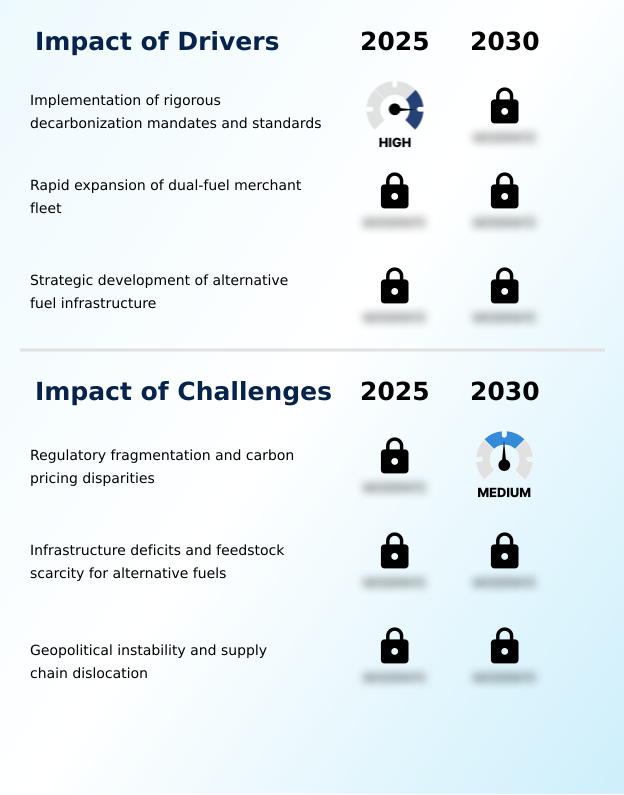

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern Bunker Fuel Market requires a sophisticated understanding of competing decarbonization pathways. A central decision for fleet operators is the VLSFO vs HSFO with scrubbers debate, where the ROI of dual-fuel vessel conversion must be weighed against initial capital outlay.

- The cost of LNG bunkering infrastructure remains a significant barrier for many ports, complicating the widespread adoption of gas-as-a-fuel. Similarly, the challenges of green methanol adoption include sourcing and price volatility. As regulations tighten, understanding marine biofuel blending regulations and the impact of EU ETS on bunkering becomes critical for compliance.

- The future of heavy fuel oil is increasingly tied to the development of onboard carbon capture technologies. For emerging zero-carbon options, establishing safety protocols for ammonia bunkering and building a resilient supply chain for green hydrogen are monumental tasks. The role of digitalization in bunkering is expanding, with technical standards for e-BDNs essential for mitigating operational risks of fuel compatibility.

- This digital shift, alongside the mass balance approach for biofuels and investment in multi-fuel terminals, is key to developing green maritime corridors. Effective management of carbon pricing in shipping now hinges on accurate carbon intensity rating calculation, strategic alternative fuel feedstock sourcing, and a clear view of market dynamics.

What are the key market drivers leading to the rise in the adoption of Bunker Fuel Industry?

- The implementation of rigorous decarbonization mandates and standards serves as a key driver for the market's transition toward cleaner fuel alternatives.

- Stringent regulations like IMO 2020 and the EU ETS are the primary driver, compelling a shift from heavy fuel oil.

- The FuelEU Maritime regulation, with its mandated greenhouse gas intensity reductions, creates direct financial incentives for adopting biofuels or renewable diesel.

- The aggressive expansion of the dual-fuel vessel order book, featuring advanced dual-fuel propulsion systems, creates immediate demand for LNG bunkering. This transition from piloting to deployment future-proofs fleets. Strategic investment in alternative fuel infrastructure is also critical.

- New multi-fuel bunkering services allow vessels to refuel at key chokepoints, while specialized bunker barges reduce turnaround times by over 30%, making new fuels operationally competitive.

What are the market trends shaping the Bunker Fuel Industry?

- The digitalization of the bunker supply chain is a prominent market trend. It is characterized by the adoption of electronic verification methods to enhance transparency and efficiency.

- The industry is shifting toward total digitalization, with the adoption of electronic bunker delivery notes (eBDN) improving transparency. Integrating mass flow meter data into digital platforms creates an immutable chain of custody, reducing verification times by over 40%. Green maritime corridors are reshaping the market, focusing on fuels like green methanol.

- These corridors aim to aggregate demand, potentially lowering the price gap for alternative fuels by 15%. A key trend is the mainstreaming of bio-blending solutions, such as a B30 blend with VLSFO, which utilizes mass balance certification to expand availability of low-carbon alternatives.

- This digitally tracks sustainability credits, enabling compliance without requiring physical fuel segregation at every stage of the bunker supply chain.

What challenges does the Bunker Fuel Industry face during its growth?

- Regulatory fragmentation and carbon pricing disparities present a key challenge affecting the industry's operational and financial landscape.

- A fragmented regulatory landscape and carbon pricing disparities create significant distortions. This incentivizes evasive port calls to transshipment hubs to avoid regional regulations. The gap between ambition and infrastructure readiness is another challenge, particularly for fuels like green ammonia or synthetic methane, where feedstock availability is limited.

- For vessels with exhaust gas cleaning systems (scrubbers) using HSFO, this isn't an issue, but for those on VLSFO, sourcing compliant fuel is paramount. Geopolitical instability also disrupts supply chains, forcing costly rerouting that leads to bunkering delays exceeding 72 hours in some ports.

- This volatility complicates fuel procurement strategy and increases operational risk for all fuel types, including gas-to-liquids (GTL) products.

Exclusive Technavio Analysis on Customer Landscape

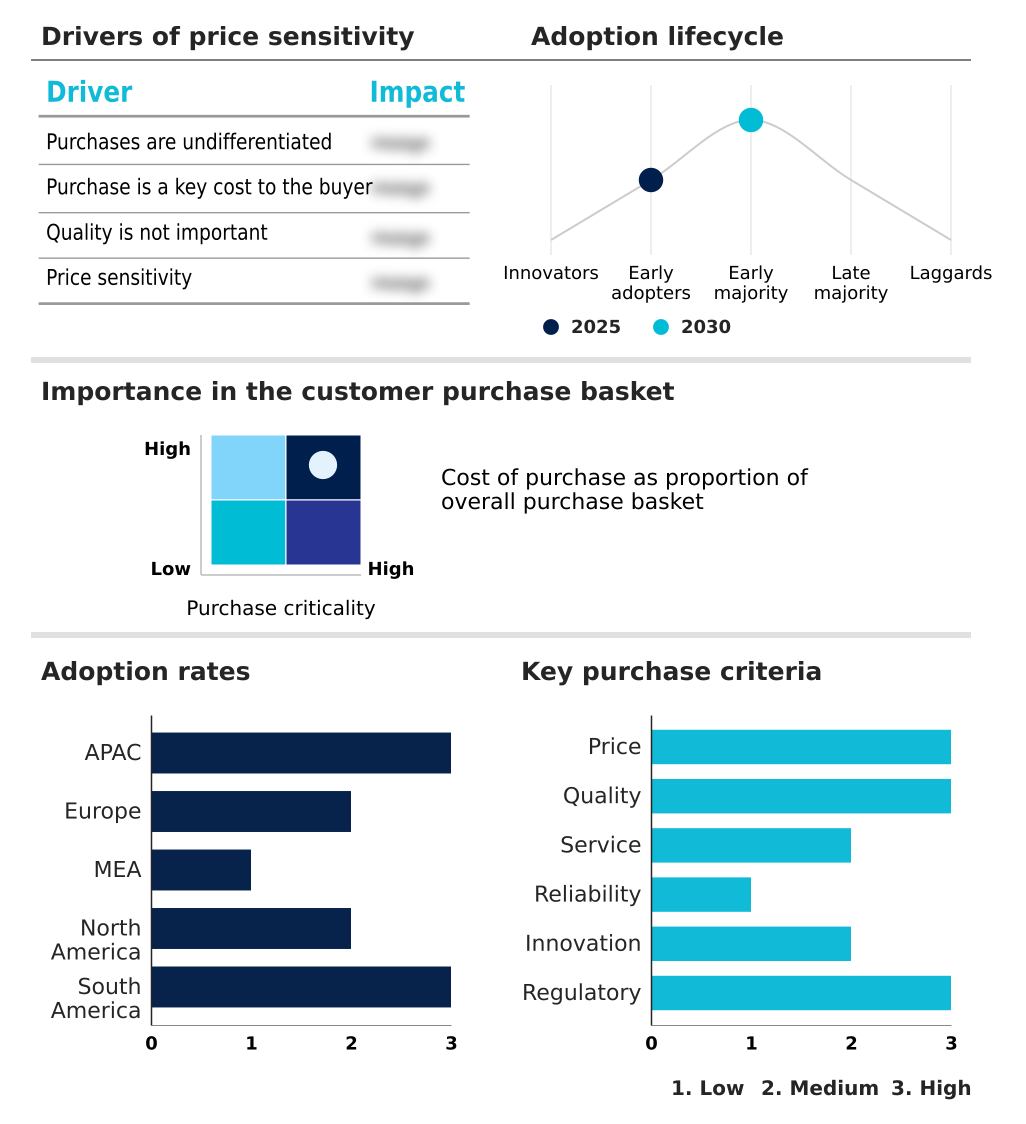

The bunker fuel market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bunker fuel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Bunker Fuel Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, bunker fuel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aegis Logistics Ltd. - Delivers key marine fuel grades, including marine gas oil (MGO), essential for global vessel propulsion and operational compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aegis Logistics Ltd.

- Bunker Oil AS

- Chevron Corp.

- Eni SpA

- Exxon Mobil Corp.

- Gulf Agency Co. Ltd.

- Hindustan Petroleum Corp. Ltd.

- Indian Oil Corp. Ltd.

- Maritime Optima

- Petroliam Nasional Berhad

- Shell plc

- Shiny Shipping and Logistics Pvt Ltd

- ShipServ Limited

- TotalEnergies SE

- Vizag Chemical International

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bunker fuel market

- In November 2024, ZeroNorth integrated its e-bunkering capability with fuel supplier systems in the Port of Rotterdam, enabling seamless transmission of digital bunker delivery notes.

- In March 2025, Panam LNG Bunkering, a joint venture between AES Corporation and Seaspan Energy, launched commercial LNG bunkering services in Panama, enhancing fuel availability at a key maritime chokepoint.

- In March 2025, Monjasa completed a B30 biofuel supply operation in the Middle East, utilizing a mass balance chain of custody to provide ISCC-certified proof of sustainability.

- In May 2025, The Port of Rotterdam Authority announced a revised timeline for its green hydrogen and methanol import terminal, citing supply chain constraints for electrolyzer procurement.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bunker Fuel Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2026-2030 | USD 36141.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.2% |

| Key countries | Singapore, China, Japan, South Korea, India, Indonesia, Germany, The Netherlands, UK, France, Spain, Italy, UAE, Saudi Arabia, South Africa, Qatar, Egypt, US, Canada, Mexico, Brazil, Chile and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Bunker Fuel Market is undergoing a profound structural shift, driven by regulatory pressures such as IMO 2020 and the EU ETS. This has fragmented the traditional reliance on heavy fuel oil (HFO) and high-sulfur fuel oil (HSFO), creating distinct pathways for compliance. One route involves installing exhaust gas cleaning systems (scrubbers) to continue using HSFO.

- The other, more common path, is the adoption of compliant fuels like very low sulfur fuel oil (VLSFO) and marine gas oil (MGO). The market is now a multi-fuel ecosystem, with LNG bunkering becoming established and emerging alternatives like green methanol and green ammonia gaining traction.

- To meet immediate carbon intensity indicator (CII) targets under regulations like FuelEU Maritime, shipowners are turning to drop-in biofuels. These include hydrotreated vegetable oil (HVO) and fatty acid methyl esters (FAME), often supplied as a B24 blend or B30 blend. The rise of dual-fuel propulsion technology is a direct response to this complexity.

- For transparency, the use of electronic bunker delivery notes (eBDN) is becoming standard, ensuring compliance with ISO 8217.

- The development of synthetic methane and gas-to-liquids (GTL) products, alongside renewable diesel and green hydrogen, points to a future where fuel choice is a critical boardroom decision, where the implementation of eBDNs has been shown to reduce administrative clearance times by up to 40%.

What are the Key Data Covered in this Bunker Fuel Market Research and Growth Report?

-

What is the expected growth of the Bunker Fuel Market between 2026 and 2030?

-

USD 36.14 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (MGO, HSFO, and VLSFO), Application (Container, Bulk carrier, Oil tanker, General cargo, and Chemical tanker), Distribution Channel (IOC or NOC, Large independent distributor, and Small independent distributor) and Geography (APAC, Europe, Middle East and Africa, North America, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, Middle East and Africa, North America and South America

-

-

What are the key growth drivers and market challenges?

-

Implementation of rigorous decarbonization mandates and standards, Regulatory fragmentation and carbon pricing disparities

-

-

Who are the major players in the Bunker Fuel Market?

-

Aegis Logistics Ltd., Bunker Oil AS, Chevron Corp., Eni SpA, Exxon Mobil Corp., Gulf Agency Co. Ltd., Hindustan Petroleum Corp. Ltd., Indian Oil Corp. Ltd., Maritime Optima, Petroliam Nasional Berhad, Shell plc, Shiny Shipping and Logistics Pvt Ltd, ShipServ Limited, TotalEnergies SE and Vizag Chemical International

-

Market Research Insights

- The bunker fuel market's dynamics are shaped by a complex interplay of logistical and regulatory factors. An effective fuel procurement strategy is paramount, moving beyond simple spot market purchasing to complex contract structures that ensure fuel compatibility and quality assurance.

- The entire bunker supply chain is being re-evaluated, with a focus on last-mile delivery and the development of alternative fuel infrastructure to support a multi-fuel bunkering reality. This includes cryogenic fuels, which demand stringent bunkering safety protocols.

- The rise of green maritime corridors and bio-blending solutions, supported by sustainability credits and a clear chain of custody, is transforming marine fuel logistics. The mass balance approach has expanded low-carbon options by 40% in ports lacking segregated infrastructure.

- Meanwhile, onboard carbon capture and voyage optimization technologies are critical for improving vessel energy efficiency, helping operators manage carbon pricing mechanisms and navigate transshipment hubs for strategic port call optimization. The use of mass flow meters has also reduced quantity disputes by up to 25%, demonstrating the value of transparency in fuel hedging for both marine distillates and residual fuels.

We can help! Our analysts can customize this bunker fuel market research report to meet your requirements.

RIA -

RIA -