Cellulose Derivatives Market Size 2024-2028

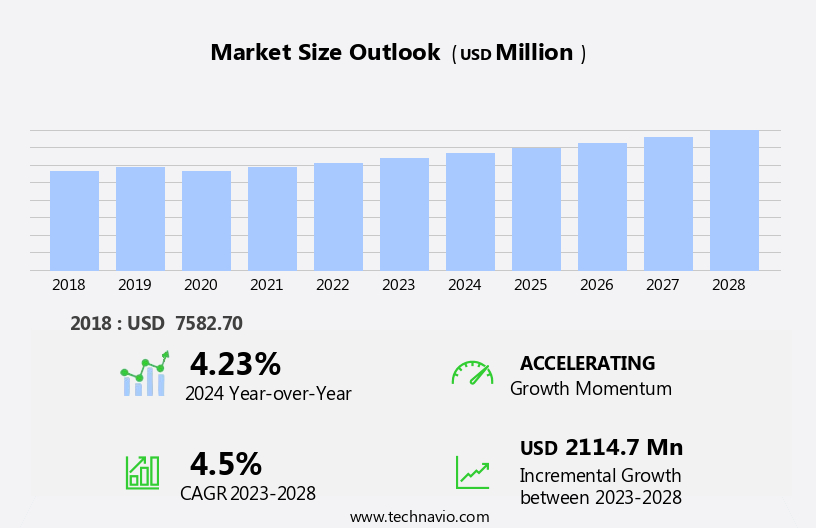

The cellulose derivatives market size is forecast to increase by USD 2.11 billion, at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing end-use applications in various industries, including textiles, food, pharmaceuticals, and agriculture. These derivatives offer numerous benefits, such as improved performance, cost savings, and sustainability, making them a preferred choice for manufacturers. However, the market faces challenges from stringent regulations and policies, particularly in the production and application of cellulose derivatives. For instance, the European Union's REACH regulations impose strict requirements on the production, use, and disposal of these chemicals.

- Additionally, there is a growing focus on the environmental impact of cellulose derivatives, with increasing pressure to adopt sustainable production methods and reduce waste. Companies seeking to capitalize on market opportunities must navigate these regulatory challenges while also addressing the need for sustainable production and innovation to meet evolving customer demands.

What will be the Size of the Cellulose Derivatives Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the constant demand for innovative applications across various sectors. Hydroxypropyl methylcellulose (HPMC) and water-soluble polymers, for instance, play significant roles in drug delivery systems, offering enhanced chemical resistance and biocompatibility. In the realm of biodegradable plastics, cellulosic polymers such as HPMC, hydroxyethyl cellulose (HEC), and carboxymethyl cellulose (CMC) are gaining traction due to their renewable nature and eco-friendly attributes. Meanwhile, the supply chain management of cellulose derivatives is undergoing transformative changes, with a focus on efficient raw material sourcing and inventory management. Membrane technology, thermal stability, and molecular weight distribution are crucial factors influencing the production and application of cellulose triacetate in areas like filtration and fiber optics.

In the realm of pharmaceutical excipients, cellulose derivatives like HPMC, HEC, and hydroxypropyl cellulose (HPC) are indispensable components in various formulations. Their role in improving mechanical properties, such as thickening and film-forming, is essential in the production of tablets, capsules, and coatings. Moreover, cellulose derivatives are making strides in the personal care industry, with applications ranging from thickening agents in cosmetics to ion exchange resins in water treatment. The ongoing research and development in this sector aim to enhance the performance and sustainability of these products. In the ever-changing landscape of cellulose derivatives, regulatory compliance and quality control are paramount.

Testing standards and product lifecycle management are critical aspects that ensure the consistent production and delivery of high-quality cellulose derivatives. As the market continues to unfold, the potential applications of cellulose derivatives in areas like ink jet printing, protective coatings, and solution casting are being explored, further expanding their reach and significance. The continuous dynamism of the market is a testament to the versatility and adaptability of these renewable resources.

How is this Cellulose Derivatives Industry segmented?

The cellulose derivatives industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

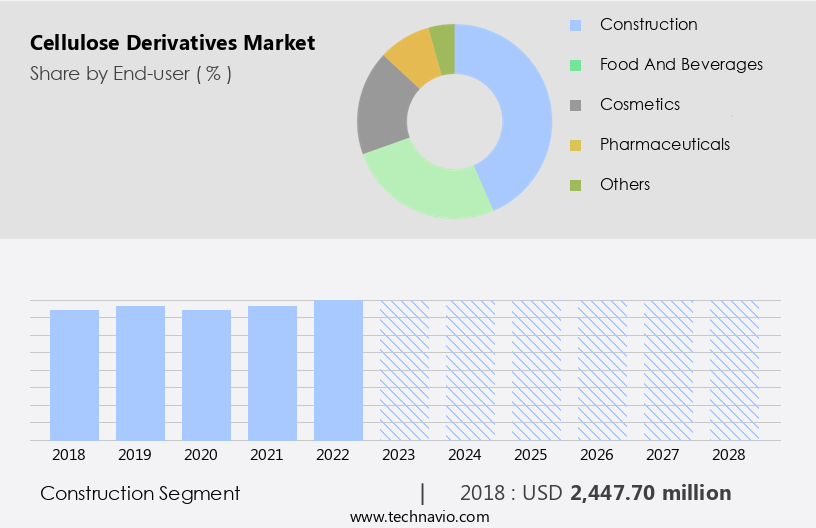

- Construction

- Food and beverages

- Cosmetics

- Pharmaceuticals

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period.

The market is experiencing notable growth, particularly in the construction segment. This segment's revenue growth is anticipated to outpace other industries, including food and beverages, cosmetics, and pharmaceuticals, during the forecast period. The construction industry's preference for cellulose derivatives is driven by the surge in residential, commercial, and industrial projects worldwide. Additionally, the increasing focus on eco-friendly chemicals in construction is fueling the demand for cellulose derivatives as a sustainable alternative to traditional chemicals. Cellulose derivatives, such as thickening agents, dispersing agents, cellulose nitrate, film forming agents, and paper coatings, play crucial roles in various industries.

In the construction sector, they enhance the mechanical properties of building materials, ensuring better performance and longevity. Moreover, cellulose derivatives' biodegradability and chemical resistance make them suitable for membrane technology, ion exchange resins, and protective coatings in construction applications. The raw material sourcing and supply chain management of cellulose derivatives are essential aspects of the market. Renewable resources, such as wood pulp, are the primary raw materials for producing cellulose derivatives. The production process involves chemical treatments, such as acetylation, etherification, and nitration, to modify the cellulose structure and create various derivatives. Cellulose derivatives have diverse applications in various industries, including membrane technology, fiber optics, pharmaceuticals, food additives, personal care products, and drug delivery systems.

For instance, in membrane technology, cellulose derivatives are used to create ion exchange resins and filtration membranes. In pharmaceuticals, they serve as excipients and coating materials for tablets and capsules. In food additives, they function as thickening agents, dispersing agents, and stabilizers. In personal care products, they are used as water-soluble polymers for solution casting and as film formers for skin care products. Regulatory compliance and testing standards are essential factors influencing the market dynamics. The regulatory bodies, such as the Food and Drug Administration (FDA) and the European Chemicals Agency (ECHA), set guidelines for the production, use, and labeling of cellulose derivatives.

Stringent testing standards ensure the quality and safety of cellulose derivatives, which is crucial for their adoption in various industries. In summary, The market is witnessing significant growth, particularly in the construction sector, due to the increasing focus on green chemicals and sustainable building materials. The diverse applications of cellulose derivatives in various industries, coupled with the stringent regulatory environment, ensure their continued demand and growth in the future.

The Construction segment was valued at USD 2.45 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

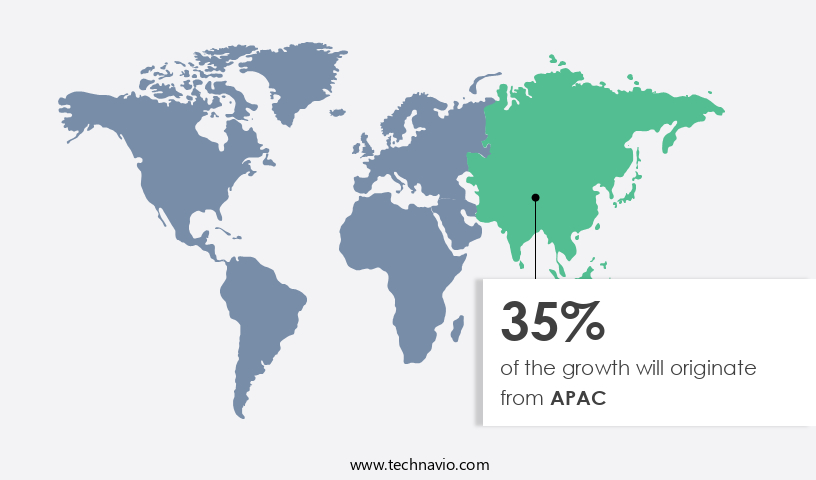

APAC is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market encompasses a range of products derived from cellulose, including thickening and dispersing agents, film forming agents, paper coatings, and more. These derivatives exhibit desirable properties such as thermal stability, chemical resistance, and biodegradability, making them valuable in various industries. In 2023, APAC emerged as the largest market for cellulose derivatives, driven by the region's significant production in countries like China, India, and Japan. The increasing demand for cellulose derivatives in applications such as veterinary foods, wood, paper, fibers, clothes, cosmetics, and pharmaceuticals is propelling market growth. Key players in this market include Shin-Etsu Chemical Co., Ltd., Shandong Head Co., Ltd., Hebei Jiahua Cellulose Co., Ltd., DKS Co.

Ltd., and DuPont de Nemours Inc. These companies contribute significantly to the market through their production of hydroxyethyl cellulose (HEC), hydroxypropyl methylcellulose (HPMC), carboxymethyl cellulose (CMC), cellulose acetate, and other cellulosic polymers. The market also incorporates raw material sourcing, membrane technology, testing standards, ink jet printing, and regulatory compliance to ensure product quality and consistency. Additionally, cellulose derivatives are used in various industries, including food additives, personal care products, pharmaceutical excipients, and coating materials, among others. The market's evolution is further characterized by innovations in molecular weight distribution, hydroxypropyl cellulose (HPC), and polymer additives, as well as the increasing use of renewable resources in the production of cellulose derivatives.

Supply chain management, solution casting, protective coatings, and spray coating are other key aspects of the market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Cellulose Derivatives Industry?

- The primary factor fueling market growth is the expanding scope of end-use applications.

- Cellulose derivatives are widely utilized in various industries due to their unique properties, leading to the market's significant expansion. These derivatives find extensive applications in pharmaceuticals, personal care, food, construction, oil and gas, and other sectors. In personal care, they act as modifiers in soaps, shampoos, and body lotions, which are popular among consumers. In the construction industry, cellulose derivatives are used for stabilizing, binding, water retention, film foaming, emulsion, and thickening in cement, textiles, detergents, coatings, paper-making, electronic components, chemical, and petroleum sectors.

- Moreover, the food industry's increasing demand for cellulose derivatives is noteworthy. They are used as thickeners in canned fruit pie fillings and frozen food production, as stabilizers, crystallization controllers, and moisture retention agents in various drinks and processed food formulations. The market's growth is driven by the expanding demand for these versatile products in numerous applications.

What are the market trends shaping the Cellulose Derivatives Industry?

- The current business landscape is witnessing significant advancements that are shaping market trends. These recent developments are essential for professionals to stay informed and adapt accordingly.

- The market is experiencing a significant surge in new product launches, driving consumer interest and increasing competition. Manufacturers are focusing on innovative and sustainable additives for various industries, including paints and coatings. For instance, in August 2021, Nouryon announced plans to construct a new manufacturing plant to meet the growing demand for such additives. Cellulose derivatives are widely used as thickening and dispersing agents in various applications, such as paper coatings and membrane technology. Their film-forming properties make them essential in these industries.

- Hydroxyethyl cellulose (HEC), a common cellulose derivative, is known for its thermal stability and molecular weight distribution, making it a preferred choice for numerous applications. Manufacturers are continually researching and developing new products to meet the evolving needs of their customers. This competition is leading to innovations and differentiation in the market, ensuring a diverse range of high-quality cellulose derivatives products for consumers.

What challenges does the Cellulose Derivatives Industry face during its growth?

- The strict regulations and policies in place represent a significant challenge to the expansion and growth of the industry.

- Cellulose derivatives, specifically hydroxypropyl methylcellulose (HPMC), play a significant role in various industries such as pharmaceuticals, food, and plastics due to their unique properties. In the pharmaceutical sector, water-soluble polymers like HPMC are extensively used in drug delivery systems for their chemical resistance and biodegradability. However, the production of cellulose derivatives is subject to stringent regulations from regulatory bodies like the Environmental Protection Agency (EPA), Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH), and the US Food and Drug Administration (FDA).

- These regulations, which include compliance with current good manufacturing practices (CGMP) and guidelines under the regulation EU No 10/2011, increase production costs and restrict market growth. Despite these challenges, cellulose derivatives continue to be in demand due to their wide range of applications, including ion exchange resins, wound dressings, and mechanical properties enhancement in various industries.

Exclusive Customer Landscape

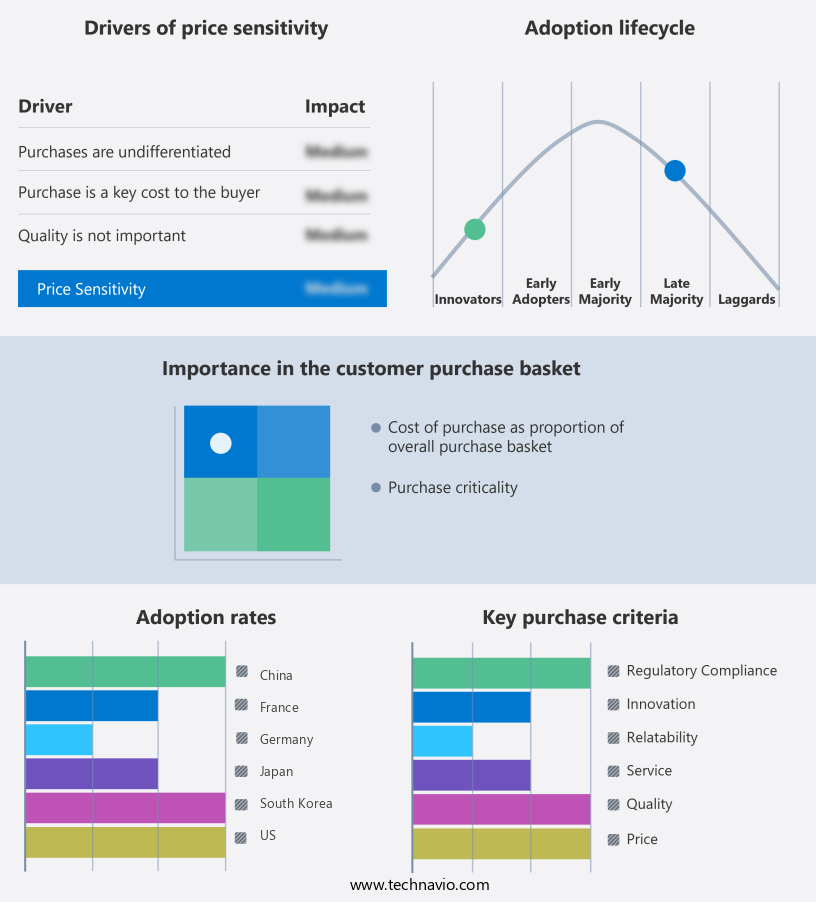

The cellulose derivatives market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cellulose derivatives market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, cellulose derivatives market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akzo Nobel NV - The company specializes in the production and supply of cellulose derivatives, including Bermocoll, which are utilized in various industries for their binding, thickening, and gelling properties. These eco-friendly alternatives offer numerous benefits, such as improved product performance and sustainability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Ashland Inc.

- Birla Cellulose

- Cerdia International GmbH

- Colorcon Inc.

- Daicel Corp.

- DKS Co. Ltd.

- DuPont de Nemours Inc.

- Eastman Chemical Co.

- FENCHEM

- J M Huber Corp.

- J RETTENMAIER and SOHNE GmbH and Co KG

- Lamberti SpA

- LOTTE Fine Chemical Co.

- Nouryon

- Sappi Ltd.

- SE Tylose GmbH and Co. KG

- Shandong Head Co. Ltd.

- Shin Etsu Chemical Co. Ltd.

- Zhejiang Haishen New Material Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cellulose Derivatives Market

- In January 2024, Eastman Chemical Company announced the expansion of its cellulose derivatives production capacity at its Kingsport, Tennessee, facility. This USD100 million investment aimed to increase production of cellulosic fibers and films, addressing the growing demand for sustainable alternatives in various industries (Eastman Press Release).

- In March 2024, Mitsubishi Chemical Corporation and Nippon Paper Industries Co. Ltd. Entered into a strategic collaboration to develop and commercialize new cellulose derivative products. Their joint efforts focused on enhancing the performance and sustainability of these materials for use in packaging, textiles, and other applications (Nikkei Asia).

- In May 2024, Avantor Performance Materials, a leading supplier of specialty chemicals, completed the acquisition of a majority stake in Carboseal, a cellulose ester manufacturer. This strategic move expanded Avantor's portfolio and capabilities in the market (Avantor Press Release).

- In April 2025, the European Union approved the use of microbial cellulose in food packaging, marking a significant regulatory milestone for the cellulose derivatives industry. This approval opened new opportunities for the production and commercialization of sustainable, biodegradable alternatives to traditional plastic packaging materials (European Commission Press Release).

Research Analyst Overview

- The market encompasses a wide range of applications, from sustainable packaging to biomedical uses. Sustainable packaging applications, driven by consumer demand for eco-friendly solutions, continue to fuel market growth. In drug encapsulation, cellulose derivatives offer advantages such as controlled release and improved stability. Tensile strength and impact resistance are crucial factors in construction materials, making cellulosic fibers a popular choice. Biomedical applications, including tissue engineering and chemical modification, leverage the unique properties of regenerated cellulose and cellulose nanocrystals (CNC) and nanofibrils (CNF). Production capacity expansion and process optimization are essential for meeting market demands. Water resistance and oxygen barrier properties are essential for packaging materials, while moisture content and gas permeability are key considerations for oil and gas applications.

- Chemical modification and particle size distribution play a significant role in enhancing the rheological behavior and surface tension of cellulose derivatives. Barrier properties, UV resistance, and dissolution testing are crucial for various industries, including additives manufacturing and 3D printing. Cellulose microfibrils and CNC offer enhanced water absorption and oil absorption capabilities, making them valuable in various applications. Flexural strength and gas permeability are essential factors in composite materials. Understanding the polymer chemistry behind cellulose derivatives is crucial for developing new applications and improving existing ones.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cellulose Derivatives Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 2114.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, China, Japan, Germany, France, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Cellulose Derivatives Market Research and Growth Report?

- CAGR of the Cellulose Derivatives industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the cellulose derivatives market growth of industry companies

We can help! Our analysts can customize this cellulose derivatives market research report to meet your requirements.

RIA -

RIA -