Europe Chocolate Market Size 2024-2028

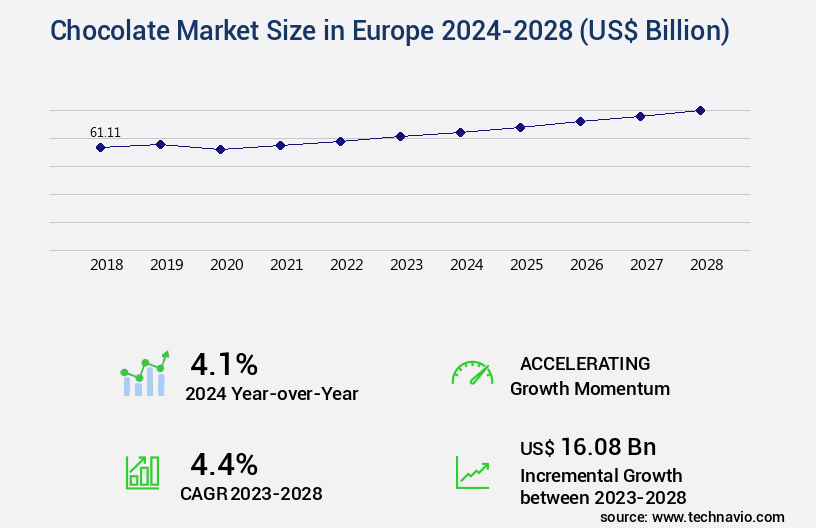

The europe chocolate market size is forecast to increase by USD 16.08 billion, at a CAGR of 4.4% between 2023 and 2028.

Major Market Trends & Insights

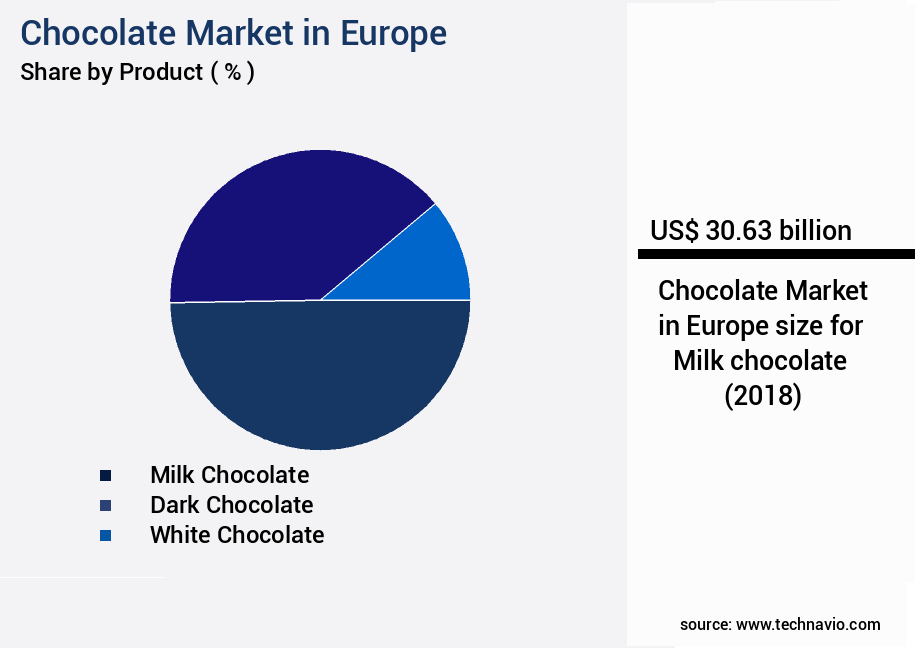

- By Product - Milk chocolate segment was valued at USD 30.63 billion in 2022

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 36.88 billion

- Market Future Opportunities: USD 16083.40 billion

- CAGR : 4.4%

Market Summary

- Europe's chocolate market witnesses significant evolution, with key trends shaping its dynamics. Dark and organic chocolate segments experience increasing preference, accounting for a substantial market share. According to market research, the European chocolate market size was valued at over €20 billion in 2020, representing a notable portion of the global chocolate industry. The advent of digitalization influences the chocolate market, with online sales gaining traction. In 2021, online chocolate sales in Europe are projected to reach approximately 10% of the total market share. However, the market faces challenges from substitute products, such as sugar-free and vegan chocolates, and occasional product recalls.

- Despite these challenges, the chocolate industry remains a thriving business landscape, driven by consumer preferences and technological advancements.

What will be the size of the Europe Chocolate Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is a significant and dynamic sector, characterized by continuous innovation and growth. According to recent estimates, the European chocolate market was valued at €25 billion in 2020, with a projected compound annual growth rate of 3% from 2021 to 2026. Consumer segmentation plays a crucial role in market expansion, with dark chocolate holding a 40% market share due to its perceived health benefits. Cocoa butter extraction and crystallization kinetics are essential process control strategies to ensure optimal chocolate texture and taste. Distribution channels are diverse, ranging from supermarkets to specialty stores and online platforms.

- Sustainability initiatives, ethical sourcing programs, and carbon footprint reduction are key priorities for chocolate manufacturers, driving innovation in encapsulation technologies and ingredient interactions. Pricing strategies, marketing campaign management, and brand positioning are critical elements of competitive differentiation. Sales promotion activities, sensory attribute profiling, and product stability testing are ongoing efforts to meet evolving consumer preferences and expectations.

How is this Europe Chocolate Market segmented?

The chocolate in europe industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

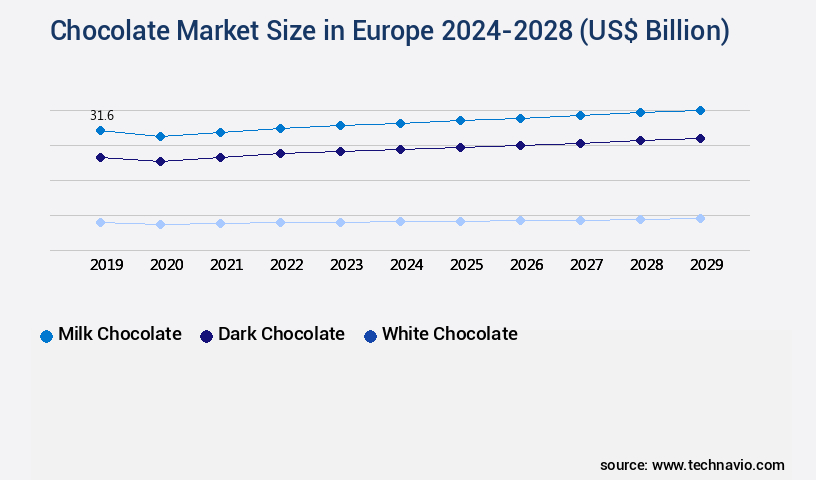

- Product

- Milk chocolate

- Dark chocolate

- White chocolate

- Distribution Channel

- Offline

- Online

- Geography

- Europe

- France

- Germany

- Italy

- UK

- Europe

By Product Insights

The milk chocolate segment is estimated to witness significant growth during the forecast period.

In the European chocolate market, milk chocolate holds a significant share, accounting for 15%-20% of cocoa solids and milk solids. Its creamier texture, derived from the dilution of cocoa solids with milk solids, sugar, and cream, makes it a preferred choice for many consumers. In 2022, milk chocolate was the most consumed chocolate type in Europe, with an estimated high growth during the forecast period. However, the increasing preference for dark chocolates, particularly in Western Europe, poses a challenge to the milk chocolate segment's growth. To maintain their market position, companies are investing in product innovation.

Food safety regulations, supply chain optimization, and tempering parameters are crucial aspects of chocolate production. Manufacturers are focusing on ingredient sourcing practices that ensure quality and sustainability. Cost reduction through manufacturing processes, energy efficiency measures, and fat bloom prevention are essential for maintaining profitability. Particle size distribution, new product development, and allergen management are other key areas of focus. Conching techniques, shear thinning behavior, product traceability systems, flavor compound analysis, and quality assurance protocols are integral to ensuring the highest standards. Cocoa bean processing, waste management strategies, chocolate viscosity measurement, chocolate mass production, and quality control systems are essential for efficient and effective production.

Sensory evaluation methods, sugar crystallization control, flow properties modeling, process automation systems, shelf life prediction, and packaging material selection are all critical components of chocolate manufacturing. Polymorphism studies, mass spectrometry analysis, product formulation design, texture profile analysis, and chromatographic separation are advanced techniques used to improve production yield and enhance product quality. Continuous innovation and adaptation to evolving consumer preferences and market trends are essential for success in the European chocolate market.

The Milk chocolate segment was valued at USD 30.63 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Enhancing Chocolate Production in Europe: Performance Improvements, Compliance, and Innovation The European chocolate market is a significant player in the global confectionery industry, with a strong focus on quality, innovation, and sustainability. One crucial aspect of chocolate production is understanding the impact of cocoa bean origin on chocolate flavor. By analyzing the chemical composition of beans from various regions, manufacturers can optimize chocolate formulations for desired taste profiles. Another essential factor is conching time, which significantly influences chocolate viscosity. By precisely controlling conching duration, manufacturers can ensure optimal texture and improve production efficiency. Innovation in chocolate production also extends to advanced techniques like measuring chocolate texture using rheometry and analyzing sugar crystal size to optimize sweetness and mouthfeel. Predictive modeling helps assess chocolate shelf life, ensuring product consistency and reducing waste. Sustainability is a critical concern, with efforts to improve chocolate production efficiency, manage cocoa bean supply chain sustainability, and reduce manufacturing costs. Food safety is another priority, with rigorous testing and certification processes to maintain high standards. Technological advancements play a significant role in chocolate production, including the use of image analysis to detect defects, X-ray diffraction (XRD) for analyzing chocolate polymorphism, and advanced tempering process control. Consumer perceptions are essential, and assessing their preferences through market research and surveys is crucial. Innovative product formulations, such as vegan or allergen-free chocolates, cater to evolving consumer demands. Lastly, manufacturers focus on maintaining chocolate quality during storage and transportation, minimizing environmental impact, and creating sustainable chocolate supply chains. These efforts not only benefit the environment but also contribute to long-term business success.

What are the key market drivers leading to the rise in the adoption of Europe Chocolate Market Industry?

- The market is propelled forward by the escalating demand for and growing popularity of premium chocolate varieties, particularly dark chocolate and organic options.

- The European chocolate market has witnessed a notable shift towards the consumption of dark chocolate in the last decade. Dark chocolate, renowned for its rich flavor and numerous health benefits, has gained considerable popularity among consumers. This preference is driven by the presence of essential nutrients like fiber, antioxidants, magnesium, and iron in dark chocolate. The flavonoids found in dark chocolate contribute significantly to cardiovascular health, enhanced blood flow, and improved cognitive functions. Furthermore, dark chocolate has a relatively minimal impact on dental health compared to other chocolate varieties, making it a healthier choice. This trend is evident in several European countries, including the UK, France, Germany, Switzerland, Belgium, the Netherlands, and Italy.

- The demand for dark chocolate has been on the rise due to its perceived health advantages and its appeal as an appropriate gifting option. Between 2010 and the present, the market for dark chocolate in Europe has experienced substantial growth. This expansion can be attributed to the increasing awareness of its health benefits and the changing consumer preferences towards healthier food choices. In comparison to milk chocolate, the market share of dark chocolate in Europe has shown a significant increase. This trend is expected to continue as consumers become more health-conscious and seek out chocolate options with added nutritional value.

- The European chocolate market's evolution underscores the dynamic nature of consumer preferences and the ongoing transformation of the food industry.

What are the market trends shaping the Europe Chocolate Market Industry?

- The increasing prevalence of online retailing represents a significant market trend moving forward. (Alternatively: Online retailing is experiencing significant growth and is becoming a prominent market trend.)

- The market has witnessed significant evolution, with e-commerce playing a pivotal role in expanding the reach of chocolate manufacturers and boosting their profits. Online and e-commerce channels facilitate both business-to-consumer (B2C) and business-to-business (B2B) transactions. The increasing average transaction value and the growing number of online transactions are key factors fueling the popularity of this sales channel. The surge in Internet users and the readiness of customers to buy online contribute to the prominence of online retailing in the European chocolate market.

- For example, the UK market is anticipated to experience substantial growth due to the increasing number of online shoppers in Europe. This trend is expected to significantly contribute to the sales of chocolate products via this channel. The market continues to unfold, with ongoing developments and shifting patterns.

What challenges does the Europe Chocolate Market Industry face during its growth?

- The industry faces significant challenges from the rising threat of substitute products and the potential for product recalls, which can impede growth.

- Europe's chocolate market has experienced fluctuating trends over the past five years. Major chocolate markets, including the UK, Germany, Russia, France, and Italy, have reported stable sales and consumption volumes. This trend is largely attributed to the growing health consciousness among consumers, leading them to prefer healthier snacking alternatives. These options include energy bars, meat snacks, peanut butter, granola bars, nuts, cereals, yogurt, sugar-free confectionery, and conventional snacks. The chocolate industry in Europe has faced additional challenges due to product recalls initiated by leading manufacturers. These recalls have negatively impacted consumer trust and influenced their purchasing decisions, contributing to the decline in per capita chocolate consumption.

- Despite these challenges, the market continues to evolve, with manufacturers focusing on innovation and product development to cater to evolving consumer preferences. For instance, there has been a surge in demand for dark chocolate, which is perceived as a healthier option due to its higher cocoa content. Additionally, the rise of veganism and other dietary trends has led to the introduction of vegan and allergen-free chocolate products. The market's dynamic nature underscores the importance of staying informed about the latest trends and consumer preferences to effectively navigate this industry.

Exclusive Customer Landscape

The chocolate market in europe forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the chocolate market in europe report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market research and growth strategies.

Customer Landscape of Europe Chocolate Market Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, chocolate market in europe forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market research report.

Alfred Ritter GmbH & Co. KG - The Belgian chocolate manufacturer produces high-quality chocolates under the brands Callebaut, Cacao Barry, and Carma, catering to the global market with a focus on sustainable cocoa sourcing and innovative product development. Their offerings prioritize taste, texture, and versatility for various applications in the food industry.

The market growth and forecasting report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alfred Ritter GmbH & Co. KG

- Barry Callebaut AG

- Blanxart Chocolate

- Chocoladefabriken Lindt & Sprüngli AG

- Chocolate Amatller

- Confiserie Leonidas SA

- Duffy's Chocolate

- Ferrero International SA

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Polo del Gusto SRL

- Valrhona Chocolate

- Whitakers Chocolates Ltd.

- Yildiz Holding AS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chocolate Market In Europe

- In January 2024, Ferrero, the Italian confectionery company, announced the launch of its new vegan chocolate brand, Kinder Schoko-Bonbon, in the United Kingdom. This expansion into plant-based chocolate aimed to cater to the growing demand for vegan and sustainable food products (Ferrero press release).

- In March 2024, Mondelēz International, a global snacking powerhouse, signed a strategic partnership with TerraCycle, a recycling solutions company. The collaboration focused on the collection and recycling of chocolate packaging in Europe, aligning with Mondelēz's commitment to reducing waste and enhancing sustainability (Mondelēz International press release).

- In May 2025, Barry Callebaut, the world's leading manufacturer of high-quality chocolate and cocoa products, acquired a 40% stake in French chocolate maker, Poulain Chocolatier. This strategic move expanded Barry Callebaut's presence in the premium chocolate market and strengthened its position in the European chocolate industry (Barry Callebaut press release).

- In the same month, the European Commission approved a new regulation to reduce the sugar content in chocolate products by 30% by 2025. This initiative aimed to improve public health and combat obesity, potentially leading to significant changes in the chocolate industry's product offerings and consumer preferences (European Commission press release).

Research Analyst Overview

- The chocolate market encompasses a dynamic and evolving industry, with a significant focus on waste management strategies, chocolate viscosity measurement, chocolate mass production, quality control systems, sensory evaluation methods, sugar crystallization control, and flow properties modeling. Chocolate manufacturers continually seek to optimize their operations to meet consumer preferences and industry growth expectations. Waste management strategies are crucial for chocolate mass production, as the industry generates substantial waste in the form of cocoa shells and chocolate scraps. Innovative approaches to waste reduction include anaerobic digestion, which converts organic waste into biogas, reducing reliance on fossil fuels. Additionally, recycling initiatives for cocoa shells have gained traction, with applications in animal feed, biofuels, and fertilizers.

- Chocolate viscosity measurement is essential for maintaining consistent product quality and ensuring efficient chocolate mass production. Advanced sensory evaluation methods, such as texture profile analysis and chromatographic separation, enable manufacturers to assess chocolate's sensory properties and identify any deviations from desired specifications. Consumer preference mapping, achieved through market research and data analysis, guides new product development and ingredient sourcing practices. Sugar crystallization control is another critical aspect of chocolate production, with flow properties modeling and conching techniques used to optimize sugar crystallization and achieve the desired texture. Process automation systems, such as temperature control and shear thinning behavior analysis, ensure consistent chocolate mass production and reduce manufacturing costs.

- Industry growth is expected to reach 3.5% annually, driven by increasing consumer demand for high-quality, sustainable chocolate products. The focus on waste management strategies, chocolate viscosity measurement, and quality control systems will continue to be essential for chocolate manufacturers to remain competitive and meet evolving consumer preferences.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chocolate Market in Europe insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.4% |

|

Market growth 2024-2028 |

USD 16.08 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.1 |

|

Key countries |

Germany, UK, France, Italy, and Rest of Europe |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Chocolate Market in Europe Research and Growth Report?

- CAGR of the Europe Chocolate Market industry during the forecast period

- Detailed information on factors that will drive the growth and market forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the chocolate market in europe growth of industry companies

We can help! Our analysts can customize this chocolate market in europe research report to meet your requirements.

RIA -

RIA -