Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market Size 2026-2030

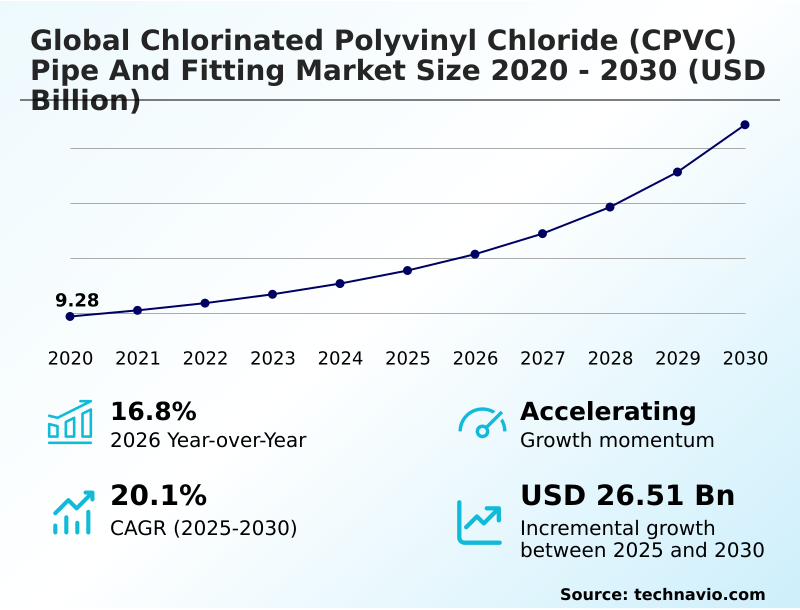

The chlorinated polyvinyl chloride (cpvc) pipe and fitting market size is valued to increase by USD 26.51 billion, at a CAGR of 20.1% from 2025 to 2030. Increasing preference for CPVC pipes over traditional metal pipes will drive the chlorinated polyvinyl chloride (cpvc) pipe and fitting market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 56% growth during the forecast period.

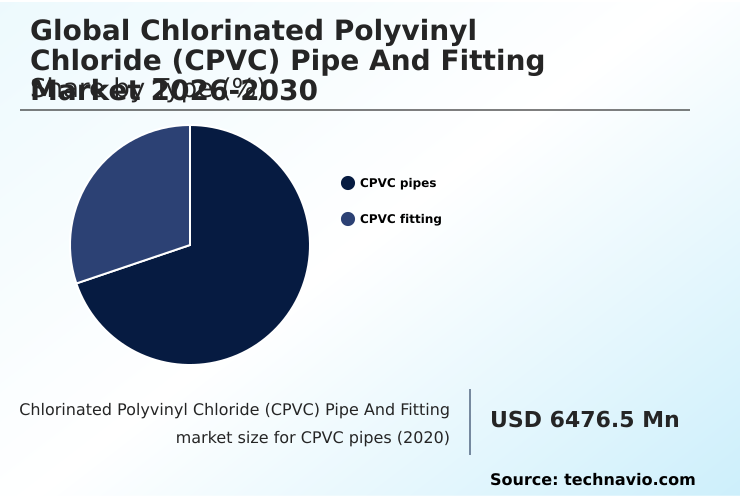

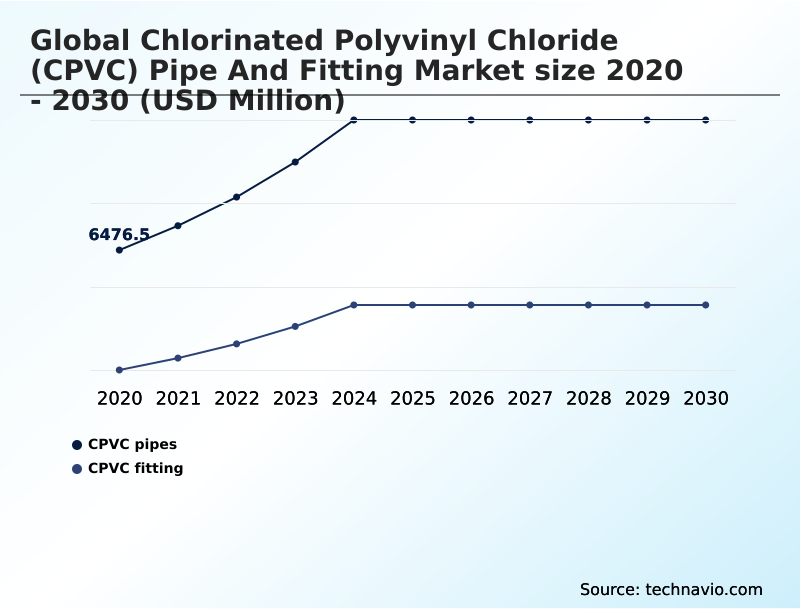

- By Type - CPVC pipes segment was valued at USD 10.46 billion in 2024

- By End-user - Industrial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 34.86 billion

- Market Future Opportunities: USD 26.51 billion

- CAGR from 2025 to 2030 : 20.1%

Market Summary

- The chlorinated polyvinyl chloride (CPVC) pipe and fitting market is characterized by steady expansion, driven by the material's inherent advantages in durability, chemical resistance, and high-temperature tolerance. These properties make it a preferred choice for a range of applications, from hot and cold-water distribution in residential and commercial buildings to critical industrial fluid handling.

- A key market driver is the ongoing replacement of traditional metal piping, which is prone to corrosion and scaling. This shift is particularly evident in renovation and retrofit projects where longevity and low maintenance are paramount. The integration of digital technologies in manufacturing is an emerging trend, with Industry 4.0 concepts being applied to enhance production precision and quality control.

- For instance, a chemical processing plant implementing CPVC piping for corrosive fluid transport can leverage its superior material properties to reduce system failures and extend maintenance cycles, thereby optimizing operational efficiency. However, the market faces challenges from the high initial cost compared to other plastics and competition from alternative materials like PEX.

- Stringent environmental and safety regulations also add complexity to manufacturing and compliance, influencing market dynamics and encouraging innovation in sustainable production practices.

What will be the Size of the Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market Segmented?

The chlorinated polyvinyl chloride (cpvc) pipe and fitting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- CPVC pipes

- CPVC fitting

- End-user

- Industrial

- Residential

- Commercial

- Application

- Hot and cold-water distribution

- Wastewater treatment

- Chemical processing

- Fire sprinkler systems

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The cpvc pipes segment is estimated to witness significant growth during the forecast period.

The market is segmented by type, with chlorinated polyvinyl chloride pipes representing the core component. These thermoplastic plumbing materials are integral to modern construction due to their suitability for both hot and cold-water distribution.

Their adoption in residential plumbing networks is driven by performance advantages over legacy systems, including a long operational lifespan and reduced maintenance requirements.

Installation via solvent cement joining ensures leak-proof connections, a critical factor in both new builds and renovation and retrofit projects.

In industrial settings, particularly for chemical processing applications, these modern piping solutions demonstrate superior resilience, with proper installations showing a 98% reduction in corrosion-related failures compared to certain metal alternatives. This durability underpins their growing preference across diverse applications.

The CPVC pipes segment was valued at USD 10.46 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

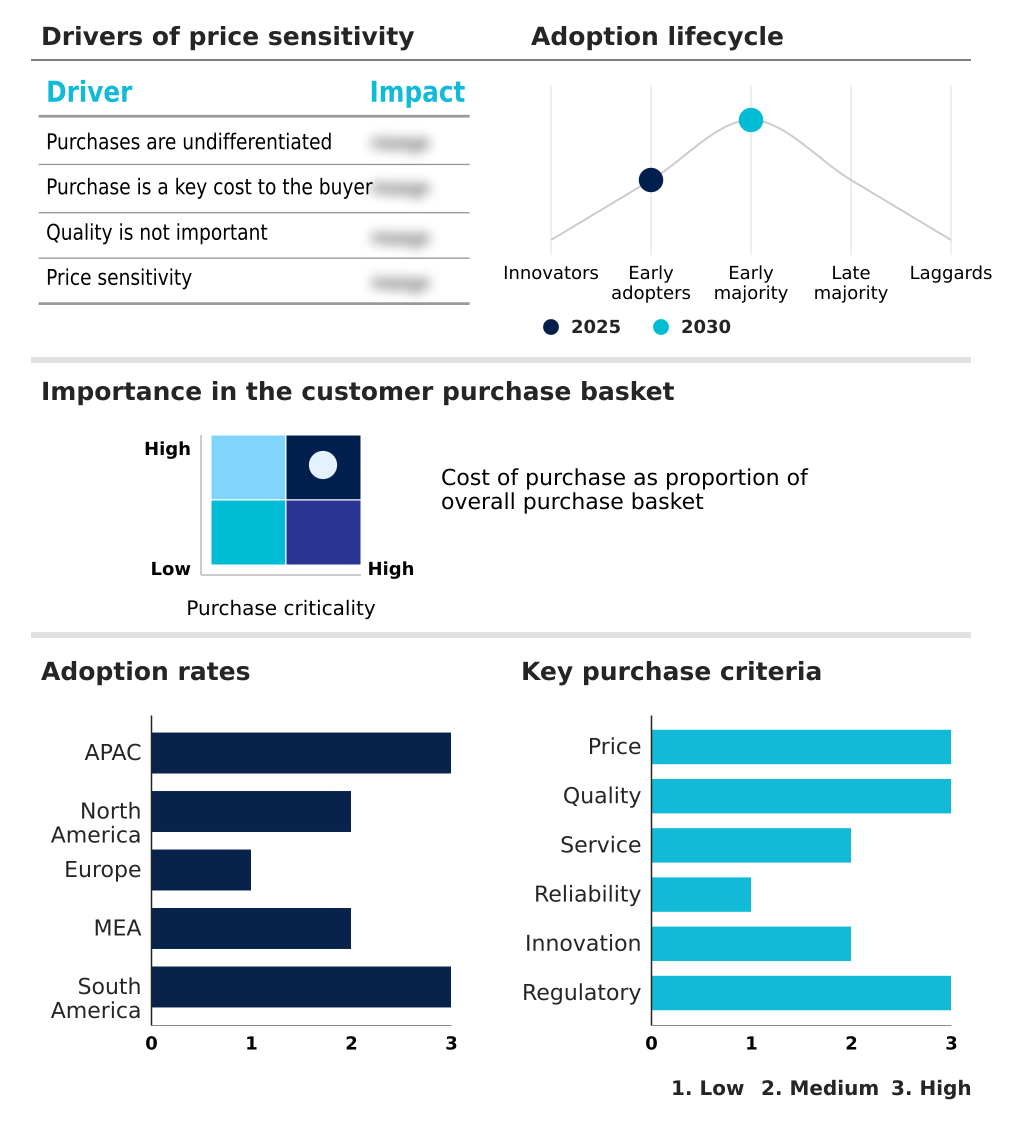

APAC is estimated to contribute 56% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market Demand is Rising in APAC Get Free Sample

The APAC region is a significant growth engine, contributing over 56% of the market's incremental growth, driven by extensive residential construction projects and industrial expansion.

Rapid urbanization fuels demand for reliable plumbing and water supply systems in new residential plumbing networks. In this region, the adoption of modern piping solutions for fire sprinkler installations and commercial building infrastructure is accelerating.

Industrial growth, especially in chemical processing applications, further boosts demand for robust industrial piping solutions. The focus on infrastructure modernization has led to large-scale aging infrastructure replacement programs, where CPVC's durability is favored.

Manufacturers are ensuring uniform wall thickness and quality to meet the diverse needs of this dynamic and expansive market.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The adoption of specialized CPVC products is accelerating across key industrial and construction sectors, highlighting the material's versatility. In demanding environments, cpvc pipes for high-temperature industrial use are becoming essential, offering reliability where standard materials fail. The chemical sector, in particular, relies on corrosion-resistant cpvc in chemical plants to ensure operational safety and prevent costly system failures.

- This application demonstrates a clear performance advantage, with such systems lasting over twice as long as certain metal alternatives under similar corrosive conditions. For residential and commercial construction, the focus on health and safety has amplified the importance of cpvc pipe and fitting for potable water, ensuring clean and safe water delivery without the risk of leaching or contamination.

- Simultaneously, building codes and insurance mandates are driving the specification of advanced cpvc for fire sprinkler systems, valued for its fire-retardant properties and ease of installation. A crucial element enabling this widespread use is the refinement of installation methods, where mastery of solvent cement techniques for cpvc fittings guarantees strong, leak-proof joints.

- As sustainability becomes a core design principle, the role of sustainable cpvc piping in green buildings is also expanding, contributing to certifications through its long service life and reduced maintenance needs.

What are the key market drivers leading to the rise in the adoption of Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Industry?

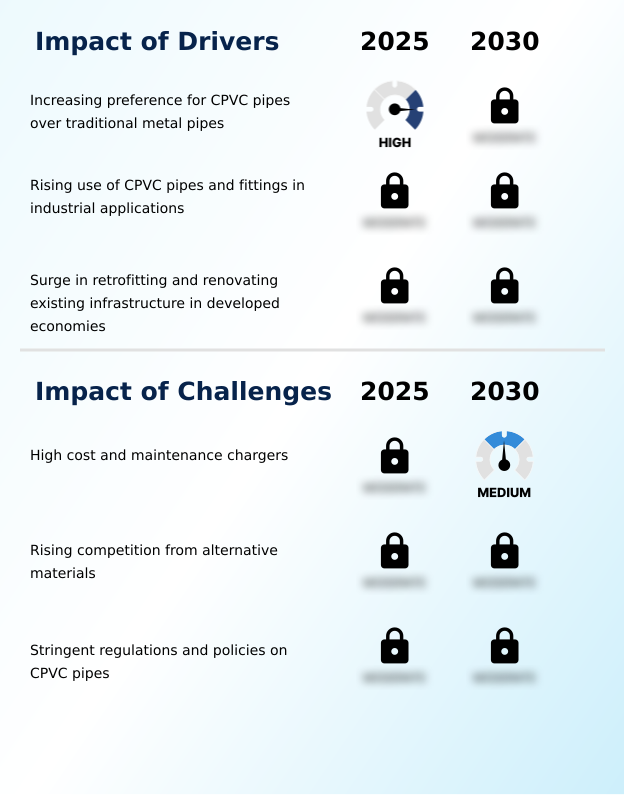

- The increasing preference for CPVC pipes over traditional metal alternatives stands as a key market driver.

- Market growth is fueled by the superior corrosion resistance and high temperature tolerance of CPVC, making it ideal for industrial fluid handling and hot water applications.

- In residential construction projects and commercial building infrastructure, CPVC provides efficient fluid handling for potable water systems, ensuring long-term reliability.

- Its adoption in industrial piping solutions leads to significant operational benefits, with some plants reporting a 40% reduction in maintenance downtime related to pipe corrosion.

- Furthermore, in building safety infrastructure, the use of CPVC for fire sprinkler systems can accelerate installation times by up to 50% compared to traditional metal systems, directly impacting project timelines and labor costs.

What are the market trends shaping the Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Industry?

- The integration of digital technologies and Industry 4.0 concepts is an emerging trend within the CPVC pipe and fitting manufacturing sector. This evolution aims to enhance production efficiency, quality control, and lifecycle management.

- Key trends center on material science innovation and sustainability. Advances in polymer formulation technology are enhancing fire resistance properties and thermal performance, expanding applications. Concurrently, the adoption of sustainable building materials is driving demand for eco-friendly plumbing solutions that align with green building standards.

- Manufacturers are leveraging advanced extrusion systems to achieve precise dimensional accuracy, which reduces material waste by up to 15%. This focus on environmentally responsible production supports water conservation efforts by ensuring system integrity.

- The market is also seeing a push towards materials with lower lifecycle environmental impact, where certain CPVC innovations contribute to a 20% improvement in energy efficiency during manufacturing compared to older methods.

What challenges does the Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Industry face during its growth?

- High initial costs and maintenance charges present a significant challenge affecting industry growth.

- The market contends with challenges related to cost perception and competition from alternative materials. Although CPVC offers long-term benefits like reduced maintenance requirements, its initial cost can be up to 25% higher than standard PVC, impacting adoption in price-sensitive projects. The pipe and fitting manufacturing process, including chlorination process enhancement, requires significant capital investment.

- Moreover, competition from materials like PEX, which can offer up to a 30% faster installation in certain residential applications, pressures manufacturers to innovate. Ensuring structural integrity retention and UV stability enhancement for applications like wastewater treatment systems or fire protection systems demands ongoing R&D, adding to operational costs and influencing the competitive positioning against other modern piping solutions.

Exclusive Technavio Analysis on Customer Landscape

The chlorinated polyvinyl chloride (cpvc) pipe and fitting market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the chlorinated polyvinyl chloride (cpvc) pipe and fitting market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, chlorinated polyvinyl chloride (cpvc) pipe and fitting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ashirvad Pipes Pvt. Ltd. - Key offerings include chlorinated polyvinyl chloride (CPVC) pipes and fittings, engineered for advanced plumbing and water supply applications in residential and commercial sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ashirvad Pipes Pvt. Ltd.

- Astral Ltd.

- Bina Plastic Industries Sdn Bhd

- Charlotte Pipe and Foundry Co.

- China Lesso Group Holdings

- Cresline Plastic Pipe Co

- Finolex Industries Ltd.

- Georg Fischer Ltd.

- IPEX Inc.

- JM Eagle Inc.

- NIBCO Inc.

- Plastic Pipe and Valve Company

- Prince Pipes and Fittings Limited

- SAM Mouldings Ltd

- Sekisui Chemical Co. Ltd.

- Skipper Ltd.

- Spears Manufacturing Co.

- The Lubrizol Corp.

- The Supreme Industries Ltd.

- Truflo Pipes

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chlorinated polyvinyl chloride (cpvc) pipe and fitting market

- In May 2025, Lubrizol Corp. reported increased adoption of CPVC compounds in industrial piping systems, citing growing demand from chemical and manufacturing sectors for high-performance solutions.

- In April 2025, Georg Fischer Ltd. highlighted increased demand for piping replacement solutions in renovation and retrofit projects across European infrastructure, reflecting the growing shift toward modern and durable piping systems.

- In March 2025, Ashirvad Pipes Pvt. Ltd. highlighted the increasing shift from metal to CPVC piping systems in residential and commercial construction due to durability and cost efficiency advantages.

- In February 2025, Lubrizol Corp. emphasized the importance of regulatory compliance and material certification in its CPVC solutions segment, reflecting the increasing complexity of meeting global safety and environmental standards.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.1% |

| Market growth 2026-2030 | USD 26506.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.8% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- From a research perspective, the market's evolution is heavily influenced by material science innovation. Advances in polymer formulation technology are critical, directly impacting high temperature tolerance and superior corrosion resistance. This is expanding the use of thermoplastic plumbing material beyond traditional residential plumbing networks into more demanding sectors like industrial fluid handling and chemical processing applications.

- The manufacturing process itself is a key battleground, where advanced extrusion systems are employed to achieve precise dimensional accuracy and uniform wall thickness, enhancing product reliability. The chlorination process enhancement continues to be a focal point for R&D, aiming to improve fire resistance properties and UV stability enhancement.

- A key boardroom consideration is how these technical advancements align with the need for reliable fire sprinkler installations and potable water systems.

- For example, firms that master the balance of performance and cost in pipe and fitting manufacturing, especially for hot and cold-water distribution, are better positioned for strategic growth, as enhanced structural integrity retention directly translates to a stronger value proposition and reduced lifecycle costs for end-users, with some systems showing a 30% longer service life.

What are the Key Data Covered in this Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market Research and Growth Report?

-

What is the expected growth of the Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market between 2026 and 2030?

-

USD 26.51 billion, at a CAGR of 20.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (CPVC pipes, and CPVC fitting), End-user (Industrial, Residential, and Commercial), Application (Hot and cold-water distribution, Wastewater treatment, Chemical processing, Fire sprinkler systems, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing preference for CPVC pipes over traditional metal pipes, High cost and maintenance chargers

-

-

Who are the major players in the Chlorinated Polyvinyl Chloride (CPVC) Pipe And Fitting Market?

-

Ashirvad Pipes Pvt. Ltd., Astral Ltd., Bina Plastic Industries Sdn Bhd, Charlotte Pipe and Foundry Co., China Lesso Group Holdings, Cresline Plastic Pipe Co, Finolex Industries Ltd., Georg Fischer Ltd., IPEX Inc., JM Eagle Inc., NIBCO Inc., Plastic Pipe and Valve Company, Prince Pipes and Fittings Limited, SAM Mouldings Ltd, Sekisui Chemical Co. Ltd., Skipper Ltd., Spears Manufacturing Co., The Lubrizol Corp., The Supreme Industries Ltd. and Truflo Pipes

-

Market Research Insights

- The market's dynamism is shaped by the push for modern piping solutions in renovation and retrofit projects, where durability is key. In aging infrastructure replacement, CPVC systems demonstrate a significant advantage, with studies showing a 70% lower incidence of leak-related failures over a 20-year period compared to some legacy materials.

- This reliability is crucial for building safety infrastructure, particularly in fire protection systems. The adoption of eco-friendly plumbing solutions is also pivotal, with green building standards influencing material selection.

- In residential construction projects, using these resource-efficient plumbing materials can contribute to a building's overall water conservation efforts, reducing potential water loss by up to 5% annually through enhanced joint integrity and corrosion resistance.

We can help! Our analysts can customize this chlorinated polyvinyl chloride (cpvc) pipe and fitting market research report to meet your requirements.

RIA -

RIA -