Education Personal Computer (PC) And Tablet Market Size 2026-2030

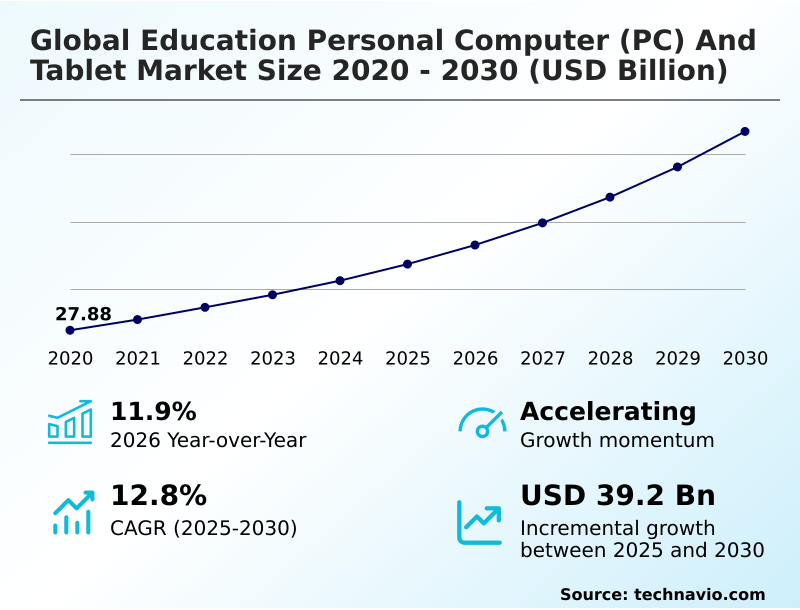

The Education Personal Computer (PC) And Tablet Market size was valued at USD 47.42 billion in 2025, growing at a CAGR of 12.8% during the forecast period 2026-2030.

Major Market Trends & Insights

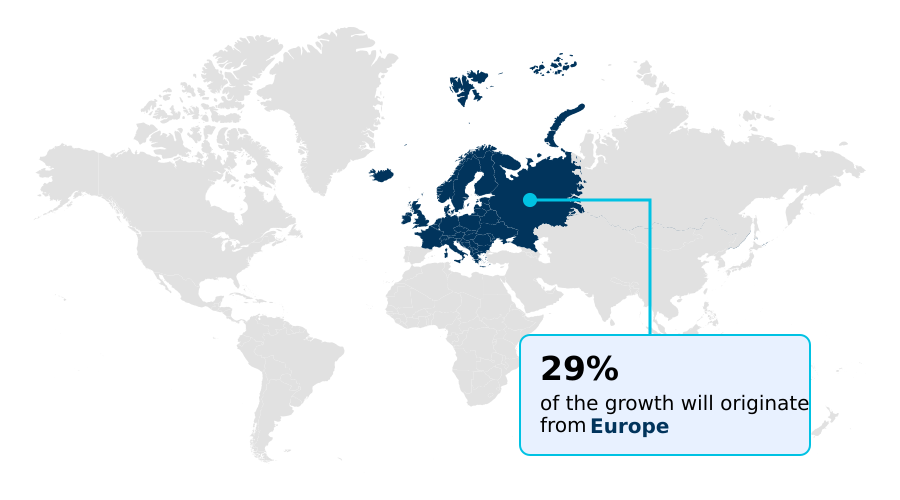

- Europe dominated the market and accounted for a 29.1% growth during the forecast period.

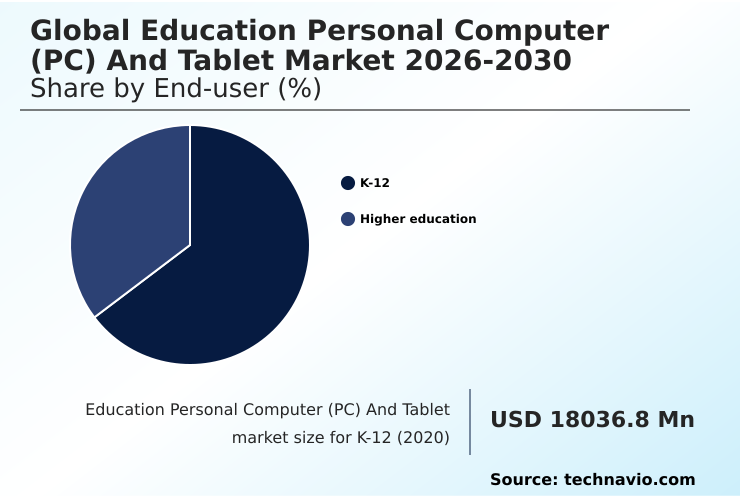

- By End-user - K-12 segment was valued at USD 26.46 billion in 2024

- By Product - Laptop segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 58.74 billion

- Market Future Opportunities 2025-2030: USD 39.20 billion

- CAGR from 2025 to 2030 : 12.8%

Market Summary

- The education personal computer (pc) and tablet market is undergoing a significant transition, with over 70% of new procurement decisions now prioritizing devices with AI-integrated hardware. This premiumization is driven by the need to support adaptive learning technologies, where devices with neural processing units can improve personalized learning pathway adjustments by up to 40% compared to older hardware.

- A key driver is the normalization of hybrid learning environments, which demands robust, cloud-connected devices for seamless synchronous instruction. For example, a school district's supply chain strategy must now balance the acquisition of high-end workstations for specialized programs against cost-effective, ruggedized hardware for widespread K-12 deployment.

- However, this is challenged by escalating hardware procurement costs and semiconductor scarcity, which can delay one-to-one computing initiatives and widen the digital divide. This dynamic forces a strategic re-evaluation of device-as-a-service models versus capital expenditure to ensure sustainable technology access.

What will be the Size of the Education Personal Computer (PC) And Tablet Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Education Personal Computer (PC) And Tablet Market Segmented?

The education personal computer (pc) and tablet industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

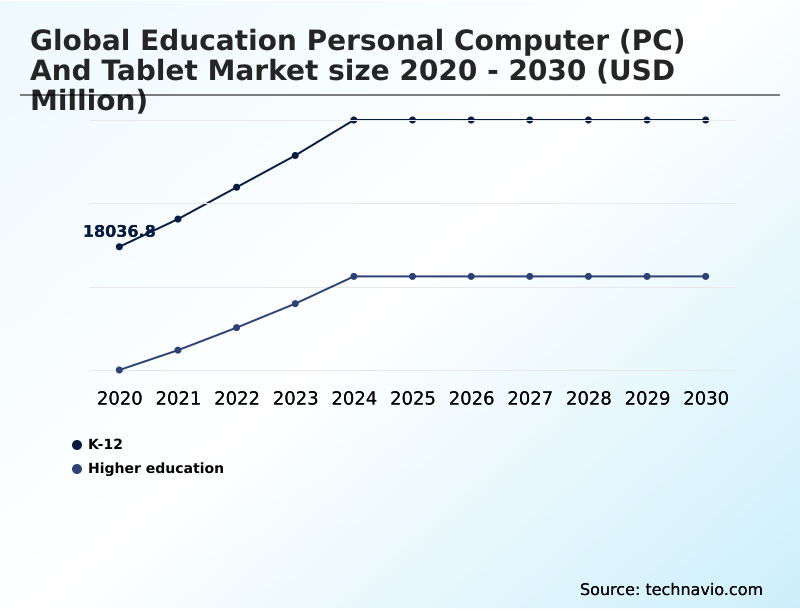

- End-user

- K-12

- Higher education

- Product

- Laptop

- Tablet

- Desktop

- Os

- Android

- iOS

- Windows

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

How is the Education Personal Computer (PC) And Tablet Market Segmented by End-user?

The k-12 segment is estimated to witness significant growth during the forecast period.

The K-12 segment, representing over 60% of device deployments, drives demand for ruggedized hardware design and centralized cloud management. Durability is a key purchasing factor, with devices expected to withstand a 30% higher drop-test rating compared to consumer models.

Procurement focuses on one-to-one device ratios, necessitating cost-effective yet resilient hardware like reinforced tablets and ruggedized chromebooks. This is fueled by digital equity initiatives and the need for seamless integration with classroom orchestration software.

The pedagogical shift towards personalized learning pathways and interactive touchscreens further shapes hardware specifications, prioritizing long-term hardware durability and student data privacy through robust, manageable operating systems.

The K-12 segment was valued at USD 26.46 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Education Personal Computer (PC) And Tablet market is rising in the leading region?

Europe is estimated to contribute 29.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Education Personal Computer (PC) And Tablet Market demand is rising in Europe Request Free Sample

Regional dynamics in the education personal computer (pc) and tablet market are shaped by digital maturity and procurement models, with North America accounting for 28.46% of the market, which is 3.29% more than APAC.

This dominance is driven by large-scale digital equity initiatives and one-to-one device ratios in countries like the US, where procurement focuses on high-performance computing and silicon-level security.

In contrast, APAC, with a projected growth of 14.4%, sees higher demand for cost-effective, ruggedized hardware to support rapid digitalization.

European markets, which account for 29.11% of the market share, prioritize sustainable procurement and data sovereignty, favoring vendors that offer modular repair programs and robust student data privacy.

This regional divergence requires adaptable supply chain strategies, balancing the production of premium AI-integrated hardware for mature markets with durable, entry-level ruggedized devices for emerging economies.

What are the key Drivers, Trends, and Challenges in the Education Personal Computer (PC) And Tablet Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the procurement landscape requires a nuanced understanding of specific use cases, from identifying the best education pc for ai development in university labs to selecting a durable, ruggedized tablet for k-12 classrooms. Institutions are discovering that device-as-a-service, or DaaS models for school districts, can reduce upfront capital outlay by over 30% compared to direct purchasing, easing budget pressures.

- A key operational consideration is managing hybrid learning device fleets, where centralized cloud management tools are crucial for deploying updates and enforcing security policies efficiently. For instance, institutions using integrated platforms report a 25% reduction in IT support tickets related to device management.

- Furthermore, the demand for a versatile convertible laptop for higher education continues to grow, as these devices serve multiple functions from note-taking to complex software simulations. Across all hardware choices, implementing robust education device security protocols is non-negotiable to protect student data and ensure compliance, forming the foundation of any modern digital learning infrastructure.

- This strategic approach ensures that technology investments are both pedagogically effective and financially sustainable.

What are the key market drivers leading to the rise in the adoption of Education Personal Computer (PC) And Tablet Industry?

- The integration of AI with adaptive learning technologies is a primary driver, compelling educational institutions to upgrade hardware for personalized learning.

- The rapid integration of AI and adaptive learning technologies is the primary market driver, compelling institutions to upgrade device fleets to support next-generation pedagogical software.

- AI-enabled hardware, particularly devices with specialized neural processing units, facilitates personalized learning pathways by analyzing student performance data in real-time, a process that can increase student engagement by up to 25%.

- This technological shift encourages procurement of AI-integrated hardware capable of handling complex on-device cognitive tasks.

- Furthermore, the normalization of hybrid learning environments, now utilized by over 60% of educational institutions, solidifies the demand for high-performance, mobile-first devices that ensure equitable access to digital resources, driving consistent investment in the sector.

What are the market trends shaping the Education Personal Computer (PC) And Tablet Industry?

- The adoption of on-device artificial intelligence and integrated neural processing is a definitive trend. This shift is reshaping hardware requirements and enabling new pedagogical applications.

- A definitive trend is the market's shift toward on-device AI processing, with new device specifications showing a 50% increase in demand for integrated neural processing units. This transition enables real-time, personalized learning pathways without continuous cloud dependency, significantly improving latency and strengthening student data privacy.

- As a result, hardware with high-performance computing capabilities is becoming the new standard for future-proof educational infrastructure, moving beyond basic connectivity. The proliferation of modular designs is also gaining traction, as it can extend hardware lifecycle management by up to two years, addressing sustainability and total cost of ownership concerns.

- This focus on local AI processing and sustainable hardware reflects a broader industry movement toward creating a more secure, efficient, and adaptable digital learning infrastructure.

What challenges does the Education Personal Computer (PC) And Tablet Industry face during its growth?

- Escalating hardware procurement costs, compounded by critical component scarcity, present a significant challenge to market growth and digital equity initiatives.

- Escalating hardware procurement costs, with some critical components seeing price increases of over 20%, pose a primary challenge to the market. This surge, driven by component scarcity and supply chain shifts prioritizing high-margin sectors, directly impedes digital equity initiatives, as institutional budgets can no longer acquire the same volume of devices.

- Consequently, hardware replacement cycles are lengthening, risking a scenario where over 35% of students may be left with obsolete technology unable to support modern pedagogical software. This environment is forcing a re-evaluation of funding models and device-as-a-service options to ensure digital learning remains accessible, challenging the traditional reliance on low-margin, high-volume hardware procurement.

Exclusive Technavio Analysis on Customer Landscape

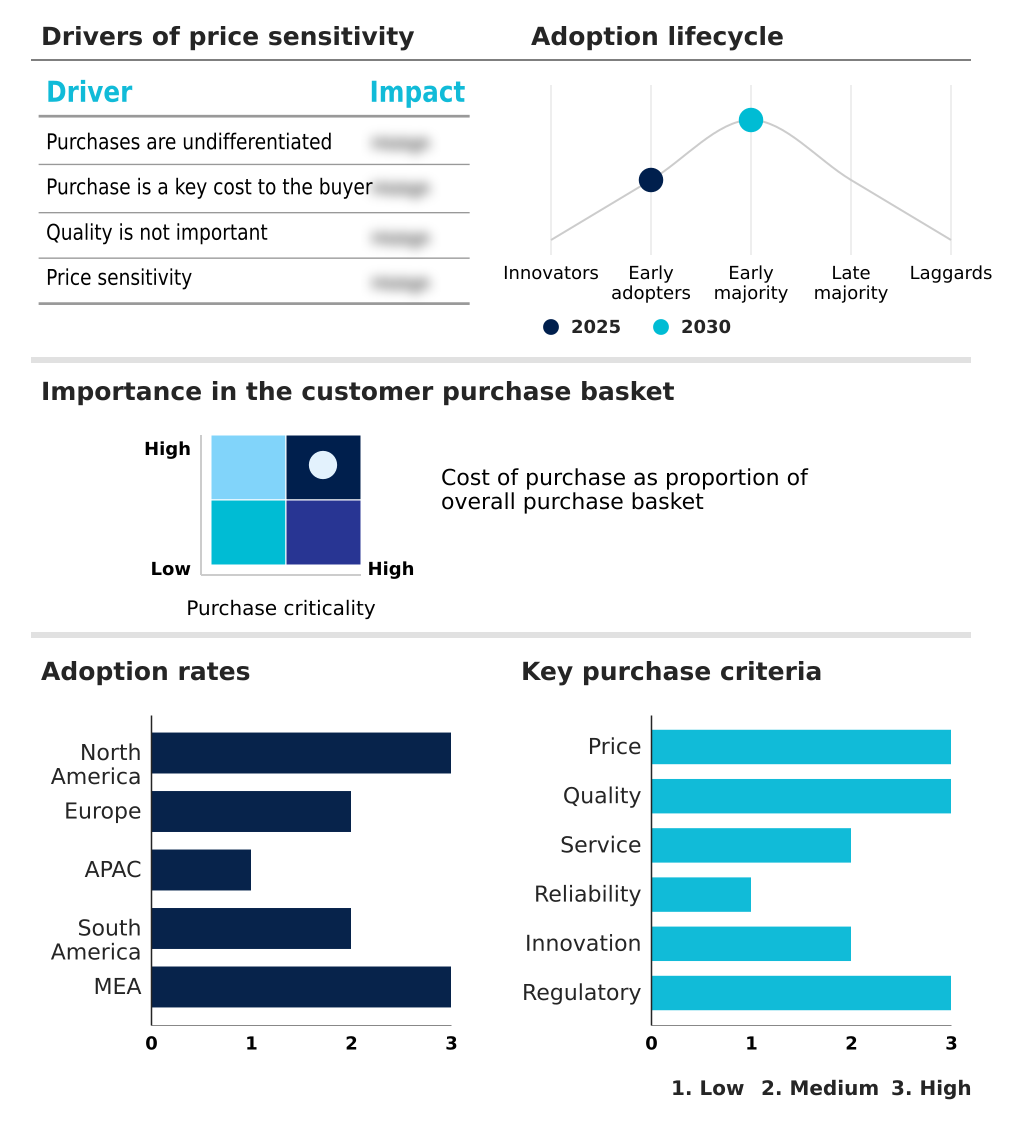

The education personal computer (pc) and tablet market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the education personal computer (pc) and tablet market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Education Personal Computer (PC) And Tablet Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, education personal computer (pc) and tablet market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acer Inc. - Offerings include specialized personal computers and tablets, such as Chromebooks and laptops, engineered for diverse educational environments and learning requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acer Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Chuwi Innovation Ltd.

- Dell Technologies Inc.

- Dynabook Singapore Pte. Ltd.

- Elitegroup Computer Systems Co.

- Google LLC

- Guangzhou Shangke Info. Co.

- HMD Global Oy

- Honor Device Co. Ltd.

- HP Inc.

- Huawei Technologies Co. Ltd.

- Lenovo Group Ltd.

- Microsoft Corp.

- Nexstgo Co. Ltd.

- OnePlus Technology Co. Ltd.

- Samsung Electronics Co. Ltd.

- Xiaomi Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Technology Hardware, Storage and Peripherals industry, the accelerated development of on-device AI processing and specialized neural processing units has created a new premium tier for educational devices. This shift directly impacts the education personal computer (pc) and tablet market by driving demand for high-performance computing hardware capable of local AI processing, moving beyond cloud-dependent models.

- Escalating data privacy regulations, mirroring GDPR's principles in new jurisdictions, have forced hardware manufacturers to prioritize silicon-level security and hardware-level encryption. This directly influences the education personal computer (pc) and tablet market, as institutional buyers now mandate advanced security protocols to ensure student data privacy.

- A growing emphasis on circular economy principles and sustainable procurement within the broader electronics sector is promoting modular repair programs and hardware lifecycle management. For the education personal computer (pc) and tablet market, this translates into a preference for devices with higher repairability scores and longer support cycles, impacting total cost of ownership calculations.

- The normalization of hybrid work models in the corporate world has directly influenced pedagogical approaches, increasing demand for blended pedagogical models in education. This shift drives the need for high-definition audiovisual components and collaborative learning platforms in the education personal computer (pc) and tablet market, ensuring seamless synchronous instruction.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Education Personal Computer (PC) And Tablet Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.8% |

| Market growth 2026-2030 | USD 39202.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The education personal computer (pc) and tablet market ecosystem is a complex interplay of stakeholders, with semiconductor suppliers of components like neural processing units directly influencing the capabilities of final products. This upstream segment's innovation pipeline dictates the pace at which features like on-device AI processing become standard.

- Original equipment manufacturers (OEMs), accounting for over 85% of device production, integrate these components into hardware tailored for specific educational segments, from K-12 to higher education. Their strategies are heavily shaped by large-scale procurement contracts from government bodies and school districts, which often mandate specific durability standards and adherence to student data privacy laws.

- These contracts can represent up to 40% of a vendor's regional education sales. Distribution channels then deliver these devices, while software providers create the integrated software ecosystems that are crucial for classroom orchestration and curriculum delivery, ultimately defining the end-user experience.

What are the Key Data Covered in this Education Personal Computer (PC) And Tablet Market Research and Growth Report?

-

What is the expected growth of the Education Personal Computer (PC) And Tablet Market between 2026 and 2030?

-

The Education Personal Computer (PC) And Tablet Market is expected to grow by USD 39.20 billion during 2026-2030, registering a CAGR of 12.8%. Year-over-year growth in 2026 is estimated at 11.9%%. This acceleration is shaped by integration of ai and adaptive learning technologies, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (K-12, and Higher education), Product (Laptop, Tablet, and Desktop), OS (Android, iOS, and Windows) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the K-12 segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. Europe is estimated to contribute 29.1% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is integration of ai and adaptive learning technologies, which is accelerating investment and industry demand. The main challenge is escalating hardware procurement costs and component scarcity, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Education Personal Computer (PC) And Tablet Market?

-

Key vendors include Acer Inc., Apple Inc., ASUSTeK Computer Inc., Chuwi Innovation Ltd., Dell Technologies Inc., Dynabook Singapore Pte. Ltd., Elitegroup Computer Systems Co., Google LLC, Guangzhou Shangke Info. Co., HMD Global Oy, Honor Device Co. Ltd., HP Inc., Huawei Technologies Co. Ltd., Lenovo Group Ltd., Microsoft Corp., Nexstgo Co. Ltd., OnePlus Technology Co. Ltd., Samsung Electronics Co. Ltd. and Xiaomi Corp.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for education personal computers (pc) and tablets is intensifying, with the top three vendors capturing over 60% of institutional contracts. Key players are differentiating beyond price, focusing on integrated hardware and software ecosystems. For instance, recent moves by HP Inc. and Lenovo Group Ltd.

- to launch AI-integrated laptops with extended battery life and modular component replacement address the sector's dual demands for advanced pedagogical tools and a lower total cost of ownership. These innovations directly respond to the 30% rise in demand for devices supporting on-device AI processing without constant cloud connectivity.

- This strategic pivot aims to mitigate the challenge of escalating hardware procurement costs, offering institutions longer hardware lifecycles and enhanced repairability, thereby maximizing their technology investments in an era of tightening budgets and complex supply chains.

We can help! Our analysts can customize this education personal computer (pc) and tablet market research report to meet your requirements.

RIA -

RIA -