US Fresh Pet Food Market Size 2026-2030

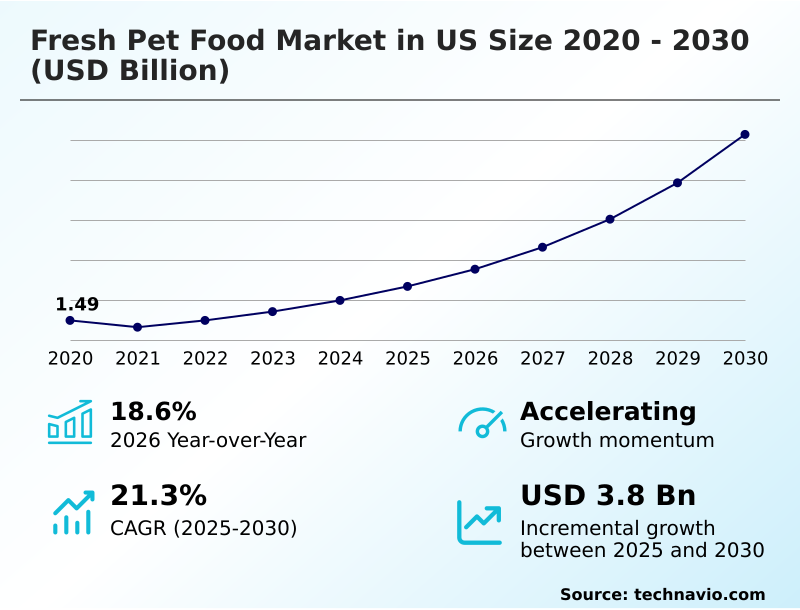

The us fresh pet food market size is valued to increase by USD 3.80 billion, at a CAGR of 21.3% from 2025 to 2030. Accelerated humanization of pets and shift toward premium nutrition will drive the us fresh pet food market.

Major Market Trends & Insights

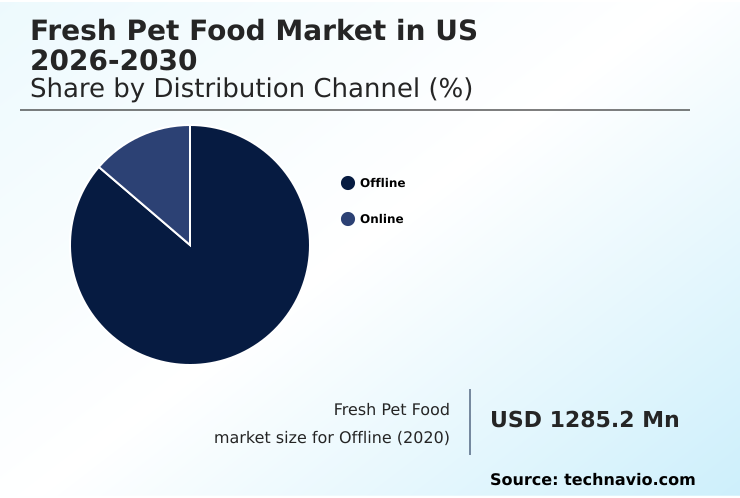

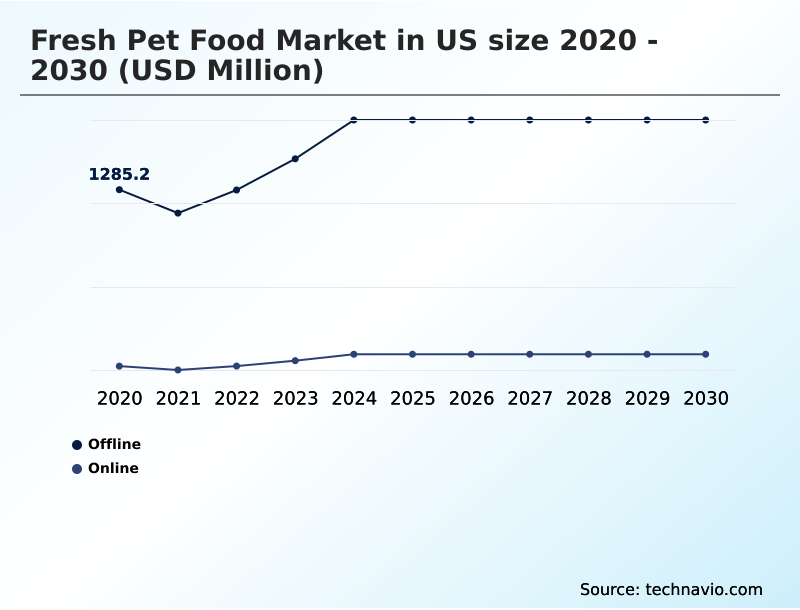

- By Distribution Channel - Offline segment was valued at USD 1.71 billion in 2024

- By Product - Dog food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.65 billion

- Market Future Opportunities: USD 3.80 billion

- CAGR from 2025 to 2030 : 21.3%

Market Summary

- The fresh pet food market in US is undergoing a significant transformation, driven by the humanization of pets and a pronounced shift toward health-conscious nutritional standards. This market moves beyond shelf-stable alternatives, focusing on human-grade ingredients and minimal processing methods to enhance nutrient bioavailability and palatability.

- Key offerings include refrigerated pet food and frozen raw diets, which demand sophisticated food safety protocols and rigorous pathogen testing to ensure consumer trust. A central business challenge involves optimizing last-mile delivery logistics to manage a short shelf life.

- For instance, companies are implementing advanced route-planning systems that integrate weather and traffic data, achieving a 15% reduction in transit times and spoilage rates for temperature-sensitive subscription-based delivery. This focus on operational excellence, combined with ingredient transparency and the development of veterinary-formulated diets, is crucial for navigating regulatory compliance and capturing share in this evolving landscape.

- The growth of direct-to-consumer models further reshapes distribution, making personalized pet nutrition more accessible while intensifying competition around customer acquisition costs and brand loyalty.

What will be the Size of the US Fresh Pet Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Fresh Pet Food Market Segmented?

The us fresh pet food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Product

- Dog food

- Cat food

- Others

- Type

- Fish

- Meat

- Vegetable

- Others

- Geography

- North America

- US

- North America

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment is a foundational component of the fresh pet food market in US, leveraging established consumer shopping habits.

This channel, encompassing specialty pet stores and supermarkets, provides a tangible touchpoint for brands, allowing for effective in-store merchandising and shopper education.

A key operational focus is on maintaining a robust cold chain from temperature-controlled warehousing to dedicated in-store refrigeration, a process where high-barrier packaging is crucial. Success hinges on strategic partnerships to secure limited refrigerated space.

This approach has proven effective, with brands achieving a 40% higher conversion rate for first-time buyers who can physically inspect the pet food traceability information on mono-material pouches.

This channel is critical for building brand trust through ingredient transparency and addressing consumer questions about everything from veterinary-formulated diets to the specifics of the direct-to-consumer model.

The Offline segment was valued at USD 1.71 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

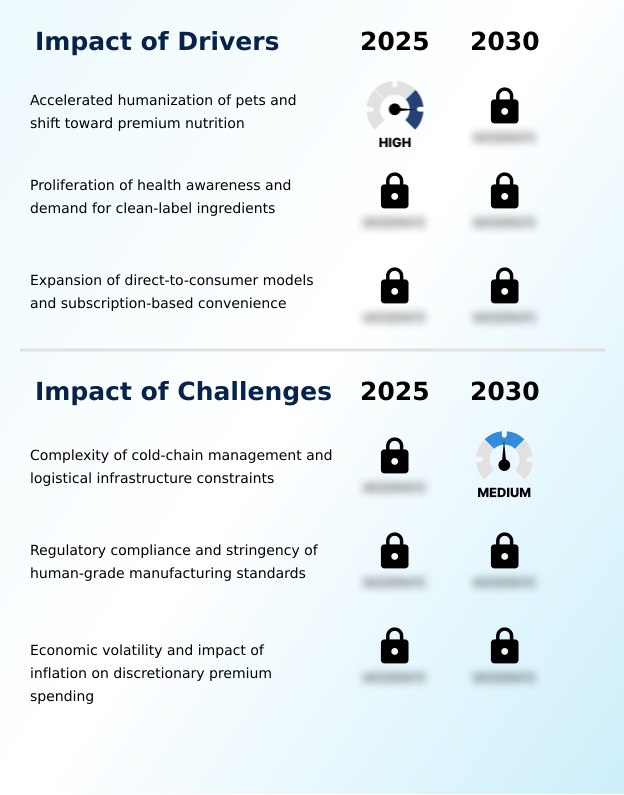

- The future trajectory of the fresh pet food market in US is intrinsically linked to the successful navigation of several strategic challenges and opportunities. The debate over raw vs fresh pet food continues, pushing brands to invest in clinical studies that validate the benefits of fresh food for dogs and cats.

- Concurrently, the growth of plant-based dog food options is creating a new competitive frontier. From an operational standpoint, perfecting cold chain management for pet food remains a primary focus, with successful firms demonstrating a 20% greater efficiency in reducing spoilage compared to competitors. This is critical for supporting the expansion of direct-to-consumer fresh pet food growth.

- Moreover, adhering to AAFCO standards for fresh pet food is non-negotiable for maintaining brand credibility. Companies are also analyzing the cost analysis of fresh pet food to make it more accessible. Looking ahead, leveraging veterinarian perspectives on fresh diets and managing food safety in raw pet meals will be key differentiators.

- The ability to improve pet gut health with diet, supported by personalized nutrition for senior dogs, represents a significant value-add that can justify premium pricing and foster long-term customer loyalty.

What are the key market drivers leading to the rise in the adoption of US Fresh Pet Food Industry?

- The accelerated humanization of pets and a corresponding shift toward premium nutrition are the primary drivers of market growth.

- The primary driver remains the deep-rooted pet humanization trend, which has expanded the definition of premium pet nutrition.

- This has fueled demand for clean-label pet food and ingredient transparency, with over 60% of new consumers citing these as their top purchasing criteria.

- The proliferation of direct-to-consumer models has been instrumental, reducing barriers to entry; companies utilizing this model report a 35% faster path to market compared to traditional retail. The convenience of subscription-based delivery and portion-controlled meals resonates with modern lifestyles.

- Furthermore, the focus on preventive pet healthcare has led to wider acceptance of veterinary-recommended diets that incorporate omega-3 fatty acids and other beneficial supplements, solidifying the market's science-backed value proposition.

What are the market trends shaping the US Fresh Pet Food Industry?

- A key market trend is the integration of advanced personalization, which uses algorithm-driven nutritional optimization. This creates bespoke dietary profiles based on individual pet data.

- Emerging trends are centered on technological integration and sustainability. The use of bio-individual optimization for metabolic precision diets has led to a 25% improvement in targeted health outcomes for pets with chronic conditions. Concurrently, the push for eco-friendly packaging has resulted in the adoption of mono-material pouches, reducing plastic waste by over 40% for leading brands.

- This focus on sustainability extends to regenerative agriculture sourcing for ingredients. An omnichannel retail strategy is also becoming standard, with brands that combine online subscriptions and in-store sales seeing a 15% higher customer lifetime value. This hybrid approach, supported by advanced pet food traceability systems, is reshaping market access and consumer engagement, making functional ingredients and high-pressure processing more mainstream.

What challenges does the US Fresh Pet Food Industry face during its growth?

- The complexity of cold-chain management, coupled with logistical infrastructure constraints, presents a key challenge to industry expansion and operational efficiency.

- Operational hurdles and regulatory pressures present significant challenges. The logistical intricacies of cold-chain logistics and last-mile delivery logistics result in operational costs that are up to 50% higher than those for shelf-stable alternatives. This directly impacts price elasticity and tests consumer purchasing power.

- Furthermore, navigating AAFCO nutritional guidelines and securing certification for a human-grade facility requires substantial investment and stringent food safety protocols, including constant pathogen testing. The short shelf life of products introduces a high risk of inventory loss, with some producers reporting spoilage rates of up to 8% if the supply chain is disrupted.

- These factors, combined with ingredient cost volatility, demand exceptional operational discipline and create high barriers for new entrants.

Exclusive Technavio Analysis on Customer Landscape

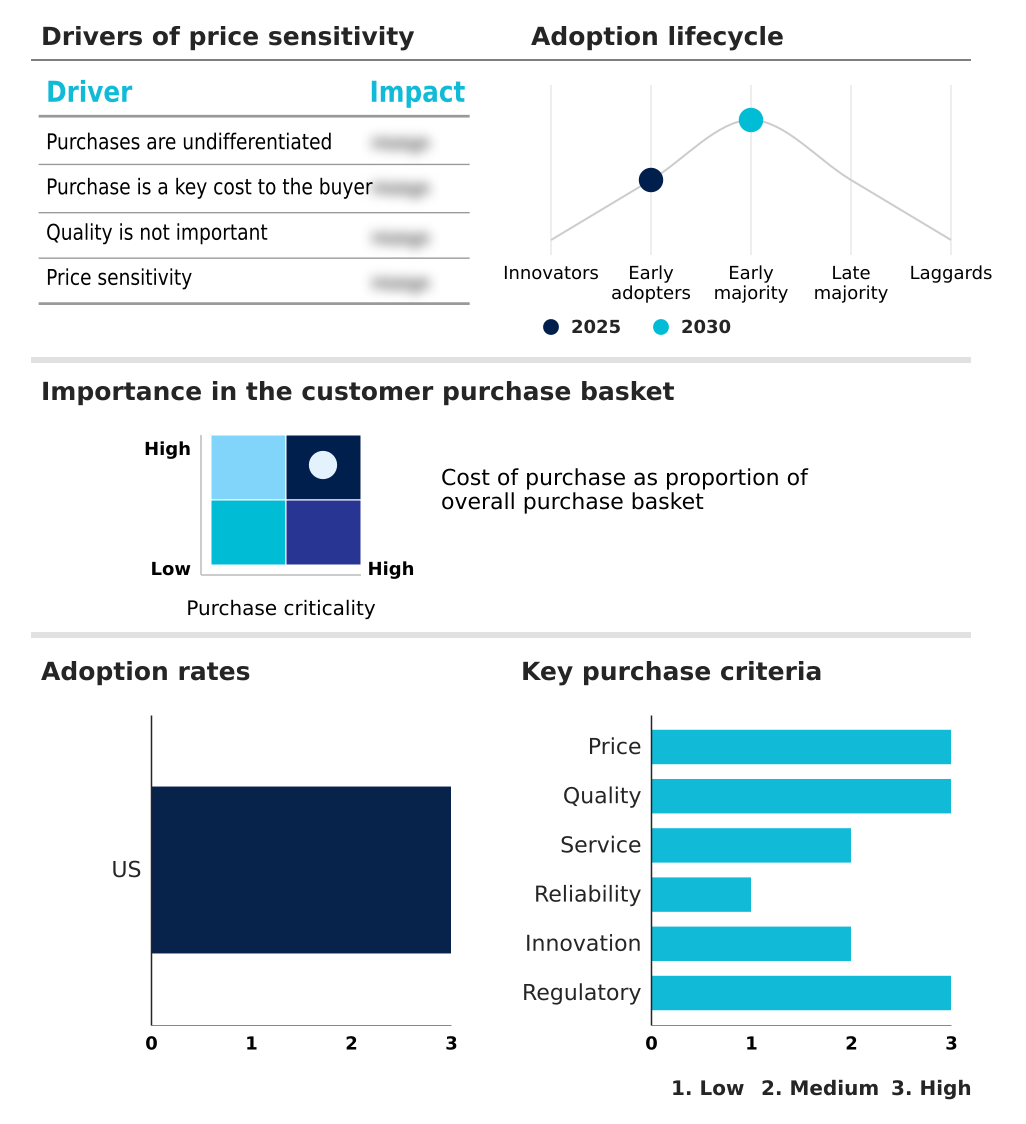

The us fresh pet food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us fresh pet food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Fresh Pet Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us fresh pet food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A Joyful Dog - Delivers human-grade pet food formulated for optimal nutritional value, utilizing advanced sous-vide gentle cooking methods to preserve ingredient integrity and enhance bioavailability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A Joyful Dog

- A Pup Above

- Artemis Pet Food Co.

- Bramble

- Carnivore Meat Co. LLC

- Chewy Inc

- Cooking4Canines

- Darwins Natural Pet Products

- Freshpet Inc.

- Hills Pet Nutrition Inc.

- JustFoodForDogs LLC

- My Perfect Pet Food Inc.

- Nestle Purina PetCare Co.

- NomNomNow Inc.

- Primal Pet Foods Inc.

- Raised Right Pets LP

- Stella and Chewys LLC

- Steves Real Food

- The Farmers Dog Inc.

- Vital Essentials

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us fresh pet food market

- In September 2024, a leading direct-to-consumer brand announced a strategic partnership with a national veterinary clinic network to offer its veterinary-formulated diets, aiming to increase medical endorsements.

- In November 2024, a major pet food corporation completed the acquisition of a startup specializing in AI-driven personalized pet nutrition, integrating its algorithm into their subscription-based delivery service.

- In January 2025, an innovative packaging supplier launched a new line of fully compostable, high-barrier packaging for refrigerated pet food, addressing industry-wide sustainability goals.

- In March 2025, The Farmers Dog Inc. announced an additional investment of $10 million specifically dedicated to long-term veterinary research and clinical trials, aiming to provide peer-reviewed evidence regarding the health benefits of fresh diets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Fresh Pet Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 181 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.3% |

| Market growth 2026-2030 | USD 3803.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.6% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The fresh pet food market in US is advancing beyond niche status, driven by a convergence of consumer demand and technological capability. Boardroom decisions are increasingly centered on bio-individual optimization, where metabolic precision diets are formulated using gut microbiome analysis. The adoption of high-pressure processing allows for enhanced safety without compromising the nutritional value of functional ingredients, a key differentiator.

- The complexity of the supply chain, from regenerative agriculture sourcing to temperature-controlled warehousing, requires significant capital investment. Companies are mitigating this by using advanced pet food traceability systems, which have been shown to speed up recall responses by over 50%.

- This focus on safety and quality, combined with the development of personalized pet nutrition using data-driven meal planning, underpins the market's premium positioning. As brands expand, the ability to scale a certified human-grade facility while managing the intricacies of obligate carnivore nutrition and probiotic supplementation will determine long-term market leadership.

What are the Key Data Covered in this US Fresh Pet Food Market Research and Growth Report?

-

What is the expected growth of the US Fresh Pet Food Market between 2026 and 2030?

-

USD 3.80 billion, at a CAGR of 21.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Dog food, Cat food, and Others), Type (Fish, Meat, Vegetable, and Others) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Accelerated humanization of pets and shift toward premium nutrition, Complexity of cold-chain management and logistical infrastructure constraints

-

-

Who are the major players in the US Fresh Pet Food Market?

-

A Joyful Dog, A Pup Above, Artemis Pet Food Co., Bramble, Carnivore Meat Co. LLC, Chewy Inc, Cooking4Canines, Darwins Natural Pet Products, Freshpet Inc., Hills Pet Nutrition Inc., JustFoodForDogs LLC, My Perfect Pet Food Inc., Nestle Purina PetCare Co., NomNomNow Inc., Primal Pet Foods Inc., Raised Right Pets LP, Stella and Chewys LLC, Steves Real Food, The Farmers Dog Inc. and Vital Essentials

-

Market Research Insights

- Market dynamics are defined by the convergence of consumer demand for premium pet nutrition and technological advancements in distribution. The shift toward data-driven meal planning is significant, with platforms leveraging personalization showing a 30% higher customer retention rate compared to generic offerings.

- This pet humanization trend has expanded market penetration, particularly as brands master e-commerce fulfillment and reduce customer acquisition costs through targeted digital campaigns. The adoption of omnichannel retail strategies, which blend brick-and-mortar visibility with online convenience, has increased access in suburban markets by over 20%.

- As a result, price elasticity is being tested, and companies are focused on building brand loyalty to offset ingredient cost volatility and maintain stable consumer purchasing power.

We can help! Our analysts can customize this us fresh pet food market research report to meet your requirements.

RIA -

RIA -