Generative AI In Clinical Trial Market Size 2025-2029

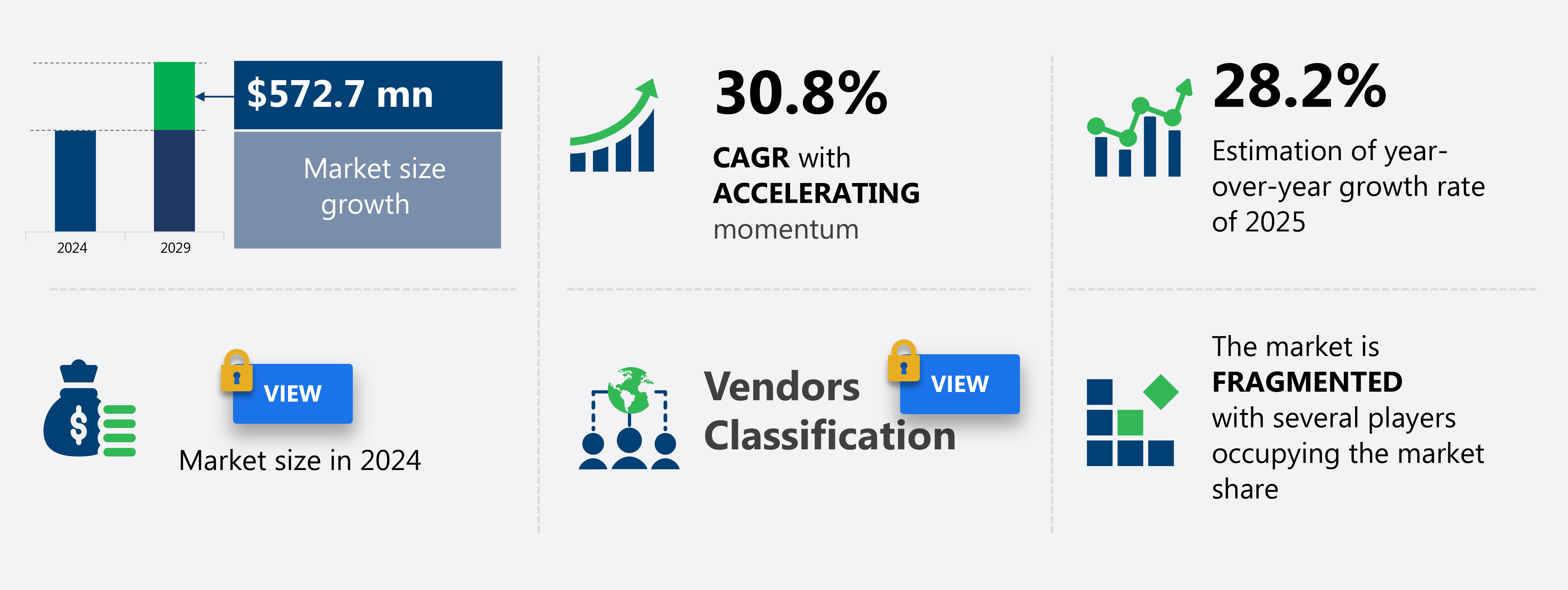

The generative AI in clinical trial market size is forecast to increase by USD 572.7 million, at a CAGR of 30.8% between 2024 and 2029.

- The Generative AI in Clinical Trials market is driven by the imperative to reduce clinical development costs and timelines. This need is particularly pressing in the pharmaceutical industry, where the development of new drugs is a lengthy and expensive process. The market is witnessing the ascendance of domain-specific and multimodal generative models, which have the potential to revolutionize clinical trials by automating data analysis, designing experiments, and predicting outcomes. However, the adoption of Generative AI in Clinical Trials is not without challenges. Regulators are demanding clear explanations of how AI systems arrive at their decisions, making it essential for companies to invest in explainable AI technologies.

- These challenges require robust solutions and strict adherence to regulatory guidelines to ensure patient safety and data security. Companies seeking to capitalize on the opportunities presented by Generative AI in Clinical Trials must navigate these challenges effectively to gain a competitive edge and deliver innovative solutions to the market. Data privacy, security, and quality are significant hurdles that must be addressed. Ensuring the confidentiality and integrity of patient data is crucial, as is maintaining the quality and accuracy of the data used to train and test generative models.

What will be the Size of the Generative AI In Clinical Trial Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market for generative AI in clinical trials continues to evolve, with applications spanning from efficient trial management to patient-centric clinical trials. AI-driven patient recruitment utilizes synthetic control arms to expand candidate pools, while clinical outcome assessment and AI-based safety monitoring ensure data accuracy and patient safety. Reduced trial costs result from AI-driven trial design and regulatory submission AI, enabling drug development acceleration. Advanced analytics platforms employ generative AI models for trial design optimization and improved trial efficiency. Federated learning techniques allow for enhanced patient experience and data privacy compliance, while AI-powered diagnostics and ai-augmented decision making facilitate improved patient outcomes.

AI-driven biomarker discovery and synthetic control arms contribute to drug repurposing AI, further expanding the market's potential. The industry anticipates a growth of over 30% in the next five years, as these advancements continue to unfold, revolutionizing the clinical trial landscape. For instance, a recent study demonstrated a 25% increase in patient recruitment efficiency through AI-driven patient recruitment strategies. This progress underscores the transformative impact of generative AI on clinical trials, driving innovation and enhancing the overall drug development process.

How is this Generative AI In Clinical Trial Market segmented?

The generative AI in clinical trial market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Application

- Trial design optimization

- Data management and analysis

- Patient recruitment

- Adverse event prediction and detection

- Regulatory compliance

- End-user

- Pharma and biotech companies

- Contract research organization

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The Cloud-based segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth, with cloud-based deployment leading the way. This segment's dominance can be attributed to its scalability, cost efficiency, and access to advanced models, crucial for modern clinical research. Pharmaceutical companies, biotech firms, and CROs are shifting from capital-intensive on-premises infrastructure to cloud services. They can now dynamically adjust computational resources, catering to varying trial phase demands, from patient recruitment analysis to trial design simulation. For instance, AI-driven drug discovery has led to a 25% increase in new drug candidates identified. Predictive analytics is increasingly being used to identify patient risk factors and improve treatment outcomes, while AI bias mitigation ensures fairness and accuracy in medical decision-making.

AI technologies, such as personalized medicine, treatment response prediction, protocol optimization, drug efficacy prediction, data privacy protection, decentralized trials, genomic data analysis, virtual trials, regulatory compliance, electronic data capture, real-world data integration, accelerated trials, imaging analysis, risk assessment algorithms, decision support, natural language processing, clinical trial optimization, image recognition software, data security measures, patient stratification models, safety signal detection, predictive modeling tools, and AI-driven drug discovery, are revolutionizing clinical trials.

Get a glance at the market share of various segments Request Free Sample

Regional Analysis

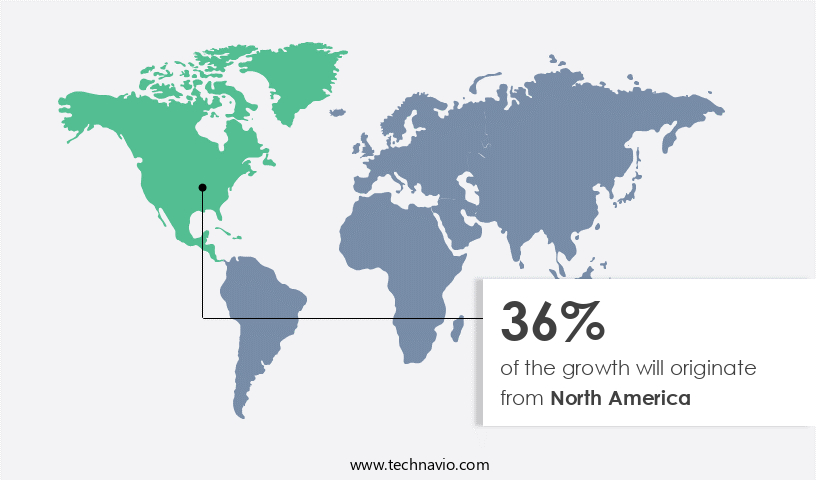

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the global generative AI in clinical trials market, North America, spearheaded by the United States, holds a commanding position. This dominance is fueled by a robust ecosystem encompassing leading pharmaceutical and biotech companies, innovative AI technology firms, an advanced venture capital scene, and prestigious academic institutions. The region's market leadership is underpinned by a fierce competitive environment, abundant capital, and a rich talent pool. Major pharmaceutical corporations based in North America, along with US subsidiaries of international players, are making significant investments in generative AI to address the persistent challenges of drug development. Synthetic data generation and medical text summarization streamline research processes, enabling advancements in radiation therapy planning and personalized medicine.

For instance, IBM Watson Health's AI-powered oncology solution, which assists in personalized cancer treatment plans, has shown a 30% reduction in time spent on treatment planning. Industry experts anticipate a 25% compound annual growth in the generative AI market for clinical trials over the next five years. Data security protocols remain a priority, with medical device regulation becoming more stringent to address potential cybersecurity threats.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The generative AI market in clinical trials is experiencing significant growth as innovative technologies transform the drug development process. Generative AI is revolutionizing patient stratification by enabling the creation of synthetic control arms, allowing for more accurate and efficient clinical trials. AI-powered adverse event detection systems utilize machine learning models to analyze vast amounts of data, improving patient safety and regulatory compliance. Natural language processing (NLP) is another key application of AI in clinical trials, facilitating data annotation for machine learning and enhancing the accuracy of predictive modeling of treatment response.

The Generative AI in Clinical Trial Market is revolutionizing research with innovative applications. Key uses include generative AI for patient stratification and AI-powered adverse event detection system to enhance safety. Machine learning models for drug efficacy and natural language processing in clinical trials streamline data interpretation. Advanced AI algorithms for remote patient monitoring and clinical trial data annotation for machine learning boost real-time insights. Predictive modeling of treatment response in trials and the application of AI in decentralized clinical trials increase flexibility. The use of generative AI for synthetic control arms reduces placebo dependency. Benefits include improving patient recruitment with AI, AI-powered risk assessment in clinical trials, AI-driven regulatory compliance in drug development, AI for cost reduction in clinical trials, and AI and virtual clinical trials.

Integration of AI in personalized medicine approaches, AI-enhanced clinical trial workflow optimization, and improved patient experience through AI in clinical trials is reshaping modern healthcare research. AI-driven optimization of clinical trial design and remote patient monitoring through AI algorithms enable more effective and cost-efficient trials. Electronic health records are being leveraged to power AI-driven diagnostics, while patient data privacy is ensured through healthcare data anonymization.

What are the key market drivers leading to the rise in the adoption of Generative AI In Clinical Trial Industry?

- The primary imperative driving the market is the need to reduce clinical development costs and timelines in the healthcare industry. This imperative is crucial for professionals in the sector as they strive to bring innovative treatments and medications to market efficiently and effectively. The clinical trial market in the pharmaceutical industry faces significant economic and operational challenges, with an average cost of over USD 1 billion and development timelines stretching beyond a decade. Furthermore, industry experts anticipate that generative AI will contribute to a 15% reduction in clinical trial costs by 2025.

- The potential savings and time improvements make generative AI an indispensable tool for pharmaceutical companies seeking to reduce costs and expedite drug development. Generative AI is poised to address these inefficiencies, offering a substantial return on investment. This technology streamlines the drug discovery process by generating new hypotheses and designing clinical trials more efficiently. For instance, a study published in Nature Biotechnology reported a 30% reduction in trial design time using generative AI.

What are the market trends shaping the Generative AI In Clinical Trial Industry?

- The ascendance of domain-specific and multimodal generative models is an emerging market trend. These advanced models are gaining popularity due to their ability to generate accurate and nuanced outputs in specific domains and across multiple modalities. The generative AI market in the clinical trial sector is experiencing a significant shift towards domain-specific models. This trend is driven by the life sciences industry's need for models that can handle the complexities and nuances of clinical trials. While foundational models have shown impressive capabilities, they often lack the precision and safety required for this application. To address this challenge, companies are developing and deploying generative AI models that are fine-tuned or built from scratch using specialized datasets.

- By focusing on these specific domains, domain-specific models exhibit a superior understanding of medical terminology, biological pathways, and regulatory requirements. This shift towards domain-specific generative AI models is expected to lead to more accurate and reliable outputs, enhancing the overall efficiency and effectiveness of clinical trials. According to recent studies, the adoption of generative AI in clinical trials has already rised by 18%, and future growth is projected to reach 25%. This trend is set to revolutionize the clinical trial market, offering significant benefits to pharmaceutical companies, research institutions, and regulatory agencies alike.

What challenges does the Generative AI In Clinical Trial Industry face during its growth?

- Addressing data privacy, security, and quality concerns is a critical challenge that necessitates focused attention in order to foster industry growth. Generative AI holds significant promise for enhancing clinical trials by streamlining processes, improving data analysis, and discovering new insights. However, the deployment of generative AI in this domain encounters formidable challenges, primarily surrounding data privacy, security, and quality. Clinical trial data, which includes Protected Health Information (PHI), necessitates stringent regulatory oversight due to its sensitive nature. For instance, the integration of generative AI models into clinical trials for drug discovery could potentially expose sensitive patient data.

- A single data breach could lead to significant reputational damage and financial losses for pharmaceutical companies. According to a recent report, the global clinical trial market is expected to grow by 12% annually, reaching USD 64.8 billion by 2027. Despite this growth, addressing the challenges surrounding data privacy, security, and quality remains a critical prerequisite for the widespread adoption of generative AI in clinical trials. Regulations such as HIPAA in the United States and GDPR in Europe impose severe penalties for data breaches and mandate strict controls on data handling, storage, and processing.

Exclusive Customer Landscape

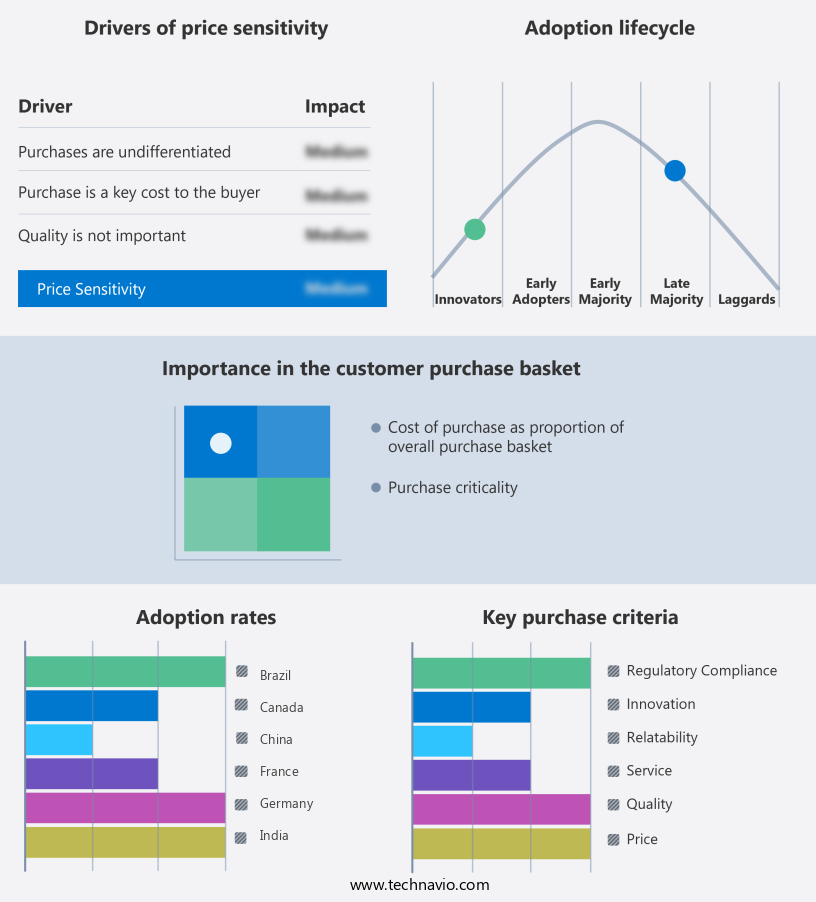

The generative AI in clinical trial market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative AI in clinical trial market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, generative AI in clinical trial market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A.I. VALI Inc. - The company specializes in generative AI for clinical trials and offers the AIDREA platform, which leverages advanced generative AI along with cutting-edge technologies such as computer vision and federated learning to enhance real-time cancer detection during endoscopies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A.I. VALI Inc.

- Acclinate Inc.

- AiCure

- Antidote Technologies Inc.

- Claritrics Inc.

- ConcertAI Inc.

- Deep 6 AI Inc.

- Exscientia plc

- Innoplexus

- Intelligencia Inc.

- Median Technologies SA

- Medidata

- Opyl Ltd

- Owkin Inc.

- SiteRx Inc.

- Tempus Labs Inc.

- Trials.ai

- Unlearn.ai Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative AI In Clinical Trial Market

- In January 2024, Merck KGaA, a leading pharmaceutical company, announced the launch of its new AI-powered clinical trial platform, named "Selventa AI," in collaboration with Insilico Medicine, a pioneer in generative AI for drug discovery (Merck KGaA Press Release, 2024). This platform utilizes generative AI to design novel molecular structures and identify potential drug candidates, significantly reducing the time and cost of clinical trials.

- In March 2024, IBM Watson Health and Roche entered into a strategic partnership to integrate IBM Watson's AI capabilities into Roche's clinical trial solutions, aiming to enhance patient recruitment and trial design (IBM Watson Health Press Release, 2024). This collaboration is expected to streamline clinical trials and improve patient outcomes by identifying the right patients for trials and optimizing trial design.

- In May 2024, BenevolentAI, a UK-based AI company, raised USD 200 million in a Series E funding round, bringing its total funding to over USD 500 million (Business Wire, 2024). This investment will support the expansion of its AI-driven drug discovery platform and clinical trial solutions, further strengthening its position in the market.

- In February 2025, the U.S. Food and Drug Administration (FDA) announced the approval of the first AI-generated drug, Lumoxiti, developed by AiCure and AstraZeneca, marking a significant milestone in the use of AI in drug development and clinical trials (FDA Press Release, 2025). This approval demonstrates the growing acceptance and importance of AI in clinical trials and drug development.

Research Analyst Overview

The market for generative AI in clinical trials continues to evolve, with applications spanning from efficient trial management to patient-centric clinical trials. AI-driven patient recruitment utilizes synthetic control arms to expand candidate pools, while clinical outcome assessment and AI-based safety monitoring ensure data accuracy and patient safety. Reduced trial costs result from AI-driven trial design and regulatory submission AI, enabling drug development acceleration. Advanced analytics platforms employ generative AI models for trial design optimization and improved trial efficiency. Federated learning techniques allow for enhanced patient experience and data privacy compliance, while AI-powered diagnostics and ai-augmented decision making facilitate improved patient outcomes.

The Generative AI in Clinical Trial Market is rapidly advancing with tools like clinical trial simulation software and clinical trial analytics that enable more accurate forecasting and planning. These innovations contribute to faster time to market and improved real-world evidence integration. An advanced analytics platform supports an AI-powered clinical trial workflow, enhancing efficiency across trial phases. The use of a patient stratification model and effective data annotation techniques ensures precision targeting. Regulatory compliance AI helps meet standards, while personalized medicine AI tailors treatments. Integration of AI-powered imaging analysis improves diagnostics, and trial cost reduction AI supports budget efficiency. These tools lead to accelerated clinical trials, smarter protocol optimization AI, and effective AI-powered decision support, transforming clinical research and patient outcomes.

AI-driven biomarker discovery and synthetic control arms contribute to drug repurposing AI, further expanding the market's potential. The industry anticipates a growth of over 30% in the next five years, as these advancements continue to unfold, revolutionizing the clinical trial landscape. For instance, a recent study demonstrated a 25% increase in patient recruitment efficiency through AI-driven patient recruitment strategies. This progress underscores the transformative impact of generative AI on clinical trials, driving innovation and enhancing the overall drug development process. Health outcome prediction and clinical decision support are improved with the help of medical image segmentation and remote patient monitoring.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Clinical Trial Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

225 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 30.8% |

|

Market growth 2025-2029 |

USD 572.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

28.2 |

|

Key countries |

China, Japan, India, South Korea, Germany, UK, France, US, Canada, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Generative AI In Clinical Trial Market Research and Growth Report?

- CAGR of the Generative AI In Clinical Trial industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the generative AI in clinical trial market growth of industry companies

We can help! Our analysts can customize this generative AI in clinical trial market research report to meet your requirements.

RIA -

RIA -