High-performance Computing (HPC) For AI Market Size 2026-2030

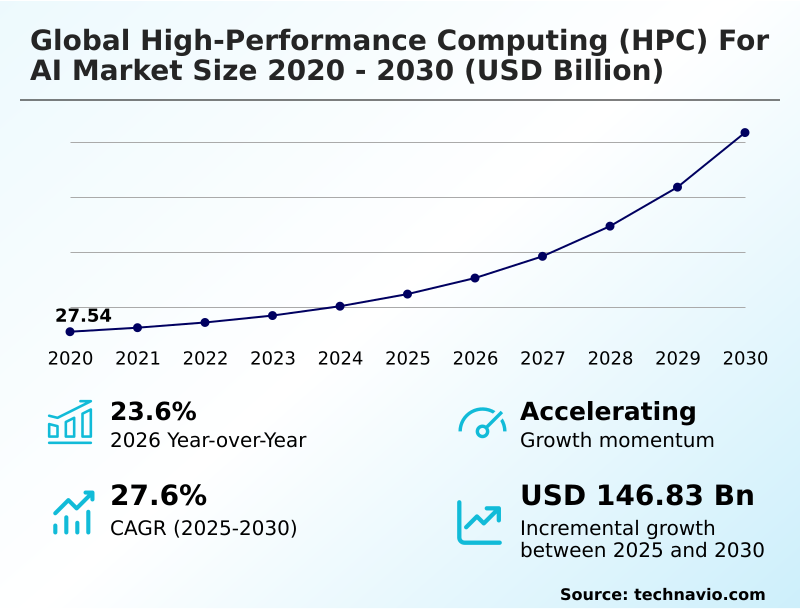

The high-performance computing (hpc) for ai market size is valued to increase by USD 146.83 billion, at a CAGR of 27.6% from 2025 to 2030. Escalating computational demands of generative AI will drive the high-performance computing (hpc) for ai market.

Major Market Trends & Insights

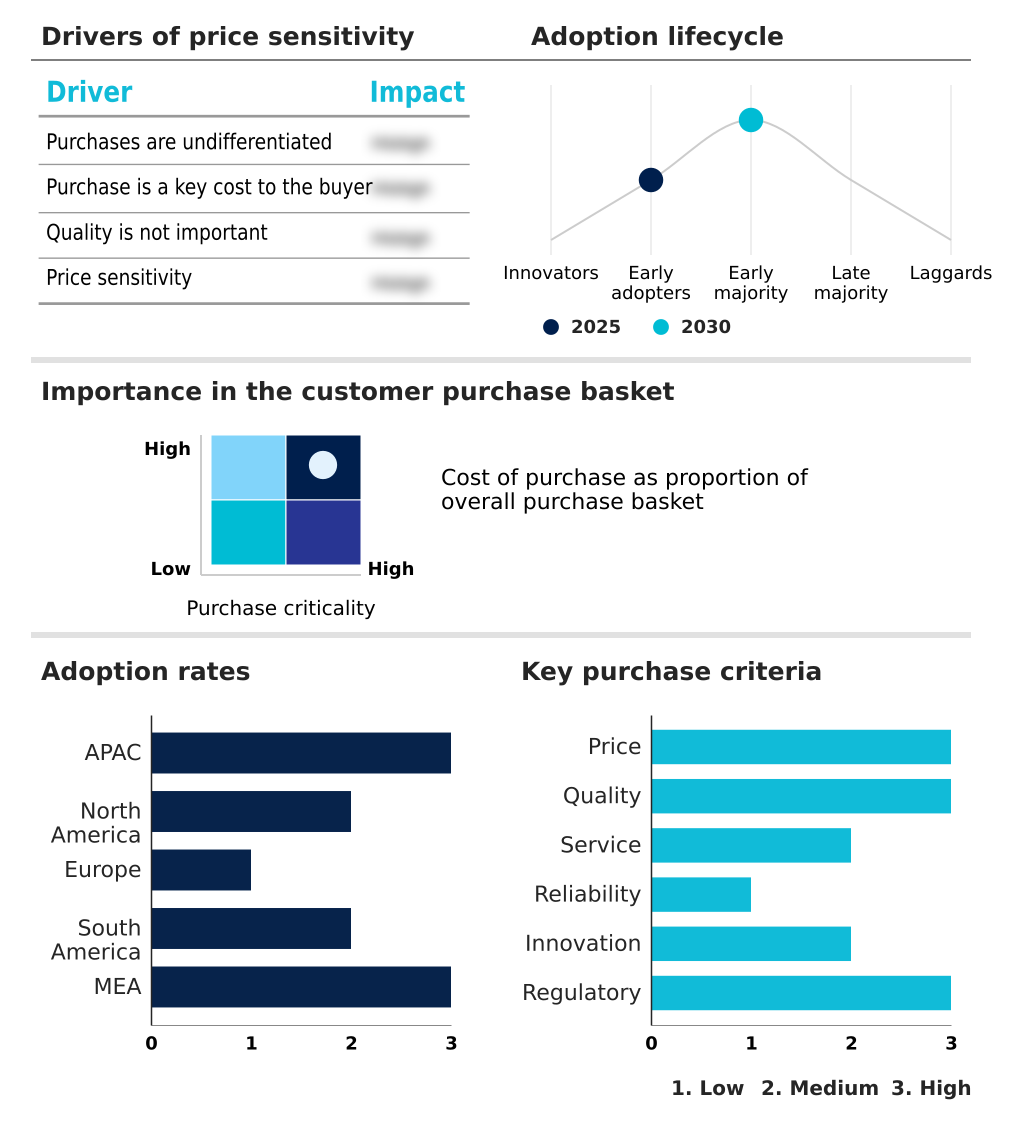

- APAC dominated the market and accounted for a 41.5% growth during the forecast period.

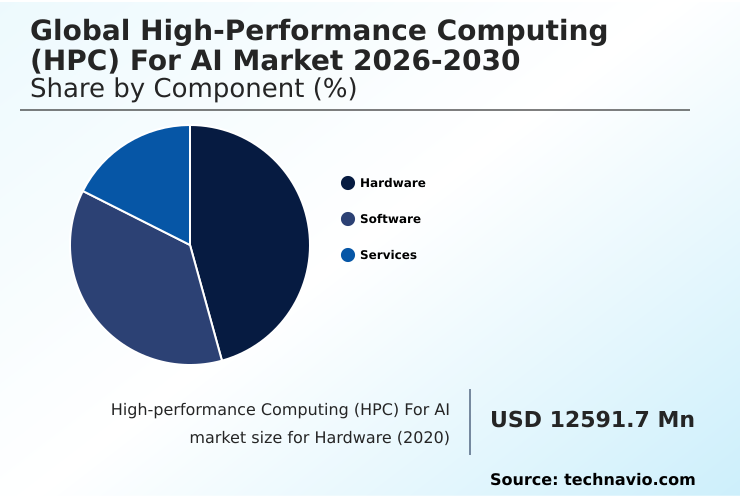

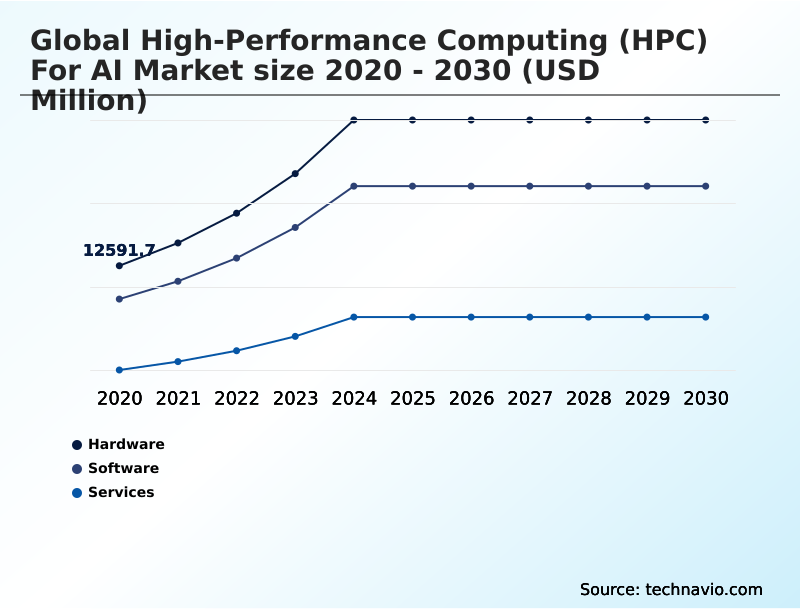

- By Component - Hardware segment was valued at USD 23.43 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 181.02 billion

- Market Future Opportunities: USD 146.83 billion

- CAGR from 2025 to 2030 : 27.6%

Market Summary

- The high-performance computing for AI market is defined by the integration of massive computational power with advanced algorithms to process complex datasets at exceptional speeds. This involves parallel processing architectures, such as graphics processing units and specialized AI accelerators, to enable deep learning, neural network training, and large-scale analytics.

- Unlike standard computing, it leverages high-speed interconnects and extensive memory bandwidth to execute trillions of calculations per second. This capability is essential for innovation in fields like genomic sequencing, climate modeling, and autonomous vehicle development. For instance, in pharmaceutical research, it facilitates complex molecular docking simulations, drastically reducing the time required to identify viable drug candidates.

- By accelerating both model training and inference, high-performance computing for AI provides a critical strategic advantage, enabling organizations to solve intricate problems that were previously computationally infeasible and forming the foundational backbone for modern scientific and industrial advancement.

What will be the Size of the High-performance Computing (HPC) For AI Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the High-performance Computing (HPC) For AI Market Segmented?

The high-performance computing (hpc) for ai industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Services

- Deployment

- On-premises

- Cloud

- Industry application

- Manufacturing

- Industrial

- Energy and utilities

- Pharmaceuticals

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment forms the foundation of high-performance computing for AI, encompassing specialized accelerators and high-density servers. This category includes high-speed interconnects, advanced storage, and sophisticated thermal management systems like direct-to-chip liquid cooling.

The demand for next-generation silicon offering superior performance-per-watt is driven by a shift to heterogeneous computing environments that utilize parallel processing.

These infrastructure components are critical for real-time data analysis in autonomous systems and genomic research, with AI-driven data center infrastructure enabling a 30% reduction in thermal management costs.

As neural network complexity increases, high-bandwidth memory and low-latency networking become key differentiators, driving investment in AI inference stacks and exascale computing platforms to support advanced AI factory operations and complex digital twin simulations.

The Hardware segment was valued at USD 23.43 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How High-performance Computing (HPC) For AI Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by North America, which is the epicenter for hyperscale data centers and semiconductor innovation, contributing over 32% of the market's incremental growth.

The APAC region is the fastest-growing, driven by national AI strategies and digital transformation, projected to account for 41.5% of market expansion. This growth is supported by a vibrant semiconductor base and the deployment of sovereign AI clouds.

In Europe, the focus is on technological sovereignty and sustainable practices, with many facilities repurposing waste heat and adopting direct-to-chip liquid cooling, which can reduce server energy use by 15%.

South America and the Middle East are emerging regions, leveraging high-performance resources for the energy sector and ambitious smart city projects, using hybrid quantum-HPC workflows for complex optimization tasks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

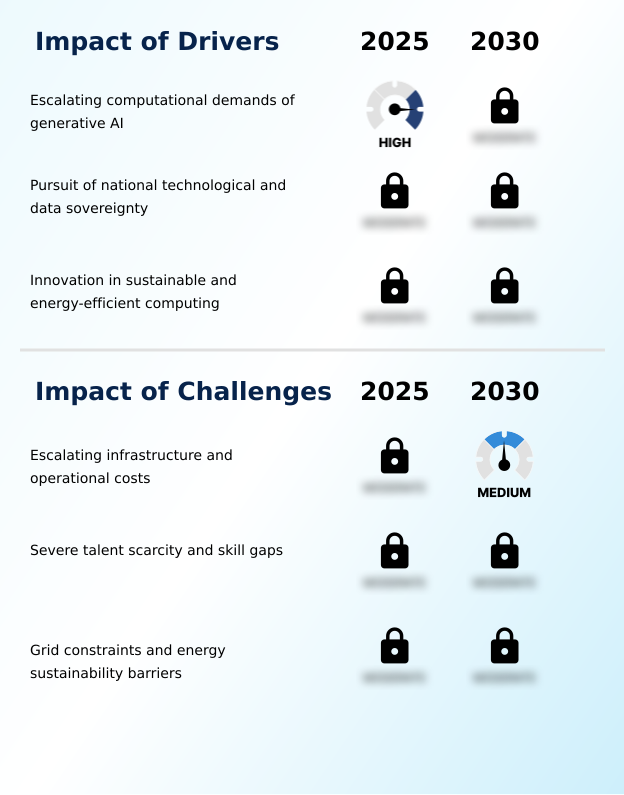

- The strategic implementation of high-performance computing for AI is increasingly focused on optimizing specific, high-value workloads, moving beyond general-purpose capabilities. For enterprises, on-premises HPC for AI security remains a primary concern, driving investment in private clusters that ensure data sovereignty and control.

- Concurrently, the appeal of cloud-based HPC for AI scalability allows organizations to manage fluctuating computational demands without massive capital outlay. A key area of development is large-scale model training infrastructure, where innovations in high-speed interconnects and distributed file systems are critical for reducing training times.

- In a direct comparison, businesses using optimized AI supercomputing energy efficiency protocols have reported up to a 40% reduction in power-related operational expenditures compared to those with legacy systems. This is particularly relevant in the context of AI factory operational cost reduction, where every watt saved translates to significant savings.

- Furthermore, specialized accelerated computing for drug discovery and sovereign AI data residency solutions are becoming distinct market segments. Successfully navigating this landscape requires addressing the HPC for AI talent gap through automated cluster management tools and managed services, ensuring that the sophisticated infrastructure delivers tangible business value and a competitive edge.

What are the key market drivers leading to the rise in the adoption of High-performance Computing (HPC) For AI Industry?

- The primary market driver is the escalating computational demand of generative AI and large language models, which require specialized, massively parallel infrastructure.

- The primary market driver is the unprecedented computational demand of generative artificial intelligence and large language models, necessitating a shift toward specialized AI factories.

- These facilities utilize high-density GPU clusters and advanced interconnects to maintain competitive model performance, reducing time-to-market for new AI applications by over 50% in some sectors.

- A second key driver is the pursuit of technological sovereignty, leading to massive investments in domestic supercomputing infrastructure and sovereign AI clouds. This trend fosters localized innovation and addresses supply chain volatility.

- Lastly, the critical need for energy efficiency and sustainable operations has become a major driver.

- The adoption of advanced cooling technologies and energy-optimized accelerators helps manage operational costs, as power consumption for some AI data centers can be reduced by 30% through such innovations.

What are the market trends shaping the High-performance Computing (HPC) For AI Industry?

- A defining market trend is the structural convergence of traditional high-performance computing, neural network training, and quantum systems into a unified, hybrid computational stack. This approach addresses multidimensional problems by combining classical and quantum processing.

- The market is defined by the convergence of traditional supercomputing, neural network training, and emerging quantum processors into a unified computational stack. This trend fosters heterogeneous architectures and hybrid quantum-HPC workflows, enabling the solution of complex problems in drug discovery and climate modeling, reducing simulation times by up to 60%.

- The proliferation of sovereign AI clouds is another major trend, as nations invest in domestic high-performance infrastructure to ensure data residency and technological independence, supported by open-source hardware like RISC-V. Concurrently, sustainability has become a core technical requirement, driving the adoption of advanced thermal management solutions such as direct-to-chip liquid cooling.

- This focus on green computing has led to new metrics like Power Compute Effectiveness, with some systems achieving a 40% improvement in performance-per-watt.

What challenges does the High-performance Computing (HPC) For AI Industry face during its growth?

- A significant market challenge is the escalating capital and operational costs associated with building and maintaining cutting-edge high-performance computing infrastructure.

- The market faces the significant challenge of escalating capital and operational expenditure, as the hardware required for trillion-parameter AI models, including AI accelerators, becomes increasingly expensive. High energy consumption and the need for advanced cooling systems create a high barrier to entry.

- This is compounded by a severe talent shortage in niche areas like parallel programming and large-scale cluster orchestration, with reports indicating AI-related skills are the most difficult for employers to find, widening the skills gap by an estimated 25% annually. Furthermore, physical grid-scale power availability has emerged as a primary bottleneck.

- The power density of AI-optimized racks can destabilize regional grids, transforming site selection into a critical search for available megawatts and hindering expansion despite technologies like performance-per-watt metrics.

Exclusive Technavio Analysis on Customer Landscape

The high-performance computing (hpc) for ai market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high-performance computing (hpc) for ai market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of High-performance Computing (HPC) For AI Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, high-performance computing (hpc) for ai market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - Offerings center on specialized hardware and scalable infrastructure, including advanced processors, AI accelerators, and comprehensive supercomputing systems designed for complex, high-performance AI and simulation workloads.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon Web Services Inc.

- Atos SE

- Cerebras Systems Inc.

- Cisco Systems Inc.

- DataDirect Networks Inc.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Google LLC

- Hewlett Packard Enterprise Co.

- IBM Corp.

- Intel Corp.

- Lenovo Group Ltd.

- Microsoft Corp.

- NEC Corp.

- NVIDIA Corp.

- Oracle Corp.

- Penguin Solutions Inc.

- SambaNova Systems Inc.

- Super Micro Computer Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in High-performance computing (hpc) for ai market

- In April, 2025, Compu Dynamics established a dedicated High-Performance Computing and Artificial Intelligence Services division to provide specialized design-build and operational support for organizations adopting data-intensive AI strategies.

- In February, 2025, The National Oceanic and Atmospheric Administration (NOAA) highlighted its use of a unified High Performance Computing and Communications (HPCC) program to support large-scale data processing and AI-driven modeling for critical weather and climate research.

- In October, 2025, Altair released Altair HPCWorks 2026, a significant platform update focused on enhancing AI and GPU-accelerated workloads through new features like Jupyter Notebook integration and AI-powered memory resource prediction for optimized job scheduling.

- In November, 2025, Equinix, in collaboration with Lenovo and Merck KGaA, Darmstadt, Germany, launched a new high-performance supercomputer designed to accelerate AI-driven scientific discovery in sectors like life sciences and healthcare, hosted in an AI-ready data center in Germany.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled High-performance Computing (HPC) For AI Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.6% |

| Market growth 2026-2030 | USD 146827.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.6% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is driven by the convergence of exascale computing capabilities with the demands of generative artificial intelligence, creating a need for specialized AI factories. These environments rely on massive parallel processing and high-density GPU clusters to handle multi-modal data streams and train large language models.

- A key development is the shift toward heterogeneous architectures that combine traditional CPUs with AI accelerators and, in experimental cases, quantum processors. This move is supported by advanced interconnects and high-bandwidth memory to overcome communication bottlenecks.

- For boardroom consideration, the adoption of sustainability-first designs, such as direct-to-chip liquid cooling and immersion systems, is now a critical budgetary and compliance factor, as organizations have demonstrated a 40% reduction in data center cooling energy.

- The pursuit of sovereign AI clouds also reflects a strategic pivot toward data residency and technological independence, requiring modular infrastructure and domestically designed chips to foster secure, localized innovation ecosystems.

What are the Key Data Covered in this High-performance Computing (HPC) For AI Market Research and Growth Report?

-

What is the expected growth of the High-performance Computing (HPC) For AI Market between 2026 and 2030?

-

USD 146.83 billion, at a CAGR of 27.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Deployment (On-premises, and Cloud), Industry Application (Manufacturing, Industrial, Energy and utilities, Pharmaceuticals, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating computational demands of generative AI, Escalating infrastructure and operational costs

-

-

Who are the major players in the High-performance Computing (HPC) For AI Market?

-

Advanced Micro Devices Inc., Amazon Web Services Inc., Atos SE, Cerebras Systems Inc., Cisco Systems Inc., DataDirect Networks Inc., Dell Technologies Inc., Fujitsu Ltd., Google LLC, Hewlett Packard Enterprise Co., IBM Corp., Intel Corp., Lenovo Group Ltd., Microsoft Corp., NEC Corp., NVIDIA Corp., Oracle Corp., Penguin Solutions Inc., SambaNova Systems Inc. and Super Micro Computer Inc.

-

Market Research Insights

- Market dynamics are shaped by the dual demands for computational power and operational efficiency, leading to the adoption of heterogeneous computing and innovative modular data center designs. The development of AI-driven data center management tools has improved power usage effectiveness by over 35% in some deployments.

- As organizations prioritize sustainability, the use of low-latency networking and energy-aware job scheduling has become standard. This focus is not just on raw processing speed but also on achieving superior performance-per-watt, a metric where advanced immersion systems can reduce cooling energy consumption by up to 90% compared to traditional air-based methods.

- This shift toward sustainability-first architectures, including AI inference stacks optimized for low power, is crucial for managing the escalating energy needs of modern AI factories.

We can help! Our analysts can customize this high-performance computing (hpc) for ai market research report to meet your requirements.

RIA -

RIA -