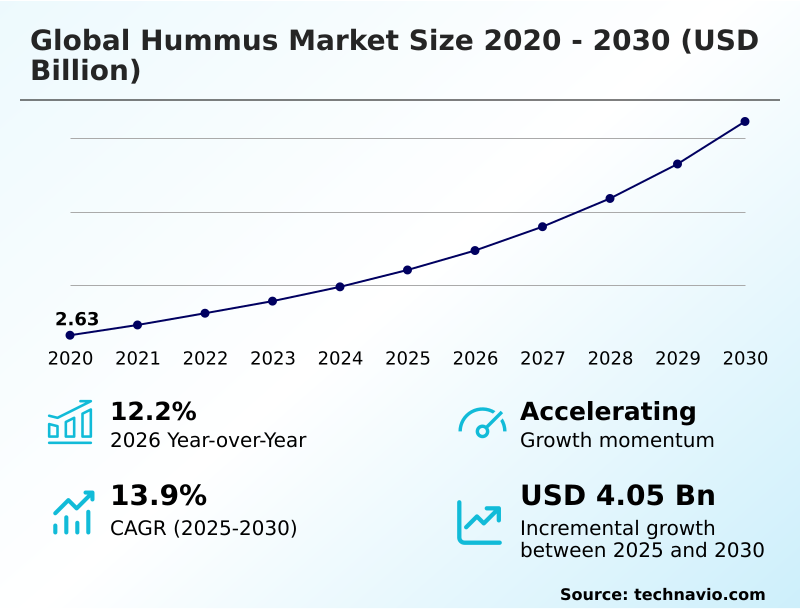

Hummus Market Size 2026-2030

The hummus market size is valued to increase by USD 4.05 billion, at a CAGR of 13.9% from 2025 to 2030. Introduction of new packaging in market will drive the hummus market.

Major Market Trends & Insights

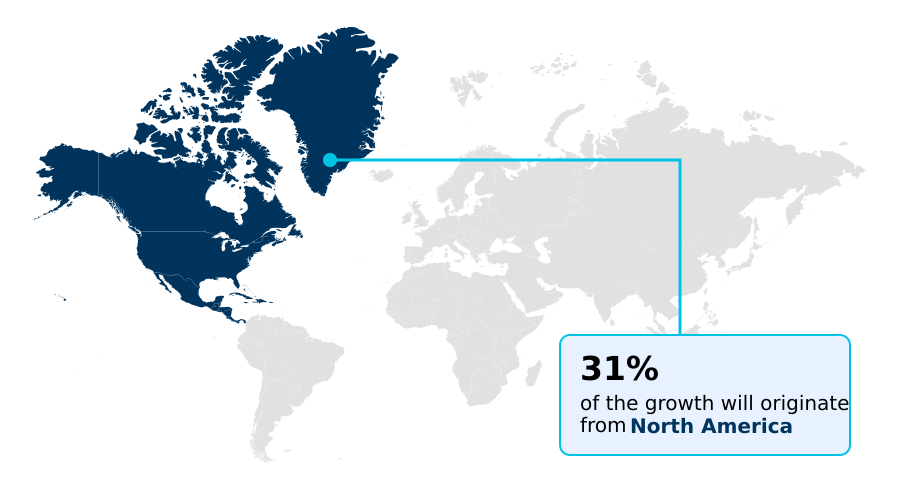

- North America dominated the market and accounted for a 30.9% growth during the forecast period.

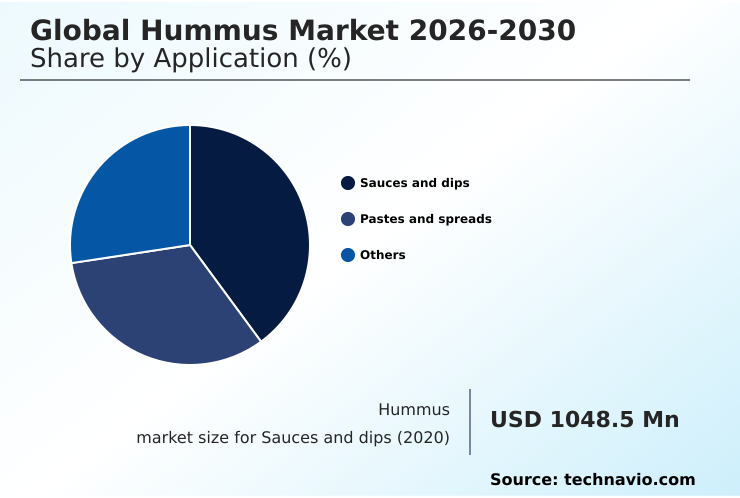

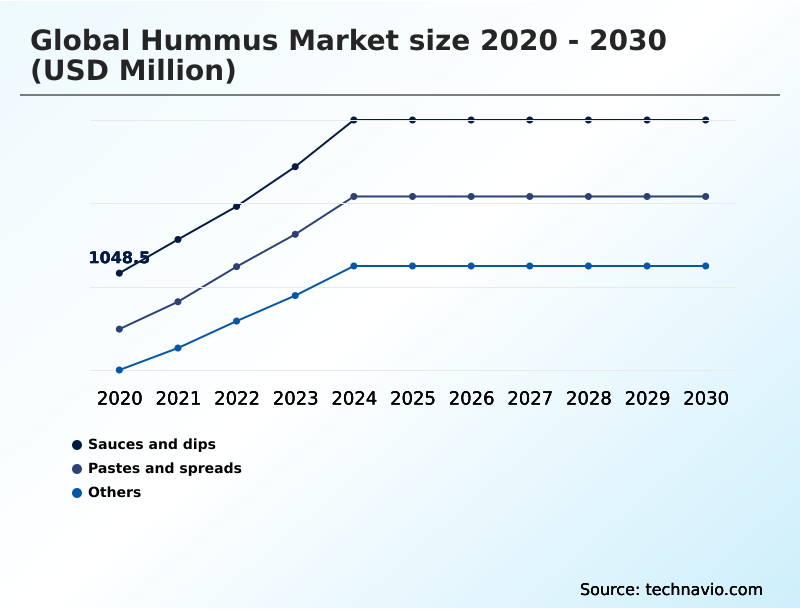

- By Application - Sauces and dips segment was valued at USD 1.57 billion in 2024

- By Type - Classic hummus segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.83 billion

- Market Future Opportunities: USD 4.05 billion

- CAGR from 2025 to 2030 : 13.9%

Market Summary

- The hummus market is characterized by robust consumer demand for healthy, convenient, and plant-based foods. As a staple in the refrigerated food category, this chickpea-based spread is evolving from a niche ethnic product to a mainstream dietary component. Key drivers include rising consumer health awareness and a shift towards plant-based nutrition.

- The market is also influenced by the pervasive snacking culture trend, with hummus positioned as a high-protein snack. In response, manufacturers are focusing on product innovation, offering an organic hummus variant and products with clean-label ingredients to meet consumer expectations for transparency and quality.

- A significant operational challenge involves managing a complex foodservice supply chain for a preservative-free recipe, where maintaining freshness and ensuring food safety compliance is critical. For instance, a producer might implement advanced cold-chain logistics, using real-time temperature monitoring to reduce spoilage by over 25%, thereby ensuring product integrity from production to the end consumer.

- This focus on quality control and innovation is essential for navigating a competitive landscape shaped by both established brands and agile private-label manufacturing.

What will be the Size of the Hummus Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Hummus Market Segmented?

The hummus industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Sauces and dips

- Pastes and spreads

- Others

- Type

- Classic hummus

- Lentil hummus

- Others

- Packaging

- Jars

- Tubs

- Pouches

- Distribution channel

- Offline

- Online

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The sauces and dips segment is estimated to witness significant growth during the forecast period.

The sauces and dips segment remains a cornerstone of the market, driven by its versatility as a healthy, savory food spread. A key application is as a creamy dip formulation for snacking, where consumer health awareness is paramount.

Demand for this plant-based protein is bolstered by the snacking culture trend, where it serves as a nutritious alternative to traditional, less healthy options. The authentic flavor profile of these products, often using clean-label ingredients, is a significant draw.

Manufacturers are responding with innovative packaging solution options, with data showing that redesigned containers can increase purchase frequency by 15% among loyal consumers. This reflects a broader shift towards convenience and ready-to-eat meal component items.

The Sauces and dips segment was valued at USD 1.57 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 30.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hummus Market Demand is Rising in North America Get Free Sample

The market’s geographic distribution is marked by varying maturity levels. In established markets, growth is driven by innovative offerings like the organic hummus variant and gluten-free food option products.

Here, a key focus is on single-serve packaging and family-size tub format options to cater to diverse household needs.

In emerging regions, market penetration is accelerating due to rising consumer incomes and exposure to global food trends, with adoption rates in some urban centers growing by 40% year-over-year.

Success in these new territories depends on adapting to local tastes through traditional recipe adaptation and overcoming logistics hurdles. The rise of the portion-controlled snack is a universal trend, linking geographies through shared consumer behaviors.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- An in-depth analysis of the sector reveals distinct dynamics shaping its trajectory. The classic hummus versus lentil hummus comparison highlights a diversification trend, where consumers are exploring alternatives beyond traditional chickpea-based foods. This shift is a key factor in the plant-based dip category competitive landscape.

- For producers, effective strategies for hummus raw material sourcing are critical for cost management, as is understanding the nutritional benefits of chickpea-based foods to guide marketing. Simultaneously, packaging innovations for ready-to-eat dips are revolutionizing consumer convenience and shelf presence.

- A significant portion of growth opportunities in the ready-to-eat food sector is linked to the product's positioning as a healthy snack alternative. This is reinforced by a texture and consistency in dip manufacturing that appeals to modern palates. Food safety regulations for refrigerated dips and a detailed cost analysis of hummus production ingredients are major operational considerations.

- The impact of vegan diets on food purchasing has been profound, creating a fertile ground for marketing strategies for ethnic food brands that emphasize clean-label food spreads. As the market evolves, an online sales strategy for fresh foods and innovation in savory dip flavor profiles become essential for capturing market share.

- Retailers are seeing a clear difference in sales velocity, with brands that effectively communicate consumer preferences for organic food ingredients and adhere to regional flavor trends in savory spreads outperforming others by a notable margin. Finally, the private-label versus branded product analysis shows a narrowing gap in consumer trust, compelling all players to refine their value propositions.

- The successful navigation of supply chain logistics for refrigerated foods and achieving shelf life improvement for fresh dips will ultimately determine long-term market leaders.

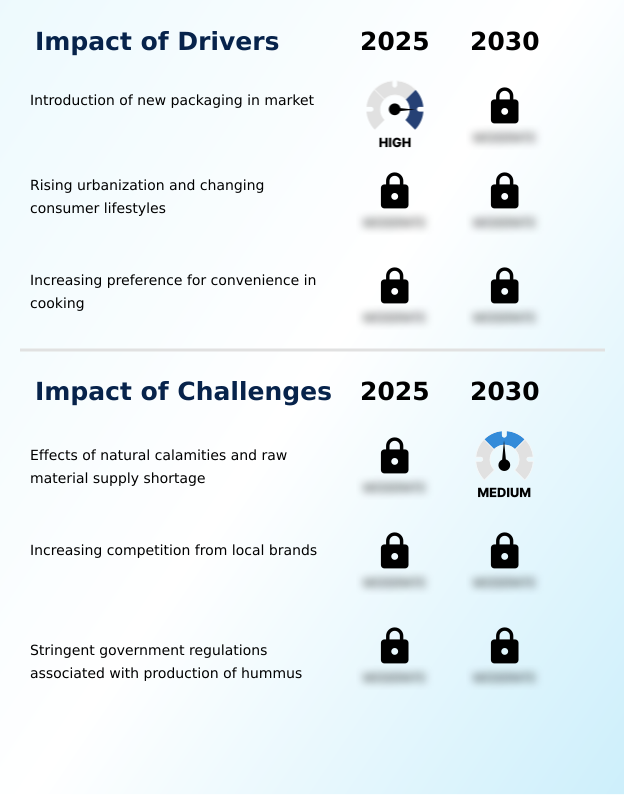

What are the key market drivers leading to the rise in the adoption of Hummus Industry?

- The introduction of new and innovative packaging solutions is a key driver for the market.

- Market expansion is significantly propelled by the increasing preference for high-protein snack options and nutrient-dense food.

- The growth is particularly evident in the refrigerated food category, where innovations in cold-pressure processing improve freshness and safety, leading to a 25% reduction in spoilage-related returns. This supports the growing on-the-go consumption trend.

- Formulations are evolving to include low-fat food formulation and low-sodium product variants to appeal to a wider health-conscious base. The development of an allergen-free product line also opens new consumer pathways.

- Promotional marketing activity often highlights these benefits, driving adoption rates and solidifying the product's position as a staple in modern diets.

What are the market trends shaping the Hummus Industry?

- The expansion of retail space is augmenting market growth, improving product visibility and accessibility for a wider consumer base.

- The emergence of private-label manufacturing is reshaping the competitive landscape, as retailers leverage brand differentiation strategy to offer value. This trend is fueled by the flexitarian diet adoption and the expanding vegan food market, which has seen product trials increase by 22% in key demographics. Value-added ingredient inclusions and regional flavor customization are becoming standard for capturing niche consumer segments.

- Success hinges on strategic retail shelf placement and a robust e-commerce distribution network. Furthermore, the push for sustainable packaging material and non-gmo certification is increasingly influencing consumer purchasing behavior, with over 60% of shoppers indicating a preference for brands with clear sustainability credentials. This dynamic necessitates a proactive approach to product development.

What challenges does the Hummus Industry face during its growth?

- The effects of natural calamities and resulting raw material supply shortages present a key challenge to industry growth.

- Navigating market challenges requires addressing both supply-side and competitive pressures. Significant supply chain vulnerability exists due to a reliance on specific agricultural outputs, where crop yield variations can cause raw material sourcing costs to fluctuate by up to 30% annually. This directly leads to competitive pricing pressure.

- The threat of market saturation point in developed regions is also a concern, intensified by an influx of smaller players. Establishing food safety compliance and managing preservative-free recipe integrity across a complex foodservice supply chain adds another layer of operational cost. Firms are mitigating these risks through direct-to-consumer sales channels and exploring cross-category application to diversify revenue streams.

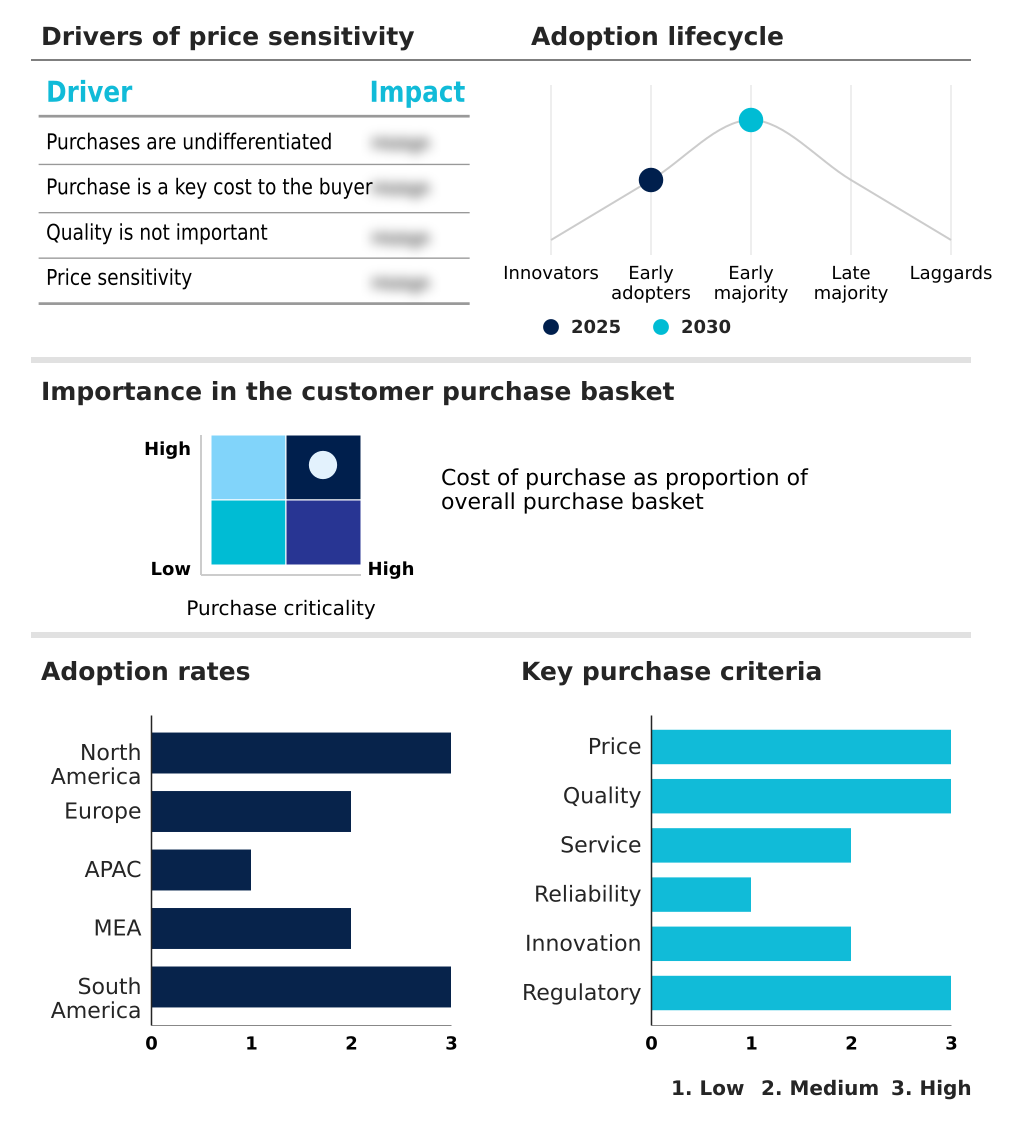

Exclusive Technavio Analysis on Customer Landscape

The hummus market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hummus market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hummus Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hummus market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Al Wadi Al Akhdar SAL - Key offerings center on refrigerated plant-based dips, leveraging flavor innovation and clean-label ingredients to meet evolving consumer health and convenience demands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Al Wadi Al Akhdar SAL

- Athenos

- Boars Head Brand

- Cedars Mediterranean Foods Inc.

- Conagra Brands Inc.

- Deldiche N.V.

- Dina Foods Ltd

- Greencore Group Plc

- Haliburton International Foods

- Hope Foods LLC

- Ithaca Hummus

- Nestle SA

- PepsiCo Inc.

- Pilpel Fine Foods

- Roots Hummus

- Sabra Dipping Co. LLC

- Savencia SA

- Strauss Group Ltd.

- The Hain Celestial Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hummus market

- In May, 2025, Cedar Mediterranean Foods Inc., introduced redesigned resealable packaging for its hummus products, focusing on freshness retention and consumer convenience in retail markets.

- In May, 2025, Walmart, expanded its private label refrigerated dips and spreads range across multiple regions, reflecting growing retailer investment in hummus and similar plant-based products.

- In April, 2025, Sabra Dipping Co. LLC, reported rising demand for single serve hummus packs in retail channels, highlighting growing consumer preference for convenient and portable food options.

- In March, 2025, The Good Food Institute, reported continued global growth in plant-based food consumption, highlighting increasing consumer preference for vegan and plant forward diets across major markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hummus Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.9% |

| Market growth 2026-2030 | USD 4051.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The hummus market is undergoing a significant transformation, driven by strong consumer health awareness and the mainstreaming of plant-based nutrition. As a key plant-based protein and dietary fiber source, this chickpea-based spread has cemented its place in the refrigerated food category.

- Success now hinges on more than a basic preservative-free recipe; it requires a commitment to clean-label ingredients, non-gmo certification, and developing an organic hummus variant to meet boardroom-level strategic goals for sustainability. The authentic flavor profile of a savory food spread remains crucial, but the product's role as a ready-to-eat meal component is expanding.

- This shift is influenced by the prevailing snacking culture trend. For manufacturers, navigating the complex foodservice supply chain while ensuring food safety compliance is paramount. Furthermore, leveraging an innovative packaging solution with sustainable packaging material is no longer optional.

- Firms using advanced techniques like cold-pressure processing to achieve shelf-life extension are reporting a 20% improvement in product longevity, directly impacting distribution efficiency and market reach for high-protein snack and gluten-free food option products.

What are the Key Data Covered in this Hummus Market Research and Growth Report?

-

What is the expected growth of the Hummus Market between 2026 and 2030?

-

USD 4.05 billion, at a CAGR of 13.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Sauces and dips, Pastes and spreads, and Others), Type (Classic hummus, Lentil hummus, and Others), Packaging (Jars, Tubs, and Pouches), Distribution Channel (Offline, and Online) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Introduction of new packaging in market, Effects of natural calamities and raw material supply shortage

-

-

Who are the major players in the Hummus Market?

-

Al Wadi Al Akhdar SAL, Athenos, Boars Head Brand, Cedars Mediterranean Foods Inc., Conagra Brands Inc., Deldiche N.V., Dina Foods Ltd, Greencore Group Plc, Haliburton International Foods, Hope Foods LLC, Ithaca Hummus, Nestle SA, PepsiCo Inc., Pilpel Fine Foods, Roots Hummus, Sabra Dipping Co. LLC, Savencia SA, Strauss Group Ltd. and The Hain Celestial Group

-

Market Research Insights

- Market dynamics are increasingly shaped by sophisticated consumer choices, with a clear preference for value-added ingredient options and products catering to flexitarian diet adoption. The expansion of single-serve packaging has led to a 15% increase in purchase frequency for on-the-go consumption occasions.

- Concurrently, brand differentiation strategy is critical, as private labels now account for a significant share of retail shelf placement, with some retailers reporting that their store brands outperform national competitors by a ratio of 1.2 to 1. E-commerce distribution channels are also gaining traction, offering a platform for regional flavor customization and traditional recipe adaptation to reach new audiences.

- These shifts underscore the necessity for agile responses to evolving consumer purchasing behavior.

We can help! Our analysts can customize this hummus market research report to meet your requirements.

RIA -

RIA -