Hydrogel Market Size 2024-2028

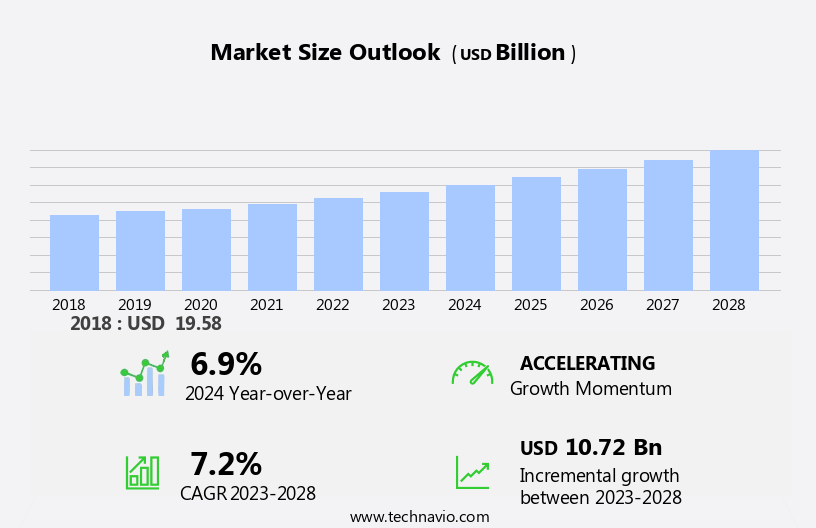

The hydrogel market size is forecast to increase by USD 10.72 billion at a CAGR of 7.2% between 2023 and 2028.

- The market exhibits long-term viability due to its increasing application in various sectors, including pharmaceuticals for medication delivery and environmental domains for wound dressing. In the pharmaceutical industry, hydrogels are utilized for the proliferation of epidermis and the treatment of dead tissue. Hydrogel formulations, such as those made from hyaluronic acid, collagen, and fibrin, are gaining popularity for their ability to mimic the natural extracellular matrix. Furthermore, the synthetic hydrogels segment is expected to grow due to the production of eco-friendly goods. Market trends include the integration of hydrogels into 3D printing technologies and the stringent regulatory requirements related to medical products. These factors contribute to the market's growth and sustainability.

What will the size of the market be during the forecast period?

- The market is experiencing significant growth due to its extensive applications in various industries, including biotechnology, tissue engineering, agriculture, medicine, personal care, and health care items. These hydrogels are primarily composed of hydrophilic polymers, such as acrylate polymers, polyvinyl alcohol, and polyacrylate, which have the unique ability to absorb and retain large quantities of water or biological fluids. In the biotechnology sector, hydrogels are used as scaffolds for tissue engineering applications, enabling the growth and proliferation of cells for the development of new tissues and organs. In the medical field, hydrogels are utilized in wound dressings and drug delivery systems, providing effective healing and controlled drug release. The agriculture industry benefits from hydrogels as soil conditioners and water retention agents, improving crop yield and reducing water usage. In the personal care industry, hydrogels are used in various products such as baby diapers, sanitary pads, paper towels, and feminine hygiene products, enhancing their absorbency and comfort properties.

- Furthermore, contact lenses are another application of hydrogels in the medical field, providing comfort and oxygen permeability to the eyes. Hydrogels also find applications in e-commerce sales, as they are used as packaging materials to ensure the safe transportation of temperature-sensitive and fragile items. The production cost of hydrogels varies depending on the type of polymers used and the manufacturing process. Synthetic polymers are typically more expensive than natural polymers but offer superior properties in terms of durability and consistency. External stimuli, such as temperature, pH, and electric fields, can be used to control the properties of hydrogels, expanding their potential applications. The market is expected to continue growing due to the increasing demand for advanced materials in various industries. The potential for innovation in hydrogel technology and the development of new applications will further drive market growth.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Material

- Synthetic

- Natural

- Hybrid

- Type

- Semi-crystalline

- Amorphous

- Crystalline

- Geography

- North America

- US

- APAC

- China

- Japan

- Europe

- Germany

- France

- South America

- Middle East and Africa

- North America

By Material Insights

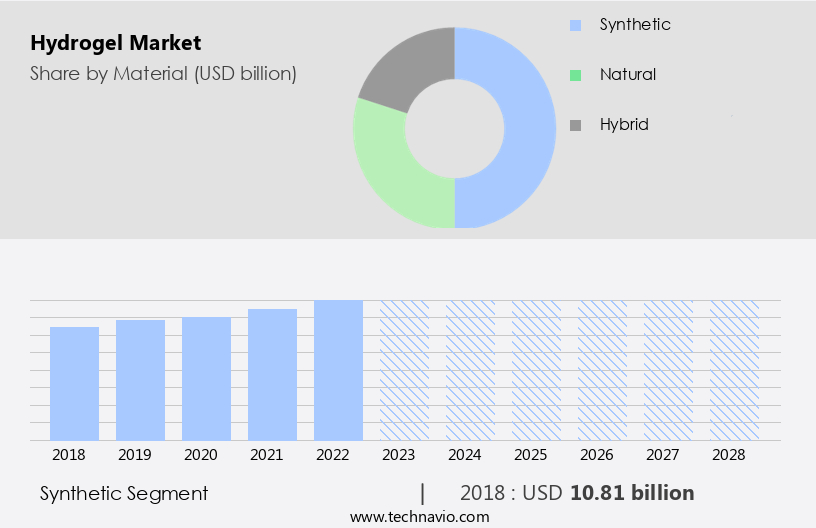

- The synthetic segment is estimated to witness significant growth during the forecast period.

Synthetic hydrogels, derived from chemically synthesized polymers such as polyacrylamide, polyvinyl alcohol, and polyethylene glycol, are gaining significant traction in various industries due to their tunable properties. In the medical sector, these materials have become indispensable in wound care and drug delivery systems. The capacity to absorb and retain water in synthetic hydrogels creates an optimal healing environment for wounds. Furthermore, the controlled drug release from synthetic hydrogel matrices enhances therapeutic efficacy. Notable synthetic hydrogel materials in the medical field include Matrigel, alginate, chitosan, and skill fibers. The amorphous hydrogels segment, comprising glycerin and water-based compounds, is popular in the wound dressing business for ulcers and surgical wounds.

Furthermore, hydrogel films and coatings under the films & matrices segment are also gaining popularity due to their ease of application and effectiveness. Some common synthetic hydrogel materials include Matrigel, alginate, chitosan, and skill fibers. In the medical field, amorphous hydrogels, such as those made from glycerin and water-based compounds, are widely used in the wound dressing business for treating ulcers and surgical wounds. Hydrogel films and coatings, which fall under the films & matrices segment, are increasingly being adopted due to their ease of application and effectiveness. Synthetic hydrogels offer a range of benefits, making them suitable for diverse applications.

Get a glance at the market report of share of various segments Request Free Sample

The synthetic segment was valued at USD 10.81 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

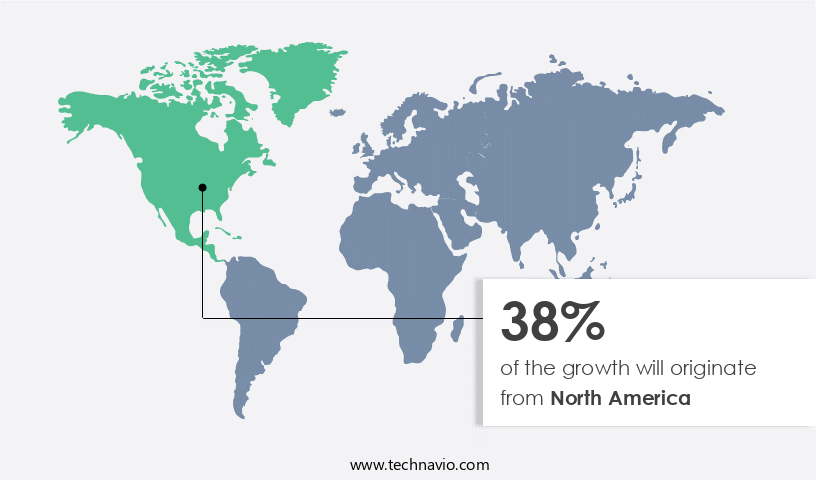

- North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America is experiencing significant growth, primarily due to the expanding applications in the personal care industry, agriculture, pharmaceuticals, and healthcare sectors in the United States and Canada. In the pharmaceutical industry, the use of hydrogels is gaining momentum, with key players driving demand. Hydrogels are essential in pharmaceuticals, particularly in drug delivery systems and wound care applications. The US's well-developed medical infrastructure and dynamic research and development sector foster innovations in hydrogel applications, notably in the areas of wound care and drug delivery systems. Hydrogels are versatile materials, available in various forms such as Amorphous, Semi Crystalline, and Crystalline.

Furthermore, they are primarily composed of Hydrophilic polymers, including both Synthetic and Natural polymers. Hydrogel production costs have been decreasing due to advancements in technology and manufacturing processes. Wireless communication, radar systems, and satellite communications are increasingly utilizing hydrogels in various applications. External stimuli such as temperature, pH, and magnetic fields can be used to control the properties of hydrogels, making them ideal for various industries. In the biomedical sector, hydrogels are used for tissue engineering, drug delivery, and wound healing. The personal care industry is also a significant consumer of hydrogels, with applications ranging from skincare to diapers.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Hydrogel Market?

Raising awareness of personal care and hygiene is the key driver of the market.

- Hydrogels, characterized by their hydrophilic structure, have gained significant traction in various industries due to their remarkable absorbent properties. These biotechnological advancements have found extensive applications in tissue engineering, agriculture, medicine, and consumer products. In the realm of personal care and hygiene, hydrogels have become essential components.

- They are integral to baby diapers, ensuring optimal absorbency and preventing skin irritation. In adult incontinence products, hydrogels provide efficient moisture absorption, ensuring user comfort and maintaining skin health. In feminine hygiene products, such as sanitary pads and tampons, hydrogels enhance absorbency and leakage prevention. Their capacity to retain moisture creates products that offer reliable and discreet protection, catering to the increasing demand for hygiene and comfort. Additionally, hydrogels are employed in healthcare items, paper towels, and other applications, further expanding their market reach.

What are the market trends shaping the Hydrogel Market?

Integration of hydrogels into 3D printing technologies is the upcoming trend in the market.

- Hydrogel-based 3D printing is an innovative trend at the nexus of materials science and additive manufacturing, gaining significant traction in various sectors. Hydrogel materials, characterized by their high water content and ability to absorb and retain large quantities of water, are meticulously deposited in layers to create intricate three-dimensional structures. This technology's versatility makes it suitable for applications in pharmaceuticals, particularly medication delivery, and environmental domains, such as wound dressing.

- In the epidermis layer, hydrogel formulations promote the proliferation of dead tissue, enhancing the healing process. In the realm of bioprinting, synthetic hydrogels segmented from hyaluronic acid, collagen, and fibrin serve as bioinks. These bioinks offer a supportive matrix for the deposition of living cells, paving the way for the creation of artificial tissues and organs. The potential applications of this technology extend beyond medical domains, encompassing ecofriendly goods and other industries. The long-term viability of hydrogel-based 3D printing is promising, offering a sustainable solution for various applications.

What challenges does the Hydrogel Market face during its growth?

Stringent regulatory requirements related to medical products is a key challenge affecting the market growth.

- In the medical field, hydrogels play a significant role in applications such as wound care and drug delivery. However, the regulatory approval process for these products is complex and time-consuming due to stringent safety, efficacy, and quality standards. Compliance with regulations from organizations like the US Food and Drug Administration (FDA) and the European Medicines Agency (EMA) adds complexity, leading to delays and increased development costs. Biocompatibility, sterilization, and clinical efficacy are essential requirements for hydrogel-based medical devices.

- Natural hydrogels derived from biological sources and synthetic hydrogels made from chemical raw materials like polyethylene glycol have unique properties suitable for various biomedical applications, including biomolecular release matrices and regenerative medicine structures. Edible polymer hydrogels and recyclable hydrogels also gain attention for their potential in reducing pollution. Ensuring the safety and efficacy of these materials while meeting regulatory requirements is a challenge for researchers and manufacturers in the medical sciences.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Alliqua Biomedical Inc.

- Ashland Inc.

- B.Braun SE

- Bristol Myers Squibb Co.

- Cardinal Health Inc.

- Coloplast AS

- Dow Chemical Co.

- Essity AB

- Evonik Industries AG

- Integra Lifesciences Corp.

- Johnson and Johnson

- Koninklijke DSM NV

- Medline Industries LP

- Medtronic Plc

- Paul Hartmann AG

- Procyon Corp.

- Smith and Nephew plc

- The Cooper Companies Inc.

- Axelgaard Manufacturing Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Hydrogels, a class of cross-linked hydrophilic polymers, have gained significant attention in various industries due to their unique properties. These water-absorbing materials possess a three-dimensional network structure that can retain large amounts of water or biological fluids. The biotechnology sector has embraced hydrogels for tissue engineering applications, including the development of regenerative medicine structures, biomolecular release matrices, and biocompatible materials for cell culture. In medicine, hydrogels have been utilized in the production of wound dressings for ulcers, surgical wounds, skin tears, minor burns, and infected wounds. They promote wound healing by maintaining a moist environment, preventing infection, and facilitating the proliferation of cells.

Furthermore, the synthetic hydrogels segment dominates the market due to its high water absorption capacity and versatility. Hydrogels have also found applications in agriculture as soil conditioners and water retention agents. In the personal care industry, they are used in baby diapers, sanitary pads, paper towels, and other hygiene products. Technological advancements in hydrogel production have led to the creation of eco-friendly goods, such as edible polymer hydrogels, which address concerns related to pollution and long-term viability. The pharmaceutical industry employs hydrogels as medication delivery systems, while the environmental domains utilize them in dielectric materials for microwave industry applications, such as antennas and radar systems.

Moreover, hydrogel films, coatings, and physiologically interfaced devices are used in various sectors, including the medical sciences, soft tissue rebuilding, and the production of anti-adhesive membranes. The market comprises a wide range of products, including polyethylene glycol hydrogels, hyaluronic acid, collagen, fibrin, matrigel, alginate, chitosan, skill fibers, superabsorbent polymers, and acrylate polymers. The market's growth is driven by the increasing demand for hydrogel-based products in various industries and the continuous development of new applications. Despite their advantages, challenges such as biocompatibility, toxicity, and production cost remain key considerations for market growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.2% |

|

Market Growth 2024-2028 |

USD 10.72 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.9 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -