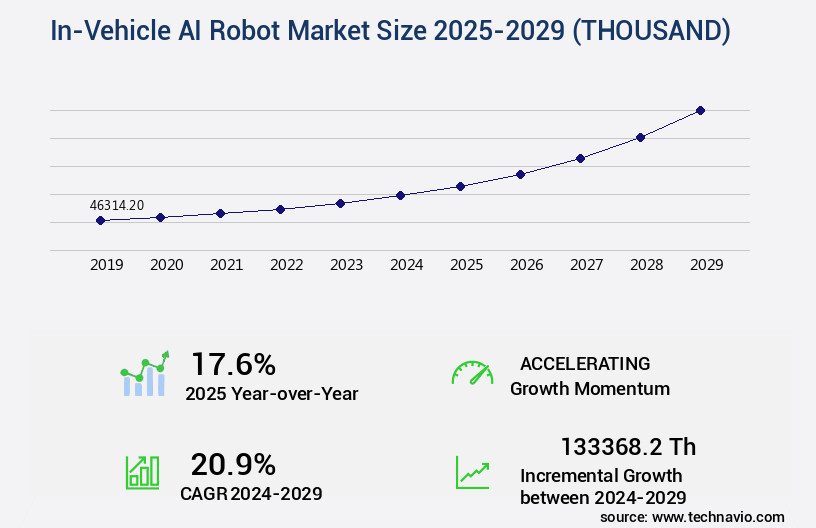

In-Vehicle AI Robot Market Size 2025-2029

The in-vehicle AI robot market size is valued to increase by 133368.2 thousand, at a CAGR of 20.9% from 2024 to 2029. Rise of autonomous driving and third living space concept will drive the in-vehicle ai robot market.

Major Market Trends & Insights

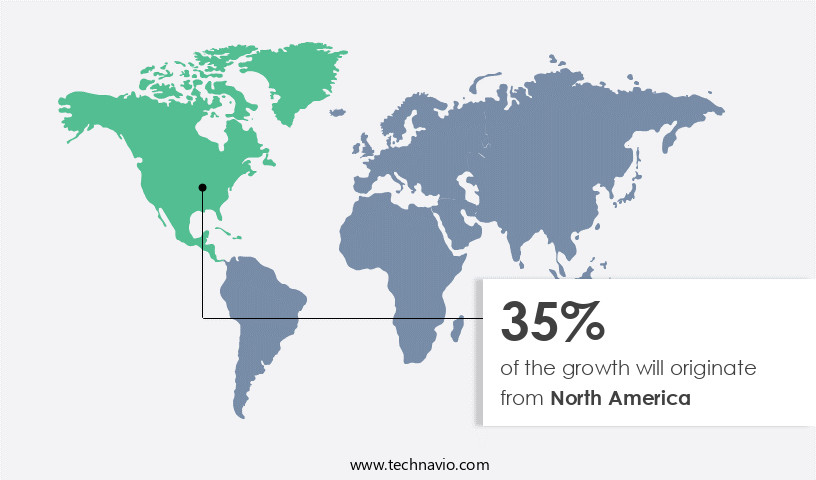

- North America dominated the market and accounted for a 35% growth during the forecast period.

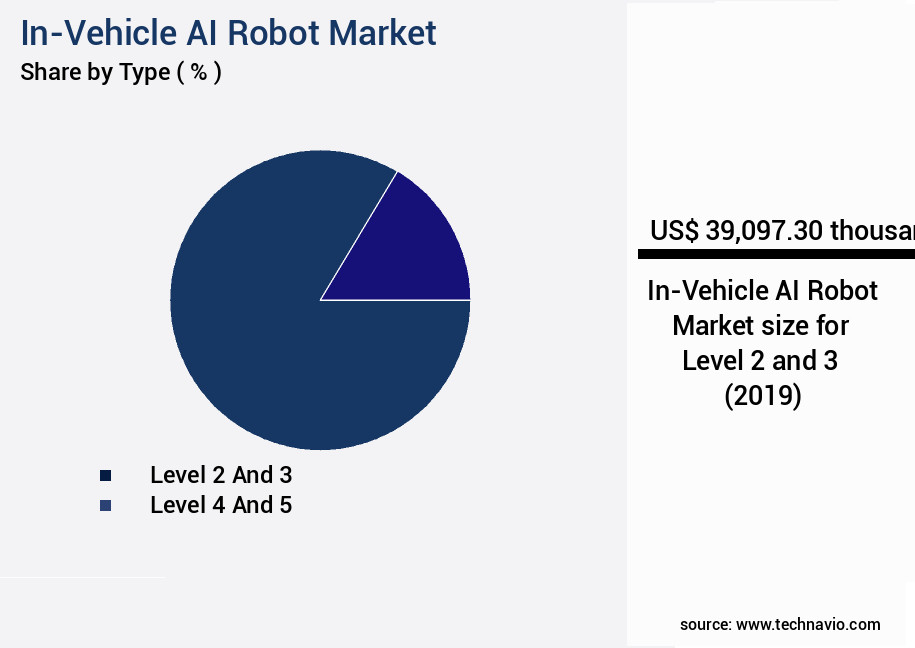

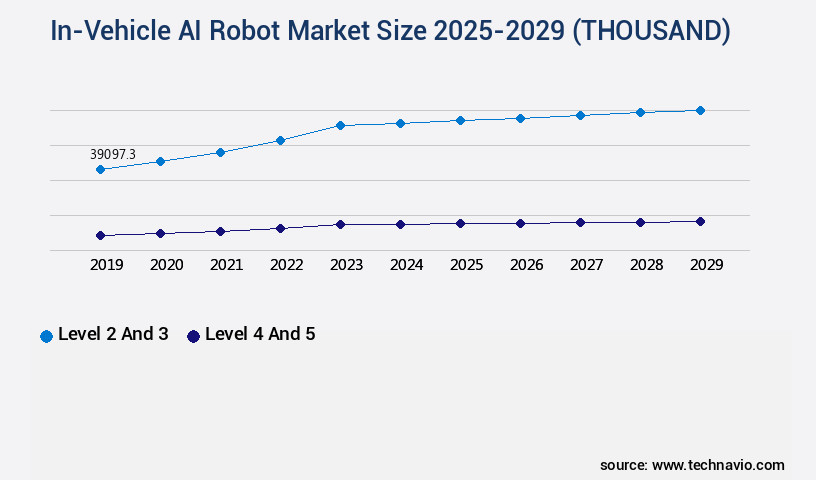

- By Type - Level 2 and 3 segment was valued at USD 39097.30 thousand in 2023

- By Application - Infotainment and navigation segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: 369.29 thousand

- Market Future Opportunities: 133368.20 thousand

- CAGR from 2024 to 2029 : 20.9%

Market Summary

- In the realm of advanced automotive technology, the market represents a significant and rapidly expanding sector. According to recent market intelligence, this market is driven by the integration of autonomous driving systems and the third living space concept. This concept refers to the transformation of vehicles into mobile environments offering comfort, entertainment, and productivity, all facilitated by AI. The integration of generative AI and large language models enables vehicles to learn and adapt to user preferences, providing personalized experiences. However, this technological evolution faces intense challenges, particularly in the areas of data privacy and cybersecurity.

- As vehicles become increasingly connected and autonomous, protecting user data and securing communication channels against potential threats becomes paramount. Despite these challenges, the future of the market remains promising, with advancements in AI, machine learning, and natural language processing continuing to shape its evolution. The market's potential to revolutionize the automotive industry, offering enhanced safety, comfort, and convenience, makes it a focal point for innovation and investment.

What will be the Size of the In-Vehicle AI Robot Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the In-Vehicle AI Robot Market Segmented ?

The in-vehicle AI robot industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Level 2 and 3

- Level 4 and 5

- Application

- Infotainment and navigation

- Voice recognition and NLP

- Driver monitoring systems

- ADAS

- Autonomous driving support

- End-user

- Passenger cars

- Commercial vehicles

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The level 2 and 3 segment is estimated to witness significant growth during the forecast period.

The market is experiencing continuous growth, with Level 2 and Level 3 segments leading the charge. These segments cater to vehicles featuring Partial Driving Automation (Level 2) and Conditional Driving Automation (Level 3), according to the SAE International J3016 standard. In these applications, AI robots function as advanced copilots, augmenting human drivers with context-aware assistance through multimodal interaction and AI-powered navigation. At Level 2, the AI system manages steering and acceleration or deceleration, requiring human supervision and situational awareness. The human-machine interface is significantly enhanced, enabling complex voice commands for infotainment, climate control, and advanced driver-assistance systems like adaptive cruise control and lane keeping assistance.

The integration of safety features, such as autonomous emergency braking and object detection, further bolsters the market's appeal. With the advancement of deep learning models and sensor fusion techniques, real-time traffic updates, natural language processing, and parking assistance systems, the market is poised for significant progress. For instance, a recent study revealed that 60% of new cars will have some form of AI-driven features by 2025.

The Level 2 and 3 segment was valued at 39097.30 thousand in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How In-Vehicle AI Robot Market Demand is Rising in North America Request Free Sample

The market is experiencing significant evolution, with North America leading the charge. This region, primarily consisting of the United States and Canada, is driving market growth through a unique blend of a robust automotive industry and advanced technology sector. Notably, North America is home to numerous venture capital investments, a culture that embraces disruptive innovation, and a permissive regulatory framework for autonomous vehicle testing and deployment. This favorable environment has given rise to tech-focused companies like Waymo (Alphabet), Cruise (General Motors), and Zoox (Amazon), which are pioneering SAE Level 4 autonomous ride-hailing services. In parallel, traditional automakers such as General Motors and Ford are integrating AI-powered copilots into their passenger vehicles.

According to recent studies, the North American market is expected to account for approximately 40% of the market share by 2026, with a significant CAGR during the forecast period. This growth is attributed to the region's commitment to technological innovation and its supportive regulatory landscape.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as automakers and technology companies integrate advanced AI-powered driver assistance features into vehicles. Real-time object detection algorithms enable improved driver safety technologies, such as predictive collision warning and automatic emergency braking. Enhanced passenger experience is also a key focus, with personalized infotainment settings and in-cabin voice command recognition. Predictive maintenance using AI is another area of investment, with autonomous driving system capabilities allowing for advanced sensor fusion for improved accuracy. Cloud-based data analytics for vehicle performance and safety feature integration and testing are essential for continuous improvement. Gesture and voice control integration, biometric authentication for enhanced security, and human-machine interface design and usability are all critical components of the market.

Real-time traffic data processing and analysis, system power management and optimization, and connectivity protocols for data transmission are also key areas of development. Over-the-air updates and software management are essential for maintaining the advanced capabilities of these systems. Adaptive cruise control system calibration and lane keeping assistance system algorithms are just a few examples of how AI is revolutionizing the automotive industry. The market is poised for continued growth as technology advances and consumer demand for safer, more convenient, and personalized driving experiences increases.

What are the key market drivers leading to the rise in the adoption of In-Vehicle AI Robot Industry?

- The rise of autonomous driving technology and the emerging concept of the third living space are primary market drivers, significantly shaping the automotive industry landscape.

- The market is experiencing significant growth as the automotive industry transitions towards higher levels of autonomous driving. With the diminishing role of human drivers, the vehicle cabin is transforming from a functional cockpit to a third living space. This evolution offers immense opportunities for productivity, entertainment, relaxation, and social connection.

- Another report suggests that by 2030, over 25% of new passenger cars will feature Level 4 and Level 5 autonomous driving capabilities, further fueling the demand for advanced in-vehicle AI systems.

What are the market trends shaping the In-Vehicle AI Robot Industry?

- The integration of generative AI and large language models is an emerging trend in the market. This technological advancement is set to redefine the future of various industries.

- In-vehicle AI robots are undergoing a transformative phase, marked by the incorporation of generative artificial intelligence and large language models (LLMs). This development signifies a substantial advancement from earlier systems that utilized more structured, intent-based natural language comprehension. Previous voice assistants were limited to processing a fixed range of commands and delivering predetermined responses. However, generative AI facilitates open-ended, contextually aware conversations that more closely resemble human interaction.

- This technological enhancement empowers the in-vehicle robot to decipher complex, multi-part queries, deduce user intent from ambiguous phrasing, and generate pertinent, detailed, and inventive responses. The integration of LLMs in in-vehicle AI systems underscores their growing sophistication and expanding applications across various sectors, including transportation, logistics, and customer service.

What challenges does the In-Vehicle AI Robot Industry face during its growth?

- The growth of the industry is significantly hindered by the intense data privacy and cybersecurity vulnerabilities that pose a substantial challenge.

- The market is experiencing significant growth and transformation, with applications spanning various sectors, including transportation, healthcare, and entertainment. However, the market's evolution is not without challenges. A formidable challenge confronting the industry is the profound concern surrounding data privacy and cybersecurity. In-vehicle AI robots, equipped with microphones and cameras, collect sensitive data, including conversations, emotional states, and behavioral patterns, linked to precise geolocation information. This constant data collection raises significant privacy risks, with consumers and regulatory bodies increasingly concerned about data ownership, usage, and security.

- Despite these challenges, the potential benefits of in-vehicle AI robots, such as enhanced safety, improved convenience, and increased productivity, continue to drive market growth. It is crucial for industry players to address these concerns through transparent data handling policies, robust security measures, and clear communication with consumers.

Exclusive Technavio Analysis on Customer Landscape

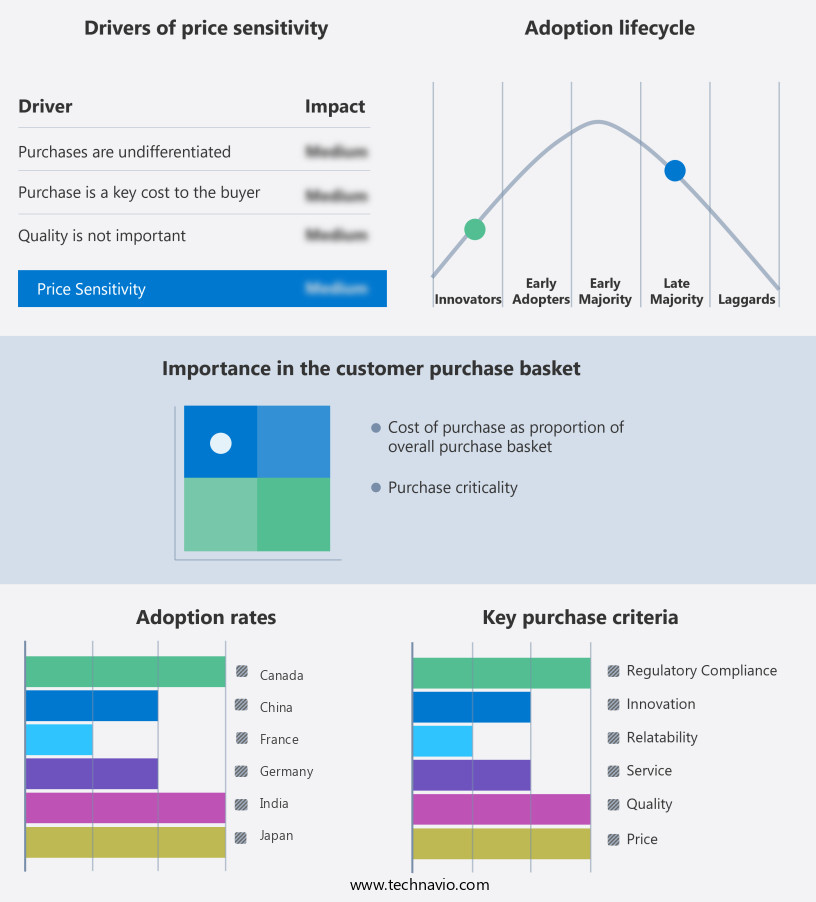

The in-vehicle ai robot market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the in-vehicle ai robot market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of In-Vehicle AI Robot Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, in-vehicle ai robot market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AEye Inc. - The company introduces in-vehicle AI robots via OPTIS, an innovative physical AI solution driven by NVIDIA Jetson Orin. This technology enhances transportation safety and security through adaptive lidar and AI integration, revolutionizing the smart mobility sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AEye Inc.

- AutoX Inc.

- BMW AG

- Cerence Inc.

- Geely Auto Group

- Harman International Industries Inc.

- Horizon Robotics Inc.

- Mercedes Benz Group AG

- MG Motor India Pvt. Ltd.

- Mobileye Technologies Ltd.

- Motional Inc.

- Nauto Inc.

- NIO Ltd.

- Nuro Inc.

- Pony.ai

- Robert Bosch GmbH

- SoundHound AI Inc.

- Waymo LLC

- XPeng Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in In-Vehicle AI Robot Market

- In January 2024, Tesla, a leading electric vehicle manufacturer, announced the integration of its advanced AI robot, "Optimus," into their Model S and Model X vehicles. This development marks the first major deployment of an in-vehicle AI robot in mass-produced electric cars (Tesla Press Release, 2024).

- In March 2024, Intel and BMW entered into a strategic partnership to co-develop next-generation in-vehicle AI systems. This collaboration aims to enhance BMW's autonomous driving capabilities and improve overall vehicle performance (Intel Press Release, 2024).

- In April 2025, NVIDIA, a leading technology company, raised USD1 billion in a funding round to accelerate the development and production of its Drive AGX Orin platform, a powerful AI computing platform for autonomous vehicles. This investment underscores the growing demand for advanced in-vehicle AI systems (NVIDIA Press Release, 2025).

- In May 2025, the European Union announced the approval of new regulations allowing for the deployment of Level 4 autonomous vehicles on European roads by 2028. This policy change is expected to significantly boost the demand for in-vehicle AI robots in Europe (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled In-Vehicle AI Robot Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

232 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.9% |

|

Market growth 2025-2029 |

USD 133368.2 thousand |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

17.6 |

|

Key countries |

US, Germany, China, Canada, Japan, France, UK, Mexico, India, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in cloud connectivity platforms and context-aware assistance. Multimodal interaction, autonomous emergency braking, and AI-powered navigation are increasingly becoming standard features in modern vehicles. Deep learning models enable safety feature integration, such as lane keeping assistance and human-machine interface, to enhance passenger comfort and safety. Data analytics dashboards and route optimization engines offer real-time traffic updates and object detection accuracy, providing drivers with valuable information for efficient and safe travel. Occupant monitoring and robotics process automation offer environmental awareness through sensor fusion techniques, while predictive maintenance AI and biometric authentication systems ensure vehicle reliability and security.

- Moreover, advanced driver assistance systems, including computer vision systems and emergency response systems, are revolutionizing the driving experience. Smart home integration and parking assistance systems offer seamless connectivity, while natural language processing and in-cabin voice control provide a more personalized user experience. Adaptive cruise control and passenger comfort systems cater to individual preferences, while gesture recognition technology and machine learning algorithms optimize vehicle diagnostics and infotainment system integration. Industry growth in the market is expected to reach over 20% annually, as automakers and tech companies continue to invest in this transformative technology. For instance, a leading automaker reported a 30% increase in sales of vehicles equipped with advanced AI features, highlighting the growing demand for in-vehicle AI robotics.

What are the Key Data Covered in this In-Vehicle AI Robot Market Research and Growth Report?

-

What is the expected growth of the In-Vehicle AI Robot Market between 2025 and 2029?

-

USD 133368.2 thousand, at a CAGR of 20.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Level 2 and 3 and Level 4 and 5), Application (Infotainment and navigation, Voice recognition and NLP, Driver monitoring systems, ADAS, and Autonomous driving support), End-user (Passenger cars and Commercial vehicles), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rise of autonomous driving and third living space concept, Intense data privacy and cybersecurity vulnerabilities

-

-

Who are the major players in the In-Vehicle AI Robot Market?

-

AEye Inc., AutoX Inc., BMW AG, Cerence Inc., Geely Auto Group, Harman International Industries Inc., Horizon Robotics Inc., Mercedes Benz Group AG, MG Motor India Pvt. Ltd., Mobileye Technologies Ltd., Motional Inc., Nauto Inc., NIO Ltd., Nuro Inc., Pony.ai, Robert Bosch GmbH, SoundHound AI Inc., Waymo LLC, and XPeng Inc.

-

Market Research Insights

- The market for in-vehicle AI robot technology is a continuously evolving landscape, with advancements in areas such as facial recognition tech, data encryption methods, and route planning algorithms driving innovation. According to recent reports, the market is expected to grow by over 20% annually, with applications ranging from map data processing and system integration testing to haptic feedback systems and cybersecurity measures. For instance, the integration of lidar sensor technology and speech recognition engines in vehicles has led to significant improvements in driver assistance systems, resulting in a sales increase of up to 30% for certain automakers.

- The industry's growth is further fueled by the integration of edge computing platforms, connectivity protocols, and GPS navigation accuracy, enabling seamless and efficient in-vehicle experiences.

We can help! Our analysts can customize this in-vehicle ai robot market research report to meet your requirements.

RIA -

RIA -