Liquid Cooling For AI Data Centers Market Size 2026-2030

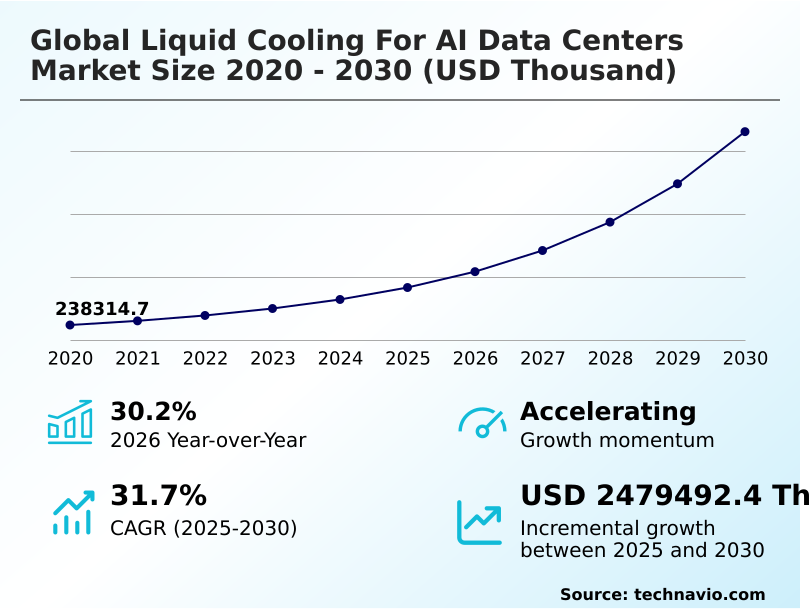

The liquid cooling for ai data centers market size is valued to increase by USD 2.48 billion, at a CAGR of 31.7% from 2025 to 2030. Elevated thermal design power and rack density in AI hardware will drive the liquid cooling for ai data centers market.

Major Market Trends & Insights

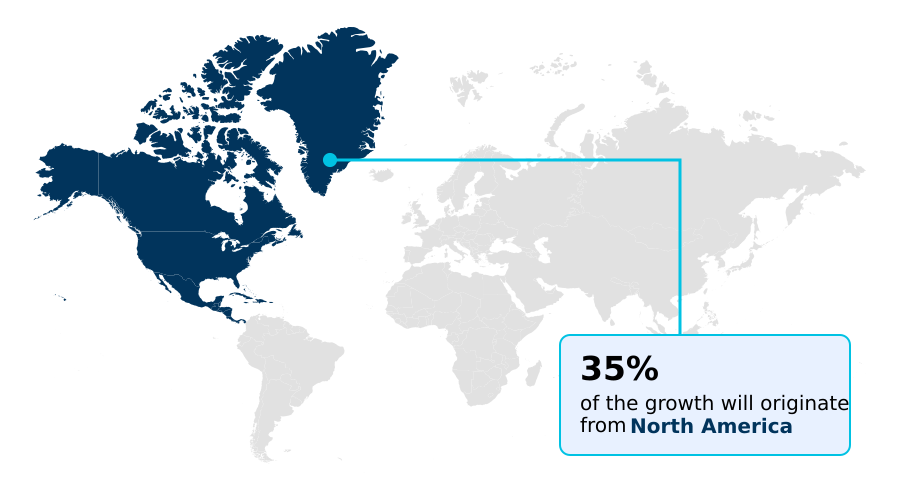

- North America dominated the market and accounted for a 34.6% growth during the forecast period.

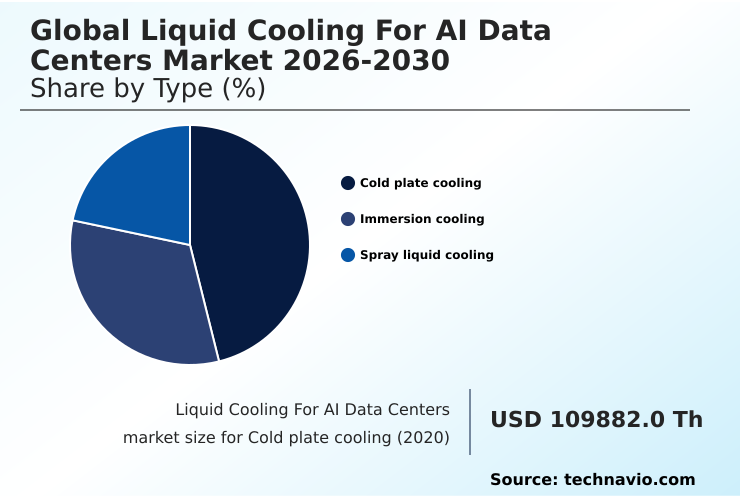

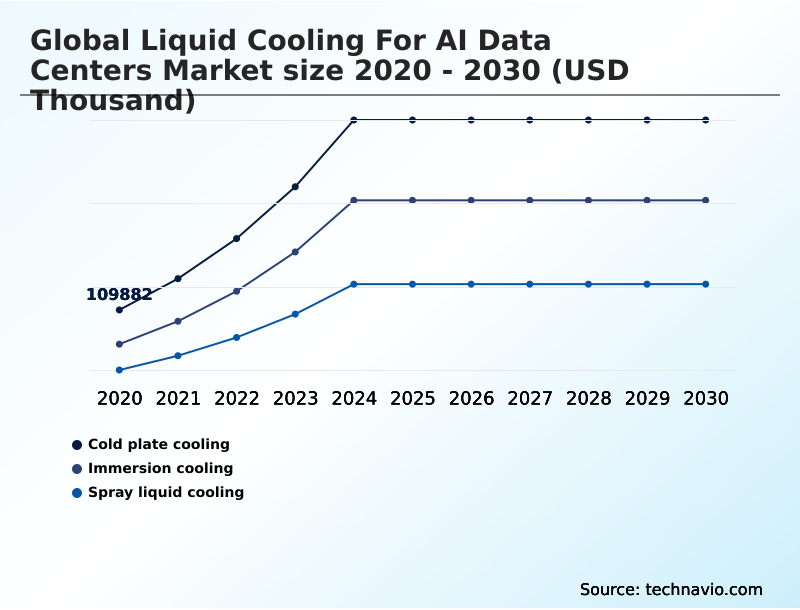

- By Type - Cold plate cooling segment was valued at USD 293.84 million in 2024

- By End-user - Hyperscale data centers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 2.48 billion

- CAGR from 2025 to 2030 : 31.7%

Market Summary

- The liquid cooling for AI data centers market is fundamentally reshaped by the escalating computational demands of modern workloads. The transition away from traditional air cooling is no longer optional for facilities deploying high-density racks for generative AI infrastructure. Key innovations in direct-to-chip cooling and single-phase cooling are becoming standard to mitigate thermal throttling and ensure hardware reliability.

- For instance, a financial services firm deploying an AI-powered risk modeling platform must prevent processor overheating to maintain data integrity and speed, making advanced thermal management systems a critical investment. This necessity drives the market toward solutions that not only manage extreme heat flux but also improve power usage effectiveness (PUE).

- The industry is also seeing a move towards modular cooling and retrofitting existing brownfield data center sites, addressing the high capital costs associated with full greenfield deployment. Operational risks, such as managing coolant chemistry and ensuring leak detection systems are flawless, remain a significant consideration for facility management.

What will be the Size of the Liquid Cooling For AI Data Centers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Liquid Cooling For AI Data Centers Market Segmented?

The liquid cooling for ai data centers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Cold plate cooling

- Immersion cooling

- Spray liquid cooling

- End-user

- Hyperscale data centers

- Colocation data centers

- Others

- Component

- Solutions

- Services

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The cold plate cooling segment is estimated to witness significant growth during the forecast period.

Cold plate cooling, a form of direct-to-chip cooling, is a pivotal segment in the liquid cooling for AI data centers market.

This method involves mounting a plate with microchannels directly onto high-power components, circulating a specialized non-conductive fluid to facilitate superior heat transfer.

Its adoption allows for a hybrid cooling environment, integrating with existing data center infrastructure management (DCIM) and reducing reliance on computer room air handler units, which can account for nearly 40% of power consumption.

The design is crucial for managing thermal throttling in AI accelerators and is a key component of effective thermal management systems.

This approach enhances hardware reliability for mission-critical hardware, offering a pragmatic balance between performance and the total cost of ownership.

The Cold plate cooling segment was valued at USD 293.84 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Liquid Cooling For AI Data Centers Market Demand is Rising in North America Get Free Sample

The geographic landscape is defined by distinct regional drivers and adoption patterns. North America, contributing over 34% of the market’s incremental growth, leads due to its high concentration of hyperscale data centers and AI accelerators, necessitating advanced thermal management systems.

In APAC, which is the fastest-growing region, the push is driven by government-led digital transformation and the need for high-density computing in urban centers, leading to increased adoption of single-phase cooling and immersion cooling.

Europe's market is heavily influenced by stringent regulations on energy conservation and carbon emissions reduction, making power usage effectiveness (PUE) a critical metric. This has accelerated the deployment of solutions that support waste heat recovery.

South America and the Middle East are emerging markets, with initial deployments in colocation facilities focusing on improving data center efficiency to handle compute-intensive workloads in challenging climates.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As organizations increasingly invest in high-performance computing, understanding the nuances of advanced thermal management becomes critical. The debate over immersion cooling vs direct-to-chip cooling often centers on application-specific needs, with the former offering comprehensive heat dissipation for the highest computational density, while the latter provides a targeted, more easily retrofitted solution.

- The primary benefits of direct-to-chip cooling include its compatibility with existing server architecture and its efficiency in managing heat flux at the source. For new builds, strategies for data center liquid cooling design are evolving to incorporate modularity and waste heat recovery from the outset.

- A major driver is reducing data center PUE with liquid cooling, which can lower energy consumption for cooling by more than half compared to legacy air systems. This is particularly crucial for AI training clusters, where the sustained, high-power draw of GPU clusters makes thermal management a primary operational challenge.

- Consequently, the focus on liquid cooling for AI training clusters is intense. For existing facilities, the process of retrofitting data centers with liquid cooling presents a viable path to upgrade capabilities without a complete rebuild, allowing operators to support liquid cooling for high-density racks and manage escalating thermal loads effectively.

What are the key market drivers leading to the rise in the adoption of Liquid Cooling For AI Data Centers Industry?

- The market is primarily driven by the elevated thermal design power and increasing rack density of specialized AI hardware.

- The primary market driver is the exponential growth in generative AI and high-performance computing (HPC) workloads, which has led to a rapid increase in the thermal design power of AI accelerators.

- Modern GPUs now generate heat loads that make traditional air cooling ineffective, necessitating a shift to liquid-based thermal management systems. This transition is not a preference but a technical requirement for facilities hosting high-density computing clusters.

- Adopting liquid cooling allows data centers to support more compute power in a smaller footprint, with some operators seeing a 50% increase in computational density per rack.

- Furthermore, imperatives for energy conservation and sustainability are compelling operators to adopt these more efficient systems, which can reduce a data center's power usage effectiveness (PUE) ratio by up to 40% compared to legacy air-cooled facilities.

What are the market trends shaping the Liquid Cooling For AI Data Centers Industry?

- A key trend is the industry's shift toward standardized, modular cooling architectures. This includes an emphasis on retrofitting strategies for existing data centers.

- Key market trends are centered on the strategic dominance of single-phase cooling and innovations in direct-to-chip cooling. The industry is moving towards modular cooling architectures, enabling scalable greenfield deployment and simplifying the retrofitting of a brownfield data center.

- These prefabricated systems, which integrate components like a coolant distribution unit, reduce onsite engineering complexity and accelerate deployment timelines for generative AI infrastructure. This standardization allows for greater interoperability between high-performance hardware and thermal management systems. For instance, facilities are achieving a 15% faster deployment time with modular units.

- Additionally, the development of advanced cold plate designs, often using additive manufacturing, is enhancing heat transfer efficiency by over 25%, allowing single-phase systems to manage thermal loads previously thought to require more complex two-phase cooling solutions.

What challenges does the Liquid Cooling For AI Data Centers Industry face during its growth?

- Significant capital expenditure requirements and the complexity of infrastructure integration present a key challenge to market growth.

- A significant market challenge is the high upfront capital expenditure and the complexity of integrating liquid cooling into existing data center infrastructure. Retrofitting a facility often involves significant downtime and modifications to the central plant, disrupting critical services. These high costs create a barrier for smaller operators, slowing broader adoption.

- The specialized nature of components like precision plumbing and coolant distribution units also leads to extended procurement lead times, delaying deployment of essential AI accelerators. Furthermore, there is a critical shortage of skilled labor capable of designing and maintaining these complex fluid dynamics systems.

- This talent gap can increase operational expenditure by up to 20% due to the need for premium compensation or reliance on external consultants for routine facility management tasks.

Exclusive Technavio Analysis on Customer Landscape

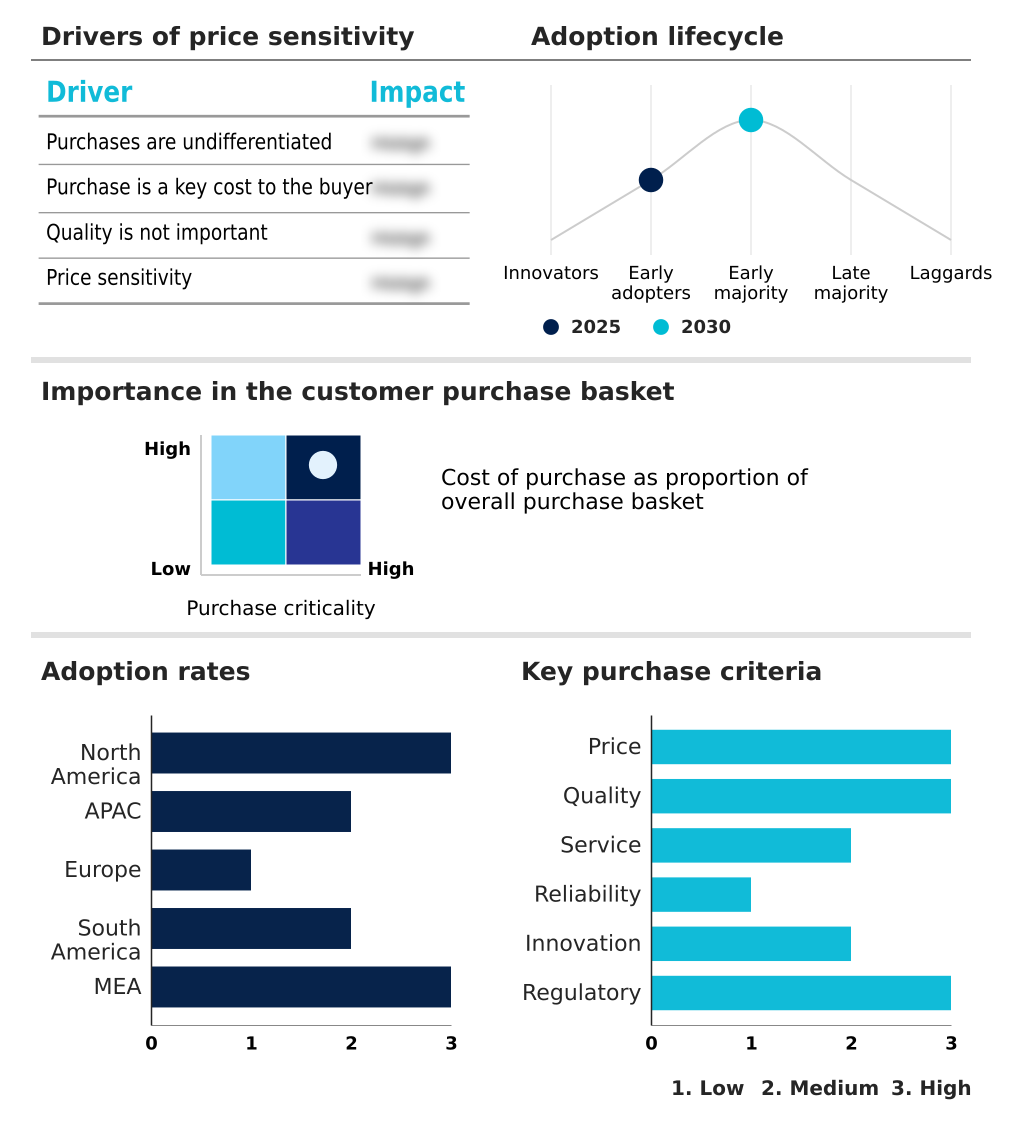

The liquid cooling for ai data centers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the liquid cooling for ai data centers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Liquid Cooling For AI Data Centers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, liquid cooling for ai data centers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aecorsis BV - Offerings include advanced thermal management systems, such as direct-to-chip and immersion cooling, which are vital for high-density AI hardware and optimizing data center efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aecorsis BV

- Asetek Danmark AS

- Boyd Corp.

- Chilldyne

- Coolit Systems

- Danfoss AS

- Dell Technologies Inc.

- Delta Electronics Inc.

- Fujitsu Ltd

- Hewlett Packard Enterprise Co.

- Iceotope Technologies Ltd.

- Lenovo Group Ltd.

- LiquidStack BV

- Motivair Corp.

- nVent Electric Plc

- Rittal GmbH and Co. KG

- Schneider Electric SE

- STULZ GmbH

- Super Micro Computer Inc.

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Liquid cooling for ai data centers market

- In February 2025, Microsoft announced a landmark update to its data center design philosophy, mandating direct-to-chip liquid cooling for all new server deployments intended for its Azure AI and high-performance computing cloud services.

- In March 2025, Hewlett Packard Enterprise announced an expanded strategic alliance with Coolit Systems to co-engineer a new generation of servers for the HPE Cray portfolio, featuring pre-installed direct-to-chip liquid cooling.

- In April 2025, Equinix announced the launch of its AI Powerhouse initiative in its Ashburn, Virginia campus, involving a strategic partnership with Vertiv to build new data halls engineered for immersion cooling.

- In May 2025, G42, an Abu Dhabi-based AI and cloud computing company, announced a partnership with LiquidStack to build a new AI supercomputing center in Masdar City using two-phase immersion cooling.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Liquid Cooling For AI Data Centers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 31.7% |

| Market growth 2026-2030 | USD 2479492.4 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.2% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The liquid cooling for AI data centers market is driven by the physical limitations of air in managing the thermal design power of modern processors. Innovations center on direct-to-chip cooling and immersion cooling, which offer superior heat transfer. Key components like a coolant distribution unit, cold plate, and heat exchanger are essential for system efficacy.

- The industry focuses on improving power usage effectiveness (PUE) and managing the high heat flux from server rack power density. For boardroom decisions, the choice of a thermal management system directly impacts operational budgets, with advanced systems reducing energy use by over 30%. Technologies such as single-phase cooling and two-phase cooling are deployed to prevent thermal throttling and ensure reliability.

- Operators must also consider coolant chemistry, refrigerant distribution, and the use of quick-disconnect fittings to mitigate risks. Modular cooling designs and rear-door cooling units are gaining traction for their flexibility in both new and existing facilities, addressing the need for scalable solutions that support evolving hardware requirements.

What are the Key Data Covered in this Liquid Cooling For AI Data Centers Market Research and Growth Report?

-

What is the expected growth of the Liquid Cooling For AI Data Centers Market between 2026 and 2030?

-

USD 2.48 billion, at a CAGR of 31.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Cold plate cooling, Immersion cooling, and Spray liquid cooling), End-user (Hyperscale data centers, Colocation data centers, and Others), Component (Solutions, and Services) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Elevated thermal design power and rack density in AI hardware, Significant capital expenditure requirements and infrastructure integration complexity

-

-

Who are the major players in the Liquid Cooling For AI Data Centers Market?

-

Aecorsis BV, Asetek Danmark AS, Boyd Corp., Chilldyne, Coolit Systems, Danfoss AS, Dell Technologies Inc., Delta Electronics Inc., Fujitsu Ltd, Hewlett Packard Enterprise Co., Iceotope Technologies Ltd., Lenovo Group Ltd., LiquidStack BV, Motivair Corp., nVent Electric Plc, Rittal GmbH and Co. KG, Schneider Electric SE, STULZ GmbH, Super Micro Computer Inc. and Vertiv Holdings Co.

-

Market Research Insights

- Market dynamics are increasingly shaped by the need to support high-density computing and generative AI infrastructure. The total cost of ownership is a primary consideration, with operators seeking solutions that improve data center efficiency and reduce operational expenditure.

- The adoption of liquid cooling can lower cooling energy costs by more than 30% compared to traditional methods, directly impacting a facility's power usage effectiveness (PUE). Furthermore, ensuring hardware reliability and uptime for mission-critical hardware is non-negotiable. Effective thermal management reduces component failure rates by over 20%, a critical factor for colocation facilities bound by strict service level agreements.

- The shift from capital-intensive greenfield deployment to retrofitting a brownfield data center reflects a strategic pivot to manage investment while still upgrading thermal headroom for compute-intensive workloads.

We can help! Our analysts can customize this liquid cooling for ai data centers market research report to meet your requirements.

RIA -

RIA -