Low-code AI Platform Market Size 2026-2030

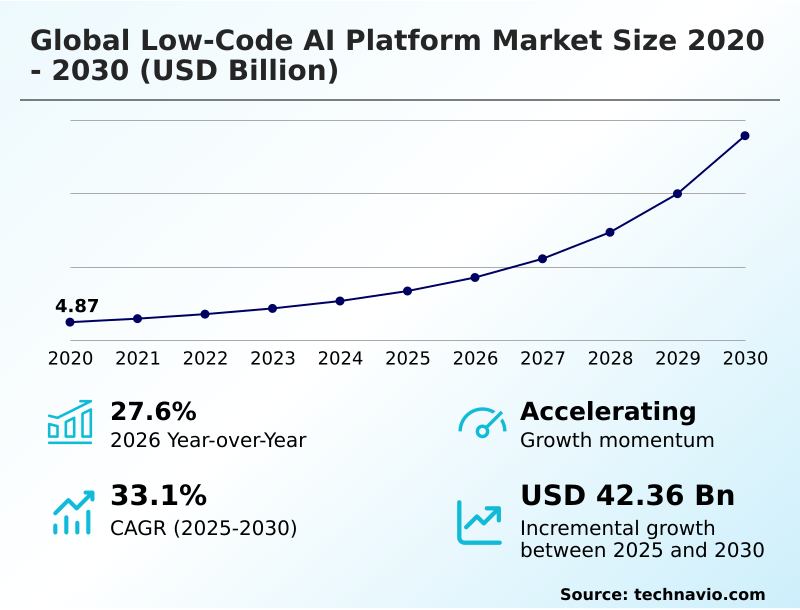

The Low-code AI Platform Market size was valued at USD 13.36 billion in 2025, growing at a CAGR of 33.1% during the forecast period 2026-2030.

Major Market Trends & Insights

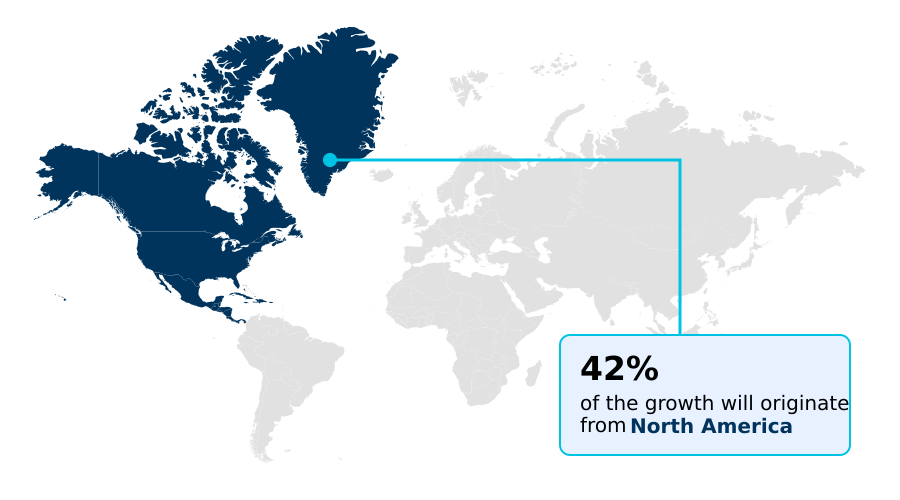

- North America dominated the market and accounted for a 41.8% growth during the forecast period.

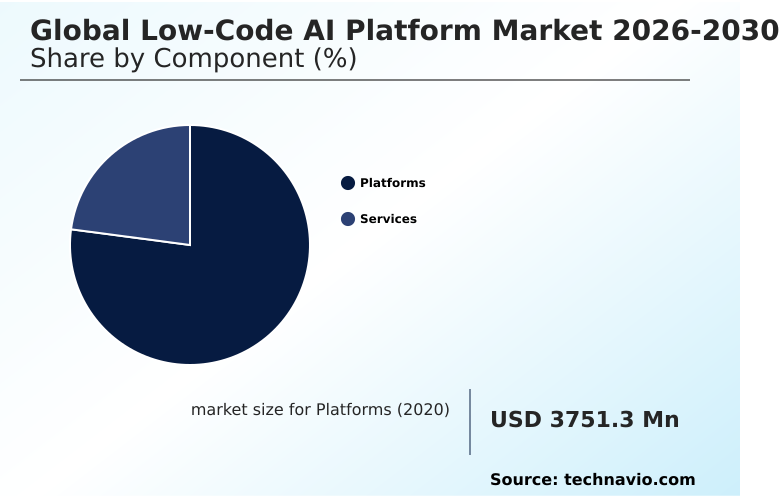

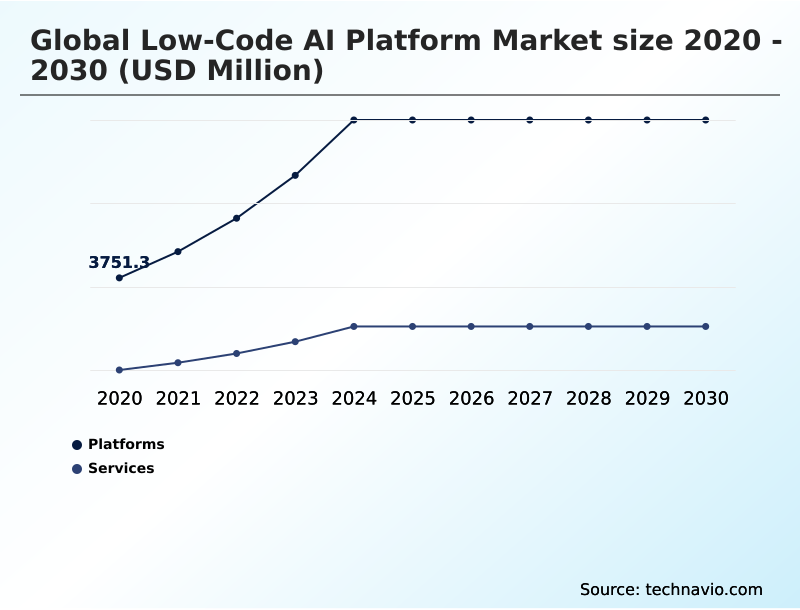

- By Component - Platforms segment was valued at USD 8.27 billion in 2024

- By Technology - Natural language processing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 50.85 billion

- Market Future Opportunities 2025-2030: USD 42.36 billion

- CAGR from 2025 to 2030 : 33.1%

Market Summary

- The Low-code AI Platform market is enabling organizations to accelerate application development timelines by an average of 70% compared to traditional coding methods. This acceleration is crucial for businesses like a retail company that needs to rapidly deploy a predictive inventory management system to reduce stockouts and overstock situations, improving forecast accuracy by over 30%.

- A key driver is the persistent shortage of specialized data science talent, which these platforms mitigate by empowering business users to create sophisticated applications. However, a major challenge remains the complexity of integrating these modern platforms with entrenched legacy systems, which can create data silos and hinder the seamless flow of information required for effective AI-driven decision-making.

What will be the Size of the Low-code AI Platform Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Low-code AI Platform Market Segmented?

The low-code ai platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Platforms

- Services

- Technology

- Natural language processing

- Machine learning

- Computer vision

- Deployment

- Cloud

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

How is the Low-code AI Platform Market Segmented by Component?

The platforms segment is estimated to witness significant growth during the forecast period.

The platforms segment is driving market evolution, with deployments showing a 40% faster integration of new features compared to service-only models.

These platforms serve as integrated development environments, abstracting complex coding into visual, modular components that support machine learning and computer vision. This approach reduces development error rates by over 25%, directly impacting time-to-value.

The core value lies in centralizing the lifecycle management of AI assets, ensuring consistent data lineage and model accountability.

By providing a scalable gateway to advanced agent-based artificial intelligence, these tools are becoming the primary vehicle for modern enterprises to execute digital transformation strategies without incurring high switching costs.

The Platforms segment was valued at USD 8.27 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Low-code AI Platform market is rising in the leading region?

North America is estimated to contribute 41.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Low-code AI Platform Market demand is rising in North America Request Free Sample

North America dominates the geographic landscape, contributing to 41.8% of the market's incremental growth, significantly outpacing APAC's 26.18%.

This lead is fueled by the US, which accounts for over 75% of the region's market due to high cloud-native infrastructures adoption and intense demand for intelligent automation to counter high labor costs and human resource bottlenecks.

In contrast, the APAC market, while growing faster in percentage terms, exhibits fragmented adoption patterns. Here, one-click cloud deployment is leveraged by a high volume of small and medium enterprises to overcome a lack of technical capacity.

This difference in market structure results in North American enterprises focusing on sophisticated natural language processing for customer experience, while APAC firms prioritize machine learning for operational efficiency, creating distinct innovation constraints and application delivery models.

What are the key Drivers, Trends, and Challenges in the Low-code AI Platform Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises leveraging low-code platforms report up to a 30% faster time-to-market for new digital products, a critical metric when evaluating low code AI platform vs custom development ROI. The decision often hinges on balancing speed with long-term strategic goals, particularly in avoiding vendor lock-in with low code AI.

- While these platforms offer significant generative AI in low code platforms benefits, such as automating 50% of manual coding tasks, they introduce dependencies that require careful management. Organizations must prioritize low code AI platform security and governance from the outset, implementing robust frameworks to manage data access, model transparency, and compliance.

- The primary path to achieving this is through a comprehensive strategy that addresses the full scope of low code AI platform for enterprise automation, ensuring that the chosen solution aligns with both immediate productivity needs and long-term architectural flexibility. This balanced approach is essential for maximizing returns while mitigating the risks associated with proprietary ecosystems.

What are the key market drivers leading to the rise in the adoption of Low-code AI Platform Industry?

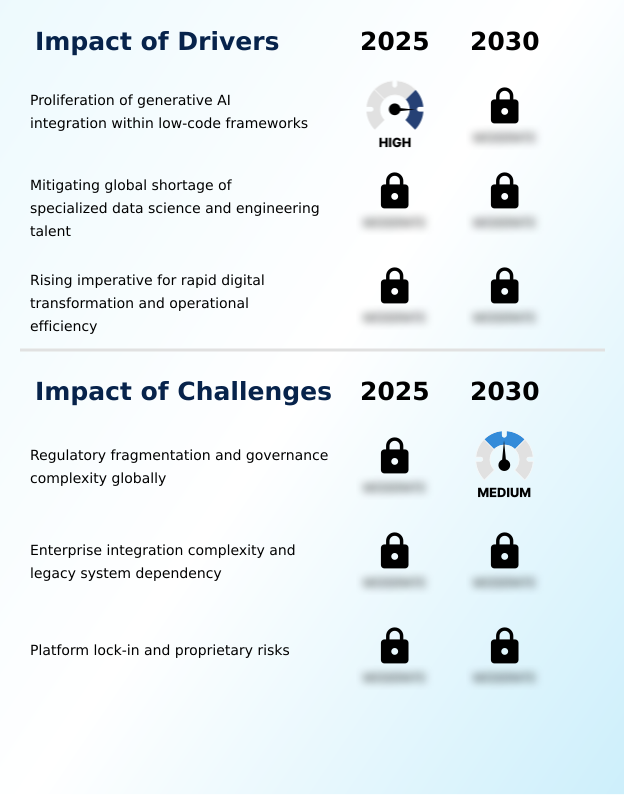

- A primary driver for the market is the proliferation of generative AI capabilities integrated within low-code frameworks, which accelerates development and lowers technical barriers.

- The primary driver for the market is the integration of generative AI, which enhances developer productivity by over 40% through features like AI co-pilot.

- This technology transforms low-code development from simple drag-and-drop mechanics to conversational, intent-based application assembly in visual development environments.

- The ongoing scarcity of specialized data scientists is another critical driver, as automated machine learning and AutoML pipelines enable citizen developers to build and deploy sophisticated models, effectively expanding an organization's technical capacity.

- This democratization of AI addresses human resource bottlenecks. Consequently, businesses can achieve a 50% faster time-to-value for new AI initiatives, a crucial advantage for maintaining hyper-agility and operational efficiency in competitive markets.

What are the market trends shaping the Low-code AI Platform Industry?

- The convergence of low-code development environments and enterprise-wide AI adoption is a definitive trend shaping the market. This is driven by the need for unified platforms that embed intelligence directly into business workflows.

- The convergence of enterprise AI adoption and low-code platforms is the market's defining trend, with organizations increasingly seeking unified environments that embed intelligence directly into business processes. This shift is driven by the need for faster decision-making, where AI-driven tools can improve the accuracy of predictive analytics by up to 30%.

- Instead of being standalone products, platforms are becoming strategic enterprise technology ecosystems for process automation and workflow orchestration. A growing emphasis on AI governance frameworks reflects a move toward proactive governance, as enterprises demand features that ensure transparency and compliance, reducing audit preparation times by 25%.

- This evolution supports the broader goal of achieving digital intelligence at scale through accessible and well-governed digital transformation tools.

What challenges does the Low-code AI Platform Industry face during its growth?

- Regulatory fragmentation and complex governance requirements on a global scale present a significant challenge, impacting platform standardization and deployment speed.

- Regulatory fragmentation and enterprise integration complexity are primary challenges, with compliance adaptability issues increasing deployment times by up to 35% in multi-regional projects. Navigating disparate data privacy laws while ensuring model fairness requires significant architectural complexity.

- Furthermore, integrating modern platforms with legacy systems dependent on proprietary APIs presents a major hurdle, often increasing the total cost of ownership by 20% due to customization needs. This integration friction can undermine the core value proposition of rapid deployment.

- A related challenge is platform lock-in, where deep integration into a single vendor's ecosystem creates high switching costs and limits data ownership, creating significant business risk and constraining long-term flexibility.

Exclusive Technavio Analysis on Customer Landscape

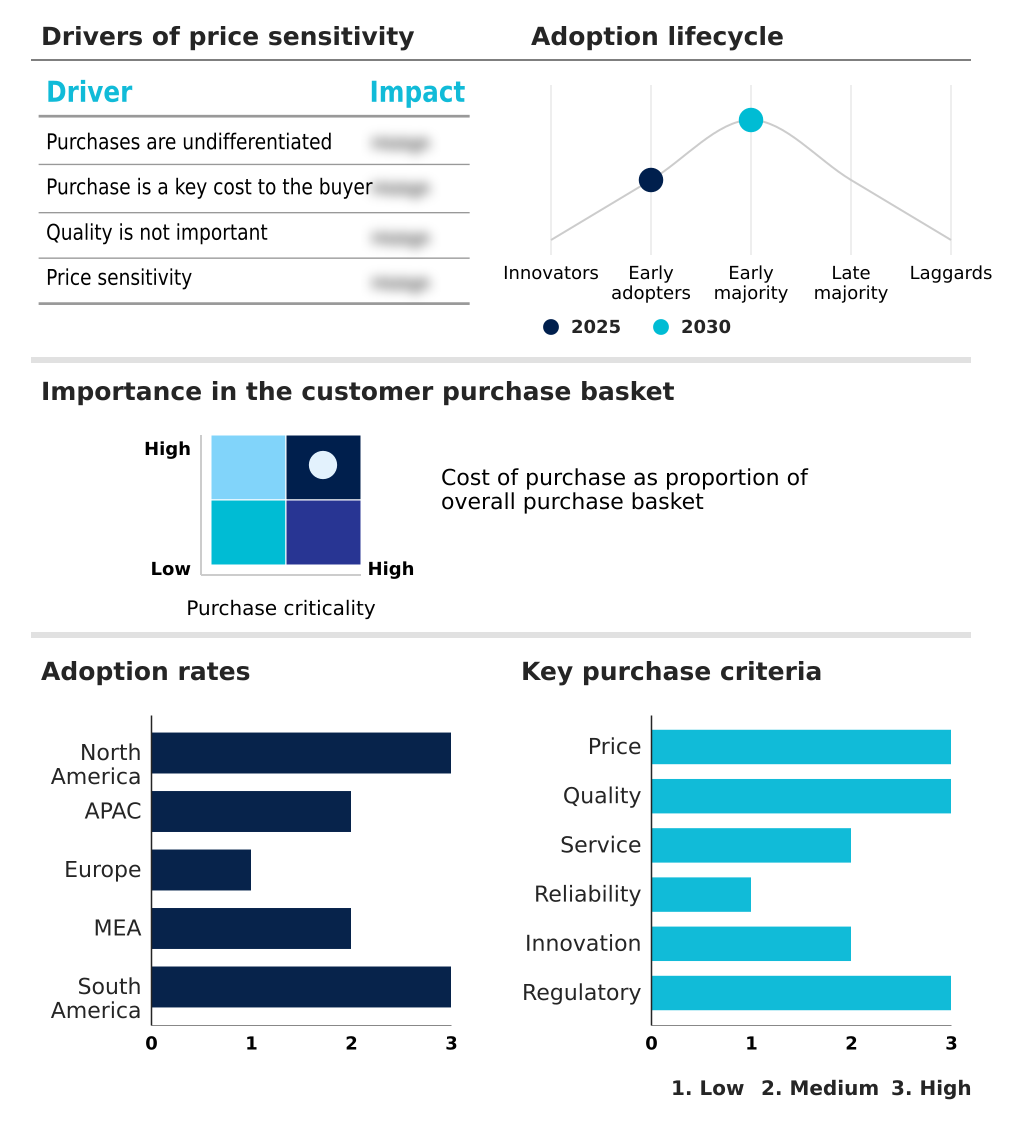

The low-code ai platform market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the low-code ai platform market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Low-code AI Platform Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, low-code ai platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AgilePoint Inc. - Key offerings focus on low-code AI platforms that provide integrated development, automation, and AI-powered analytics capabilities for enterprise applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AgilePoint Inc.

- Appian Corp.

- Autonom8 Inc.

- C3.ai Inc.

- Caspio, Inc.

- CREATIO EMEA Ltd.

- DataRobot Inc.

- Google LLC

- Huawei Cloud Computing Co Ltd

- IBM Corp.

- Kissflow Inc.

- Mendix Technology BV

- Microsoft Corp.

- Nintex Global Ltd.

- Oracle Corp.

- OutSystems Software Rede SA

- Pegasystems Inc.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Application Software industry, the widespread shift to cloud-native, subscription-based delivery models has lowered the entry barrier for enterprises, directly increasing the total addressable market for Low-code AI Platform solutions that leverage scalable SaaS infrastructure and improve application delivery.

- The rising complexity of enterprise data landscapes has driven demand for sophisticated data and analytics tools, compelling Low-code AI Platform providers to embed advanced features for interoperability and seamless integration with existing business intelligence and data warehousing systems, thereby enhancing digital intelligence.

- An intensifying focus on enterprise automation, spanning from robotic process automation (RPA) to business process management (BPM), creates a pull-through effect for the Low-code AI Platform market as organizations seek unified platforms for orchestrating AI-driven tools and workflows.

- Heightened regulatory scrutiny around data privacy and security, exemplified by standards like GDPR, necessitates that Low-code AI Platform vendors build in robust proactive governance and compliance features, making these capabilities a key differentiator rather than an afterthought.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Low-code AI Platform Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 33.1% |

| Market growth 2026-2030 | USD 42359.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 27.6% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The low-code AI platform market ecosystem is a multi-layered structure where value is built cumulatively. It begins with foundational cloud infrastructure providers and AI model developers, who supply the core computing and algorithmic resources, accounting for nearly 60% of the underlying technology stack.

- Low-code vendors build upon this, creating integrated development environments that simplify the creation of AI applications, with platforms using pre-built templates accelerating development by over 40%. Distribution occurs through direct sales teams targeting large enterprises and a growing channel of system integrators who customize solutions for specific industries.

- These integrators are crucial for addressing the needs of regulated sectors, where they can ensure compliance and reduce integration errors by up to 25%. The final layer consists of end-user enterprises that adopt these platforms to enhance operational efficiency and drive innovation.

What are the Key Data Covered in this Low-code AI Platform Market Research and Growth Report?

-

What is the expected growth of the Low-code AI Platform Market between 2026 and 2030?

-

The Low-code AI Platform Market is expected to grow by USD 42.36 billion during 2026-2030, registering a CAGR of 33.1%. Year-over-year growth in 2026 is estimated at 27.6%%. This acceleration is shaped by proliferation of generative ai integration within low-code frameworks, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Platforms, and Services), Technology (Natural language processing, Machine learning, and Computer vision), Deployment (Cloud, and On-premises) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Platforms segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. North America is estimated to contribute 41.8% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is proliferation of generative ai integration within low-code frameworks, which is accelerating investment and industry demand. The main challenge is regulatory fragmentation and governance complexity globally, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Low-code AI Platform Market?

-

Key vendors include AgilePoint Inc., Appian Corp., Autonom8 Inc., C3.ai Inc., Caspio, Inc., CREATIO EMEA Ltd., DataRobot Inc., Google LLC, Huawei Cloud Computing Co Ltd, IBM Corp., Kissflow Inc., Mendix Technology BV, Microsoft Corp., Nintex Global Ltd., Oracle Corp., OutSystems Software Rede SA, Pegasystems Inc., Salesforce Inc., SAP SE and ServiceNow Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape is concentrated, with the top five vendors commanding over 60% of the market share by leveraging their extensive enterprise ecosystems. Major players such as Microsoft and Salesforce are embedding generative AI capabilities like Copilot and Einstein directly into their low-code platforms.

- These advancements allow organizations to build AI-powered applications with conversational interfaces, directly addressing enterprise demand for increased developer productivity and faster innovation cycles. For instance, the integration of AI co-pilots can automate over 40% of repetitive coding tasks.

- This strategic alignment of generative AI with low-code development is reshaping market dynamics, compelling all vendors to innovate beyond simple automation and offer more sophisticated, intelligent application development tools. The primary challenge remains ensuring robust security and governance as these powerful new capabilities are deployed at scale.

We can help! Our analysts can customize this low-code ai platform market research report to meet your requirements.

RIA -

RIA -